There are two main ways to access your equity. The first is through a cross-securitisation loan, and the second is a standalone home loan. Let’s take a look at how each works.

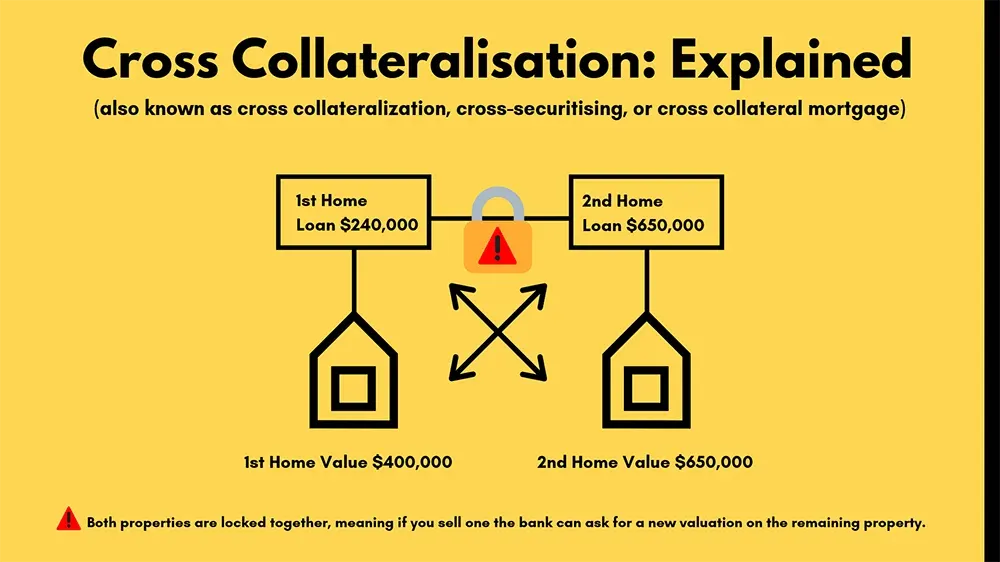

Cross-collateralisation, also known as cross-securitisation, is a loan structure in which a loan or loans are secured by two or more properties. This approach allows borrowers to finance the entire purchase price of a property, providing equity permits.

Imagine you’re interested in buying an investment property worth $500,000. Luckily, you already own a home outright valued at a million. Without the use of equity, typically, you need to provide the bank with a minimum 20% deposit plus additional monies for such things as stamp Duty. However, because you own your home— by cross-securitising both properties, you can borrow the entire purchase price plus the additional costs such as stamp duty. This means you could borrow $525,000 to cover all the costs, including the purchase price. This loan amount would be secured by both properties — that’s, both the existing property and the intended purchase property.

In this example, we have two properties valued at $1.5 million. The first is an investment property we acquired for $500,000, and the second is the existing home we own for $1 million. Through cross-collateralisation, the bank now holds a combined value of $1.5 million in properties, and in this scenario, we are only borrowing $525,000. Based on our equity position, your loan-to-value ratio would be roughly 35%.

The major downside to cross-collateralisation is that it can limit your future options. For example, if you want to sell your existing home late, you will need to revalue your new home at that point, and if the valuation comes in lower, you might OWE the bank more money.

The main benefit of cross-collateralisation is that banks sometimes give you sharper interest rates.

Crossing your properties within your structure can have pros and cons, so we suggest speaking with a Mortgage Broker to determine what is best for you.

To discuss your situation, contact our Mortgage Brokers on 1300 088 065 or fill in our free online enquiry form to get a callback.

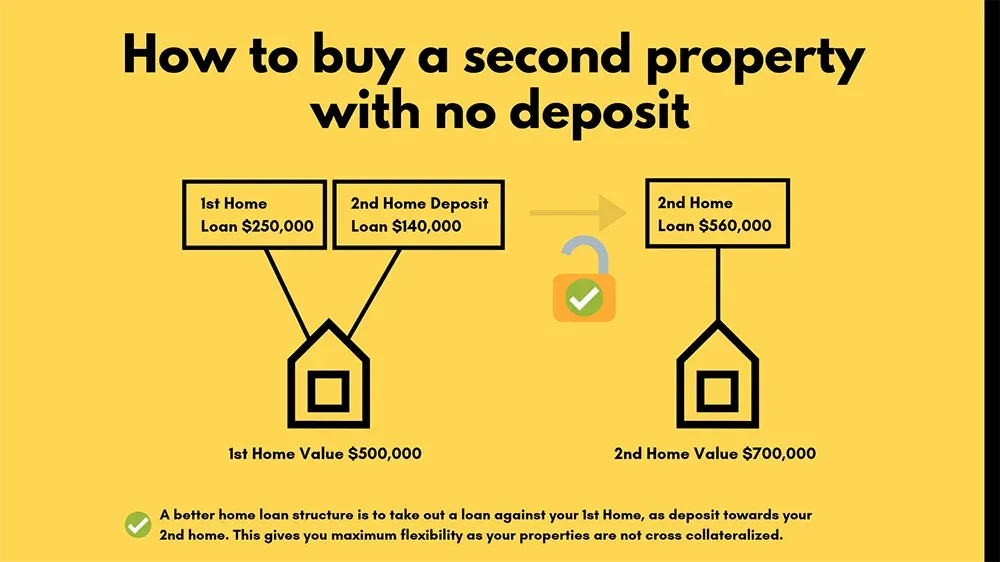

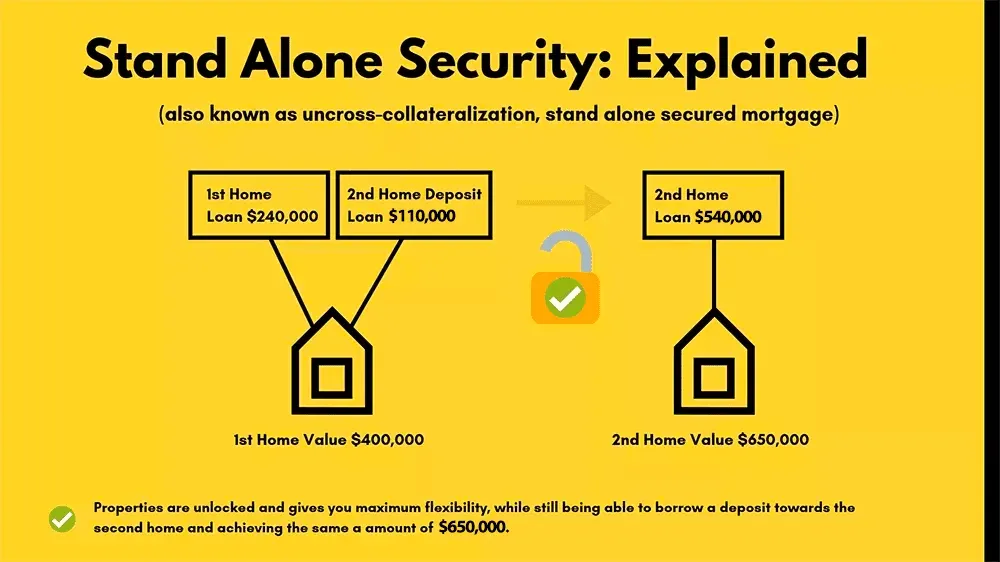

Unlike cross-collateralisation, where multiple properties secure a loan, standalone securities focus on securing loans with single properties.

Let’s use a previous example to illustrate this. In this scenario, you would need to have two loans instead. The first loan is $400,000, which is secured against the investment property valued at $500,000. This loan represents 80% of the property’s value and, by doing so, allows you to avoid paying mortgage insurance.

The second loan of $125,000 would be secured by your home, and, as before, you would still be borrowing a total of $525,000. But rather than being one loan secured by two properties, you have two loans separately secured by two different properties, allowing you to use two different banks if you so desire.

Both cross-securitisation and standalone home loans allow you to access the equity in your property, but they do it in two different ways.