21 [easy] tips to Find the Best Mortgage Broker in Brisbane

Did you know that over 60% of Australian consumers now choose to get their home loan through a mortgage broker and that this is predicted to increase to 75% by 2024?

The facts don’t lie – for most property buyers, going through a mortgage broker is the smart choice.

But you need to make sure that you find the right broker. You want someone who will give you expert advice and make the home loan application process simple and stress-free.

In this expert-written guide you’ll learn everything you need to know about finding the best mortgage broker for you.

Let’s dive right in.

Don’t have time to read the whole guide right now?

No worries. Let me send you a copy so you can read it when it’s convenient for you. Just let me know where to send it (takes 5 seconds):

What does a Mortgage Broker do?

A mortgage broker is a type of financial adviser who will help you to find the right home loan.

They will compare home loans across multiple home loan providers (banks and other lenders) and find you a loan that is a best fit for your needs and financial situation.

Once you have found the right loan, a good broker will be there to guide you through every step of the process and get your loan approved as quickly as possible.

Are all Mortgage Brokers the same?

To be blunt – no, not all mortgage brokers are the same.

As with any profession, the quality of service you will get from mortgage brokers can vary widely.

There are a lot of great brokers out there providing a high quality service for their customers.

But unfortunately, there are also some bad brokers out there. Some mortgage brokers don’t really have your best interests at heart.

It can be hard to tell the difference between a good broker and a bad broker at first glance. The process of getting a home loan is complicated and has a lot of moving parts. If you’re not a finance expert, it’s easy for a bad broker to pull the wool over your eyes.

And there’s a lot at stake – for many Australians, purchasing a home is the single largest financial decision they will ever make. If you end up working with the wrong broker, it could end up costing you tens of thousands of dollars over the lifetime of your home loan.

It can also mean the difference between getting the home of your dreams and missing out completely.

Why is that?

These days, banks are much stricter with their lending criteria than they used to be. It has never been harder to get finance approved than it is now.

The “fast and loose” days of finance are well and truly behind us.

When you apply for a home loan in today’s lending environment, the banks will go through every single piece of documentation with a fine toothed comb.

They will check your live credit scoring, which means they’ll know if you’ve paid your bills (credit card, personal loan, home loan, etc.) on time over the past two years.

And they will go through your bank statements line by line, questioning everything. Even the smallest inconsistency could raise a red flag which would cause your application to be declined.

We have even seen cases where the banks will stalk you on Facebook to check on your relationship status!

The banks are so strict at the moment that we’re seeing an average rejection rate for home loans in Australia of 40%.

Now, more than ever, it’s critical to find a broker who will go the extra mile and give you the best chance possible to get your loan approved so you can buy the property that you’ve been dreaming of.

Finding the right broker makes all the difference. While the average brokers are seeing a rejection rate of 40%, a good broker will give you a much better chance of getting your loan approved.

Here at Hunter Galloway, our average rejection rate is less than 3%.

So how do you find a good mortgage broker?

There’s only one way to sort out the superstars from the sellouts – and that’s to do some due diligence on your broker so you can make sure you’re making the right choice.

As a director at Hunter Galloway, Brisbane’s Highest-Rated Mortgage Broker, I’m confident that we are the best broker for you.

But you don’t need to take my word for it. In this guide you’ll learn everything you need to know about finding the best mortgage broker for you.

I invite you to use these tips to evaluate our service and compare it with any other broker you’d like. I’m confident that you will find our service tops any others.

Understand the Difference Between a Good Broker and a Bad Broker

Before we get into the details, let’s start with a high-level view of things.

What does a good broker do?

A good mortgage broker will put your best interests first. A broker’s role is to essentially be a conduit between you and the banks. Rather than telling you what to do, they’ll actively do the leg work for you.

It starts with spending some time with you to understand your needs and requirements. From there, they will work out exactly how much you can afford to borrow across a number of different lenders.

If they come across any issues that could prevent you from being approved for a loan, they will work with you to resolve those issues, or find you a lender who is willing to work with you.

They will find you a number of different home loan options and explain how each loan option works, including the costs associated with them.

If you decide to go ahead with a loan application, they will help you to apply for the home loan and manage the process all the way from pre-approval to settlement.

If you’re not ready to buy a home right now, a good broker won’t leave you high and dry – they will provide you with the tools and educational material you need to help you get ready.

Once your home loan is settled, they will perform regular checks to make sure you are getting the best available rate. If you’re not on the best rate, they will help you to refinance your home loan when the time is right.

What does a bad broker do?

A bad broker doesn’t really care about you. To them, you are just a number. They will do the minimum amount of work possible to get as much money out of your home loan as they can.

A bad broker will not take the time to understand your unique situation. They will pretend to listen to your needs, but they won’t have your best interests at heart when they make their recommendations.

They might push you into getting a loan that is too big – great for them, because they get a higher commission, but bad for you because you can end up with a loan that you can’t afford.

They might submit your loan application without taking the time to ensure that you have a high chance of getting approved.

Instead of offering you a loan that is suited to your goals and priorities, they will railroad you into getting a loan that offers them the biggest commission.

To be fair, not all brokers are so sinister. Some brokers are bad not because they are focused only on the money, but because they are inexperienced or disorganised.

But these brokers are just as bad – if your broker is inexperienced, they might not be able to find a suitable loan for you, simply because they don’t understand the policies of all of the different lenders.

And if they are disorganised, your loan could be declined because they missed some important information in your application, or they missed an important deadline.

Whatever the reason, you want to avoid working with a bad broker at all costs.

In the rest of this guide, we’ll dive into the details of how to sort the good brokers from the bad.

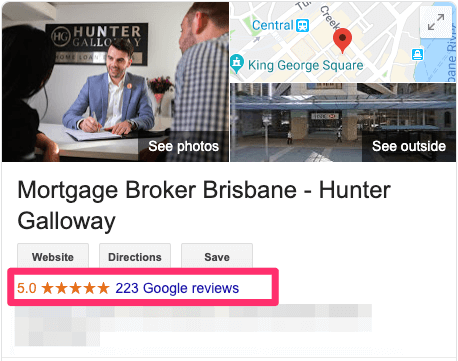

Research the Broker’s Online Reviews in Brisbane

The first thing you should do when looking for a Mortgage Broker is jump online and check their online reviews. Reading past reviews from their customers should give you an idea on their level of customer service and competence which should help you find the best mortgage broker in Brisbane.

We recommend looking at reviews on the following sites:

If your broker has a 5-star average rating, that’s a great sign. But it’s important to dig a little deeper.

Take a few minutes to read some of the reviews. Make sure that the reviews look real. Some brokers might use fake reviews to artificially inflate their ratings. But usually it’s pretty obvious which ones are fake and which ones are real.

If there are any “middle of the road” reviews (2,3, or 4 stars) take special note of these. They can give you an indication of how the broker handles customers when things don’t go smoothly.

1 star reviews are also worth looking at, but we recommend taking these with a grain of salt. 1 star reviews are often left by disgruntled customers and may not accurately reflect the business.

At Hunter Galloway, we are proud to have over 300+ Google Reviews, and 30+ Facebook reviews from our happy customers! Our team can arrange a free assessment to see what your home loan options are.

Finding the Best Home Loan in Brisbane can be as simple as looking for the best mortgage broker reviews on Google. At Hunter Galloway, we are Brisbane’s most Reviewed Mortgage Broker with over 300+ Google Reviews.

Check the Mortgage Broker’s Credentials

You should also check the broker’s credentials before contacting them about your home loan. Here are the credentials you should check:

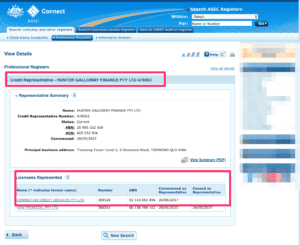

Are they registered with ASIC?

Mortgage Broker’s in Brisbane are required to have a Credit License, or be a Credit Representative to operate.

You can see if they are members on the ASIC Register portal. We are Credit Representatives 401688 authorised under Australian Credit Licence 389328.

Checking the ASIC portal can show if your mortgage broker holds the correct licenses to operate.

Are they a member of a professional broking organisation?

While it’s not a legal requirement that a mortgage broker is a member of an industry organisation, it is a requirement for many lenders and mortgage aggregators.

Your broker should be a registered member of either the Mortgage and Finance Association of Australia (MFAA) or the Finance Brokers Association of Australia (FBAA).

These associations ensure the professionalism of the best mortgage brokers across the country.

In order to maintain their membership with the MFAA or the FBAA, brokers need to undertake a certain amount of continuing education. This make sure the brokers keep up to date on the latest policies and compliance procedures.

If your broker isn’t a member of the MFAA or FBAA it should be considered a red flag as they could have been made to leave the industry due to issues in the past.

If you can’t find them on their membership lists, make sure to ask them if they are registered with the MFAA or FBAA when you speak to them.

Are they part of an ASIC-approved external dispute resolution scheme?

Mortgage Brokers in Brisbane need to be a member of the Credit & Investments Ombudsman (CIO) or the Financial Ombudsman Service (FOS). These external dispute resolution schemes (EDRs) provide a way to resolve any disputes between borrowers and lenders.

If your broker is not part of either of these schemes, tread very carefully as you may have some problems if you need to make a complaint about your home loan.

See if They Have Won Any Awards

Industry awards are another indication that the broker you’re looking at is a top performer.

The Finance Brokers Association of Australia (FBAA) and Mortgage & Finance Association of Australia (MFAA) both give awards to brokers based on their reputation and performance.

At Hunter Galloway, we have built a brilliant reputation for being extremely well organised, helpful and making the home loan process as smooth as possible.

Some of our achievements include:

🏆 Finance Brokers Association of Australia National Finance Broker of the Year 2019

🏆 Finance Brokers Association of Australia National Finance Broker of the Year 2018

🏆 Finance Brokers Association of Australia Broker of the Year 2018 (Queensland)

🏆 Finance Brokers Association of Australia National Finance Broker of the Year 2017

🏆 Finance Brokers Association of Australia Broker of the Year 2017 (Commercial)

🏆 Finance Brokers Association of Australia Broker of the Year 2017 (Queensland)

🏆 Vow Financial Rising Star of the Year 2016 (Queensland)

🏆 Bankwest New Support of the Year 2015

🏆 Finalists at the Australian Mortgage Broker awards in 2017.

🏆 Our Director Nathan Vecchio was named in The Adviser’s Top 5 Brokers in Australia under 30 for 2017

We are also regularly featured in The Adviser, Mortgage Professionals of Australia and other mortgage industry publications.

Take a Look at Their Blog and Educational Resources

The finance world is complicated and constantly changing. It can be hard to stay on top of things as a finance professional, let alone as a home buyer.

That’s why a good broker will have a wide array of educational material available for their customers to make sure they are as well-informed as possible.

Check your broker’s website and other online channels (such as Facebook and YouTube) to see whether they offer any training material for their customers.

At Hunter Galloway, we strongly believe in educating our customers. That’s why we have spent countless hours creating educational materials to help you to achieve your goals of buying a home.

Here are some of the material you can check out:

- ✅ Our Blog (what you’re reading right now)

- ✅ Hunter Galloway’ YouTube Channel

- ✅ Finance in 5 – A weekly finance newsletter

- ✅ Home & Hosed – A course for first home buyers

- ✅ Home & Hosed: Three Simple Steps to Buying Your First Home (Book)

Make sure to take a look at your broker’s website and see if they do the same.

Explain Your Needs

There are hundreds of different loan products available on the market. Each loan product has different interest rates, features, and fees. Choosing the right home loan depends on your broker getting a deep understanding of your goals and priorities.

When you speak to a mortgage broker for the first time, they should start by asking you about your financial situation and borrowing needs. If not, be careful because they might be more interested in their wallets than your financial health.

Here are some things to think about:

What are you looking at doing?

Are you buying a home? Building a home? Refinancing your existing mortgage? Or maybe you’re looking to renovate?

What kind of loan are you looking for?

Are you interested solely in the lowest interest rate possible? Or do you want to pay down your mortgage as quickly as you can? Are you planning on living in this property for several years, or are you looking to turn it into an investment or upgrade to a new property within a couple of years?

Having a clear idea on this, and explaining your needs to your mortgage broker can make sure you get the best results.

Read More: First Home Buyer Information

Ask Them Why You Should Choose Them Over a Bank

Once you’ve explained your needs to your mortgage broker, ask them this question: “Why should I choose you over a bank?”

Their answer will tell you a lot about how they perceive themselves, what areas they specialise in, and what value they add to the home loan process.

Here are some of the reasons why we recommend using Hunter Galloway over a bank:

- ✅ We can find you the best loan options across a panel of over 30 lenders – banks can only offer you a limited number of options based on their own products.

- ✅ We are always on top of the latest developments in the mortgage market and what different policies are available for you to take advantage of (for example 90% no LMI loans for pharmacists or medical professionals).

- ✅ Our internal credit team will thoroughly analyse your application to make sure we resolve any issues before the bank sees your loan application, giving you the best chance of a successful application.

- ✅ If you are looking to refinance, we are able to negotiate significant discounts with your existing bank because the bank knows we can find you a loan somewhere else.

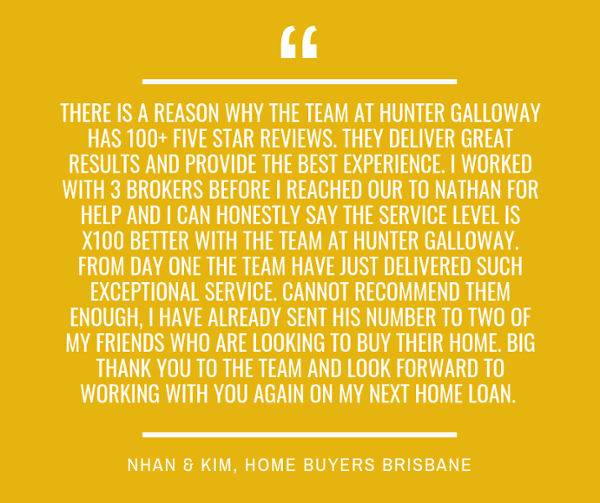

![]()

Looking at Reviews & Testimonials from your mortgage brokers existing clients can help understand who, and how they help.

Looking at Reviews & Testimonials from your mortgage brokers existing clients can help understand who, and how they help.

Determine Their Experience

In finance experience counts for everything.

If you’re working with an inexperienced broker, they might tell you that you don’t qualify for a loan because they don’t have a thorough knowledge of the lending policies of the banks. Or they might find you an inferior home loan.

An experienced broker will know the lending policies of the banks inside and out. That means that you have a better chance of qualifying for a loan, and of finding a product with a better rate.

Ask your mortgage broker how long they have been in the industry for.

Have they had banking experience previously or are they completely fresh to the industry?

This gives you a good sense of their background and if they are suitable to help you in your situation. You can even go one further and ask if they own property? Knowing they have sat on the other side of the fence can help give you some confidence they will be able to help you navigate the home loan process quickly and easily.

Here are some questions you can ask them:

|

These questions will give you an understanding of their background, where they’ve come from, and what they have done.

At Hunter Galloway, our Mortgage Brokers have a combined 30+ years of industry experience. With their experience, they know the mortgage industry inside and out. They all own multiple properties and can help to make navigating the home loan process easy.

Our team has its own internal Credit Manager who reviews each application before being submitted to the lenders, meaning we won’t apply with a lender who won’t approve your loan.

Read More: 10 [simple] Tips for Choosing the Best Home Loan in Brisbane

The Hunter Galloway Mortgage Broker Brisbane team is here to help. We have a team of home loan experts.

Ask Them Their Net Promoter Score (NPS)

The net promoter score is a metric used across many industries to measure the overall happiness of customers.

Any broker who is dedicated to delivering the best possible customer service will track their NPS so they can make sure they are doing everything they can to keep their customers happy.

When you’re talking to your broker, ask them about their NPS score. Specifically, ask them these questions:

- Do you track your net promoter score? If so, how do you track it, with what software?

- What is your current net promoter score?

The higher the NPS score, the more satisfied their customers are.

On average, brokers have a Net Promoter Score in excess of 70.

Here at Hunter Galloway, our NPS score is 88.

To contrast this, major banks will often report a negative NPS, with the highest scoring in the low 50s.

Request Their Lender Panel

There are over 50 banks and other lenders who offer home loan products in Australia, but brokers can’t offer home loans from every lender. They are restricted by the list of banks they can access. This list is known as the “lender panel”.

The majority of accredited mortgage brokers have at least 20 different lenders and bankers they can utilise to help give you the best home loan but some have as few as 9 banks on their panel.

If a broker has one a small number of banks on their panel, it can be a red flag that suggests they are focusing on a small number of lenders which could limit your options (and your ability to get a home loan).

It’s important to know which lenders are on your broker’s panel and which aren’t — and importantly, why?

In some cases, a broker might not have access to a lender due to volume requirements, where a broker doesn’t do enough business. For example theCommonwealth Bank (CBA) requires brokers to submit a minimum amount of home loan applications per year to maintain their accreditations.

Having a large range of lenders ultimately gives you more options and more choice! At Hunter Galloway, we have over 30 Lenders to choose from!

Ask About Their Home Loan Research Process

A large part of the broker’s job is to research which loans are suitable for you across the hundreds of loan products offered by the different banks and lenders.

Ask your broker how they will decide which loan will best suit your needs.

Do they have a robust process they use to search across all of the different loans? Or is their home loan research less organised, more off-the-cuff?

If they are saying they will just find you the lowest rate possible across the different banks, you will need to ask more questions.

Everyone wants the lowest interest rate possible, but what you’re really looking for is the lowest interest rate possible that also satisfies your other needs and requirements. A low-interest rate loan might seem cheaper up front, but you might end up spending more in the long run if the loan isn’t suitable for your unique financial goals.

For example, at the moment the lowest interest rates available are from fixed-rate loans. But if you’re looking to make extra repayments or you might end up selling the property within the fixed-rate period, you could attract additional fees which can add up to a significant sum.

In addition to this it’s good knowing their process and what goes on in the background to get your loan approved – do they have other team members or support staff? Do they outsource their loan processing to an offshore company, or do they do all of their own work in house?

If they are a one-person brokerage, what happens if they get sick, or take holidays – will your loan still get processed? It’s always good to know they have a team working in the background to make sure you not only get the best deal, but you are also looked after in the process.

Here at Hunter Galloway, our four brokers are supported by a team of two Mortgage Experts and six Credit Analysts, all working out of our office.

Find out your mortgage brokers research process. At Hunter Galloway, we have a team of Home Loan Experts.

Question What Mortgage Features You Need

Features and add ons can be an enticing part of buying something. Just like cars and coffee machines, home loans are also filled to the brim with features and optional add-ons.

But these features come at a cost. If you’re not going to use those features, then you’ll be wasting money.

Speak to your broker about features like extra repayments, redraw facility and offset accounts. And if you’re unsure about what any of these are, find out what they mean for you and which ones will help you.

Each situation is unique, and this will impact which features are best for you.

And, if you’re preparing for changes like a new baby on the way, going on maternity leave or renovations, you’ll need to keep this in mind as it will be able to help you figure out which features are most important and relevant to you.

Read More: Extra Home Loan Repayment Calculator

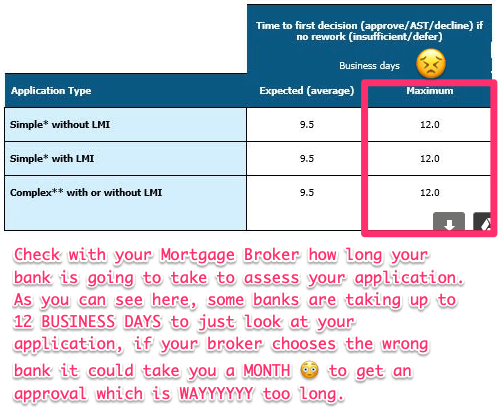

Question their Turn Around Time

You also want to ask your broker how fast they can turn around your mortgage application.

Your broker’s ability to get a quick turn around could make or break your first home purchase.

Like we mentioned in the last point, many Mortgage Brokers in Australia are one man bands, in other words they do not have any additional staff and if they are sick or away your home loan application can sit on your brokers desk not progressing.

Other brokers utilise an offshore company to aid their loan processing. This isn’t necessarily a bad thing, but it can introduce some delays in your turn around time.

Equally if you have Signed a Contract of sale subject to 14 days finance, you don’t want to risk losing the property if the broker can’t get your loan approved in time.

You also want to ask the broker what the bank you are applying with’s turn around time is, because some banks are known to be notoriously slow with processing loan applications.

In fact, we’ve heard stories of banks taking 12 business days – In other words, almost 3 weeks – to get a loan approval 😳. This is not workable for most purchases.

At Hunter Galloway, our Mortgage Brokers will be upfront with you and give expected turn around times at all stages of the home loan process and we will return all phone calls within 4 business hours.

We have very good contacts with the State Managers and Senior Management at most banks and can get things turned around much quicker than the average broker – infact our average home loan application is formally approved in under a week.

If it is going to take your broker more than a few days to get your home loan approved, then speak with our team to see how we can help you out much faster than regular mortgage brokers.

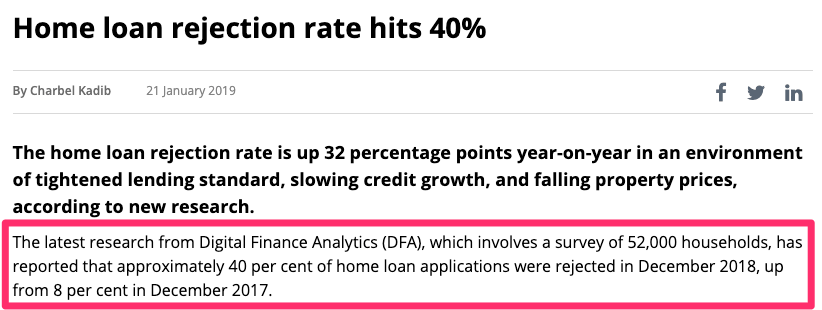

Ask Their Mortgage Application Approval (And Rejection) Rates

While broker’s can help you negotiate interest rates, an even more important function is actually getting your loan approved in the first place!

This is because getting a home loan has gotten much more difficult in 2019 in light of the Royal Commission and Banks tightening their credit criteria.

According to research completed earlier in the year, the home loan rejection rate hit over 40%.

In other words, earlier this year 4 in 10 home loan applications were being knocked back or declined.

Ask your Mortgage Broker what their approval rates are, and on average how many applications they have had declined in the past 12 months.

We take the time up front to understand your situation, what you are looking to achieve and then find a bank that fits with you.

Before your application gets to the bank, our internal Credit Team thoroughly reviews every application to make sure that there aren’t any issues that could cause your home loan to be rejected.

Thanks to this approach we have helped over 639 home owners in buying a house in the past 12 months, and our Mortgage Application Approval rate is over 97.5%.

Don’t risk having your home loan declined, get in touch with our team today to see how we can help get your Home Loan Approved.

Ask About Commissions

In general, mortgagebrokers get paid a commission from the bank that gives you your loan. That’s how we are able to offer our services free of charge to you.

In some cases, mortgage brokers will charge you a fee for their services. This typically happens with commercial loans or development finance, but it’s always best to know up front what you’re getting into so there aren’t any surprise fees later down the track.

When you get a home loan with us, we will tell you exactly how much commission we will be earning from your bank.

The commissions paid by banks do vary slightly between banks, which could be a potential conflict of interest. Rest assured that we put your own best interests before our own – it’s far more important to us that you get the best possible home loan than to earn a slightly higher commission.

Make sure that your broker is open and transparent about their fee structure. If you’re concerned they might be offering you a home loan solely based on the commission they can earn, ask them to explain why this particular loan is best for you.

At Hunter Galloway, we do not charge any additional fees for our service.

We are paid commissions by the banks so our services do not cost anything to you.

Check Their Ownership Structure

Ask your broker who owns them. Are they independently owned? Or are they owned or part-owned by one of the big banks?

Brokers who are not independent may have a significant conflict of interest – they are incentivised to sell you loans that flow straight back to the bank that owns them.

This might not be obvious at first glance – some brokers will offer “white-label loans”. These loans are branded with a different name, hiding the fact that they are actually a loan from one of the big banks.

That’s why it’s important to ask up front. You want to make sure that your broker is offering you a loan based on what’s best for you, not what’s best for lining the coffers of their parent company.

Ask About Home Loan Rebates

From time to time there are home loan rebates and specials available from mortgage lenders including cashback deals.

Lenders can offer up to $2,000 in cash back rebates and rewards after a loan has been refinanced.

Talk to a mortgage expert and see if you qualify for cash back rewards and rebates.

Check Their Communication Skills

After speaking with your broker, assess their communication skills. A good broker should be able to explain the complicated loan terms and processes in simple, easy to understand language.

They should be able to present you with a number of different loan options and clearly explain their reasons for recommending specific loans.

A good broker will also have good listening skills. If they start bombarding you with your loan options before you’ve even had a chance to explain your goals and priorities, this is a big red flag.

If your broker isn’t listening to you, there’s a good chance they are more focused on the commission you represent than getting you the best outcome. You might end up with the wrong loan.

Finally, take note if you feel pressured by the broker at any stage during the process of getting a home loan. As mentioned earlier, a good broker is a conduit between you and the banks – they will do the leg work to find your loan options for you and give you guidance, but they will not pressure you into choosing a specific loan. Brokers are not dictators.

Make Sure They Are Organised

There are a lot of moving parts in the home loan application process. As your application progresses, it will change hands multiple times. There are often follow-up requests from the banks that need to be managed, and extra documentation that needs to be supplied.

On top of this, brokers are dealing with multiple clients and applications on a daily basis. With so many balls in the air at once, if your broker isn’t organised there is a good chance they might make a mistake somewhere along the line.

If they drop the ball on your home loan application, you might miss out on your property purchase entirely.

As you interact with your broker, take note of their behaviour and the way they handle your loan application.

Are they regularly late to meetings? Do they return your calls? More importantly, is your broker proactively contacting you to keep you in the loop as your application progresses?

Do they seems to have a well structured process in place, or are the “shooting from the hip”?

A good broker will have systems and processes to make sure that nothing is missed, and that you are kept informed.

Don’t Make Too Many Applications

It’s perfectly fine to talk to multiple brokers to find someone that is a good fit for you before applying for a loan. But you should never submit multiple loan applications with multiple lenders.

Making too many home loan applications can affect your credit rating. This can cause your loan to be declined.

This goes for pre-approvals as well – too many pre-approvals in a short time can also put a dent in your credit score.

Be wary if your broker is pushing you into a pre-approval too quickly. Some brokers will use a pre-approval as a way to lock you in as a client – it’s much harder to switch if you’ve already got a pre-approval.

Here at Hunter Galloway, we will only recommend a pre-approval when you’re at the stage where you’re ready to buy within the next three months.

That keeps your options open if a better deal comes along and reduces the risk of affecting your credit score.

If you want a pre-approval in order to know your borrowing capacity, we have a better option for you.

We have developed an in-house “Home Buying Potential” report that gives you all of the information you need to feel comfortable moving forward with a home purchase without needing to go through the pre-approval process.

This internal assessment process is more detailed than many lenders’ pre-approval processes. It’s faster, takes less effort, and still gives you the confidence to get out there and start your home buying journey.

Get All Details In Writing

Always ask for written recommendations and get information on commissions, fees and products in writing.

A broker is legally obliged to follow responsible lending laws and shouldn’t sell you an inappropriate or risky loan. They are required to document your financial situation along with your financial needs and priorities.

Make sure your broker provides you a copy of their credit assessment and double check that what your broker told you matches up with what’s on paper.

ASIC recommends, a written agreement should tell you the type of loan being arranged for you, the amount of the loan, the term of the loan, the current interest rate, and any fees you have to pay. The fees could include broker’s fees or commissions, fees to the credit provider or lender for setting up the loan, and/or any early termination fees.

Your mortgage broker should always provide credit advice in writing.

Slow Down And Don’t Rush

If you’re trying to get a home loan on a tight deadline, you may be tempted to get your home loan sorted out ASAP and rush through the process.

But even if you’ve got a deadline breathing down your neck, it’s important to take the time to fully understand what you’re getting into and make sure you’re comfortable with what you’re signing.

You should never sign a blank form or leave details for the broker to fill in later.

Don’t sign anything unless you fully understand what it is. If you aren’t sure about what you are signing get independent legal advice.

And don’t let a broker pressure you into signing too quickly. Remember that the broker is supposed to help you through the home loan process, not force you through it.

If you’re feeling pressured by your broker, ask for more time to think about the loan. If they persist in pushing you to sign even if you have asked for more time, then go to another broker.

Read More: Home Loan Guide to Brisbane

Finding the best mortgage broker in Brisbane is as simple as following these steps.

Finding the best mortgage broker in Brisbane is as simple as following these steps.

Don’t Risk Being Declined

Did you know that in 2018 over 40% of home loan applications that get submitted never make it to settlement? Don’t take that risk.

Our Mortgage Brokers have seen all sorts of mistakes in the past!

With their level of experience, they know problems you may face on your loan application and how to mitigate them when applying with a specific bank or lender. We have a wide range of lenders on our panel and our brokers intimately understand their credit policies.

We can do this through our own internal credit assessment process which we complete before applying with any lender.

Our team has its own internal Credit Manager who reviews each application before being submitted to the lenders, meaning we won’t apply with a lender who won’t approve your loan.

Our Mortgage Brokers have helped lots of home owners around Paddington and Brisbane.

Our Mortgage Brokers have helped lots of home owners around Paddington and Brisbane.

Read More: Loan Declined After Pre-approval, 26 ways to get approved!

Understand How to Complain

ASIC reccomends if you have a complaint about a broker or a dispute you can’t resolve, find out how to complain or phone ASIC’s Infoline on 1300 300 630.

Your mortgage broker should always provide copies of the following, which will outline how their complaints process.

Read More: Property Market Research | 12 Steps to Research a Home in Brisbane

What does this all mean in short?

As I mentioned at the beginning of the post, there’s a reason more Australians are using brokers over banks for their home loans.

If you have the right mortgage broker on your team, applying for your home loan will be a breeze.

A good broker will find you the best loan for your needs, manage the complexities of the home loan process, and make sure you have the best chance of getting your home loan approved.

Follow the recommendations above and you will be able to make sure that you have all of the information you need to make the right decision.

Next Steps

If you’re looking to buy a home within the next 6 months, it’s time to start talking to brokers.

You can ask your friends for recommendations, search on Google, or better yet — arrange a free assessment with one of our friendly mortgage brokers here at Hunter Galloway.

We’ve helped hundreds of people just like you to find the best home loan. Our focus is on taking the stress out of the home loan process.

With our team of experts, we help you navigate over 30 lenders, taking care of the details and finding a mortgage solution that works for you.

With a 5-star rating from over 150 reviews across Google, Facebook, and Product Review, you can rest assured that we will deliver outstanding customer service and take care of you every step of the way.

Click on the button below to book a free, no-obligations phone call to see how we can help you on the next step of your home buying journey.

1300 088 065

1300 088 065

Start again

Start again