A loan can still be declined even after pre-approval if your financial position, lender policies, or the property itself no longer meet current lending criteria. Many buyers don’t realise banks reassess everything again before granting unconditional approval.

This comprehensive guide explains the hidden risks and practical steps to protect your purchase and secure final approval with confidence.

We will show you 29 techniques for turning around that decline to get unconditional approval, and consulting a mortgage broker in Brisbane is one of the most crucial steps. These strategies are working right now (in 2025).

Let’s dive in…

1. Switching Jobs After Pre-approval: What You Need to Know

Changing jobs can sometimes catch borrowers off guard. Even if your income goes up, lenders may reassess your application and decline your loan. Banks focus on stability, employment type, and how long you’ve been in your new role. Knowing how this works can help protect your home purchase.

Why Your Loan May Be Declined After Switching Jobs

Even with a pay rise, some banks might say no if you’ve recently changed employers. Here’s why:

- Employment type matters: Full-time versus casual can affect approval chances.

- Time in role: Many lenders prefer at least 12 months in your current position.

- Industry experience counts: Banks often look at your broader work history, not just the latest job.

These are the main reasons why a loan is sometimes declined after pre-approval in Australia.

Read more: Can I get a home loan if I just started a new job?

Case Study: When Pre-approval Was Reversed

Take Laura’s story. She had a pre-approved loan while working full-time at Electronic Boutique for two years. Then she moved to JB Hi-Fi on a casual basis, earning more with extra shifts.

Her bank withdrew pre-approval because she hadn’t been in her new casual role for 12 months.

Our Hunter Galloway brokers stepped in and secured unconditional home loan approval with another lender that considered her full industry experience.

This shows that what happens if your loan is declined often comes down to lender policies, not just your pay.

How to Protect Your Loan Approval

If you’ve recently switched jobs, here’s what to do:

- Tell your lender early: Being upfront helps avoid surprises at the final assessment.

- Document your experience: Provide pay slips and employment history to show stability.

- Work with a mortgage broker: They know which lenders are flexible with job changes.

- Check finance clauses: Make sure your finance clause isn’t rejected due to your new role.

Key Takeaway

Switching jobs doesn’t have to derail your home purchase. Chat with our Hunter Galloway brokers to:

- Get personalised lender advice

- Maximise your approval chances

- Protect your deposit and finance clause rights

Contact Hunter Galloway today for a free home loan assessment and expert guidance.

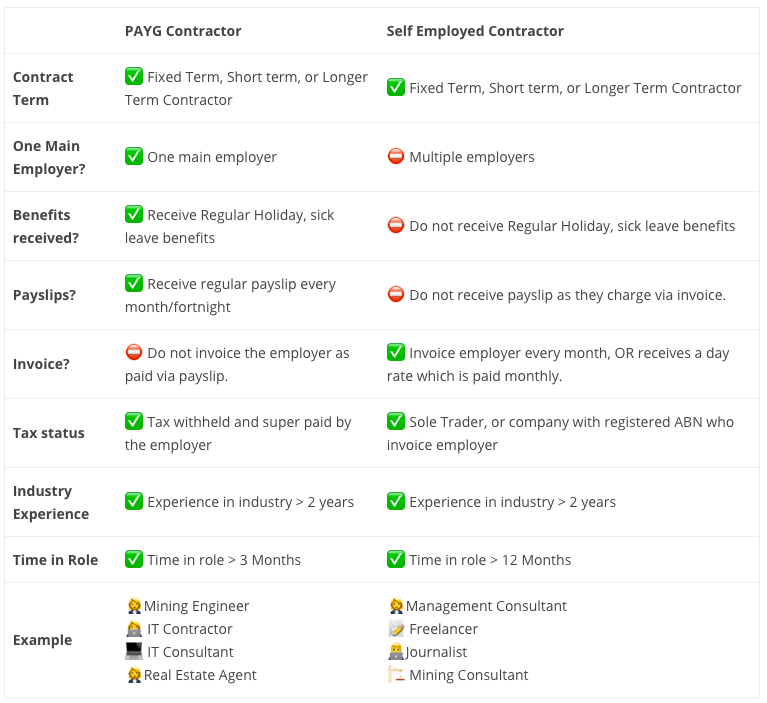

2. A Contractor For Less Than 12 Months: What It Means For Your Loan

Being paid as a contractor doesn’t mean your home loan is off the table. However, less than 12 months in a contract role can make some lenders nervous. Banks look closely at stability, contract length, and how your income is structured.

The Two Types of Contractors Lenders Assess

Most contractors fall into one of these categories, and each is treated differently by lenders:

- PAYG contractors: Work on fixed or ongoing contracts and receive sick leave and holiday pay.

- Self-employed contractors: Invoice through an ABN and cover their own tax, super, and expenses.

In both cases, a bank is likely to decline your loan if you lack a solid contract history.

Why Banks Hesitate With Short Contract History

Even a strong income isn’t always enough if your role looks unstable. Banks often decline loan after pre-approval in these circumstances:

- Short remaining contract terms

- Gaps between contracts

- Irregular income patterns

- Limited history in contracting

Case Study: Contractor With Less Than 6 Months Remaining

Kate and Thomas applied for a home loan together. Thomas worked with the same employer for three years. Four months ago, he moved into a contractor role for higher pay.

His initial contract ran for six months and had only two months left. He also invoiced monthly, making him a self-employed contractor.

His existing bank declined the loan after preapproval due to contract length and income structure.

Our Hunter Galloway home loan experts stepped in and secured unconditional home loan approval with a major lender. We used his new income rate, which was 35% higher than before. This helped them borrow more than if they had relied on his old salary.

How to Strengthen Your Application as a Contractor

If you earn contract income, here’s how to improve your chances:

- Provide your full contract and extension history

- Show consistent work in the same industry

- Demonstrate stable income across multiple months

- Use a broker who understands contractor policies

Key Takeaway

Contract work does not stop you from buying a home. It just means lender selection becomes critical.

Read more: How to get a home loan on contractor income

3. Mortgage Insurance: When LMI Causes A Loan Decline

If your deposit sits below 20%, lenders require Lenders Mortgage Insurance (LMI). While your bank may approve your profile, the mortgage insurer makes a separate decision. This is a common reason a loan is declined after pre-approval in Australia.

Why Mortgage Insurance Can Stop Your Approval

Mortgage insurers apply stricter rules than most lenders. They assess risk based on several factors, including:

- Size of your deposit

- Property type and location

- Employment stability

- Credit profile and history

- Overall loan-to-value ratio

So, even when the bank is comfortable, the insurer may still say no.

Case Study: Loan Declined After Pre approval Due To Mortgage Insurance

Shelley called us in early October after her home loan application was declined. Six weeks earlier, her bank had issued pre-approval. She quickly found a property and signed the contract.

The bank completed its valuation and assessment without any issues. However, Shelley only had an 8% deposit. This meant the lender’s mortgage insurer had to approve the deal before unconditional home loan approval was issued.

Although she met the bank’s criteria, the insurer declined the application.

Fortunately, Shelley’s story didn’t end there. Our expert mortgage brokers in Brisbane stepped in and secured approval with another lender using a more suitable insurer policy.

How to Avoid an LMI-Related Loan Decline

If your deposit is under 20%, take these steps to reduce risk:

- Confirm which insurer your lender uses

- Understand their approval criteria early

- Work with a broker who knows lender-insurer combinations

- Explore low-deposit government schemes

- Strengthen your application before submission

Doing this will reduce your chances of getting denied after pre-approval.

Key Takeaway

Mortgage insurance can block approval even when the bank supports your application. However, the right lender and strategy can change the outcome.

Read more: What is lenders mortgage insurance and how do I calculate it

4. Declined After an Assessment Rate Change

Many buyers get shocked when a bank declines a loan after pre-approval without any personal changes. Often, the issue is the lender’s assessment rate, not your finances. This is a hidden reason why your pre-approved loan may be declined.

Banks do not use today’s actual interest rate when calculating borrowing power. Instead, they apply a higher assessment rate to stress test your ability to repay. This buffer protects lenders if rates rise in the future.

What Is an Assessment Rate?

An assessment rate sits around 2–3% above your actual interest rate. It measures how well you handle repayments if rates increase. In simple terms, it acts as a financial stress test.

Because banks keep these rates private, many borrowers only discover changes at final assessment when their pre-approval is withdrawn by the bank.

How Assessment Rate Changes Kill Borrowing Power

A small rate shift can cause a large borrowing drop. Here’s a clear example:

- Single borrower income: $70,000 per year

- No existing debts

At a 5.50% assessment rate, borrowing capacity sits around $565,000.

At a 7.00% assessment rate, capacity drops to $470,000.

That’s a reduction of over $95,000, without any change to income.

Why This Causes Your Loan To Be Declined After Preapproval

You may receive pre-approval at one assessment rate. Then the bank raises it before final approval. Suddenly, the loan no longer fits serviceability rules.

This can derail your purchase and delay unconditional home loan approval. In some cases, buyers must renegotiate or withdraw from the contract.

How to Protect Yourself

If you’re worried about interest rate shifts causing your loan t be declined after pre approval, take proactive steps:

- Ask if your lender will reassess serviceability at final approval

- Confirm whether assessment rates are locked at pre-approval

- Use a broker to monitor lender rate changes

- Avoid borrowing at your absolute maximum

Key Takeaway

Assessment rate changes can quietly reduce your borrowing power. Even strong applicants can lose approval overnight.

5. Being Self-Employed: Why Approval Feels Harder (But Isn’t Impossible)

Getting a home loan while self-employed often feels tougher than it should. Some banks apply stricter rules to business owners. However, many lenders actively support self-employed borrowers.

At Hunter Galloway, we secure home loan solutions for over 89% of our self-employed clients through major banks. The key lies in matching you with the right lender.

Why Self-Employed Loans Get Declined After Pre approval

In Australia, a loan can be declined after pre-approval for business owners usually due to policy, not performance. The most common triggers include:

- Profit changes over 20% between financial years

- Active tax payment plans with the ATO

- Missing or outdated financials for the current year

Banks assess both income stability and financial management habits. Payment plans signal risk, even when income looks strong.

Different Banks, Different Rules

Not all lenders treat self-employed income the same. Their cut-offs and calculations vary widely.

Lender | Tax Returns Required | Income Calculation Method |

Bank 1 | FY25 + FY26 financials | Average of both years |

Bank 2 | FY25 only | Most recent year’s profit |

Bank 3 | FY25 + FY26 + management accounts | Lower of both years |

This variation directly impacts borrowing power and the risk of a finance clause rejected scenario.

Case Study: Strong Profits, Declined by the Bank

Sally and Erica ran a successful wedding photography business for over 18 months. Their profits grew by 142% year-on-year. They applied for an investment loan to expand.

Their bank declined the application due to less than two years of trading history. They also refused to assess the most recent year’s higher profit.

Using bank policy flexibility, our brokers secured unconditional home loan approval with a major lender. We relied on their latest financials to reflect true income strength.

This case highlights that when your loan is declined after pre-approval, it’s not the end of the world.

How to Strengthen Your Self-Employed Application

If you run a business, take these steps before applying:

- Keep tax returns and financials up to date

- Avoid ATO payment plans where possible

- Maintain consistent business income records

- Work with a broker experienced in self-employed lending

These actions reduce the risk of rejection and improve approval certainty.

Key Takeaway

Being your own boss doesn’t block your path to property ownership. It simply requires smarter lender selection and expert structuring.

Speak with us today for a free assessment tailored to self-employed business owners.

Read more: Self-Employed Finance Options for Business Owners

6. Type Of Occupation: How Your Job Can Affect Your Home Loan Approval

Not all jobs are viewed the same by banks. Your occupation plays a bigger role than most buyers realise, especially if you’re relying on pre-approval.

We often see scenarios where a buyer assumes everything is fine, only for the bank to withdraw pre-approval just days before settlement!

This usually happens when your role is seen as unstable or unpredictable.

Why banks treat some occupations as higher risk

Banks care about one thing first: consistent income. If your income fluctuates or depends on seasonal demand, lenders become cautious.

Occupations commonly flagged as higher risk include:

- Underground miners

- FIFO workers

- Seasonal workers

- Farmers

- Sex workers

- Contractors

- Gig economy roles

Even if your income is strong, inconsistency can delay or stop your unconditional home loan approval.

During COVID-19, we saw heightened scrutiny around job security, contract types, and employer stability. That cautious approach still influences lending decisions today.

How this leads to declined loans after pre-approval

A pre-approval is only a conditional green light. It does not guarantee your loan will be funded.

Before settlement, banks perform a final assessment called formal approval. This is where many borrowers encounter a nasty surprise.

If you work in a higher-risk occupation, lenders may:

- Reassess your income under stricter criteria

- Request additional payslips or contracts

- Reduce the amount they are willing to lend

- Recalculate your borrowing power

- Apply tighter policy rules at the last minute

Even small changes can trigger alarm bells. A shift in hours. A new contract. A drop in overtime. A change of employer.

Banks also re-verify employer stability and ongoing work prospects. If they perceive uncertainty, they may reverse their earlier decision, even days before settlement.

What happens if your loan is declined because of your job?

When this happens, the consequences can be serious.

You could:

- Lose the property

- Risk your deposit

- Miss settlement deadlines

- Have your contract fall through

How Hunter Galloway helps you avoid this trap

Here’s the good news. Different banks view occupations very differently.

Some lenders actively work with borrowers in non-traditional roles. Others avoid them completely. Our job is to place your application with a lender that understands your employment structure.

We look at:

- Your income consistency

- Industry stability

- Contract terms

- Employer profile

Key Takeaway

Your type of occupation can directly impact your home loan approval. If a bank reassesses your job as high risk, they may withdraw pre-approval, delay your unconditional home loan approval, or cause your finance clause to be rejected. The safest move is to speak with a broker early and match your application to a lender that supports your industry.

7. Going On Holidays Can Trigger A Loan Decline

Taking time off can unexpectedly impact your approval, especially if you’re a casual or contract worker. When income pauses, banks may assume your earnings have dropped, even if it’s only temporary.

Why Your Loan Can Be Declined After Preapproval

Full-time employees receive paid leave. Casuals and contractors usually do not. When income temporarily drops, lenders reassess affordability during final checks.

Here’s where it can go wrong:

- Banks request your most recent payslip before unconditional home loan approval.

- If that payslip shows low or nil income, they annualise the figure.

- A reduced income can lower your borrowing capacity.

- That change may cause the bank to withdraw pre-approval.

Short-term income gaps often play a bigger role than expected in getting your home loan declined after preapproval

Real-World Example: Casual Worker On Leave

A relief teacher earning strong income throughout the year applies during the Christmas break. Because no shifts were worked, the latest payslip shows no income.

The bank uses that figure to reassess serviceability. Borrowing power drops. Approval fails. Pre-approval is withdrawn.

Key Takeaway

Temporary income pauses can cause a loan to be declined after pre-approval, even when your overall earnings remain strong. Choosing a lender that assesses total yearly income can protect your approval and avoid last-minute stress.

8. Overtime, Shift Loading, Bonuses, and Salary Sacrifice

For many employees, extra pay like overtime, shift loading, and bonuses make up a significant portion of income. Banks often handle this differently, which can affect your loan approval after pre-approval.

Not all lenders recognise that this pay is essential, especially in industries like nursing or shift work.

Why Lenders Adjust Overtime and Bonus Income

Some banks only consider 50–80% of your overtime or bonus income and may ignore salary sacrifice contributions like extra superannuation.

This approach can dramatically reduce the amount you can borrow, even if your total earnings remain high.

Real-World Example: Nurses

Nurses often rely on overtime and shift loading as a core part of their pay.

- Working different shifts month-to-month can show variable income.

- Banks that don’t account for this may decline the loan at final assessment.

At Hunter Galloway, we work with lenders who understand shift work income. They can consider 100% of overtime, shift loading, and bonuses where appropriate.

What You’ll Need to Qualify

To maximise your borrowing capacity using overtime or bonus income, we usually require:

- Your two most recent payslips

- Your latest PAYG group certificate

- In some cases, a letter from your employer confirming regular overtime for 1–2 years

Type of Income | Bank A | Bank B | Bank C |

Overtime | 100% can be used | Unacceptable | 80% can be used |

Bonuses | 100% if >12 months history | Under 2 years unacceptable | 80% can be used |

Salary Sacrifice | Can be added back if discretionary | Unacceptable | Can be added back if discretionary |

Key Takeaway

Banks often undervalue overtime, bonuses, and salary sacrifice, reducing borrowing power. With the right lender and documentation, you can maximise income recognition and protect your approval.

If your income relies on overtime or shift penalties, speak with Hunter Galloway today.

9. Uber Income Or Second Job Not Being Accepted

Extra income from a side hustle, like driving for Uber, Ola, GoCatch, Lyft, Shebah, or having a second job, can boost your borrowing power. However, not all banks recognise this type of income. Some may only accept 50% of it, which can impact your loan approval after pre-approval.

Why Banks Restrict Side Income

Lenders want to see consistency and reliability. Income from gig work or casual second jobs is considered less stable than traditional employment. Without proper documentation, your bank might withdraw pre-approval if you are relying on your second income.

How to Get Your Side Income Accepted

Banks typically require at least 12 months of proof that your Uber or second job income is consistent. This demonstrates stability and helps maximise your borrowing capacity.

Type of Income | Bank A | Bank B | Bank C |

Uber or Second Job | Most recent year’s tax return | Lowest figure from last 2 years’ tax returns | Average figure from last 2 years’ tax returns |

Documentation You’ll Need

To have your side income considered, prepare:

- Your most recent year’s tax return

- Your most recent ATO Notice of Assessment

- Business Activity Statements (BAS) if applicable

- 6–12 months of business account statements

Key Takeaway

Not all banks accept Uber or second job income, but with proper documentation and lender selection, you can boost your borrowing capacity and protect your home purchase.

10. Taking On An Extra Credit Card

When you receive pre-approval, the bank works out how much you can borrow based on your income and your current financial commitments at that exact point in time.

In simple terms, they run your numbers through their calculator to check what you can comfortably manage.

The problem starts when something changes after that — like taking out a new credit card, increasing an existing limit, or financing a car. Even small changes can have a bigger impact than most people realise.

Here’s the catch: banks assess credit cards based on the full limit, not how much you actually owe. So even if you never touch the card, a new $10,000 limit can significantly reduce your borrowing capacity.

If you’re already close to your maximum, that one decision can be enough to tip your application from approved to declined.

(Those QANTAS points suddenly feel a little less rewarding…)

Why this can lead to a declined loan after pre approval

Before settlement, your lender will re-check your financial position. This includes your credit file, liabilities, and any changes since your pre-approval was issued.

If your new commitments push you outside their serviceability rules, they may:

- Reduce the amount they’re willing to lend

- Ask for more funds upfront

- Or decline the loan altogether

It’s one of the more common and avoidable reasons buyers lose their pre-approval.

Simple ways to protect your borrowing power

- Avoid applying for new credit before settlement

- Lower unused credit card limits

- Close Afterpay and similar accounts

- Pay down existing loans where possible

- Check with your broker before making any changes

Read More: How do I increase my borrowing capacity?

11. Too Many Credit Enquiries

As if age, property type, and job security weren’t enough, banks can also decline your home loan simply because you’ve had too many credit enquiries.

If you’ve made more than two or three credit applications in the past six months, some lenders may see this as a red flag and lower your credit score — even if your income and savings are strong.

What surprises most people is where these enquiries come from.

It’s not just credit cards.

Every time you:

- Sign up for a phone plan

- Switch electricity providers

- Apply for Afterpay or Zip

- Take out interest-free finance

A credit check is often recorded on your file.

So without realising it, you could be stacking up enquiries that make you look risky in the bank’s eyes.

Why this causes problems with your loan

From a lender’s perspective, multiple enquiries can suggest financial stress or over-reliance on credit — even when that’s not the reality.

When they see too many recent checks, they may:

- Lower your credit score

- Flag your file as high risk

- Decline your application outright

And frustratingly, this can happen even if you’ve never missed a single repayment.

The good news: not all lenders treat this the same

Some banks take a more practical view. If there are genuine reasons for your enquiries — like moving house, changing utilities, or upgrading phones — they may still approve your loan.

There are also lenders who don’t rely heavily on automated credit scoring and instead assess your situation more holistically.

How to stay in control of your credit file

- Request a free copy of your credit file from Veda (or we can organise this for you)

- Set up Credit File Alerts through Equifax

- Space out any credit applications

- Avoid unnecessary finance or “buy now, pay later” services

- Work with lenders who use manual assessments rather than strict credit scoring

Our team regularly works with these more flexible lenders and can help you understand your options with a free, no-obligation assessment.

Read More: What positive credit reporting means to home loans

12. Missing A Phone Bill

Most people think a bad credit history only comes from big issues like bankruptcies or court judgments. But what many buyers don’t realise is that even something as small as a missed phone bill can derail their home loan.

Defaults as low as $100 can be enough for a bank to decline your application just days before settlement.

We recently helped a first home buyer who had a small phone bill sent to an old address. They’d moved, never received the notice, and had no idea the account was overdue. The telco placed a default on their credit file, and the buyer only discovered it when their bank refused to proceed with formal approval.

In their case, the fact that the bank withdrew pre-approval put the purchase at risk.

Fortunately, they came to us before it was too late. We matched them with a lender who took a more practical view of the situation, and they were still able to secure unconditional home loan approval and move into their dream home.

How lenders look at phone bills

Here’s how different banks typically treat telco defaults:

Phone Bill Default | Bank A | Bank B | Bank C |

Under $100 | No | Yes, if paid | Yes, if paid |

Under $500 | No | Yes, if paid | Yes, if paid |

Over $1,000 | No | No | Yes, if paid |

As you can see, the lender you choose makes a huge difference. The wrong bank can lead to rejection even when the issue is minor and has already been paid.

Ways to navigate a bad credit file

A black mark on your credit file doesn’t always mean your loan will be declined — but it does mean your choice of lender becomes critical.

Here’s what you can do:

- Get a free copy of your credit file from Veda (or we can organise this for you)

- Sign up for Credit File Alerts through Equifax

- Dispute incorrect defaults where appropriate

- Work with lenders who don’t rely solely on rigid credit scoring

- Get expert guidance before submitting your application

Your situation might feel stressful, but it’s often far from hopeless. The right strategy can mean the difference between rejection and approval.

Speak with our Bad Credit Experts on 1300 088 065 to find out how we can help you avoid a declined application and secure the right outcome.

Read More: What happens if I have a bad credit history?

13. Late On A Rent Payment

Most people would assume that being late on rent has nothing to do with getting a home loan. Unfortunately, some lenders see it very differently.

Many banks now request a 12-month rental history (also known as a tenancy ledger) as part of the assessment process. This shows whether your rent has been paid on time and consistently.

If you’ve missed a rental payment or been late more than once in the past 12 months, your loan can be declined — even when everything else looks solid on paper.

Case study: One late payment, one real scare

Sally and Tom had been renting their Brisbane unit for three years with a perfect payment record. In January, they went on holiday and had their funds sitting in their savings account, not their everyday transaction account where the rent was deducted.

Their rent tried to come out as usual, but there wasn’t enough money in that account. The payment failed, their rent showed as late, and an overdrawn fee was charged.

As a result, the bank was about to withdraw their preapproval due to what they labelled as “poor rental conduct” — putting the couple at risk of losing their home

Fortunately, they came to Hunter Galloway. We provided evidence that they had sufficient funds and explained it was purely a timing issue while they were travelling. The lender reversed their decision, and Sally and Tom successfully secured their loan

How late rent can derail your approval

From a bank’s point of view, late rent can suggest:

- Poor money management

- Cash flow issues

- Higher risk of missed mortgage repayments

What to do if your loan is declined after pre approval for late rent

A late payment doesn’t automatically mean your home loan will fail — especially if there’s a reasonable explanation. What matters is how it’s presented.

Here’s what can help:

- Show it was a timing issue or transfer delay

- Provide proof of funds in another account

- Explain admin errors or direct debit failures

- Demonstrate otherwise perfect rental history

Missing one rent payment is frustrating, but it doesn’t have to end your home buying plans. With the right lender and a clear explanation, this situation can often be resolved.

14. Spending Habits

When you apply for a home loan, most banks will ask to see your last three months of everyday transaction statements — and some will even request four. They go through these line by line to understand how you actually spend your money, not just what you earn.

And yes, it can be surprisingly detailed.

If you regularly spend large amounts at fashion retailers, bottle shops, betting platforms, or subscription-based entertainment sites, this can raise concerns. From a lender’s perspective, patterns that look like gambling or uncontrolled discretionary spending can directly affect whether or not you receive unconditional home loan approval.

Why your spending can trigger a declined loan

Banks analyse your recent transactions and “annualise” them to calculate your likely yearly living costs. If your expenses look high — even for a short period — they may conclude you don’t have enough surplus income to service a mortgage.

Case study: A holiday that almost cost a home

Tara had just returned from a Sydney holiday and applied for pre-approval through her bank, Suncorp. They reviewed four months of statements and calculated she was spending $2,000 per month on entertainment, plus $1,532 on general living costs.

On paper, this left just $468 per month to cover a mortgage — not nearly enough under their assessment rules.

As a result, her loan was declined, purely due to an unusually expensive month.

Our team stepped in and demonstrated that these expenses were out of character and holiday-related. By identifying once-off costs like flights, airport transfers and accommodation, we were able to reposition her application and secure approval through a more suitable lender.

How to explain high living expenses

High spending doesn’t automatically mean rejection — what matters is how it’s explained and who assesses it.

Helpful steps include:

- Identifying recent holidays or temporary lifestyle changes

- Highlighting once-off purchases or travel costs

- Ensuring your declared expenses match your bank statements

- Working with a lender that considers context, not just raw numbers

Your spending history can absolutely be managed with the right strategy. One expensive month shouldn’t cost you your dream home.

If you’re worried your statements could affect your application, speak with our Home Loan Experts on 1300 088 065. We’ll help you navigate the process and avoid unnecessary setbacks.

Read More: 21 easy tips to find the best mortgage broker in Brisbane

15. Decreases In Income

At the time your pre-approval was issued, your bank assessed your income based on what you were earning then. But if your hours have since dropped, a bonus has stopped, or your workload has temporarily reduced, your income on paper may now look lower — and that can be enough for the bank to withdraw pre-approval.

This situation is especially common for casual and shift workers, where hours naturally fluctuate.

Why income drops cause problems

When banks reassess your application before issuing unconditional home loan approval, they verify your most recent payslips. If these show reduced earnings, lenders may conclude you no longer meet their serviceability criteria.

That means:

- Your borrowing capacity may shrink

- Your approval may be downgraded

- Your loan can get declined because of that

How different banks assess casual income

Not all lenders treat variable income the same way. Here’s how the same weekly income can be interpreted very differently:

Type of Income | Bank A | Bank B | Bank C |

Casual Income | Weekly pay × 46 weeks | Weekly pay × 52 weeks | Year-to-date payslip annualised |

Real example: Matthew the barista

Matthew works as a casual barista. During December, his hours dipped due to public holidays and slower shifts. He supplied this quieter-month payslip to his bank, and suddenly his income appeared lower than usual.

Here’s how three banks assessed him:

- Bank A: $500 × 46 = $23,000 per year

- Bank B: $500 × 52 = $26,000 per year

- Bank C: Year-to-date method = $30,000 per year (more accurate reflection)

The wrong lender made Matthew look riskier than he was. The right lender understood the pattern — and that made all the difference.

What helps support fluctuating income

To avoid unnecessary rejection, lenders may accept previous higher income if it’s supported correctly. Typically, they’ll ask for:

- Your two most recent payslips

- Your latest PAYG summary or group certificate

- Your most recent tax return (if available)

- A clear explanation for the temporary drop

The takeaway

A short-term dip in income doesn’t mean your home loan is doomed. What matters is context, documentation, and choosing a lender that understands how your industry really works.

If you’re worried that recent changes could affect your approval, speak with our Mortgage Broker Brisbane Home Loan Experts on 1300 088 065. We’ll guide you through the safest path to securing approval and protecting your purchase.

Read More: Loans for people with unique employment

16. Working For Family

Working for a family member can have its perks, but when it comes to home loans, it can quickly become a headache. In fact, it’s one of the more common reasons a loan can be declined after pre-approval in Australia.

From a bank’s perspective, family employment can be a red flag. They may worry that your income isn’t truly independent or that your role could change easily if circumstances shift. And when we say “family”, the definition is broad — parents, spouse, de-facto partner, siblings, grandparents, children, in-laws, or even a legally appointed guardian all fall into this category.

Because of this, lenders often apply extra scrutiny. They may want to confirm:

- That your income is genuine and ongoing

- That your role isn’t created just to help secure a loan

- That you’re paid at market rates and under normal conditions

This can mean providing additional documents such as:

- An employment contract outlining your role and pay

- Payslips and bank statements showing consistent income

- Evidence the business is financially viable (like BAS or financial statements)

- A letter from the employer confirming your position and hours

The good news? Working for family doesn’t automatically mean your loan will be declined. It just means the application needs to be structured carefully and placed with a lender that understands your situation.

17. The Type Of Rental You Receive

Not all rental income is treated the same by lenders. While most banks will usually accept around 80% of your rental income, the actual amount they use can vary depending on the type of rental and how stable they believe it is.

Case Study: Airbnb Rental Income on an Investment Property

If you rent out a spare room or use platforms like Airbnb or Stayz, some banks may only take 50–60% of your gross rental income into account. This is because short-term rentals are seen as less predictable than a standard long-term lease.

That said, not all lenders take such a conservative approach. Some will accept the rental income shown on the property valuation, and others (including several we work closely with) may allow up to 80% of short-term rental income — as long as you can support it with your latest tax return showing rental income and expenses.

Here’s a snapshot of how differently banks can assess rental income:

Type of Rental Income | Bank A | Bank B | Bank C |

Standard Rental | 80% of gross rent | 80% of gross rent | 75% of gross rent |

Student Accommodation | 60% | 60% | 60% |

DHA Lease | Not accepted | 100% of net rent | 75% of gross rent |

Serviced Apartment | Not accepted | 60% | 60% |

Holiday Rental | Not accepted | 80% | 60% |

Short-Term Rental (Airbnb, Stayz, Guest Housing) | Not accepted | 80% | 50% |

Commercial Rental | 70% | 70% | 70% |

To use this rental income, most lenders will ask for:

- Your most recent Airbnb or rental platform statement showing income within the last 120 days

- Your two most recent PAYG group certificates

- Your two most recent tax returns and ATO Notices of Assessment

If your loan was declined due to the type of rental income you receive, it doesn’t mean you’re out of options. The key is getting an expert mortgage broker to help you apply with the right lender who understands your rental structure.

18. Using Your Deposit Can Get Your Loan Declined After Pre approval

Home loan pre-approvals can last up to six months, so it’s not uncommon for your deposit to look very different by the time you actually find the right property. Maybe life happened, unexpected costs popped up, or you simply dipped into those savings — and now you’re worried about the bank declining your loan because your deposit has dropped.

The good news? Using some (or even all) of your deposit doesn’t automatically mean an unconditional home loan approval is off the table.

Here are some practical ways to navigate it:

- Look for a lender willing to accept a smaller deposit. Some can approve loans up to 95% LVR, or even 100% if you have a guarantor.

- Consider a gifted deposit from parents or family to cover the shortfall.

- Explore brand-new properties where you may qualify for the $30,000 Queensland First Home Owner Grant.

- Adjust your purchase price to reduce the deposit needed and improve your approval chances.

We regularly help clients who thought their situation would lead to a loan declined after pre-approval in Australia, only to secure approval by choosing the right lender and structure.

Not having enough deposit isn’t the end of the road, you can secure approval by choosing the right lender and structure.

Read more: How much is the First Homeowners Grant?

19. Buying In A High-Density Area

Buying an apartment in a high-density complex can make lenders nervous. Most banks consider a property “high-density” if the building has more than 50 units and is over four storeys high. Others base it purely on postcode, with areas like Brisbane CBD (4000) automatically flagged as high-risk.

Even when banks are open to apartment purchases, they often decline loans after pre approval for concerns such as:

- Restrictions based on suburb or postcode

- Limits when the building exceeds four storeys

- Minimum apartment size requirements (especially under 40sqm)

- Exposure limits if the bank already has too many loans in the same building

How banks view high-density properties

Type of Property / Criteria | Bank A | Bank B | Bank C |

High Density (Maximum LVR) | 65% | 90% | 95% |

Minimum apartment size | 1 bedroom 50sqm2 bedrooms 60sqm | Maximum LVR depends on factors like borrower type, loan amount, property location and valuation report | Has to be an owner-occupied purchase (i.e. you will live there) |

How to reduce the risk of having your loan declined after pre approval

If you’re buying in a high-density area, here’s what you should do to avoid problems later:

- Ask your mortgage broker to confirm the bank will accept the specific building

- Arrange a valuation early to identify any red flags

- Double-check the internal floor size of the apartment

- Ensure the lender hasn’t exceeded its exposure limit in that complex

Some lenders will still allow borrowing up to 95% LVR for high-density apartments — but choosing the wrong one can quickly lead to having your home loan declined even after preapproval.

Read more: How to find the best home loan in Brisbane

20. Saving History

When borrowing with a smaller deposit, banks will want to understand your savings history — often referred to as genuine savings. This is simply money that you’ve personally saved and held in your account over time.

Typically, banks look for funds that have been in your account for at least three months. In recent years, many lenders expect at least 5% of the property’s purchase price to be in genuine savings.

What counts as genuine savings?

While it depends on the lender, some situations allow you to borrow with less than a 10% deposit without showing genuine savings. Banks may accept alternative evidence of financial stability, such as:

- Equity held in other properties

- Rental history over at least six months

- Term deposits

- Shares held

Each lender has its own rules for genuine savings, usually based on your deposit size and the property type. Not having traditional savings doesn’t automatically mean your home loan will be declined, but it can influence your approval if not managed correctly.

How banks assess genuine savings

Type of Savings | Bank A | Bank B | Bank C |

Genuine Savings | Over 85% LVR | Over 90% LVR | Over 80% LVR |

Using Rental History as Genuine Savings To Get Your Loan Approved

If you want to demonstrate savings through your rental history, banks usually require a letter from your real estate agent confirming:

- Full names of tenants

- Property address you rented

- Start date of tenancy

- Rent paid per week, fortnight, or month

- Confirmation that no payments were missed

This can be a great way to show financial discipline without a large deposit sitting in your account.

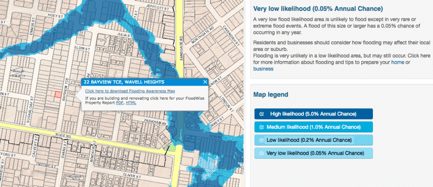

21. Purchasing A Property In A Flood Zone

Buying a property in a flood-prone area can make banks nervous — especially in Brisbane, where certain areas have a greater than 1 in 100 chance of flooding. This is often measured using the Q100 flood level, which estimates water height based on previous flood events. Some lenders simply won’t approve a home loan for a property in a flood zone.

How to check if your property is in a flood zone

You can find out if a property is in a flood zone by:

- Checking the Flood Awareness Map on the Brisbane City Council website

- Seeing if it falls within postcodes historically affected by flooding

Flood Prone Postcodes in Brisbane | Suburbs Affected by Flooding in 2011 |

|

|

Can you still buy in a flood zone?

Yes — it’s not impossible! Some lenders will consider your application if you can provide:

- Comprehensive flood cover insurance

- A satisfactory property valuation or survey report

- Additional context such as loan amount, property type, location, and loan structure

Buying in a flood zone doesn’t automatically mean your home loan will be declined. With the right lender and documentation, you can still secure a home loan even in higher-risk areas.

If you’re considering a flood-prone property, our Home Loan Experts can guide you through the process and help ensure your application is successful. Call us on 1300 088 065.

Read More: Research if your home has gone swimming (i.e., flooded in Brisbane)

22. Purchasing A Property With Renovation Issues

That “worst house on the best street” or “renovator’s delight” might look like a dream investment… until the bank declines your loan after pre-approval!

Banks are generally cautious about properties that are incomplete or in poor condition. Missing kitchens, bathrooms with holes, or structural issues are often enough for a lender to say no — especially if your deposit is less than 20%.

What banks look for

Whether a property with renovation issues can be financed depends on the severity and type of problems. Key questions include:

- How bad is the house? Is it structurally sound?

- Are the issues cosmetic or major?

- Will it cost less than $50,000 to fix?

- Can you provide quotes or a building contract for the renovations?

- Will you be able to live in the house while renovating?

Even with renovation issues, your home loan doesn’t have to be declined. The right lender and proper documentation can make all the difference in securing unconditional home loan approval.

23. Changes In Credit Criteria

Bank credit policies are constantly evolving — and with the ongoing impact of the Banking Royal Commission, these changes can happen even more frequently.

So, what happens if you applied for pre-approval in February but only find the right property in March, after the bank has updated its credit criteria? Your loan might be declined, even though it was previously pre-approved.

How to navigate changes in credit criteria

Working with an experienced mortgage broker can make all the difference. Ask plenty of questions before you commit, such as:

- How many years of experience do you have as a mortgage broker in Brisbane?

- What did you do before becoming a mortgage broker?

- Do you own property yourself, and how many?

- What types of home loan customers do you usually assist?

- How many home loans do you arrange each week, and what is the average loan size?

The right broker will guide you through any shifts in credit criteria and ensure your application is structured correctly to maximise your chances of unconditional home loan approval.

24. Failing The Bank's Credit Score

Many banks now rely on credit scores to evaluate applicants instead of manually reviewing past transactions. Your credit score takes into account several factors, including:

- Number of credit enquiries in the past 3–6 months

- Types of finance you’ve applied for in the past 12 months

- Overdue or defaulted debts in the past 5 years

- Bankruptcy in the past 10 years

- Late payments on utilities like electricity, gas, or mobile phones

- Interest-free or Buy Now, Pay Later loans like AfterPay

- Court writs or judgments

Case Study 1: Tyrone – Loan declined due to recent credit activity

Tyrone applied for a home loan, but in the previous four months he had applied for a personal loan, two credit cards, and an interest-free purchase. He also had one late electricity payment while travelling for work. His bank declined his loan after pre-approval because of a low credit score.

Hunter Galloway stepped in and found a lender that didn’t credit-score home loan applicants. By explaining Tyrone’s travel situation and clarifying his other financial activity, we were able to get his loan approved.

Case Study 2: Nick – Loan declined after pre approval over a 13-year-old missed payment

Nick was a perfect applicant with a high credit score (over 900), stable employment, no debt, and a 20% deposit. Despite this, his bank declined the application because of an unpaid default from 13 years ago. Banks often have long memories, and past history with the institution can still influence decisions.

Failing a bank’s credit score does not automatically mean your home loan will be declined. With the right lender and guidance, you can still secure approval.

25. An Unreliable Pre-approval

This is one of the biggest reasons why people get their loan declined after pre approval – they got the wrong pre approval to begin with…

Not all banks handle pre-approvals the same way. You may hear them called a conditional approval, indicative approval, approval in principle, or home seeker — it depends on the lender.

In most cases, a pre-approval is just an indication that the bank is open to considering your loan. Some banks may only complete a basic credit check and not fully verify your documents until you lodge a full mortgage application.

A full mortgage application is completed once you find a property. At that stage, the lender will thoroughly assess your loan by verifying:

- Payslips and income information

- Bank statements and savings

- Existing liabilities

Getting a pre-approval does not guarantee that the bank can lend you the money — so it’s important to understand the limits of that approval.

26. The Pre-approval Expired

Bank pre-approvals are usually valid for 90 to 180 days (3–6 months). This is also called the approval-in-principle period.

But what happens if you find a house after 6 months and 1 day? Your pre-approval has expired, and you’ll need to provide the bank with updated payslips, bank statements, and identification.

Different banks handle expired pre-approvals differently:

- Some may simply confirm that your financial position hasn’t changed over the past 90–180 days.

- Others may require all new supporting documents, including payslips, bank statements, and identification.

The downside is that if your financial situation has changed, the bank could potentially decline your loan even after it was previously pre-approved. That is why it is important to work with an experienced mortgage broker.

27. Forgetting A Few Details Can Get Your Loan Declined After Pre approval

Applying for a home loan involves a lot of documents and information. You need to provide details of every credit card, transaction account, and other financial commitments. Forgetting even a small detail can cause major headaches with banks.

Banks usually request 3–4 months of day-to-day transaction statements. If you forget to mention a credit card that has direct debits coming from your main account, the bank may view this as an undisclosed debt or liability.

A common example is an interest-free credit card you may have received from a store like Harvey Norman a few years ago — perhaps you haven’t used it in years and completely forgot about it. With some banks, undisclosed liabilities can lead to an instant loan decline after pre-approval.

How to avoid missing details

- Check your credit report: Ask your mortgage broker to get a copy of your credit file. This shows all credit enquiries over the past 7 years and can jog your memory.

- Review day-to-day statements: Your broker can go through your accounts with you to ensure no credit cards, AfterPay accounts, or other liabilities have been overlooked.

28. Banks Misunderstanding Your Expenses

Sometimes, banks misinterpret your spending. For example, if you regularly shop at Baby Bunting, they might assume you have a dependent child, even if it’s just a one-off situation like helping a friend or family member.

Case Study: Loan declined over IVF

One of our clients, Jane, was preparing to buy her first home with a significant deposit. When the bank reviewed her application, they noticed payments to an IVF clinic and assumed she had a dependent child. They declined her application outright for non-disclosure and a perceived servicing shortfall.

After explaining the situation — that she was freezing her eggs and did not have a dependent — the bank overturned their decision.

29. Being Too Young… Or Too Old

While laws such as the Discrimination Act are in place to prevent age discrimination, it’s still common for banks to ask older borrowers — typically over 45 — for an exit strategy to repay their home loan.

These age-related requirements can limit your mortgage options, depending on the lender. Some common exit strategies banks may ask for include:

- Downsizing to a smaller home once you reach retirement age

- Selling investment properties or shares to free up funds

- Using recurring income from your superannuation to make repayments

- Accessing funds from your superannuation to pay down the loan

Even if your loan is declined after pre-approval due to age, it doesn’t have to be the end of the road. Speak with our Home Loan Experts on 1300 088 065 to get your home loan approved.

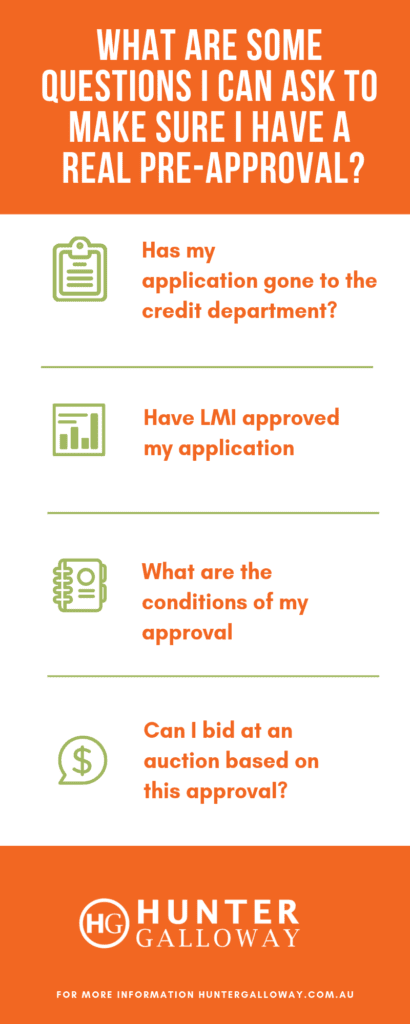

What To Do If Your Home Loan Is Declined After Pre-approval?

If your loan is declined after pre-approval, don’t panic. Here’s what to do right away — with clarity and purpose.

- Ask for a Clear Reason – Request specific feedback from your lender. Ask: “Which criteria triggered the decline?” Knowing the exact reason helps you fix it.

- Review & Correct Your Documents – Double-check your payslips, bank statements, tax returns, and credit report. Look for errors or missing liabilities. Even small undeclared debts (like BNPL or a phone bill) can hurt. Disclose any recent changes truthfully — such as a job switch or higher living costs.

- Pause Property Commitments When Necessary – If you’re under contract, discuss your decline with your conveyancer or broker. Use your finance clause or cooling-off period if the risk is too high. Don’t rush to extend or re-sign until you understand what went wrong.

- Stabilise Your Financial Profile – Avoid taking on new debt or opening new credit lines. Freeze spending to minimise risks in your transaction statements. Consider waiting a short period to reapply once you’ve corrected your issue.

How a Mortgage Broker Can Recover Your Application

A skilled mortgage broker can be your strongest ally when a pre-approval falls through. Here’s how they help you bounce back.

Strategic Lender Matching

- Brokers know which lenders are more forgiving on valuation shortfalls, credit issues, or income structure.

- They can pivot your application to a more suitable lender quickly, leveraging their lender panel.

- Their network can make or break your second chance — they may already have relationships that smooth the process.

Re-Structuring Your Application

A broker can help rework your application to strengthen it:

- Adjust how you present your income (e.g., re-classify overtime, bonuses).

- Help you improve your deposit picture (gifts, savings, genuine savings documentation).

- Identify and reduce liabilities or undisclosed debts that concern lenders.

Provide a clear, professional explanation letter for any red flags (job changes, credit hits, large expenses).

Timing Your Re-Application

- Brokers advise when your credit profile has stabilised to minimise the risk of another decline.

- They track the best moment when lender policies are more favourable.

- They help you minimise credit enquiries, reducing hard-pull hits that could hurt your score.

Bottom Line

Pre-approval is a strong start, but it’s not the finish line. Lenders re-assess in depth at the formal application stage. If things go wrong, act quickly: ask for clarity, correct your documents, and lean on your broker. With the right strategy, you can often recover and still secure that home loan.

What Happens If Your Loan Is Declined After You’ve Signed The Contract?

When a home loan is declined after signing a contract, many buyers feel blindsided and uncertain. Understanding your rights, legal exposure, and the correct steps can protect your deposit and keep your purchase on track.

Key Risks Buyers Must Understand

- Losing your entire deposit – You can forfeit it if finance conditions aren’t met or contract deadlines are missed.

- Breaching contract conditions – Failure to complete settlement as agreed can trigger legal penalties.

- Facing legal action from the seller – Sellers may pursue compensation for financial losses caused by withdrawal.

- Paying damages beyond the deposit – Extra costs may apply if the property resells for less.

- Missing settlement deadlines – Delays expose you to penalties, default notices, and potential contract termination.

Risks During Cooling-Off and Finance Clause Periods

- You can withdraw during cooling-off – Exiting early is possible, but small penalties often still apply.

- You may still lose a small penalty fee – It compensates the seller for disruption and lost time.

- Penalty fees usually range from 0.25% of the purchase price – Amounts vary depending on state law and contract terms.

- Finance clause failures can let you exit without losing your full deposit – Only following the correct process preserves this protection.

- Acting within the agreed timeframe is crucial – Missing deadlines removes legal protection immediately.

Buyer Rights vs Legal Exposure

- A valid finance clause protects you if approval falls through – It links your obligation to secure a loan.

- Without a finance clause, the seller can keep your deposit – Loan declines outside your control may not offer protection.

- Sellers can pursue additional damages in some cases – Especially if the property resells at a lower price.

How Timing Affects Deposit Recovery

- Notify all parties immediately after a decline – Prompt action demonstrates good faith and triggers legal protections.

- Provide formal evidence of loan rejection – Written confirmation from the lender is required for contract compliance.

- Follow the contract’s exact process – Deviating from the stated procedure weakens your claim to deposit recovery.

When To Engage Your Conveyancer Or Broker

Contact Your Conveyancer Immediately To:

- Assess legal standing – A conveyancer checks if your contract protections are still valid.

- Issue termination notices if required – Proper legal wording and timelines are critical for protection.

- Advise on deposit recovery strategy – Expert guidance maximises your chances of getting your money back.

Contact Your Mortgage Broker At The Same Time To:

- Explore alternative lenders – Brokers can identify other lenders who may approve your loan.

- Assess emergency approval pathways – Specialist or non-bank lenders might offer fast solutions.

- Restructure your loan application quickly – Adjusting income, deposit, or liabilities can improve approval chances.

Bonus: What Happens After Your Home Loan Is Approved?

So, you’ve got your approval letter from the bank, your loan is unconditionally approved, and your property purchase is just around the corner. What’s next? Here’s the step-by-step process after your home loan approval.

1. Sign your loan documents

This usually includes your mortgage documents, loan contracts with interest rates, general terms and conditions, and setting up your direct debits. If your contract has a finance clause, you don’t need to sign the loan contracts to go unconditional—you just need to provide the approval letter from your mortgage broker.

2. Talk with your solicitor or conveyancer

Your solicitor will have important documents for you to sign. Make sure to:

- Confirm you’ve signed your loan contracts

- Check for any stamp duty concessions or First Homeowner Grant applications

- Ensure there are no pending searches or adjustments at settlement

3. Arrange mail, power, and internet

Connect your utilities a few days before moving in. You don’t want to arrive at your new home without electricity or internet. Plan early—some services take weeks to activate.

4. Organise a pre-settlement inspection

Two or three days before settlement, inspect the property to make sure it’s in the same condition as when you first saw it. If there are issues—like a missing dishwasher or a hole in the wall—you can address them before settlement. Once settlement happens, any problems become your responsibility.

5. Celebrate (after picking up the keys!)

On settlement day, usually around 3 pm, your solicitor will confirm everything is complete. Then you can collect your keys from the real estate agent. Congratulations—you’re officially a homeowner!

Loan Declined After Pre-approval FAQs

Can a bank legally cancel pre-approval?

Yes, banks can withdraw pre-approval if your financial situation changes or new information affects risk assessment.

Does pre-approval guarantee loan approval?

No, pre-approval is conditional and depends on final checks, including property valuation, credit, and income verification.

What happens if your loan is declined after offer exchange?

You may pause or cancel the contract under finance clauses, protecting your deposit while reviewing options.

How long should you wait before reapplying?

Typically, wait until your credit, income, or documentation issues are fully resolved, often 1–3 months.

Is pre-approval the same as formal approval?

No, formal approval is granted after the lender completes all checks and valuations, unlike conditional pre-approval.

Can changing jobs cause loan rejection after pre-approval?

Yes, a significant employment change can alter your income assessment and increase the risk of decline.

Will a declined loan affect future applications?

A single declined application may temporarily impact your credit, but addressing issues can improve chances with future lenders.

Next Steps And Settling Your New Home

Our team here at Hunter Galloway is here to help you buy a home in Brisbane.

Unlike other mortgage brokers who are just one-person operators, we have an entire team of experts to help make your home loan journey as simple as possible.

If you want to get started, please get in touch here, and we can book a time that suits you – either a phone call information session or a face-to-face meeting (which doesn’t cost you anything).

More Resources For Home Buyers…

- Comprehensive first home buyer guide

- First Home Owners Grant QLD -Are you eligible?

- LMI Waivers: the definitive guide

- 22 mistakes nearly all first-home buyers make

- 16 hidden costs of buying a home in Brisbane

Note: Information is subject to change without any further notification. Any home loan application is subject to credit approval and verification of all supporting documentation. Consider this article as general in its nature and not to be taken as advice.

Start again

Start again