Did you know specialized accountant home loans allow eligible professionals to borrow up to 95% of a property’s value without paying Lenders Mortgage Insurance (LMI)—potentially saving over $24,000 upfront? While many banks require high income thresholds, new lender policies for 2026 have opened these benefits to early-career professionals and those earning under $120,000. In this complete guide, we explain exactly how an experienced accountant mortgage broker can help you qualify for these exclusive waivers and interest rate discounts.

Why Accountants Get Better Home Loan Deals

Banks view accounting professionals as “blue-chip” borrowers. Your career path offers stability, consistent income growth, and a low risk of default. Consequently, lenders actively compete for your business by offering exclusive discounts and policy waivers.

These specialized Accountant home loans provide significant advantages over standard mortgages. In fact, you can enter the property market sooner and keep more cash in your pocket.

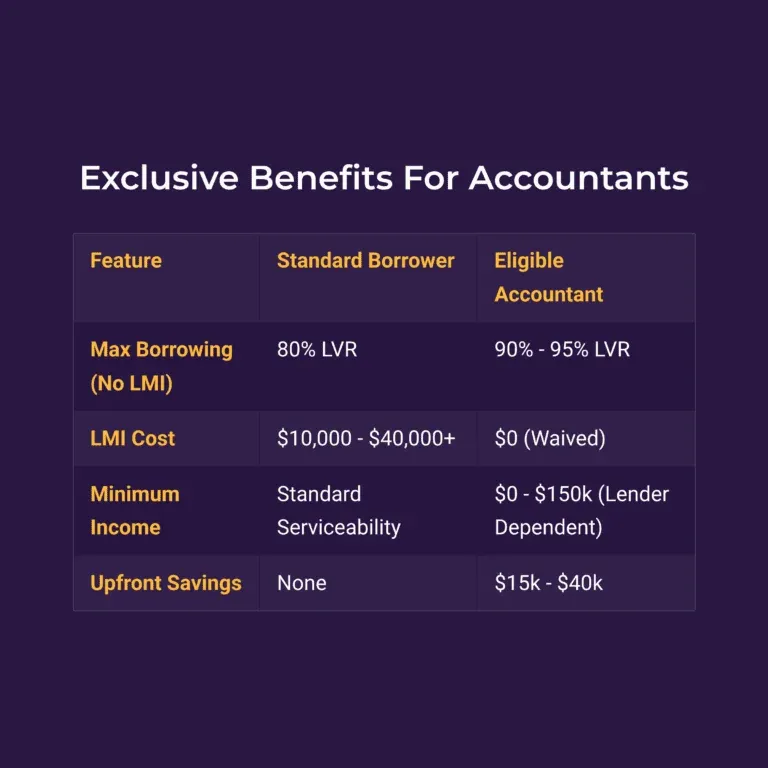

At a Glance: Your Exclusive Benefits

Here is a quick summary of what you can access in 2026.

Top 3 Benefits of Accountant Home Loans

While most borrowers are subject to standard lending policies, your qualification as an accounting professional unlocks a different tier of banking products. These benefits are designed to acknowledge your lower risk profile and higher lifetime value to the bank.

1. The LMI Waiver (Save Thousands)

Lenders Mortgage Insurance (LMI) is typically a mandatory fee for any borrower with a deposit smaller than 20%. It protects the bank—not you—in case you default. For standard borrowers, this fee can be astronomical.

As an eligible accountant, you can have this fee completely waived up to a 90% Loan-to-Value Ratio (LVR). This means you only need a 10% deposit to buy a property without paying a cent in insurance premiums.

Real World Math: How much do you actually save?

- Property Value: $1,000,000

- Your Deposit: $100,000 (10%)

- Loan Amount: $900,000

- Standard Borrower LMI Cost: ~$24,000

- Eligible Accountant LMI Cost: $0

- Total Upfront Savings: $24,000

That is $24,000 you can keep in your offset account rather than handing it over to an insurance company.

2. Discounted Interest Rates

Banks don’t just waive fees; they also compete on price. Because accountants are statistically reliable borrowers, lenders are willing to offer “professional package” interest rates that are often significantly lower than advertised rates.

These aren’t always public offers. An experienced broker can negotiate discretionary pricing on your behalf, potentially shaving 0.15% to 0.40% off your variable rate. Over a 30-year mortgage, a small percentage drop saves you tens of thousands of dollars in interest repayments.

3. Higher Borrowing Power (95% No LMI)

While the industry standard for LMI waivers is 90%, a select group of lenders has recently pushed this boundary even further.

In 2026, we are seeing exclusive offers allowing strong applicants to borrow up to 95% of the property value without paying LMI. This is a game-changer for first home buyers. It allows you to enter the market with just a 5% deposit, bypassing the months or years typically needed to save that extra 5%.

Note: This 95% waiver is highly specific and often restricted to borrowers with pristine credit history and stable employment. It’s vital to speak with a broker who knows which specific accountant home loans currently feature this offer.

Read more: Grants to buy your first home – 2026 guide

Eligibility Criteria: Do You Qualify?

Navigating bank policies can be confusing. One lender might approve you while another declines the exact same application. To qualify for exclusive accountant home loans and waivers, you generally need to meet specific employment, membership, and income standards.

Here is the complete checklist to help you self-qualify instantly.

Eligible Job Titles

Your official job title is the first box lenders tick. While standard roles are well-known, many specialized positions also qualify.

Standard Eligible Roles:

- Accountant

- Actuary

- Auditor

- Chief Financial Officer (CFO)

- Director / Partner

- Finance Director

- Finance Manager

- Financial Controller

Accepted Specialist Roles:

- Tax Consultant

- Insolvency Practitioner

- Bursar

- Forensic Accountant

Note: If your title differs slightly (e.g., “Internal Auditor” instead of “Auditor”), we can often explain this to the credit assessor to get it approved.

Required Industry Memberships

You must hold a valid membership with a recognized governing body. A simple university degree is usually not enough on its own; you need to be a practising professional.

Recognized Australian Bodies:

- Chartered Accountants Australia and New Zealand (CAANZ)

- Certified Practising Accountants (Australia) (CPA)

- Institute of Public Accountants (IPA)

- Chartered Financial Analyst Institute Australia (CFA)

- Institute of Actuaries of Australia (FIAA)

Do Overseas Qualifications Count?

Yes, they often do. If you obtained your qualification overseas, you are likely eligible if your institute is part of the Global Accounting Alliance (GAA).

Australian banks frequently recognize reciprocal memberships from bodies like the ICAEW (UK), AICPA (USA), or SAICA (South Africa). If you have converted your overseas accreditation to a local CA or CPA membership, you should be fully eligible for an LMI waiver.

Minimum Income Requirements (By State)

Income thresholds are the most common stumbling block. Historically, banks required a high minimum income. However, in 2026, policies have become much more flexible.

The requirement depends entirely on which lender you choose.

Lender Category | NSW, VIC, QLD, ACT | WA, SA, NT, TAS |

Standard Lenders | Min. $150,000 p.a. | Min. $120,000 p.a. |

Select Lenders | No Minimum Income | No Minimum Income |

Important Income Rules:

- No Minimum Income: Some lenders now offer waivers to CA/CPA members regardless of income, provided you have a strong credit history.

- Rental Income: Most banks will include rental income to help you reach the $120k/$150k threshold.

- Spousal Income: Banks usually exclude your partner’s income from this specific threshold test, unless your partner is also an eligible accountant.

Check to see if you are eligible for a home loan

Special Rules for Partners and Firms

Becoming a partner is a major career milestone, but it often complicates your mortgage application. Standard bank policies struggle to categorize your income, often treating you as self-employed rather than a high-income professional.

However, most accountant home loans have built-in exceptions for these scenarios. If you know which lender to approach, the process becomes significantly smoother.

Partner Income & Liability

The biggest hurdle for partners is a legal concept called “Joint and Several Liability.”

Because partnerships are not separate legal entities, banks often view the firm’s liabilities as your personal debt. Consequently, most lenders demand full financial statements and tax returns for the entire practice. Providing these documents is often difficult, intrusive, or simply impossible if you are one of 50 partners.

How We Solve This

At Hunter Galloway, we work with specific credit teams that understand the accounting partnership structure.

- Waiver of Business Financials: We can often get the requirement for firm-wide financials waived completely.

- Profit Share Recognition: Instead of assessing the whole business, these lenders focus solely on your individual income distribution.

- Simplified Assessment: As long as we can evidence your personal earnings (via tax returns or an accountant’s letter), the bank ignores the firm’s broader liabilities.

Simplified Verification for Big 4 & Mid-Tier Firms

If you are a partner at a major firm, the process is even easier.

Banks recognize the stability of global top-tier firms. Therefore, they offer a “low doc” verification process for partners at specifically approved companies. You generally do not need to provide tax returns at all.

Instead, a simple letter from your Administration Manager, HR, or Finance Director confirming your income is sufficient evidence.

Eligible Firms typically include:

- The Big 4: Deloitte, Ernst & Young (EY), KPMG, PwC.

- Legal & Mid-Tier: Allens, Clayton Utz, MinterEllison, Grant Thornton, McGrathNicol, Gadens, Corrs Chambers Westgarth.

Note: This list changes regularly. If your firm isn’t listed, ask us for a free assessment, as we can often negotiate exceptions.

Which Banks Offer Best Accountant Home Loans?

Choosing the right lender is just as important as securing a waiver. Every bank has a different appetite for risk, and their policies for accountant home loans can vary wildly depending on your income, deposit, and employment type.

While many lenders offer professional packages, the “Big Four” and their subsidiaries tend to have the most robust policies for accountants.

The Major Players

Here is a general breakdown of who currently leads the market:

- ANZ: Historically, ANZ has been a market leader for professionals. They are often the go-to choice for applicants who want to bypass strict minimum income thresholds, focusing instead on your membership status (e.g., CPA or CA).

- Commonwealth Bank (CBA): As Australia’s largest lender, CBA offers consistency and speed. They are frequently competitive with interest rate discounts and have excellent digital banking tools, making them a solid choice for busy professionals.

- Westpac: Westpac is known for generous borrowing power calculations. If you are looking to maximize your loan size for a dream home or investment, their servicing policies often allow you to borrow slightly more than competitors.

- St. George: A favourite for “edge cases.” St. George often provides more flexible credit assessment criteria, which can be invaluable if your income structure is complex or involves significant bonuses.

Crucial Insight:

Bank policies change monthly. While ANZ might offer no minimum income today, St. George might release a sharper interest rate tomorrow. A lender that was perfect for accountants in 2025 might be uncompetitive in 2026.

We compare them all for you in real-time. Instead of guessing, we check the daily credit updates to ensure you are applying with the lender currently offering the most aggressive deal.

How To Apply For An LMI Waiver: The 5-Step Process

Securing an LMI waiver isn’t automatic. You cannot simply tick a box on a standard online application form. Instead, you must structure your application correctly to prove your eligibility to the credit department.

Follow this proven 5-step roadmap to ensure a smooth approval process for your Accountant home loan.

Step 1: Verify Your Membership

Lenders require proof that you are a current, practising professional. Your university degree alone is usually insufficient.

- Action: Locate your most recent industry membership certificate. Alternatively, a receipt for your annual membership payment will suffice.

- Check: Ensure your specific designation (e.g., CPA, CA, or CFA) is clearly visible and active.

Step 2: Assessing Your Income

Banks view income sources differently. Some credit assessors will use 100% of your bonus or overtime, while others may shade it by 20%.

- Action: We review your payslips and tax returns to calculate your “serviceability” accurately.

- Detail: We distinguish between your guaranteed base salary and variable income like bonuses or profit shares. This ensures we present your earnings in the strongest possible light to maximize your borrowing power.

Step 3: Lender Selection

This is the most critical step. As we mentioned before, policies vary significantly between banks.

- Action: We match your specific financial profile—your deposit size, income structure, and membership—to the lender with the most favourable policy.

- Why? This strategic selection prevents you from applying to a bank that would decline you due to a technicality (like a specific probation period policy).

Step 4: Submission & Pre-Approval

Once we have selected the right lender, we package your application with a specific “Professional Waiver” request.

- Action: We submit your application to the bank’s dedicated “Professional Credit Team” rather than the general queue.

- Outcome: You receive a Pre-Approval. This gives you a clear budget and the confidence to make offers on properties, knowing your LMI waiver is locked in.

Step 5: Valuation & Settlement

After you find your property, the bank will order a valuation to ensure the price aligns with the market.

- Action: Once the valuation is accepted, the bank issues “Unconditional Approval.”

- Outcome: We guide you through signing the loan documents, and the funds are released on settlement day. You pick up the keys to your new home—without having paid a cent in LMI.

Expert tip: Don’t risk a decline by choosing the wrong lender. A rejected application can leave a black mark on your credit file.

Contact us here to get a free assessment. We will review your situation and identify exactly which lenders will approve your LMI waiver today.

Would you like to learn about your situation?

Frequently Asked Questions About Accountant Home Loans

You likely have specific questions about your situation. Here are the most common questions our team answers for accounting professionals.

Can I borrow 95% without LMI?

Yes, but it is restricted to select lenders.

While the industry standard for accountant home loans is a 90% LMI waiver, a small number of lenders have recently introduced a 95% No LMI offer. To qualify for this higher tier, you typically need a pristine credit rating and must be buying an owner-occupied home (not an investment). Because this policy changes frequently, we recommend booking a free assessment to see if you are eligible.

Does my spouse need to be an accountant?

No, they do not.

You can apply for a joint loan with your spouse or de facto partner, even if they work in a completely different industry. As long as one applicant meets the professional eligibility criteria (job title, membership, and income), the entire loan is eligible for the LMI waiver. This is a fantastic way for couples to maximize their borrowing power using just one partner’s professional status.

Can I use this for an investment property?

Absolutely.

The LMI waiver is not limited to buying your own home. Many of our clients use this benefit to build a property portfolio. By only using a 10% deposit (instead of 20%) for each purchase, you can preserve your cash and potentially buy two investment properties with the same capital that a standard borrower would use for one.

What if I am on a visa (482/PR)?

Permanent Residents (PR) are fully eligible.

If you hold Australian Permanent Residency, you are treated exactly the same as a citizen and can access the full 90% LMI waiver.

For 482 Visa holders, policies are stricter. Most lenders cap borrowing at 80% LVR for temporary residents. However, exceptions exist depending on your remaining visa duration and income strength. We can verify your specific visa conditions with our lending panel.

Can I get approved while on maternity leave?

Yes, most banks will approve you.

Lenders understand that maternity leave is temporary. If you are currently on leave, we simply need to provide a letter from your employer confirming your return-to-work date and your salary upon return. We can then use your “return” salary to calculate your borrowing capacity, ensuring you don’t miss out on buying a home during this family milestone.

I just started a new job. Do I need to pass probation first?

Not necessarily.

Standard borrowers often need to be in a job for 6-12 months. However, for accounting professionals, banks are far more lenient. If you have moved to a similar role for higher pay (e.g., moving from one firm to another), many lenders will waive the probation requirement entirely. We just need to show your employment continuity in the industry.

Does the LMI waiver apply if I refinance?

Yes, and it is a powerful strategy.

If you bought your home with a small deposit and are currently paying a higher rate, refinancing to an accountant home loan package can be a double win. You can release equity (cash out) up to 90% of your home’s value without triggering an LMI bill, giving you funds for renovations or a new deposit.

Can I qualify for an accountant home loan if I work part-time?

Yes, provided you meet serviceability requirements.

Working part-time does not disqualify you. If you are a parent returning to work or semi-retired, you can still access professional discounts. If your income falls below the standard $150,000 threshold due to part-time hours, we will direct your application to specific lenders that have no minimum income requirements for CA/CPA members.

How do I apply for a Chartered Accountant loan?

You must follow a specific process to trigger the waiver.

You cannot simply submit a standard online application. To access exclusive rate discounts and LMI waivers:

- Verify Membership: Have your current CAANZ certificate ready.

- Use a Specialist Broker: Most bank branches don’t know these specific policies. We submit your application directly to the bank’s “Professional Credit Team” to ensure your waivers are applied correctly from day one.

Ready To Apply For An Accountant Home Loan?

As an accountant, you understand the value of expert advice.

Choosing Hunter Galloway for your home loan isn’t just about securing finance; it’s about partnering with specialists who understand your unique professional needs.

Why navigate the complex world of home loans alone when you can have a dedicated team at your side?

Our expertise as a mortgage broker for accountants means tailored solutions, competitive rates, and a smoother, more efficient process.

Take the first step towards effortless home financing.

Call us now on 1300 088 065 or contact us for a free assessment to discuss your options. Let’s make your home ownership journey as strategic and successful as you are.

More Resources For Homebuyers:

- Lenders Mortgage Insurance (LMI) Calculator – Calculate your potential savings instantly.

- How To Buy A House With A Small Deposit – Strategies for when you don’t have the full 20%.

- Guarantor Home Loans Explained – An alternative way to waive LMI if you don’t qualify for professional packages.

- Refinancing Your Home Loan – How to switch to an accountant home loan from your current lender.

- First Home Owner Grant QLD (Complete Guide) – Check your eligibility for government support.