Variety of options due to direct access to 30+ Australian banks & lenders

Highest-rated Mortgage Broker in Brisbane — 2,400+ Google reviews

Free for you, and you won't pay more — the lender pays us

35+Years of

experience

Based on

2,400+ reviews

Mortgage Broker of the Year in 2017, 2018, 2019 and 2024

Access to 30+ banks and lenders in Australia

Thousands of families helped into their homes

*Based on all applications processed through Hunter Galloway, 2024–2026.

Home Loan Extra Repayment Calculator

Did you know that despite 2025’s rate cuts, over 85% of Australian borrowers chose not to lower their repayments?

While the RBA has cut the cash rate three times this year (bringing it to 3.60%), the vast majority of homeowners have kept their direct debits high. Why? Because whether it is a consistent $50 a month or a one-off tax refund lump sum, attacking your loan principal remains the only guaranteed, tax-free return on investment—currently saving you approx. 5.5%–6.0% in interest costs.

An extra $50 per month is roughly the cost of one takeaway coffee a week. Ask yourself: Is skipping one coffee a week worth gaining 7 years of mortgage freedom? Most people would say yes in a heartbeat.

In this guide, written by an expert mortgage broker in Brisbane, we break down the math of regular vs. lump sum payments and reveal the ‘Repayment Recalculation’ secret—a manual request you must often make to unlock lower minimum monthly payments after a lump sum deposit.

How Does Compounding Interest Work?

Compound interest is the secret source that makes your bank account grow over time or your debt balloon if you’re not careful. Simply put, it is interest on interest.

Say you put $1,000 into a savings account that offers a 10% interest rate. After the first year, the balance would be $1,100 — your initial $1,000 plus $100 interest. But this is where the magic of compounding interest kicks in; in the second year, you don’t just earn interest on the initial $1,000; you earn on the whole $1,100. So, at the end of the second year, you’ll have $1,210. In the third year, you’re looking at $1,331. That is the power of compound interest.

Now, what if you’re on the borrowing side of the equation? The mechanics of compound interest work in the same way, but it’s just not so much in your favour. If you borrow $1,000 at a 10% annual interest rate and make no repayments, the same compounding effect happens — after one year, you owe $1,100; two years, you’re in the hall for $1,200; three years, you’re looking at $1,331 in debt. That’s compounding interest for you, a powerful tool when you’re saving, but it’s a necessary evil if you’re looking at borrowing to buy a home.

Now that we understand compounding interest let’s move to the real question – How much can I save by making extra repayments on my loan? How can you beat compound interest when you’re dealing with a mortgage? The simple answer is to power off your loan as quickly as you can.

Does Increasing My Home Loan Repayment Make Much Difference?

Paying an increased amount on your home loan will help you repay the loan much faster.

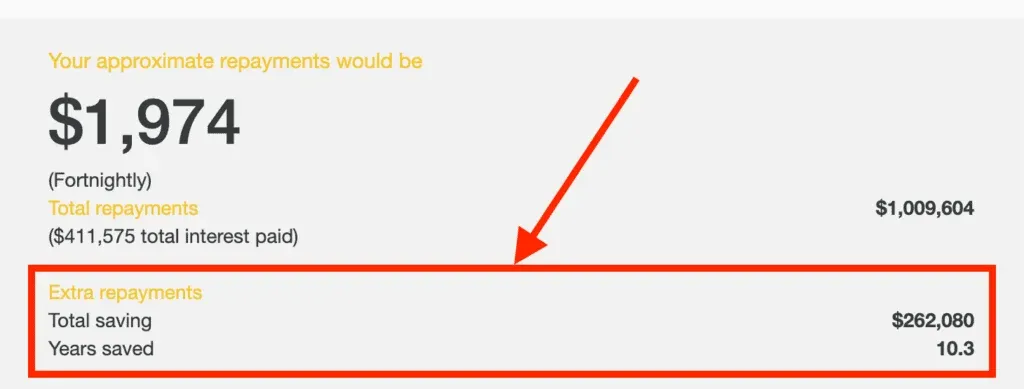

For example, Charlotte has a $600,000 loan and wants to make an extra $341 per fortnight on top of her existing fortnightly home loan repayment, paying a total of $1,974 each fortnight.

Incredibly, this will take 10 years off Charlotte’s 30-year home loan term and $262,060 in interest costs!

Why You Should Make Extra Repayments On Your Home Loan

For every dollar in extra repayments you make, it will be one dollar less in interest you will need to pay. So, the first reason is getting your interest costs down, but that isn’t the only reason you should be making extra repayments on your home loan.

In paying down your loan, you are also increasing theequity in your property, meaning you will own more house than debt.

Homeequity is calculated as the difference between the value of your home minus the loan. So, if you owed $310,000 to the bank, and your house was worth $501,000, your home equity would be $191,000 ($501,000 minus $310,000).

Making extra repayments will also help you build a buffer of savings that will accumulate in your loan and be there should you ever need them.

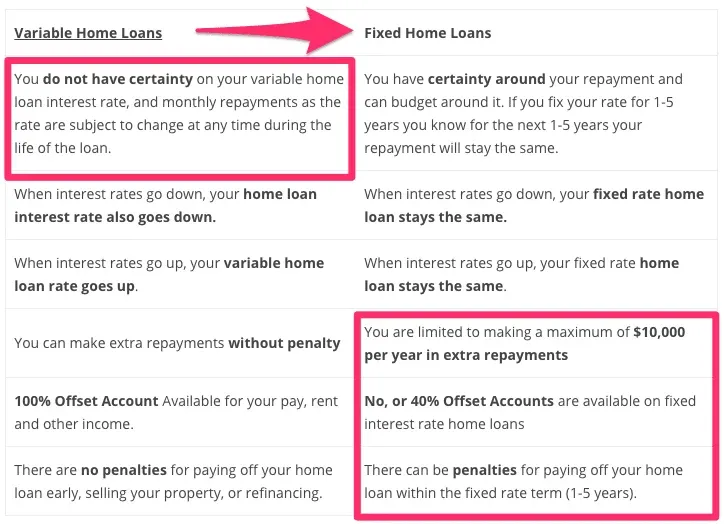

If you have avariable home loan rate, you can make as many additional repayments as you would like.

On the other hand, if you have afixed-rate home loan, there might be limitations on how much you can make in additional repayments.

Some banks will allow you to make up to $10,000 per year in additional repayments, while others will not allow any additional repayments during the fixed rate period. If you would like us to check what your bank’s requirements are,get in touch, and we will confirm.

Fixed-rate home loans are great for people who want stability and to know what their repayments will be over a set period, but they aren’t great if you are looking at making extra loan repayments.

We love extra repayments, but if you have a fixed-rate home loan, you need to be careful. Unlike variable loans, fixed-rate mortgages come with strict rules.

Most Australian banks place a “cap” on how much extra you can pay off each year.

The Cap: Typically, you can only make between $10,000 and $20,000 in extra repayments per year during the fixed term.

The Penalty: If you pay even $1 over this limit, you may trigger a “Break Cost” (also called an Economic Cost).

This fee can be thousands of dollars, wiping out all the interest savings you worked so hard to achieve.

Why do banks charge this?

When you fix your rate, the bank buys that money at a specific price from the wholesale market for a set time (e.g., 3 years). If you pay it back early, you “break” their funding contract, and they pass the cost on to you.

The Workaround: How to Pay Extra Safely

Don’t worry; you can still get ahead without getting fined. Here are two insider strategies:

The “Split” Strategy: Consider splitting your loan (e.g., 80% fixed, 20% variable). You can then dump unlimited cash into the variable portion without penalty.

Wait for the Expiry: Save your extra cash in a high-interest savings account or Term Deposit. Once your fixed term expires, dump that lump sum onto the loan before you fix it again.

Pro Tip: Some lenders (like Adelaide Bank or Great Southern Bank) offer 100% offset accounts on fixed-rate loans. If you are one of the lucky few with this feature, you can save as much as you want in the offset account without triggering a break cost!

What Counts As Extra Repayments On A Home Loan?

When you take out a home loan, you will be given a contracted term, which generally ranges from 25 to 30 years.

In other words, the bank will calculate what your principal and interest repayments should be each month for the next 25 to 30 years using something called an amortisation schedule.

Using the loan amount, interest rate and loan term, the bank will determine your monthly payment from today until it is fully repaid in 30 years’ time.

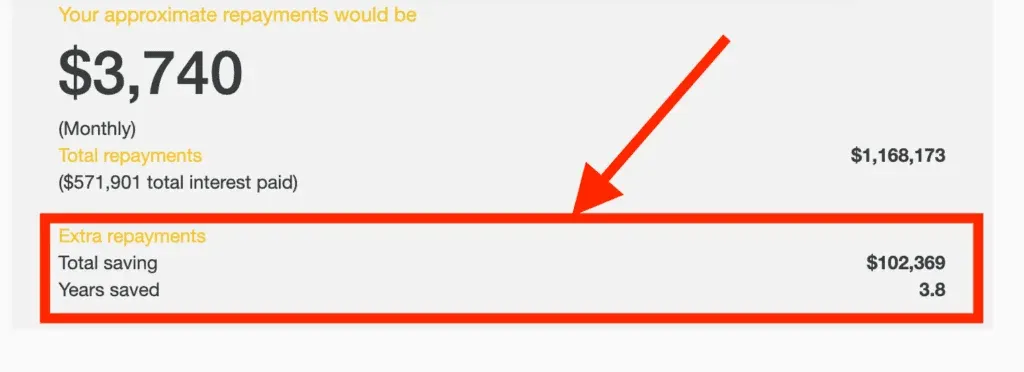

In this example, if John took a mortgage of $600,000 today at a 5.85% interest rate and made his minimum repayments of $3,540, it would take him 30 years to completely repay the loan. Over this period, he would pay $674,270 in interest to the bank!

If he started making an extra $200 per month in repayments straight away, his loan repayments would be increased to $3,740 per month, and by making this small difference, he would save 3 years, 9 months from his loan term AND $102,369 in interest costs!

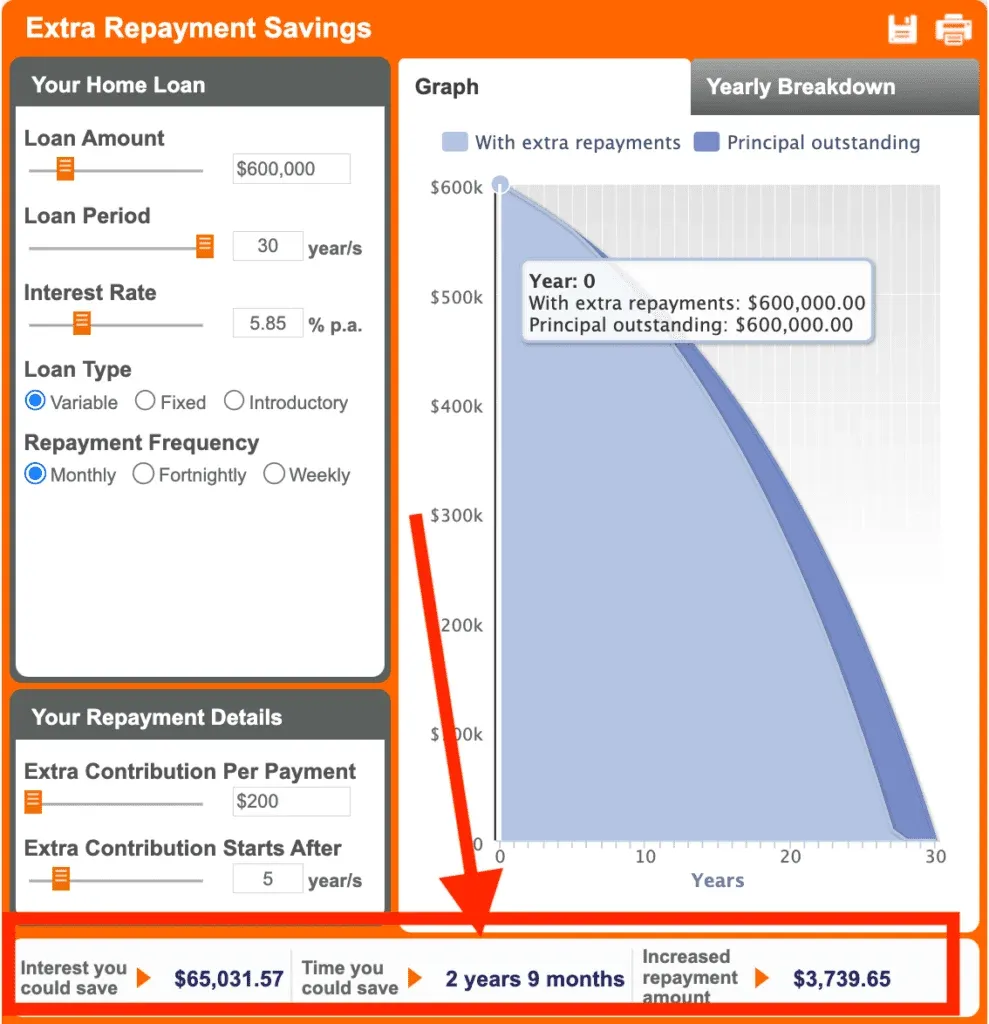

Even if you’ve had your loan for a few years, it isn’t too late to start making extra repayments. For example, if John had his loan for 5 years and only then started making an extra $200 per month in repayments, what would the difference be?

By starting to make extra repayment contributions after 5 years of $200 per month, he would still save 2 years and 9 months from his loan term AND reduce his interest costs by $65,031!

The Power Of One-Off Lump Sum Repayments

You don’t always need to increase your weekly budget to get ahead. The ‘Windfall Strategy’ is a powerful alternative for savvy homeowners. This involves using one-off cash injections to smash your loan balance whenever you have spare funds.

Think of it as a shortcut to financial freedom.

How the Math Works in Your Favour

In the early years of a mortgage, most of your standard repayment goes purely toward paying off interest. Very little actually reduces your debt.

A lump sum repayment changes the game completely. Because your interest is covered by your minimum repayment, 100% of your lump sum attacks the principal debt immediately.

This stops interest from compounding on that specific amount for the remaining life of the loan. Reducing the daily interest charge instantly creates a snowball effect that strips years off your mortgage.

Example: The Tax Return Power Move

Let’s look at the numbers to prove it.

Imagine Sarah gets a $3,000 tax return in Year 2 of her mortgage. Instead of spending it on a holiday, she throws it onto her $500,000 loan. That single decision saves her over $9,000 in interest over the life of the loan.

She essentially tripled her money just by clicking “transfer” once!

Where to Find Lump Sums

You might be surprised at how often you receive unexpected money.

Common opportunities for Australian homeowners include:

Tax Returns: Use your refund to secure your future.

Work Bonuses: Put performance bonuses straight into the loan.

Inheritance: Even small cash gifts make a difference.

Asset Sales: Selling a second car, boat, or unused electronics.

Every dollar you deposit today saves you multiple dollars in future interest.

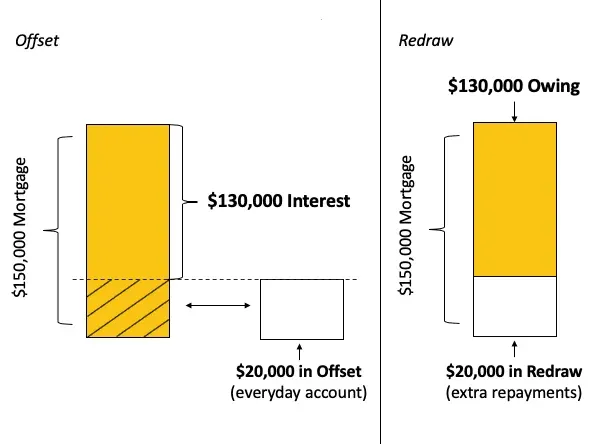

Is It Possible To Use My Offset Account To Make Higher Payments?

Ahome loan offset account helps you reduce interest costs because every dollar in your offset account reduces your home loan balance by the same amount. So, additional repayments to youroffset account will have the same effect as an extra repayment!

If you can be careful with your money it can be better to make the extra repayments into your offset account because it can be easier to access the funds compared to redraw.

But at the end of the day, an offset and redraw account do the exact same thing.

As you can see from the example above, if you had $20,000 in the offset account (or in redraw), it would reduce your home loan balance by $20,000, which means you are paying interest on a lower amount.

In this case, you would only pay interest on $130,000 (instead of $150,000)!

If you aren’t using an offset account, you canchat with our team of home loanexperts to see if it would be beneficial for your situation and how much faster it could help you pay off your loan.

Most people assume that paying extra on their mortgage automatically lowers their next monthly bill. Surprisingly, this is rarely the case. Banks typically have a “default” setting that prioritizes paying off your debt faster rather than improving your cash flow today.

The Default vs. The Choice

When you make extra repayments, most lenders keep your minimum monthly direct debit exactly the same. Because your loan balance is lower, less interest is charged each month.

Since your repayment amount hasn’t changed, more of that money goes toward smashing the principal debt.

This is fantastic for paying off your home loan years early. However, it does not help if you need extra cash in your pocket right now.

How to "Recalculate" Your Loan

If you have made significant extra payments and need to improve your monthly budget, you have a choice.

You can ask the bank to lower your required minimum repayment. This process is often called “recalculating” the loan.

They effectively look at your new, lower loan balance and spread it out over the remaining loan term.

Action Step: How to Lower Your Monthly Bill

If you need better cash flow, don’t just sit there waiting for the bank to act. Call your lender today and ask this specific question:

“Can you please recalculate my minimum repayments based on my new lower balance?”

Most lenders will adjust your direct debit down, putting extra cash back in your pocket every month.

The Trap: Cash Flow vs. Interest Savings

Before you make this call, understand the trade-off.

Lowering your repayment reduces the “interest-saving” power of your extra payments.

By dropping your repayment, you slow down the speed at which you are paying off the principal.

Keep repayments high: You save maximum interest and become debt-free sooner.

Lower repayments: You get better monthly cash flow but pay more interest over the long run.

Choose the option that fits your current financial goals best.

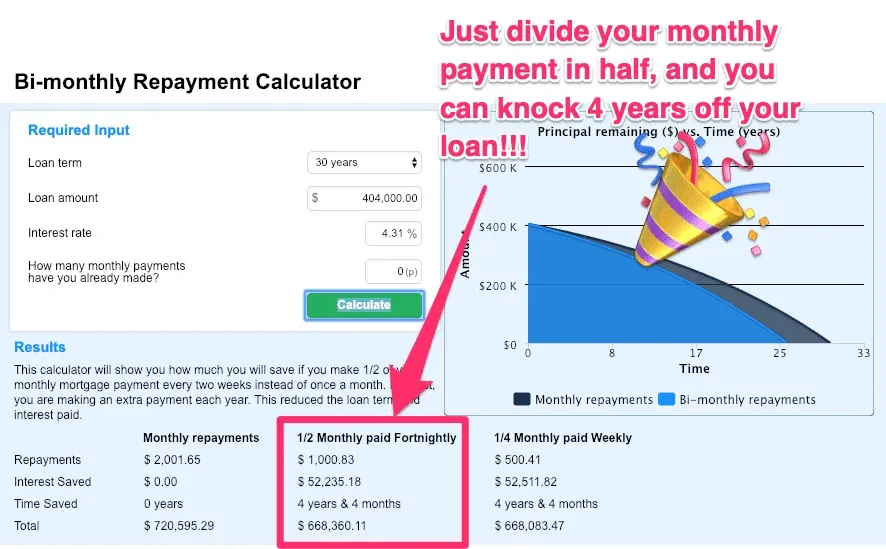

Increasing Your Repayment Frequency To Pay Off Your Loan Quicker

Out of everything, this is possibly the simplest AND most effective tip we can give you…

(The bi-monthly trick)

Most banks, by default, give you monthly repayments. So, in a year, they will assume you make 12 repayments.

Let’s say your monthly repayment is $2,000.

In a 12-month period, you will make $2,000 x 12 months = $24,000 in repayments. Simple right?

If you switch to bi-monthly (also known as fortnightly) repayments, you will make an extra 2 repayments without even realising.

So you make a $1,000 payment ($2,000 divided by 2) every fortnight, which there are 26 per year = $26,000 per year in repayments!

You will make an extra $2,000 in repayments per year without even realising AND save 4 years and 4 months from your loan!!!

How Many Years Does It Normally Take To Repay A Loan?

The banks will give you a home loan with a standard loan term of between 25 to 30 years.

There are some exceptions depending on your age, where the bank may require you to reduce your loan term. However, in general, the banks will give you a default loan term of 30 years and assume you will not make additional repayments. This is why you should look at the extra repayment calculator to see how many years you can save from your loan term!

How Many Years Will It Take To Repay A Home Loan With Extra Repayments?

The total time it will take you to repay your home loan will depend on a range of things, including your interest rate, loan balance, repayment frequency (monthly, fortnightly, weekly), the extra repayment amount and when you start making additional repayments.

Broadly speaking, the more you make in additional repayments, the sooner you make it will help you pay off the home loan faster.

When Is The Best Time To Start Making Additional Repayments?

As you have seen from the examples above, the sooner you start making additional repayments, the faster you will pay off your home loan. The table below shows how much money and time you can save by making extra repayments:

Extra repayments start

Interest saved overthe loan term

Total time saved

Immediately (0 years)

$102,357

3 years, 10 months

1 year

$93,980

3 years, 7 months

2 years

$86,076

3 years, 4 months

3 years

$78,623

3 years, 2 months

4 years

$71,615

2 years, 11 months

5 years

$65,031

2 years, 9 months

10 years

$38,009

1 year, 10 months

15 years

$19,511

1 year, 2 months

Figures calculated on a $600,000 loan amount, 30-year initial loan term, 5.85% interest rate and extra contribution of $200 per monthly payment.

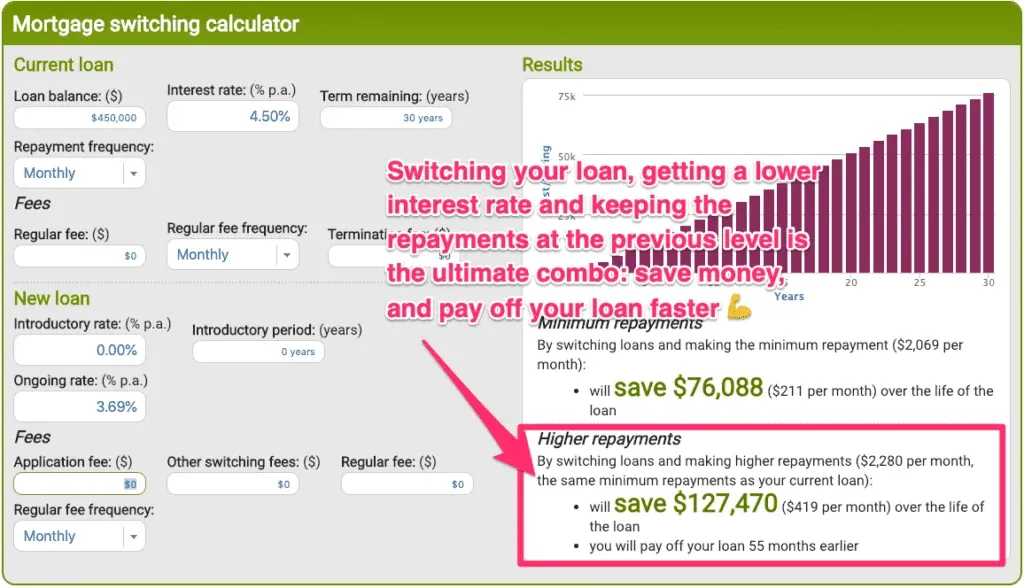

Does My Interest Rate Affect My Extra Repayments?

Switching to a lower interest rate can make a big difference in what you pay on your monthly repayment and how fast you can repay your home loan.

Generally, more than half of your monthly repayment interest, so the interest rate makes a big difference.

Let’s say you owed $450,000, had 30 years on your loan term, were paying 4.50% interest and had monthly repayments of $2,280.

If you were to switch to a lower interest rate of 3.69% (using ASIC’sMoneysmart calculator) and maintain the previous monthly repayment of $2,280 (even though your repayment would drop by default as the rate is lower), you would actually pay off the loan 4 years faster (55 months) and save $127,470 in interest costs!!

As we’ve covered, the more you can afford to repay, the less interest you will pay, and the faster you can pay your loan off.

But the amount of your extra repayments is really up to you and what you can afford.

We’ve done some numbers below based on a $600,000 home loan over 30 years to give you a bit of an idea of the difference other amounts make on your repayments.

Extra Repayments per month

Total interest savings over the life of the loan

Total time saved over the life of the loan

$100

$55,969

2 year 1 month

$200

$102,369

3 years 7 months

$300

$141,602

5 years 4 months

$400

$175,329

6 years 9 months

$500

$204,695

7 years 10 months

$1,000

$309,311

12 years 3 months

Home Loan Extra Repayment Calculator FAQs

Is there a limit to how much extra I can repay on my home loan?

Generally, there is no limit for Variable Rate home loans; you can pay off the entire debt tomorrow if you have the cash. However, Fixed Rate loans usually have a strict limit (often $10,000 to $20,000 per year). Exceeding this can trigger expensive “break costs.”

Does my monthly repayment drop automatically if I pay extra?

No. Most banks will keep your minimum monthly repayment the same, which effectively shortens your loan term (paying it off faster). If you want to lower your monthly repayment to improve cash flow, you must contact your lender and ask them to “recalculate” your repayments based on your new lower loan balance.

Is it better to make a lump sum payment or regular extra repayments?

Mathematically, a lump sum payment made today is always better than the same amount spread out over time. This is because interest is calculated daily. Killing $5,000 of debt today stops interest accruing on that $5,000 immediately, whereas spreading it out over a year allows interest to keep ticking in the background.

Can I withdraw the extra repayments if I need the money back?

Yes, if your loan has a Redraw Facility. Most variable loans allow you to pull back any “extra” payments you have made. However, be aware that some lenders may charge a small fee for this, or set a minimum withdrawal amount (e.g., $500).

How do I set up extra repayments?

You can usually set this up via your internet banking app by increasing your direct debit limit. Alternatively, you can set up a separate recurring transfer from your salary account to your home loan account labeled “Extra Repayment” to keep it distinct from your minimum required payment.

Need Some Help Crunching The Numbers?

Are you ready to make some extra repayments but don’t know where to start? Our team of home loan experts is here to help you!

Unlike other mortgage brokers who are just one-person operations, we havean entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 orbook a free assessment onlineto see how we can help.

Our team of home loan experts is here to help you buy a home in Australia