This is the ultimate guide to first home buyer loans in 2024. We’ll cover the fundamental first home buyer trends this year.

You’re also going to see new strategies that are working great right now.

So if you’re looking to buy a home within the next year, you’ll love this new guide.

Let’s dive in…

Table of Contents

What should I look for in a loan?

Not all loans are created equally.

Today, lenders often fall into a few different categories:

- lenders who offer the best interest rates,

- lenders that provide extras or

- Lenders that have a specific minimum deposit amount.

In this section, we’ll cover everything you need to know.

How do I differentiate between loans?

If you’re unfamiliar with the home loan process, then this will all be new to you.

But don’t sweat it; there are a few simple ways to differentiate between loans.

You can ask the following questions:

- Does the lender specialise in first home buyer loans? Most don’t, so it’s quite rare if you find one that does.

- Does the lender offer competitive interest rates? Interest rates can be a real sting if they’re high. So look for a lender that offers a lower interest rate that leaves you with smaller repayments. Watch out for introductory rates, which often increase a lot once the initial period ends.

- Does the lender offer low deposit loans allowing a deposit of 10% or smaller? Yes, it is possible to find a lender that provides loans for those with a deposit UNDER 20%. Some lenders even allow a loan-to-value ratio of between 90 to 95%. Speak to Hunter Galloway about these types of loans. But don’t forget, if you’re paying a deposit under 20%, you’ll have Lenders Mortgage Insurance which will be added to your loan.

- Does the lender offer extra bells and whistles? Additional features like an offset account or redraw facility can help you in times of need. In many cases, the “typical first home loan” doesn’t come with many extras. So this is something to think about.

- Does the lender offer principal and interest (P&I) repayments? If you can, try to get a loan that allows you to pay P&I because these types of loans often provide lower interest rates.

First home buyers assistance: I am still working towards a deposit…

Just like so many Millennials, the idea of having a deposit to buy a home can seem a little far off. If you’re still working hard to save up your full deposit, here are a few strategies. These are the same strategies that have helped hundreds of first-home buyers to supercharge their savings.

- Apply for the First Home Guarantee Scheme (formerly known as First Home Loan Deposit Scheme). Under the scheme, buyers will not need to pay Lenders Mortgage Insurance. Deposits as low as 5% can be put down. The best part is that this scheme can be used together with the First Home Buyers Grant and First Home Super Saver Scheme.

- Gift of inheritance. You can use a cash gift or inheritance as part of your deposit. However, the lender will still want to see some genuine savings to show that you can financially support yourself while paying your mortgage.

- Sell what you can. Any assets or items sitting around the house should be sold! This will help you boost your short-term savings goals.

- Get a guarantor. Your parents are eligible to guarantor you if they own a property and have equity in it. This can be used for part of your deposit and will avoid LMI costs.

Should I get a guarantor?

Guarantors are a great way to help first home buyers enter the market. Usually, parents will act as guarantors and use the equity from their current property to put towards the child’s deposit.

Getting a guarantor means that you can get into the market sooner and avoid LMI.

We recommend guarantors on a case-by-case basis. There is no right answer.

While they are a great idea if both parties are in the right financial position, there is also a level of risk involved. You will need to be able to prove that you can pay off the loan. Because if you default and can’t pay back the loan, this will cause financial strain on the guarantor.

Be realistic about what you can afford.

We see many first home buyers overestimate and look at properties beyond their realistic budget. Start by speaking with your broker about how much you can afford to spend, especially if you don’t mind the odd martini on a Saturday and your lifestyle matters. These ‘little’ extra expenses come into play when figuring out your budget.

There’s a difference between the maximum you can borrow and how much you can afford. Looking at what you can afford takes into account how your lifestyle expenses will fit in with your home loan.

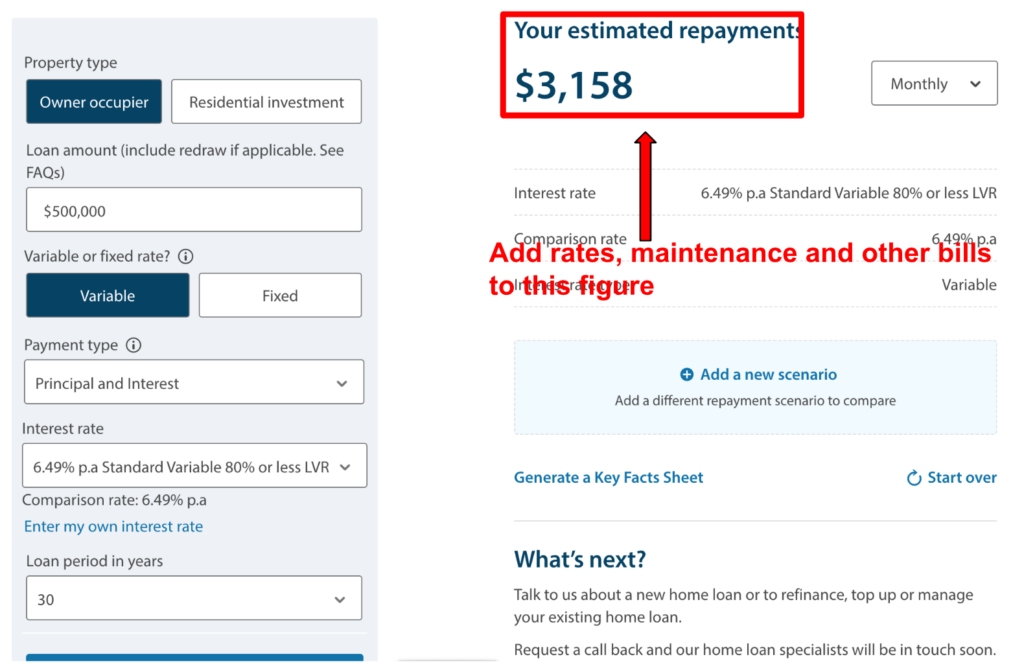

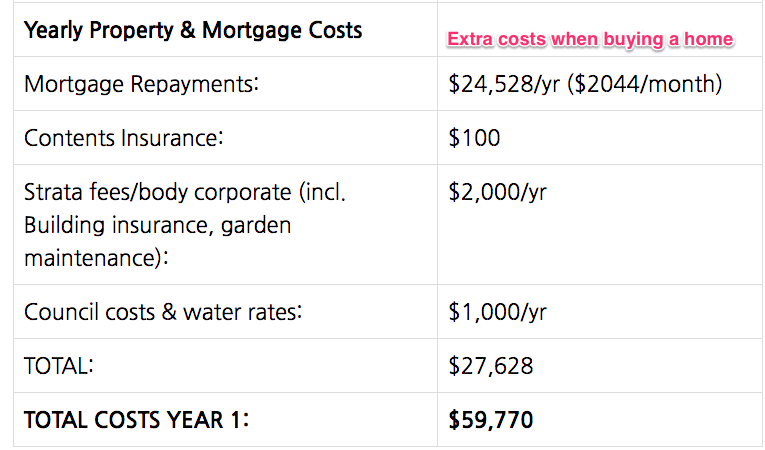

When it comes to figuring out your home loan repayments, you will also need to add on the extra costs like rates, electricity, maintenance, water bills, insurance, and potential body corporate fees. These additional costs can make your monthly budget much more than your regular rental payment.

Lenders Mortgage Insurance (LMI)

The old, dreaded LMI.

Lenders mortgage insurance is insurance for the lender (not you). If you are borrowing over 80% of the property’s value, you will be required to pay LMI. But you will be exempted from LMI if you have applied for the First Home Buyer Deposit Scheme.

LMI protects the lender if you can no longer pay your loan. While it isn’t insurance for you, it merely allows you to buy a property with less money. it doesn’t change your responsibility when it comes to paying off the loan.

What about different loan definitions?

There are so many new terms new buyers have to learn. Fixed-rate or variable rate? Well, what’s the point of being given a choice if you don’t know the difference?

So make it easier with this little cheat sheet.

Fixed-rate:

A fixed rate is when the bank/lender confirms and fixes the interest rate over a specific period.

It usually falls within a 1-year, 3-year or 5-year timeframe. Over this period, your mortgage repayments will be consistent because there is no way for your interest rate to change.

Fixing rates is a great way to gain stability around your repayments and lock in a solid interest rate. The downside? If the interest rates fall significantly, you won’t be able to get a better rate until your fixed-rate period is over. Also, fixed rates may have high break costs.

Variable-rate:

A variable interest rate will change with the Reserve Bank’s cash rate. Other rules and regulations will affect it too.

Being on a variable rate can be great if interest rates drop rapidly, so you reap the benefits. But it also means that your repayments will increase if interest rates increase…

Principal and interest repayments:

This type of repayment allows you to pay for both the interest and the principal of the loan. So during the term, you will be paying off both your mortgage debt and the interest. Principal and interest repayments are a typical home loan structure and the recommended set-up.

Interest-only:

This type of loan charges you just for the interest you are accruing on your loan. So you won’t be making any payments towards your mortgage.

It is the minimum repayment allowed on your loan. Unfortunately, when this interest-only period ends, your repayments will go up. When you sign up for a loan, you will have been given a loan term (usually 30 years). So if you stop paying the principal for, let’s say, one year, this outstanding amount will be added to your future repayments. So while interest-only repayments have a short-term gain, they sometimes provide long-term pain.

Home loan packages

Home loan packages bring together your accounts into one. It combines your mortgage/home loan with your transaction account and any other extras. These types of packages can make life much easier!

What should I be aware of when buying a property?

Many first home buyers fall in love with a home. And what does love do? It removes our ability to reason.

In this section, we will cover what you need to be aware of when buying a property….

Don’t just jump into buying; understand that it could take years.

Just because you’re financially ready to buy doesn’t mean you should rush into the first property that seems like a fit.

For some people, finding the perfect property can take up to two years.

The best advice we can give is: don’t rush it!

Even though you’ve inspected and applied for so many properties, don’t just settle because you are now tired and frustrated.

When you’ve found the right property, make sure you go through all the stages involved in buying a house.

One of the most important stages is Building and pest inspections! Do not skip out on this stage; it can be a great way to lower the price due to what the report comes back with. And do you really want to buy a termite-infested home without knowing it?

Negotiate the house price!

Remember that the real estate agent is on the seller’s side, not yours.

Negotiating the house price may help you save 5% to 10% of the purchase price!

If you are not a good negotiator and need some assistance with the buying process, consider getting a buyers agent.

When negotiating, the ball is in your court as the buyer. Remember that even though it may be just an extra $10,000 you’re negotiating over, if you add a 30-year loan term with interest to that, the amount you save goes up.

Never feel pressured by the real estate agent.

You can often be in a position where the real estate agent is pushing you.

They might mention that they have been inundated with other offers, but remember, they’re working for the seller, not you. They are not trying to get you to buy the house that best fits you – they are trying to get a fast sale and land the deal at the highest price possible for the seller.

So they may put pressure on you. If you’re feeling rushed, take a step back. It is better to leave it and move on than make a decision you may regret.

This all sounds too hard; what should I do?

Is buying a home the only option? It sure looks like it. But if you cannot afford to buy where we want, we have another solution for you: Rentvesting.

. Did you know that…

- 71.4% of households owned a home in 1994/1995

- This dropped to 68% of households that owned a home in 2015/2016

- Young people are looking for new ways of investing.

This is where rentvesting comes in.

Rentvesting

The latest investment strategy for first home buyers is rentvesting.

Rentvesting is where you buy a property to invest but rent somewhere you prefer to live — giving you the best of both worlds.

But what are the positives and negatives?

Positives:

- Buying a property that you can afford sooner.

- Investing in an up-and-coming suburb

- Using this property to gain equity

Negatives:

- You still will be renting

- You may need to hold the property for quite some time until it goes up.

- You will need to get tenants in right away to help with affordability.

When it comes to rentvesting, research is critical. You will need to figure out the suburbs that are still sitting at a lower purchase price and try to predict the future of the property market.

Be strict about what you’re looking for, and remove any emotional attachment.

It is purely an investment.

We advise speaking to a mortgage broker and financial planner before going ahead with rentvesting.

Next steps and getting your home loan

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again