Your LVR helps determine whether lenders mortgage insurance may apply. After calculating your ratio, use our LMI calculator to estimate the possible premium.

LVR Calculator

The LVR Calculator below will help you work out your loan-to-value ratio.

Here’s how to use it:

- Fill in your expected loan amount

- Fill in your property value

- Click on the ‘Calculate’ Button

The calculator will show your current LVR in the form of a percentage.

In the rest of this guide, we’ll explain what LVR is, why it’s important, and show you LVR calculations for different scenarios.

Start by calculating your LVR below, and then read on to learn what your LVR means for you as you consider working with a mortgage broker in Brisbane.

Disclaimer: This calculator is to

be used as a guide to help you better understand

your options. We have not assessed what options are

suitable for your needs or if you meet other

lending criteria that would allow you to access

your equity. Any repayments quoted above are

calculated using your current home loan balance

over a term of 30 years. We strongly recommend that

you make additional repayments and pay your loan

off sooner. If you borrow over 80% of the property

value then you may pay an LMI premium

Why Use An LVR Calculator?

An LVR calculator is essential for anyone looking to buy property, refinance an existing loan, or evaluate mortgage options. You can calculate it manually, but using the LVR calculator makes this quick and easy.

Using an LVR calculator can help you gauge potential mortgage insurance costs. Loans with higher LVRs often require Lender’s Mortgage Insurance (LMI), which can add a significant expense. By calculating your LVR upfront, you can explore ways to reduce it, such as increasing your deposit.

Finally, an LVR calculator can help you negotiate better loan terms. Knowing your LVR allows you to have more informed discussions with lenders, potentially securing a better deal.

What Is LVR?

Loan to Value Ratio (LVR) is a percentage that represents the relationship between the amount of your loan and the value of your property. It’s a key factor that both lenders and borrowers use to determine the level of risk associated with a loan. For instance, an LVR of 80% means that you are borrowing 80% of the property’s value while the other 20% comes from your deposit.

Lenders use LVR to gauge the risk they are taking on by lending to you. Generally speaking, the lower the LVR, the less risk there is for the lender. A lower LVR might lead to better interest rates or loan terms for you. On the other hand, a higher LVR can lead to additional costs, like Lenders Mortgage Insurance (LMI), which is often required when borrowing more than 80% of the property’s value.

In simpler terms, the LVR is a measure of how much equity you have in the property compared to what you owe. It’s one of the main factors that banks and lenders consider when deciding whether to approve your loan and what terms to offer you.

Read more: Home loans Brisbane, the definitive guide.

How Is LVR Calculated?

Calculating the Loan-to-Value Ratio (LVR) is simple and involves just a few basic steps. Start by determining the amount you want to borrow or the existing home loan amount if you’re refinancing. Then, find the current market value of the property. To calculate the LVR, divide the loan amount by the property value and multiply by 100 to get a percentage.

For example, if you want to borrow $480,000 for a property valued at $600,000, you would divide $480,000 by $600,000. This gives you 0.80, which means the LVR is 80%.

This percentage helps lenders assess the risk of the loan, which can affect your interest rates and whether you’ll need to pay for Lenders Mortgage Insurance (LMI).

Read more: How to value a property.

LVR Calculation For Guarantor Home Loans

How do you calculate LVR with a guarantor home loan?

Calculating LVR on guarantor home loans is similar to standard calculations but involves two properties as security instead of one.

Suppose you’re buying a home for $600,000 and want to borrow 100% of the property’s value, totalling $600,000, using a guarantor home loan. How is the LVR calculated?

This is an example of a typical guarantor home loan structure:

- Non-guarantor loan amount: $480,000

- Purchase property value: $600,000

- LVR against your property: 80%

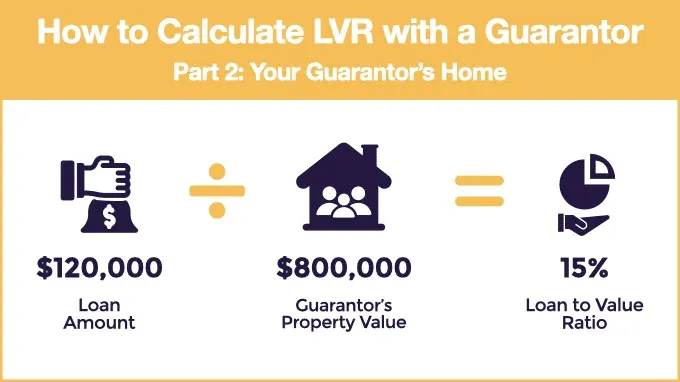

- Guarantor loan amount: $120,000

- Guarantor property value: $800,000

- Guarantor LVR: 15%

With guarantor home loans, the bank structures the loan into two parts.

First, the bank lends 80% LVR against the property you are purchasing:

- Loan amount against your property: $480,000

- Calculation: $480,000 ÷ $600,000 = 0.80 or 80% LVR

Lenders’ Mortgage Insurance is not payable as the loan is under 80% LVR.

Second, the remaining $120,000 is secured against your guarantor’s property:

- Loan amount against guarantor’s property: $120,000

- Guarantor property value: $800,000

- Calculation: $120,000 ÷ $800,000 = 0.15 or 15% LVR

Overall, this guarantor lending allows you to borrow 100% of the property’s value, but it requires a guarantor to provide their property as additional security.

Read more: Guarantor Home Loans.

Calculating LVR For An Off The Plan Purchase

When you purchase a property off the plan, there’s often a significant time gap—usually 12 to 24 months—between signing the contract and settling the property. During this period, the property’s value can change, often increasing by the time settlement comes around.

So, how does this affect your Loan to Value Ratio (LVR) when it’s time to settle?

Let’s consider an example:

At the Time of Purchase:

- Initial purchase price (off the plan): $600,000

- Original loan amount: $570,000

- Initial LVR at time of purchase: 95%

This means you planned to borrow 95% of the property’s value when you signed the contract. Since the LVR is over 80%, you’d typically be required to pay Lenders Mortgage Insurance (LMI).

At settlement (12+ Months Later):

- Property value at settlement: $713,000

- Loan amount remains the same: $570,000

- New LVR at settlement: 79.9%

Since the LVR is now approximately 79.9%, which is below 80%, lenders consider the loan to be at a lower risk. This means you may no longer need to pay LMI, potentially saving you thousands of dollars.

Understanding the Impact of the Changed LVR:

- Bank Valuation: The bank will use the updated property valuation of $713,000 (ignoring the original purchase price of $600,000, provided at least 12 months have passed) to calculate the LVR.

- LMI Savings: Dropping below the 80% LVR threshold can eliminate the need for LMI, reducing your upfront costs.

- Increased Equity: The increased property value also means you have more equity in your home from the outset.

Key Takeaways:

- Buying off the plan can be advantageous if property values rise before settlement.

- An increased property value lowers your LVR, potentially eliminating the need for LMI.

- It’s important to monitor market trends and property values during the construction period.

Buying off the plan can be beneficial and risky, depending on market fluctuations affecting the final LVR. Always consult with financial experts to understand how changes in property values can impact your loan and overall financial situation.

Read more: buying off-the-plan homes in Australia.

How To Calculate LVR When You Get A Low Valuation

Let’s say you’re buying a property for $600,000 and plan to borrow $480,000. Initially, the LVR would be calculated using the purchase price:

- LVR = ($480,000 ÷ $600,000) × 100 = 80%

In this case, the LVR is 80%, which is considered lower risk. At this level, you typically wouldn’t need to pay Lenders Mortgage Insurance (LMI).

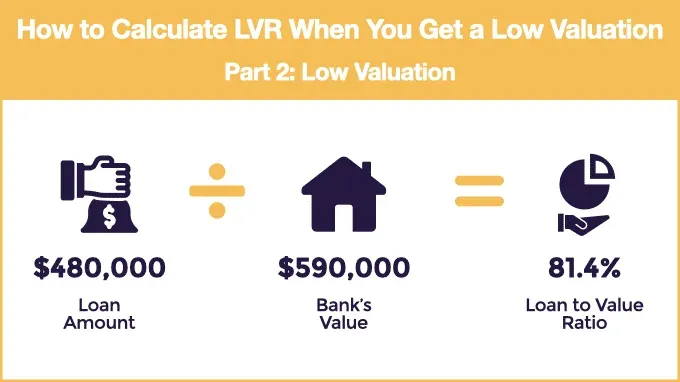

If the bank’s valuation comes in at $590,000 instead of the purchase price, the LVR is recalculated based on the lower value:

- LVR = ($480,000 ÷ $590,000) × 100 ≈ 81.35%

Since the LVR is now 81.35%, the loan is considered a higher risk by the lender. As a result, you would likely need to pay LMI, which can add significant costs to your purchase.

What to do if you get a Low Valuation

If the bank’s valuation comes in lower than the purchase price and you’ve bought the property subject to finance, you have options. You could:

- Try to exit the contract.

- Negotiate a lower price with the seller.

- Seek another bank valuation to see if a higher value can be achieved.

A low valuation doesn’t have to be the end of the road. You can still negotiate with the real estate agent or the seller to potentially lower the purchase price.

Read more: How to challenge a bank valuation.

Calculating LVR For A Construction Loan

If you’re looking to buy land for $405,000 and build a home for $405,000, here’s how the Loan to Value Ratio (LVR) would be calculated, assuming the bank values each part (land and building) at $450,000.

For a construction loan, the LVR is calculated in two parts: first for the land and then for the total property value once the construction is complete.

LVR for the Land Loan:

If you’re borrowing $405,000 for the land and the bank values the land at $450,000, the LVR for the land would be:

- 405,000 ÷ 450,000 = 90%

This LVR of 90% would likely require Lenders’ Mortgage Insurance (LMI), as it’s over the 80% threshold.

LVR for the Total Construction Loan:

Once both the land and building are complete, the total property value would be $900,000. If you’re borrowing a combined amount of $810,000, the LVR for the entire project would be:

- 810,000 ÷ 900,000 = 90%

Since the overall LVR is 90%, LMI would still apply.

Lenders also consider the build costs to ensure they align with industry standards. If the construction costs are higher than typical, the bank may give a lower valuation, impacting your LVR and increasing your overall costs.

Read more: How does construction financing work?

How To Calculate LVR For Refinance

If you’re refinancing your property, banks will conduct their own property valuation to determine the current Loan to Value Ratio (LVR). The value of your property may have changed since your initial purchase. Property prices can increase significantly—sometimes by up to 30% or more in a 12-month period, which could mean your property is worth much more than when you bought it.

However, if the market has declined, your property could be worth less than what you initially paid for it. Renovations can also impact the value, with even small upgrades, like a new kitchen or bathroom, increasing the property’s worth.

Banks use independent valuers to assess the property’s current value at the time of refinancing to accurately calculate your new LVR.

Read more: Seven reasons to refinance your home loan.

LVR Calculator FAQs

How We Can Help

At Hunter Galloway, our expert mortgage brokers are ready to guide you through every step of the home loan process. Whether you need help understanding your Loan to Value Ratio (LVR), navigating the refinancing process, or simply want expert advice on securing the right home loan, we’re here to assist.

Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Contact our team today for a free assessment by calling 1300 088 065 or clicking the button below to get in touch with us online. Let’s make your property journey as smooth as possible.