This is a comprehensive guide on Home Loans for Doctors in 2026.

Doctor Home Loans: Complete Guide 2026

The best part?

We will show you how to understand Doctor Home Loans, the different bank (and non-bank) policies and interest rates that apply right now (in 2022) across the Australian lending market. So, if you are a Doctor and want a mortgage with the best interest rate, you’ll love this guide.

Let’s get started.

How much can I borrow?

As a Doctor or Medical Professional, you can borrow much higher amounts than the regular public.

This is because the banks see your profession as a much lower risk than the general population

You can:

- Borrow up to 90% LVR and pay no LMI with the broadest lender range; a small number of select lenders may offer up to 95% under stricter criteria

- Borrow up to 90% of the property’s value and pay no LMI (largest range of lenders, less strict criteria)

- Borrow up to $4.5 million to purchase a home to live in or investment property.

In other words, if you are buying a $1 million home, you do not need any deposit and only require some savings to cover stamp duty costs.

If the property is valued at over $5 million, we have lenders and banks that will look at these on a case by case basis.

What types of Doctors are eligible?

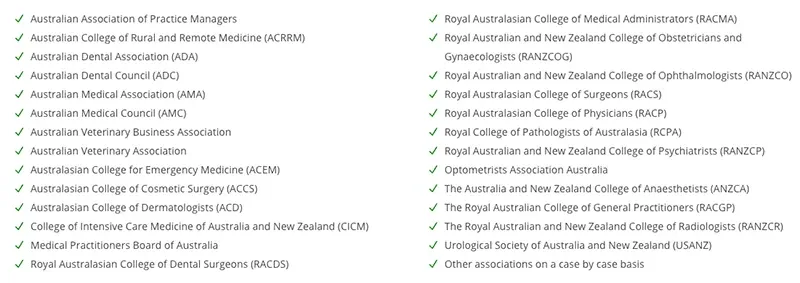

In most cases, you will also need to belong to one of the following associations:

We also work with BOQ Specialist who can provide these special offers to Allied Health Professionals, including any of the following jobs:

- Chiropractor

- Osteopath

- Optometrist

- Physiotherapist

- Pharmacist

- Dental Tech

- Podiatrist

What happens if my profession isn’t on the list?

Not all medical professionals are eligible for the same doctor home loans. Some, including naturopaths, psychologists and medical research scientists, won’t be able to access the same concessions.

The major banks have identified these medical streams as less stable and higher risk. However, it’s not all bad news. Even if you don’t qualify for the same benefits as other medical professionals, you might still be able to negotiate a lower interest rate—especially if you have decent employment history and significant savings!

Are there any benefits on mortgages for Doctors?

Home loans for doctors come with significant perks, including zero Lenders Mortgage Insurance. Our medical mortgage broker team can help you qualify for a range of special benefits, including:

- Interest rate discounts – Our medical mortgage brokers can help you get interest rates that are significantly lower than advertised.

- Asset protection – Our team will help you qualify for increased asset protection by letting you borrow in a trust.

- Faster wealth creation – Using a range of strategies, we can help you develop a wealth creation plan that involves fast repayment of your mortgage.

Why do the banks waive LMI?

The average person usually has to pay lenders mortgage insurance (LMI) if they borrow more than 80% of the value of the property they’re buying.

LMI is a once-off fee that insures banks against losses in cases where you can’t repay your mortgage.

However, medical professionals are seen as low-risk borrowers and don’t usually have to pay LMI. Doctors rarely miss mortgage repayments because of their high income and good employment prospects.

Home loans for doctors and other medical professionals can also come with other perks that aren’t available to the general public.

For example, a young medical professional may be able to borrow up to 105% of the value of their property if their parents are willing to act as guarantors.

Read More: How do Guarantor Home Loans work?

How much will I save by avoiding LMI?

The average person will be forced to pay huge amounts of LMI on luxury properties. LMI premiums skyrocket on purchases over $1 million.

As a medical professional, you could save thousands on LMI. If you find the right doctor home loan, the standard professional waiver is available up to 90% LVR, with a small number of select lenders offering up to 95% under stricter criteria.

If you’re planning on buying a luxury property, you could be forced to pay huge amounts of Lenders Mortgage Insurance. But, by looking at a bank that does not charge medical professionals LMI, you can save the following:

| Property Price | No LMI Saving |

| $450,000 | $8,476 |

| $950,000 | $24,231 |

| $1,450,000 | $41,604 |

| $1,950,000 | $51,267 |

Case Study: The Medical Mortgage Broker

Natalie and Shaun are both Doctors who have been working for the past few years. Natalie has recently been promoted in her work and received a significant income boost.

They were both renting and had enough savings to cover their stamp duty but didn’t have any deposit.

They found the perfect home for $1.25M and wanted to purchase it without going down the guarantor home loan path.

Solution:

Hunter Galloway we were able to source a 90% no-LMI home loan, with the remaining contribution assessed separately under the lender’s criteria.

This was structured:

- – 90% Home Loan over 30 years = $1.1250M loan

- – 10% Top up loan over 8 years = $0.125M loan

- – Total lending $1.250M

With Natalie’s new job, she expects to pay off the top-up loan within 3 years.

How To Maximize Your Interest Rate Discounts.

In this section, we talk about saving you some serious cash.

Why do Doctors get discounted interest rates?

As a doctor, you’re a very attractive prospect for lenders. Most medical professionals have a high income and good job prospects, making them very low-risk borrowers.

This has resulted in numerous lenders creating special home loans for doctors. Our medical mortgage broker team can help you negotiate a reduced interest rate and no LMI.

If you’re buying a property worth $900,000, you could save up to $25,000 on LMI. Similarly, you might not need a deposit, which means that you won’t need a huge amount of available capital to purchase a relatively expensive property.

Maximizing your discounts

Our medical mortgage brokers can help you get the best deal on home loans and mortgages for doctors:

- Ask about other discounts if you’re buying a commercial property or medical practice loan.

- Ask your broker which lenders offer the best interest rates/deals for doctors.

- Make sure your broker is willing to negotiate.

- Ask about hidden service fees.

- Focus on getting LMI waived if you’re borrowing more than 80% of the property’s value.

- Focus on minimizing interest rates if you’re borrowing less than 80% of the property’s value because you won’t pay LMI anyway in this case.

What income is considered acceptable?

Doctors and other medical professionals can sometimes have strange income structures that banks don’t like. This can include things like being self-employed or partnership style businesses.

Likewise, medical professionals often work as contractors or subcontractors. This means that they work as needed and earn according to their workload.

Just because you’re a contractor or are self-employed doesn’t mean that lenders will reject you.

Our medical Brisbane Mortgage Brokers will help you get the best home loan for doctors. You shouldn’t have any problems as long as you can prove that you have a regular, ongoing income.

Finding the right lender

In this section, we’ll share the tactics we use to find the right lender for you.

When you find the right lender that fits with you, you’ll usually find you will receive a sharper interest rate and better terms.

Every lender has a different approach to mortgages for doctors, including the type of properties they specialize in and how they will verify your income.

All lenders’ policies are constantly changing, so it’s hard to give a broad-brushed ‘this lender will be right for you’ answer here.

In other words, each application and situation is unique.

What we’ve done below is give you a high-level overview of the current home lending market for Doctors in Australia, with the various banks and their areas of expertise.

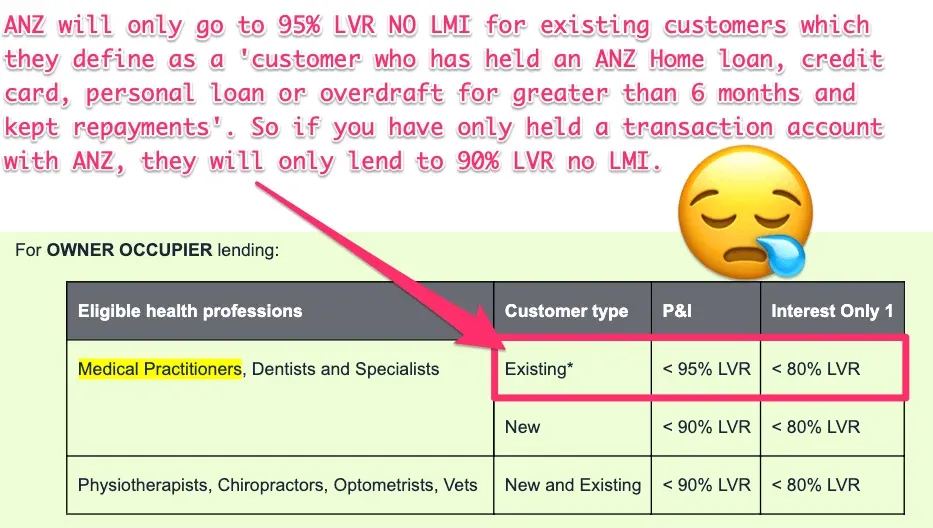

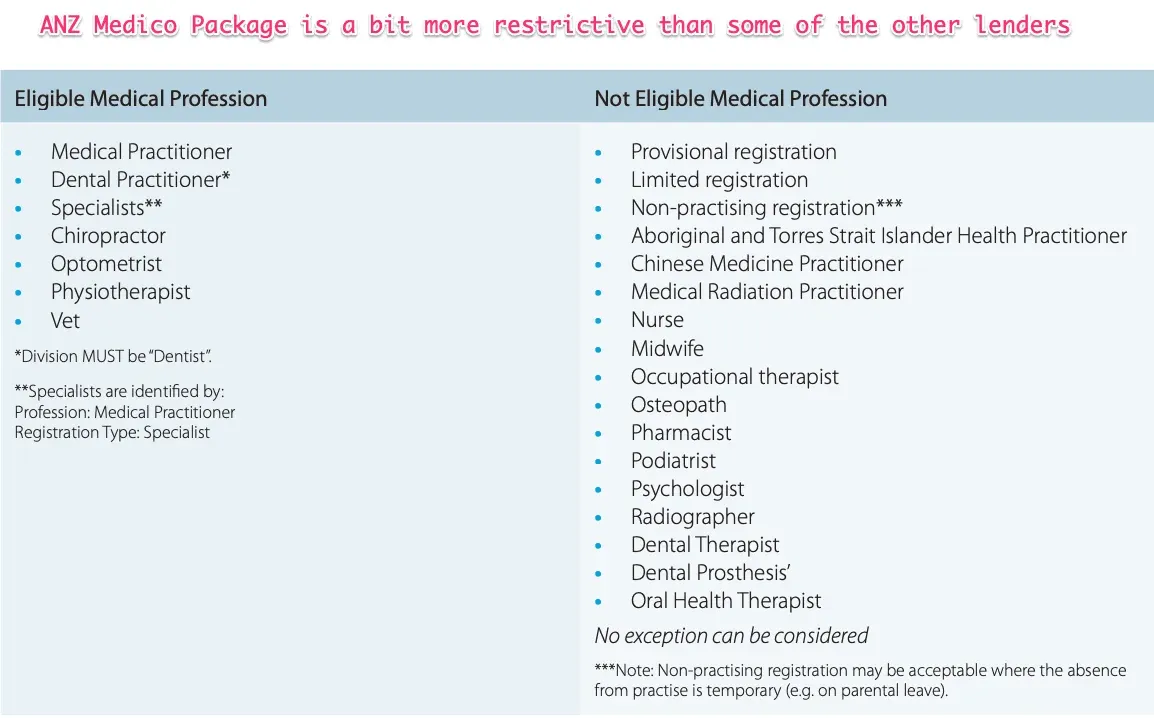

ANZ medico package

- Borrow up to 95% of the property value with no LMI – Only eligible for existing ANZ customers who are Medical Professionals, Dentists and Specialists. Principal and interest loan repayments for a home to live in.

- Borrow up to 90% of the property value with no LMI for new ANZ bank customers.

- Need to be registered with theAustralian Health Practitioner Regulation Authority.

- Eligible to receive higher interest rate discounts on loans up to 90%

- 5% Genuine savings is required to be shown.

- Pay no Lenders Mortgage Insurance up to 95%.

- Maximum loan amount is up to $2.70M per property, up to $3M property value.

Eligible Professions include:

- Medical Practitioners

- Dentists

- Medical Specialists

- Physiotherapists

- Chiropractors

- Optometrists

- Vets

Read More: ANZ Health

CBA medical professional offer

- Borrow up to 90% of the property value with no LMI (technically 89.99%).

- Need to be registered with Australian Health Practitioner Regulation Authority

- Eligible to receive higher interest rate discounts on loans up to 90%.

- Pay no Lenders Mortgage Insurance up to 90%.

- Maximum loan amount is up to $5M.

Eligible professions include:

- Anaesthetist

- Cardio Thoracic Surgeon

- Cardiologist

- Clinical Pharmacologist

- Cosmetic Surgeon

- Dentist

- Dermatologist

- Ear and Throat Surgeon

- Emergency Surgeon

- Endocrinologist

- Gastro Intestinal Surgeon

- Gastroenterologist

- General Practitioner (also known as Medical Practitioner)

- General Surgeon

- Gynaecologist

- Haematologist

- Hepatologist

- Immunologist

- Nephrologist

- Neuro Surgeon

- Neurologist

- Obstetrician

- Oncologist

- Ophthalmologist

- Optometrist

- Oral and Maxillofacial Surgeon

- Orthopaedic Surgeon

- Orthopaedic Registrars

- Otolaryngologist

- Paediatric Surgeon (Neonatal/Perinatal)

- Pathologist

- Plastic Surgeon

- Pharmacist

- Psychiatrist

- Radiologist (Note: this does not include Radiographers)

- Reconstructive Surgeon

- Respiratory/Thoracic Surgeon

- Rheumatologist

- Surgeons

- Urologist

- Vascular Surgeon

- Veterinarian

If you are a vet and looking for a mortgage with the CBA you need to be a member of your association.

Read More: CBA Healthcare Banking

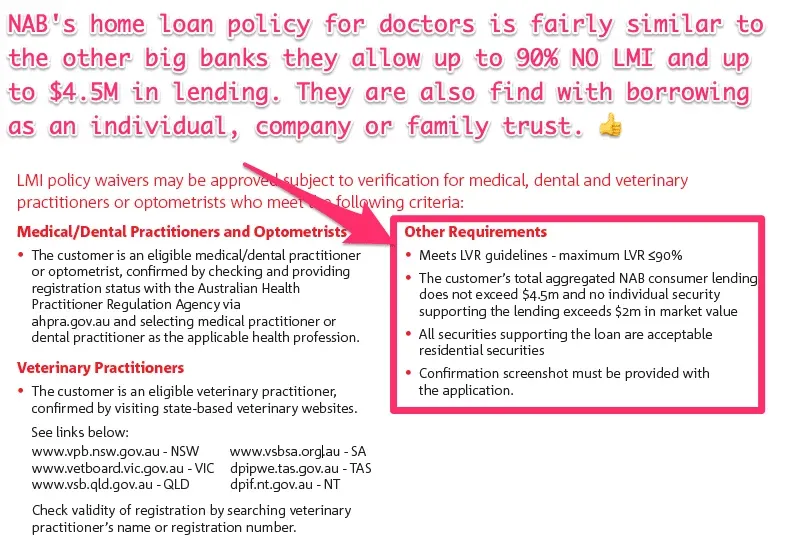

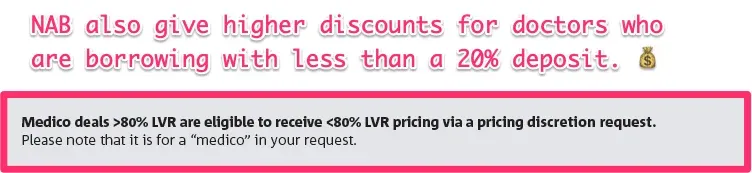

NAB Healthcare Professional Package

- Borrow up to 90% of the property value with no LMI (technically 89.99%).

- Need to be registered with theAustralian Health Practitioner Regulation Authority.

- Eligible to receive higher interest rate discounts on loans up to 90%.

- Pay no Lenders Mortgage Insurance up to 90%.

- Maximum loan amount is $4.50M.

Eligible professionals include

- Medical Practitioners

- Dental Health Practitioners

- Veterinary Practitioners

- Optometrists

Veterinary Practitioners must be registered with:

- NSW – www.vpb.nsw.gov.au

- VIC – www.vetboard.vic.gov.au

- QLD – www.vsb.qld.gov.au

- SA – www.vsbsa.org.au

- TAS – dpipwe.tas.gov.au

- NT – dpif.nt.gov.au

Read more: NAB Healthcare

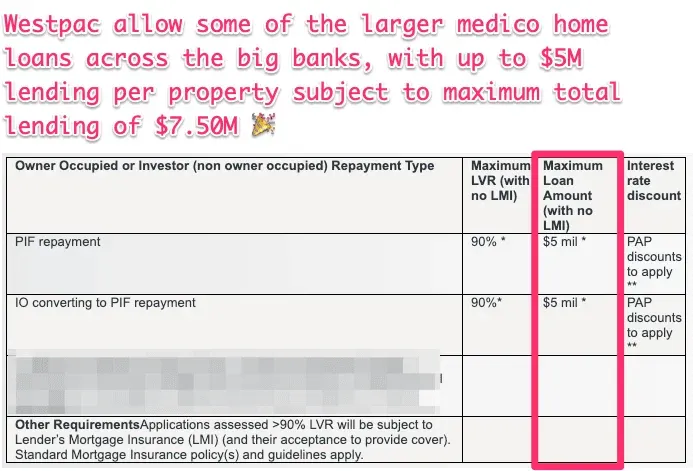

Westpac doctor home loan

- Borrow up to 90% of the property value with no LMI (technically 89.99%).

- Need to be registered with theAustralian Health Practitioner Regulation Authority

- Eligible to receive higher interest rate discounts on loans up to 90%.

- Pay no Lenders Mortgage Insurance up to 90%.

- Confirmation and validation of 5% genuine savings are not required for Doctor Home Loans.

- Maximum Loan amount without LMI is up to $5 Million, or up to $7.50M in total lending.

Eligible professions include

- Dentists

- General Practitioners

- Hospital-employed Doctors (e.g. Intern, Resident, Registrar, Staff Specialist)

- Medical Specialists - refer to this page for the list of acceptable Medical Specialties.

- Optometrists

- Pharmacists

- Veterinary Practitioners

Read More: Westpac Healthcare Doctor Loans

Bankwest Medical Practitioner Package

- Borrow up to 90% of the property value with no LMI (technically 89.99%).

- Need to be registered with theAustralian Health Practitioner Regulation Authority

- Eligible to receive higher interest rate discounts on loans up to 90%.

- Pay no Lenders Mortgage Insurance up to 90%.

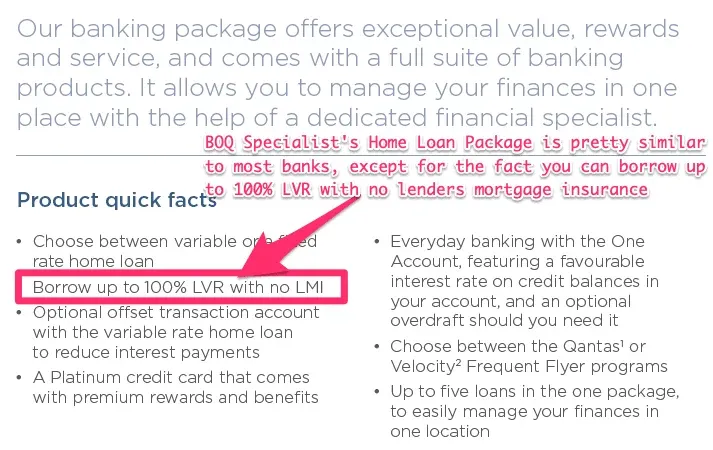

BOQ specialist home loan

- Borrow up to 90% of the property value with no LMI as the standard policy; a small number of select lenders may offer up to 95% under stricter criteria.

- Need to be registered with theAustralian Health Practitioner Regulation Authority

- Eligible to receive higher interest rate discounts on loans up to 90%.

- Pay no Lenders Mortgage Insurance up to 100%.

- BOQ Specialist home loans

Read More: BOQ Specialist Home Loan review

What if my profession isn’t on the list?

Home loans for doctors are not available to some medical professionals. This is because banks have completed a statistical analysis of their existing loan portfolios and have identified certain professions to be a higher risk. These professions include:

- Psychologist

- Medical research scientist

- Naturopath

- Nurse

Even if you don’t qualify for a specialist loan, other options are available for you. If you have a strong employment history and substantial savings, contact us or book a free assessment to find out what options are available.

Other questions to consider-fixed or variable rates?

You can choose from fixed or variable rates. Fixed-rate loans are for those who want certainty and are a bit more risk-averse. If you want to remove any volatility from your interest costs and are comfortable with the current rates, you should consider fixed rates.

On the other hand, if you are comfortable with a little bit of volatility and want to make additional repayments to your loan, a floating or variable rate home loan could be the way.

If you are building a home, you will need to use a variable rate loan.

Why do fixed rates have an early repayment cost?

Fixed rates home loans are a contract between you, the borrower, and your bank.While they give you the certainty of repayment for that set period, they also give your bank certainty about the interest repayments they will receive over the fixed-rate term. This lets the bank make hedging and funding arrangements to match.

The bank will incur interest costs in making these hedging and funding arrangements. If you repay some or all of your fixed-rate early or want to switch before the end of the fixed term, the bank will need to change the funding arrangements.

For this reason, the bank will charge you an Early Repayment Cost to recover the banks’ reasonable estimate’ of the costs in changing the arrangements.

Case Study: Fixed Rate Break Costs

Tom takes out a 2 year fixed rate loan of $500,000 at an interest rate of 7%. One year later, Tom decides to repay the loan fully, and at that time, the interest rates in the market are 5%.

Tom will need to pay roughly $9785 ($1957 per $500k early repayment) for breaking the fixed rate.

Read More: Is now a good time to fix rates?

Product features of home loans for doctors

In this section, we will show you some of the features of home loans for doctors. First, we will show you the basic features. Then we will teach you the quickest (and EASIEST) way to find the right loan features for you.

Features on Mortgages For Doctors

Home Loans for doctors are similar to regular mortgages:

- Entities: Individuals, trusts or companies as the owner.

- Loan term: Up to 30 years for residential properties or 25 years for commercial property loans.

- Interest-Only Period: Up to 10 years is acceptable.

- Extra repayments: Available on variable facilities.

- Offset accounts: Available with some lenders allowing multiple offset accounts.

- 90% LVR: Standard for eligible applicants, with a small number of select lenders considering up to 95%.

- Redraw: Sometimes available, depending on the lender.

- Cash Out: Available, depending on the purpose.

- Capitalised Interest: Available, depending on the purpose.

- Internet Banking: Available.

Different lenders have different target markets, so their product features will ultimately depend on this.

As a Doctor, can I get an interest-only no LMI home loan?

The answer is YES, you can.

However, there are certain things you have to consider before getting an interest-only doctor home loan. Let’s start by learning what interest-only loans are and how they work.

Interest Only Home Loans

An interest-only home loan allows the borrower to only make interest payments for the first few years without any increase in the principal amount.

However, once the interest-only term period is over, they are required to make both principal and interest repayments.

Regulatory authorities in the industry have imposed stringent policies encouraging banks to slow down on interest-only home loans. But you can still qualify for one, depending on the following factors:

- Purpose of a loan

- How much the loan amount is as a percentage of the property value (LVR), and

- The lender you go for.

Interest-only home loans are normally beneficial for real estate investors who want to improve their cash flow and are looking for a buffer period during which they can invest money in building a house or for other purposes.

How do Interest Only Loans Work?

When you apply for this loan type, lenders do not consider the interest-only term period while calculating your borrowing power. For example, if your loan term is 20 years, with 3 years of interest-only payments, the lender will assess your borrowing power on a 17-year loan term.

Since the interest-only repayments are small, most banks do not allow fortnightly or weekly payments. Instead, you are required to make monthly interest repayments.

While you get immediate cost savings with an interest-only home loan by paying small repayment amounts—once your interest-only period is over, you will still owe the same principal amount as you did in the beginning, unlike a standard loan.

Interest-only home loans do not reduce the principal or balance during the interest-only period.

No LMI and Interest Only Doctor Home Loan

If you intend to get an interest-only doctor home loan for investment purposes and get an LMI waiver, you can save a lot of money that you can invest elsewhere. It will give you a huge cash flow for planned investments in the future. In addition to that, your status of being a medical professional also plays a vital role in getting you a lot of other perks.

It is important to know that naturopaths, medical research scientists, and psychologists are not included in the list of medical professionals.

Apart from an interest-only doctor home loan, you can also choose to go for no LMI loan with discounted interest rates. You can save thousands of dollars if LMI is waived. In fact, with other discounts, such as reduced interest rates, you can save a lot more money.

Ability to make extra repayments

Being a Doctor, you are likely to have regular overtime, and if you structure your home loan in the right way, you can cut years from the loan by simply making $500 per fortnight in extra repayments.

According to ASIC:

“Anything extra you pay in the first 5 to 8 years (when most of your payments go towards paying off the interest) will cut your interest bill and shorten the life of your loan. Don’t delay paying off your home loan if you can. Instead, try to make small regular extra repayments.”

Read More: How to cut 7 years from your loan term with extra repayments.

Multiple Offset Accounts

Offset accounts are like a normal transaction account, but instead of earning interest, they save you interest on your home loan.

The question is can you have more than one offset account, so every dollar you have reduces your interest costs?

Here’s a great example of multiple offset accounts in action:

See how this couple has got all of their different accounts working to reduce the interest on their home loan? Clever… and super effective.

Multiple mortgage offset accounts are particularly handy if you have more than one transaction account, like an investment property that receives rent.

Read More: What is the benefit in using an offset account?

Increasing Your Repayment Frequency

Most banks, by default, give you monthly repayments. So in a year, they will assume you make 12 repayments.

Let’s say your monthly repayment is $2,000.

In a 12 month period you will make $2,000 x 12 months = $24,000 in repayments. Simple right?

If you switch to bi-monthly (also known as fortnightly) repayments, you will make an extra 2 repayments without even realizing it.

So you make a $1,000 payment ($2,000 divided by 2) every fortnight, of which there are 26 fortnights per year. This is equal to $26,000 per year in repayments!

You will make an extra $2,000 in repayments per year without even realizing AND save 4 years and 4 months from your loan!!!

Read More: Pay Off Your 30 year Home Loan 6 Years Faster ![]() [10 Easy Tips]

[10 Easy Tips]

Check to see if you are eligible for a home loan

Choosing a Lender (including bonus case study)

In this chapter, we will deep dive into “The HG Process”.

We have used this technique to negotiate hundreds of thousands in savings for clients again and again

We have also seen many other people use the HG process to get similar results.

So without further ado, let’s get started…

What is the regular process of getting a mortgage for Doctors?

Most Doctors will go back to the bank they’ve always banked with—CBA, Westpac, and all the regulars. There is nothing wrong with this if you have a big deposit and want to pay whatever interest rate they decide to offer.

However…

Put your best foot forward

As we have mentioned, the banks’ method to review Home Loans for Doctors can sometimes be complicated, depending on your income source and if you are relying on future (potential) earnings.

So determining which lender is right for you really comes down to what you want to achieve and then matching that outcome with a bank or lender that specializes in that market niche.

It is critical that as a Doctor or Specialist, you don’t just fill out a bank application form and email your paperwork.

You want to show the strengths of your application, your present situation and show why the bank should give you the money.

At Hunter Galloway, we do this using our Credit Memo, which highlights:

- A Deal Summary.

- Overview of the security property, the location and why it’s good security.

- Overview of income and the servicing position.

- Overview of you and your employment background

- Key People involved with the transaction—your lawyer, accountant and other team members

- Valuation, Financials and other supporting documentation

Including all of this information can present a stronger case to the bank and mitigate any concerns their credit team might have around the purchase and your ability to repay the loan.

Other Products for Medical Professionals

What are some other features and products that are important for Doctors and their finances?

Good question. We answer that and more in this section.

Buying a Medical Practice

As a doctor or other medical professional, you might want to start your own practice. Although a lot of work, your practice can be financially and personally rewarding.

Below we’ll have a quick look at medical practice loans and how to get the best deal when you’re setting your new practice up.

How do banks look at medical practice loans?

Banks look at several factors when deciding whether or not to approve a medical practice loan.

- Whether or not you have a medical qualification and at least a few years of relevant experience.

- Evidence of a Medicare provider number.

- Proof of registration to the Australian Dental Association (for dentists) or the Veterinary Surgeons Board (for vets).

- How many assets you have behind you. Generally, the more, the better.

Speak to our medical mortgage brokers to find out more.

How much can I borrow to start a new practice?

Starting a new practice is costly, and the amount you can borrow will depend on many factors.

A medical practice property loan will allow you to borrow up to 100% of a freehold property value with a maximum term of 25 years.

A medical practice business loan will allow you to borrow up to 100% of your business value (in leased premises), including the equipment and fit-out costs, for 10 years.

You may be able to find a low doc loan (which involves no proof of income). Interest-only and principal + interest repayment options should be available, depending on your circumstances.

Interest rates will vary according to the strength of your application, and our experienced medical mortgage brokers will help you get the best deal possible.

Mortgage Broker or Bank

Home Loans for Doctors can be more complicated than typical residential lending. You may receive regular overtime or allowances that most banks do not understand or know how to utilize.

This is further complicated by banks not publishing their interest rates and constantly changing lending policies. It’s one of the many reasons high net worth investors deal with our specialist Medical mortgage brokers when purchasing a home or investment property.

Should I use a mortgage broker?

Being one of Australia’s top Mortgage Brokers, we see some of the best rates on offer— the kind that banks do not openly advertise.

We help our clients by allowing them to leverage our:

- Highly Experience. We have helped hundreds of property owners and investors across Australia, lent over $1 billion and ranked in Australia’s Top 15 Mortgage Brokers. We can definitely help guide you through the process.

- Home Loan Specialists. Our Mortgage Brokers are highly specialized medico lending experts. We have worked in the bank’s credit departments, and we understand the type of finance that will get you the best result.

- Deep Industry Relationships. Having been in the industry for over 10 years, we have deep industry relationships—from the Heads of Banking in the major banks to individual credit managers who make decisions on your application. Knowing the right person in the bank can make a world of difference to your application.

- Sharp Pricing. At Hunter Galloway, we deal with Doctor Home lending scenarios every day, so we understand the current market. When a loan is submitted to a bank by a broker, the bank knows they need to be competitive to get the deal.

- Flexible lending policies. As detailed above, we have access to 30+ residential and specialty lenders, each with different risk appetites and funding sources. This ultimately provides you with funding from different lenders, meaning less restrictive terms.

Won’t I get a better deal going directly to the bank?

You might be surprised to hear, but we will be able to negotiate a cheaper deal with your bank than if you went to them directly.

Private Bankers and Relationship Managers are remunerated on portfolio growth and their return on equity.

In other words, in Private Banking, the bankers are focused solely on the bank’s profit.

What this means for you is that you can miss out when you deal with the Banker directly.

If, for example, you are in a challenging situation or looking for a higher LVR – they can use this as an excuse to overcharge you.

Because the industry is so opaque, it’s difficult to know what the bank’s competitors are charging, so often your bank will charge as much as they can…

When have they ever told you a competitor has a better interest rate?

The Hunter Galloway Medical Mortgage Broker team is here to help. We have a team of home loan experts, and we have all worked for banks previously and understand what they want to see to approve your doctor home loan.

How does a mortgage broker help?

In the first instance, we will chat to understand your situation and see if we are a good fit. Then we will go through the following steps with you:

- Once we have all your documentation and understand what you want to achieve, we can then negotiate with our panel of lenders to see who will be in the best position to provide the best terms at the best interest rates.

- We will collate the different bank’s responses and provide you with the indicative terms comparisons to choose the best lender and recommend an option to move forward with.

- Using ‘The HG Process’, we will approach the banks for a final round offer, showing them where their offer sits in the market and using this to negotiate further reductions in their margin and movement with their LVR and term.

- At this point, we can instruct a valuation and get that process moving, and we can speak with your accountant and solicitor if required.

- We will follow the bank through to formal approval, instruct loan contracts to be issued and assist with getting these documents signed for settlement.

How much do mortgage brokers cost?

While some mortgage brokers charge a mandate fee, we do not charge any fees. We are paid commissions by the bank to settle your doctor home loan.

If you would like to discuss your lending options, get in touch today.

Would you like to learn about your situation?

Frequently Asked Questions

1. Do you need to be a member of a medical association?

As a doctor, you must be a member of an Australian association. Hunter Galloway will speak to you about the list of associations eligible such as the following:

- Australian Association of Practice Managers

- Australian College of Rural and Remote Medicine (ACRRM)

- Australian Dental Association (ADA)

- Australian Dental Council (ADC)

- Australian Medical Association (AMA)

- Australian Medical Council (AMC)

- Australian Veterinary Business Association

- Australian Veterinary Association

- Australasian College for Emergency Medicine (ACEM)

- Australasian College of Cosmetic Surgery (ACCS)

- Australasian College of Dermatologists (ACD)

- College of Intensive Care Medicine of Australia and New Zealand (CICM)

- Medical Practitioners Board of Australia

- Royal Australasian College of Dental Surgeons (RACDS)

- Royal Australasian College of Medical Administrators (RACMA)

- Royal Australian and New Zealand College of Obstetricians and Gynaecologists (RANZCOG)

- Royal Australian and New Zealand College of Ophthalmologists (RANZCO)

- Royal Australasian College of Surgeons (RACS)

- Royal Australasian College of Physicians (RACP)

- Royal College of Pathologists of Australasia (RCPA)

- Royal Australian and New Zealand College of Psychiatrists (RANZCP)

- Optometrists Association Australia

- The Australia and New Zealand College of Anaesthetists (ANZCA)

- The Royal Australian College of General Practitioners (RACGP)

- The Royal Australian and New Zealand College of Radiologists (RANZCR)

- Urological Society of Australia and New Zealand (USANZ)

- Other associations on a case by case basis

2. Why do doctors get discounted interest rates?

Doctors are low-risk borrowers with great incomes; therefore, they receive great discounts and rates. They are favoured due to their low default rate in comparison to any other profession. Due to this, they receive a number of benefits.

3. Are [self-employed] Dentists or Doctors eligible for home loans with no LMI?

The best way to answer this question is through an example:

You’re a self-employed dentist running your own clinic for the past five years. Your income is sitting at around $120,000 per annum, with savings sitting in your bank at $200,000. You’re ready to buy and are considering a 2 bedroom home for around $670,000. What are your options, and will you have to pay LMI? Will you be eligible for waived LMI? Let’s do the maths.

| Income | Deposit (%) | Deposit ($) | Property |

$120,000 | 27% | $200,000 | $670,000 |

Yes, self-employed Dentists and Doctors are eligible for home loans with no LMI!

Self-employed doctors or dentists are eligible for home loans without LMI and your tax returns will be evidence to prove this.

However, if it isn’t possible to show your tax returns, then invoices can be used as evidence of income. Lenders are looking at your ability to repay the loan, and it certainly isn’t the first time a self-employed professional has asked for a loan.

However, if you are self-employed, lenders can sometimes look at you with an air of caution, as the income level is not stable, and there’s a higher chance of default. One way to get around this is to show regular and stable income for an extended period. Anything from 2 years + will cover this.

In order to receive benefits that dentists receive, such as waived Lenders Mortgage Insurance (LMI) or interest rate discounts, you need to be a member of the Australian Dental Association (ADA) or the Australian Dental Council (ADC).

4. Some weeks I do extra contract work outside of this. How is this income looked at?

The extra income earned outside of your dental job may be considered when calculating your borrowing power.

When it comes to determining income for self-employed professionals, lenders will often consider these factors:

- Income made over the past two years.

- Previous tax returns.

- The lowest income figures for the previous two years.

- Then rental payments and depreciation as shown on your tax return are subject to the lender.

Really, what it comes down to is proving to a lender that you have a stable income, but also showing that there is a growth in your income.

If your income has decreased over this period, that also adds doubt to the process. In that situation, additional supporting documents will be required, such as financial statements.

Speak to our team at Hunter Galloway today for details about your personal situation.

5. Can I get an interest-only doctor loan with no LMI?

When it comes to providing a home loan to doctors, eligible doctors can generally borrow up to 90% of the property value without LMI, while a small number of select lenders may consider up to 95% under stricter criteria.

Not only that, but you can also get significant discounts on interest rates. The reason behind it is simple. You are high-income earners and usually take out loans for investment purposes.

And to answer your question as to whether you can get an interest-only doctor home loan with no LMI?

The answer is YES, you can.

However, there are certain things you have to consider before getting an interest-only doctor home loan….

6. Can I get No LMI with an Interest Only Investment loan?

Being able to get no LMI and interest-only Doctor Home Loan comes down to the purpose of the loan.

If you intend to get an interest-only doctor home loan for investment purposes and also get an LMI waiver, this is completely fine. You will save a lot of money on LMI, and it will give you huge cash flow benefits for future investments.

On the other hand, the banks do not like giving Interest-only Doctor Home Loans if you are buying a property to live in (also known as an owner-occupied home). However, if, for example, you were planning on turning the property into an investment within a few months of moving in, they may consider it.

There are many options for Doctors and medical professionals when it comes to getting a home loan, and at Hunter Galloway, we can help, so talk to our team and see how we can help.

7. Do Nurses qualify for home loans for Doctors?

Nurses qualify for a different type of home loan deal, yet not quite as discounted as doctors due to lower-income.

You can read more about special deals for Nurses here.

The savings can be made via lenders insurance (LMI) by showing that you have a stable and consistent income as a nurse.

As lenders believe nurses are low-risk professionals, they can qualify for over 80% LVR loans.

The requirements for Nurse’s to get special home loan discounts include:

- The borrowing amount should not exceed 85% loan to value ratio.

- The loan size should not be more than $1,500,000.

- You hold a good credit rating.

- You have a stable job and a reasonable stream of income. Banks give preference to customers who have an annual income of more than $150,000.

More information on Nurse Home Loan specials here.

8. Will I qualify for a doctor’s home loan if my partner is a medical professional?

When partners are applying for a home loan together, the eligibility of receiving the benefits is not based on both borrowers being employed in the health profession. At least one of you must be a doctor or dentist, and then the LMI premium can be waived.

9. Can doctors access a 95% LMI waiver?

For eligible doctors, 90% LVR without LMI is the standard policy across the broader lender range. A small number of select lenders may offer up to 95% LVR without LMI, subject to stricter criteria, property type and lender policy.

Policies change, so we confirm the current options before recommending a lender.

Next Steps and How to Apply for a Doctor Home Loan

Are you thinking about buying a new home or investment property? Talk to our expert mortgage brokers about your lending requirements.

Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please call us on 1300 088 065 or book a free assessment online to see how we can help.