“My first experience with the Barefoot Investor buckets was with my sister. We were going for a coffee, and she whipped out an orange ING bank card with “SPLURGE” written in Sharpie right across the front.

She noticed my puzzled glance and proceeded to explain all about her special bank account setup.

Mojo account, Fire Extinguisher, Grow…

Initially, I thought she was talking about an Austin Powers movie, but all this has to do with different bank accounts, buckets and budgeting. And it all comes from a book written by an Aussie financial expert called “The Barefoot Investor”.

If you’ve read The Barefoot Investor, started the bucket strategy, and then gave up—you’re not alone. Many Aussies open heaps of accounts, then get stuck halfway. As a mortgage broker in Brisbane, I’ll walk you through how to set up the Barefoot Bank Accounts properly. We’ll break down each account, explain what it’s for, and show you how to keep things simple.

Let’s dive in and get your money sorted…

Barefoot Investor Basics

At its core, the Barefoot Investor offers a smarter, simpler way to manage your money using multiple bank accounts. These accounts—known as Barefoot Investor buckets —help you sort your income into clear buckets based on your goals.

The strategy focuses on automating the process – so your savings, spending, and investing happen without overthinking on your part.

Let’s be honest, Spreadsheets and strict budgets work for some, but not for most. By automating your finances, you remove stress and willpower from the equation. That frees you to focus on paying off debt, buying a home, and building long-term wealth.

When I mentioned I was writing about the Barefoot Investor, a friend sighed and said,

“Ugh! I gave up—too many accounts, too confusing.” It made me wonder—how many people start this and never finish?

If you’re feeling lost in a sea of buckets and bank accounts, you’re in the right place. I’ll explain each one—and how to make them work in 2025.

Your Money Mindset [How To Increase Your Savings ASAP]

Before we dig into the details about the barefoot investor method and bank accounts, let’s quickly talk about your money mindset – how you think about money and your financial priorities.

Your money mindset is a set of beliefs and attitudes you have about money, wealth and success, which determine how you handle money. One of the key ways of achieving financial success is by building a positive money mindset…

Why is this important?

A positive mindset is important because, regardless of how simple the Barefoot Investor principles are, they still require work. You aren’t going to pay down all your debts, buy a home and retire wealthy with a brief period of effort. It’s going to take years of commitment to achieve your financial goals.

There are going to be hard times when you’ll be tempted to throw it all away and go back to the old way of doing things. So you need to have a good reason why you’re doing this.

Identify (and master) your invisible scripts about money

There’s an old joke: Two fish are swimming in a pond when an older fish starts swimming the other way towards them. When the older fish passes them, he nods and says, “Good morning! How’s the water?” The two fish swim for a while before one of them looks to the other and asks, “What the hell is water?”

What are your invisible scripts about money?

Those poor younger fish have been trapped by Invisible scripts.

Invisible scripts are deeply ingrained beliefs we rarely question—because we’ve grown up with them. Passed down through generations, these ideas quietly shape how we think, feel, and act around money. They’re so embedded in everyday life, we often don’t notice them. Like water to a fish, they’re all around us, quietly influencing every financial decision we make.

Everyone has invisible scripts about money

Invisible scripts are the things you have internalised about money. You might not realise you have them, yet they shape how you treat your money.

Invisible scripts are a topic that doesn’t get discussed often. It is mostly because invisible scripts are revealing, and the things they reveal might be tough pills to swallow.

But the good news is that they only control you when they are invisible. Once you bring them to light, you can take back control and make good financial decisions, such as opening Barefoot Investor bank accounts. Do any of the following invisible scripts below resonate with you?

Invisible script #1: "I'm just not good with money."

This is a really common invisible script, and it’s a problem because it’s so self-defeating. If you don’t think you’re good with money, you’ve already lost the game before it starts.

Usually, when someone says, “I am not good with money”, they mean they have difficulty managing their finances, struggle to make sound financial decisions, overspend regularly, don’t save enough or don’t understand basic financial concepts.

Here’s the truth—no one is born knowing how to manage money. It’s a skill. And like any skill, it can be learned.

Being good with money isn’t about being a genius—it’s about consistency. Behaviour beats brains every time.

You don’t need to know everything. You just need to start.

Invisible script #2: "I don't earn enough money to save."

Invisible script #2: "I don't earn enough money to save."

Most people want to start saving when they ‘earn enough’. The truth is, you will never have ‘enough’. If you are undisciplined, the more you earn, the more you spend, and the barefoot investor method will be quite useless to you. Having control of your financial future has nothing to do with how much money you earn.

There are people in Australia with multiple six-figure incomes who are completely out of control with their finances. In fact, some of the “richest” looking people are the ones who are struggling the most with debt and financial security.

On the other hand, there are others who have never earned more than the minimum wage for their entire lives but have used smart saving strategies and the power of compound interest to buy their own homes and retire with a multi-million-dollar investment portfolio.

It’s not how much you earn that counts, it’s how much you keep.

Invisible script #3: "It's too late for me."

Invisible script #3: "It's too late for me."

Many people think it’s too late to start saving because they’ve made too many financial mistakes over the years. That feeling of regret can hit hard—especially when you think about retirement. It often feels like you need decades of perfect saving habits to build any real momentum.

But here’s the good news: it’s never too late to start.

Whether you’re just starting out or nearing retirement, progress is still possible. Even small changes now can have a big impact later. You don’t need to have everything figured out—you just need to begin.

Stop beating yourself up for decisions you made in your twenties or thirties. We all make mistakes. What matters is what you do next.

The best time to plant a tree was 20 years ago. The second-best time to plant a tree is today.

The average life expectancy in Australia is around 82–83 years (about 81 for men and 85 for women ). How old are you now? Subtract your current age from this number.

Now you have a rough idea of how many years you have left on this planet. What are you going to do with them? Will you continue to stress about money and feel out of control of your own life?

Or will you step up and take action? Tools like the Barefoot Investor bank accounts can help—but it starts with one small step from you.

Invisible script #4: "The economy sucks."

Invisible script #4: "The economy sucks."

I get it – things are pretty tough right now. Our generation has already lived through the GFC – and now the fallout from the pandemic is still hitting hard. Add the recent surge in inflation and interest rates into the mix, and it’s easy to see why many feel our generation has had it the toughest.

However, you can’t let that be an excuse. The economy is always going to have its ebbs and flows. But, here’s the thing, the economy also always recovers…

It really doesn’t matter what the economy is doing. You’ll still be better off financially if you follow a smart saving system – whether in good times or bad.

It’s often said that more millionaires were created during the Great Depression than at any other time. And the ones who became millionaires back then weren’t the people who gave up because the economy was in the toilet – they were the people who stuck to their guns and did the work.

You can make progress, or you can make excuses.

There are plenty of other invisible scripts you might have about your money, and it’s worth spending some time thinking about your invisible scripts so you can address them.

But no matter your situation, no matter what your invisible scripts are:

Excuses aren’t going to save you when you get hit with a financial emergency.

Excuses aren’t going to change your bank balance.

Excuses aren’t going to set you up for retirement and keep you financially secure through life’s inevitable ups and downs.

The thing that will bring control over your money and your life is taking action.

It’s hard to admit that you’re not as financially successful or sorted as you tell yourself you are. But once you commit to making daily progress, you’re already free.

Financial freedom isn’t about your bank balance or the type of house or car you have. It’s a mindset – knowing that you’re taking action to care for yourself and your loved ones. Financial freedom is having control of your finances, no matter how little you earn. It is about working towards having enough to cover your expenses, pay off debt, save for the future and have some left over to enjoy life…

What Are Your Top Money Priorities? Lessons From The Barefoot Investor

Money in itself has no value. The value in money comes from the things it helps you achieve. All the money in the world won’t make you happy. It’s what you do with your money that makes you happy.

I’m going to share my top 3 priorities with you. Yours might differ from mine, but whatever they are, you should be clear about what having money will do for you.

Here are my top three priorities:

Financial security: I don’t want to stress about money. If the worst-case scenario were to happen, I want to know that I’ve got it covered.

Freedom to travel and spend time with family and friends: For me, life is about the journey. It’s not about a hard, joyless slog through life trying to preserve every penny along the way. It’s the experiences and good times you have along the way with friends and family that make life worth living.

Build long-term wealth to retire comfortably: We’re all going to get old eventually. And when it comes time to retire, I want to be comfortable. Retirement is supposed to be your golden years – a reward for your hard work over your life. Stressing out about money isn’t part of my retirement plan.

Spend some time thinking about your own money priorities. It will make the hard times easier and make you much more likely to succeed.

Now that’s out of the way, let’s dive into the nitty-gritty details. In the rest of this post, I will explain the whole Barefoot Investor system to you.

Barefoot Investor Buckets Explained

In this section, I’m going to break down the bank accounts and simplify them, so you don’t end up like my friend, who gave up.

The Barefoot Investor recommends splitting your income into three separate groups called “buckets.”

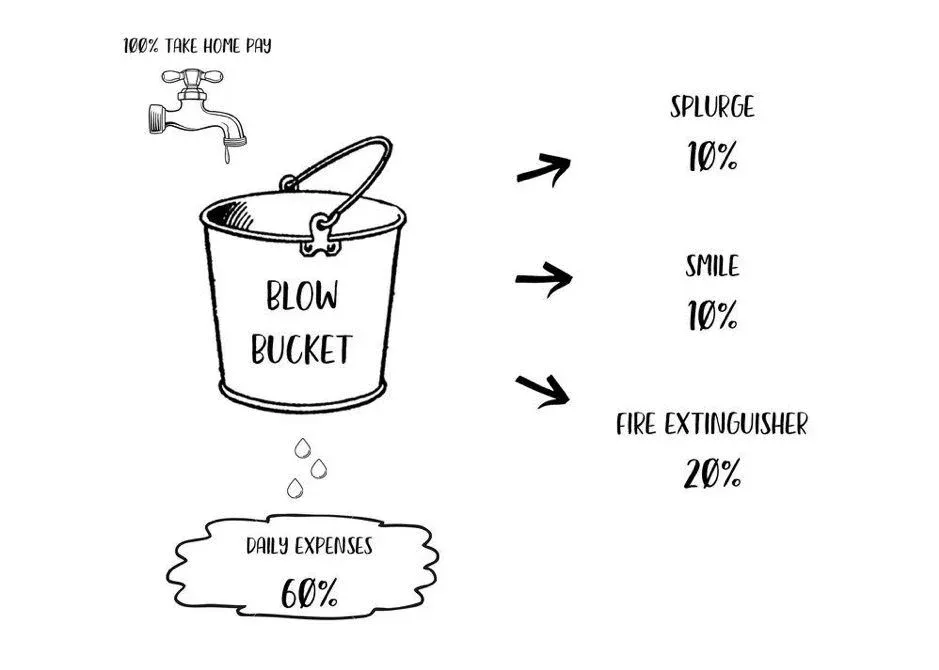

Blow Bucket: This is the money you will spend in the short term. The money here is used for daily expenses, the occasional splurge, holidays, and some extra cash to fight financial fires.

Mojo Bucket: The mojo bucket is used for your rainy-day emergency savings. It’s safety money for any financial emergencies that crop up.

Grow Bucket: This is your money-maker bucket. The grow bucket is where you do your investing and look for longer-term wealth building.

In summary, one bucket is for spending money on life, one is for savings for a rainy day/emergency, and the other is for long-term investments.

Blow Bucket

Now that we’ve moved from our three main categories and demystified the use of these funny words, it’s time to break down what the BLOW bucket means.

This is the one that causes all the confusion, and for my friend, it is the straw that broke the camel’s back.

Your Blow bucket is for expenses and splurge money. A lot of Aussies have just this one bucket and nothing else, and it’s one of the reasons why many people find it hard to save.

When you use one account for everything, the money just tends to evaporate. You might have some general ideas about saving and investing, but when it’s all in one place, it’s easier for it to disappear.

This is where the funny-named bank accounts come in.

Daily Expenses: For your day-to-day living expenses, such as food, housing costs, utilities, and fuel.

Splurge Account: Guilt-free spending money for small things like a new pair of shoes or a round of beers for your mates.

Smile Account: More guilt-free spending money, but this time for larger purchases that will put a smile on your face, like a holiday, a new couch, or a car.

Fire Extinguisher: As the name suggests, this account is for fighting “financial fires”, like paying down debt, saving a deposit, or paying off your mortgage.

In summary, under the ‘blow bucket’, the next step is to set up four bank accounts.ING offers barefoot investor accounts.

Let’s take a look at each account in more detail.

#1. Daily Expenses – Your everyday spending you need to live off (60% income)

All of your income should go into your Daily Expenses account. This account is like the routing centre for the rest of your accounts.

You will leave 60% of your income in this account for your daily expenses and then send the rest to your other accounts.

You should aim to limit your daily expenses to 60% of your take-home pay.

We can break this down further:

30% maximum on housing (rent or home loan)

5-10% on utilities

5-10% on transport

5% on insurance

5-10% on food

This 60% is a guideline – those with lower or higher incomes might have slightly different figures. But in most cases, you should be able to keep your daily expenses within this limit. If not, it might be time to re-evaluate your spending and see what you can cut down on.

#2. Splurge Account – Spending on things you love (10% income)

Now that we’ve covered your daily expenses, it’s time to break down the other 40% of your income. We’ll start with the fun one – your splurge account.

Set up an automatic transfer of 10% of your take-home pay from your Daily Expenses account into your Splurge account. Your Splurge account will have its own ATM card. Keep it at the front of your wallet and mark it SPLURGE with a Sharpie.

This is your guilt-free spending money. Go out and blow this money on whatever you want – a new pair of shoes, a round of beers for your mates, whatever you like.

The only rule for Splurge money is simple: when it’s gone, it’s gone. No dipping into other buckets!

Remember once splurge money is gone, it is gone.

#3. Smile Account – long term savings for fun things (10% income)

Another 10% of your take-home pay should be automatically transferred from Daily Expenses to your Smile account (online saver). This isn’t linked to a bank card.

The smile account is for bigger goals like holidays, weddings, and other fun things that will cost more than a few weeks’ wages.

This 10% isn’t set in stone – if you are saving up for something bigger like a wedding or a big overseas trip, do the numbers and see how much you will need to put into your Smile account to make it happen.

But if your smile account is more than 10% of your take-home pay, then you will need to adjust your living expenses accordingly.

Your smile account can be used for an overseas trip.

#4. Fire extinguisher – debt and financial stress reduction (20% income)

And finally, we have the fourth account, which is a fire extinguisher.

This account is also not linked to a bank card.

What you use this 20% for will change over time, but the allocation remains 20%. For example:

If you have high-interest debt (credit cards, personal loans), use it to pay those off first.

Debt-free but saving for a home? Funnel it into your deposit savings.

Already have a home loan? Keep making extra repayments to slash your mortgage.

You will use the fire extinguisher account at different stages in your life for different things…

Check to see if you are eligible for a home loan

Barefoot Investor Bank Account Set Up

In theory, you could set up these four core bank accounts with any bank. But in the Barefoot Investor, Scott Pape recommends that you set up these accounts withING.

Why?

According to the Reserve Bank, Australian households pay roughly $3.9 billion in bank fees each year – about $400+ per household annually . Over a lifetime, that can easily total tens of thousands of dollars.. That money is better off in your pocket, so it makes sense to find a bank with no fees.

This brings us to your new best friend – the ING Orange Everyday debit card. ING has no fees and will even refund your ATM fees as long as you put in $1,000 per month (usually covered by your salary) and make at least 5 transactions with your card.

You can set up your accounts online, and ING often offers recommendation codes that will give you a bonus for signing up. Jump online, search for “ING referral code”, and put in the code to set up your account.

Otherwise, if you don’t have a referral code, you can simply go online and set up an account following the promptshere.

You will need to set up four barefoot investor ING accounts. Two of your accounts will be Everyday bank accounts. Call one “Daily expenses” and the other “Splurge”.The other two bank accounts will be Online Saver accounts. Call those “Smile” and “Fire Extinguisher”.

Setting up your automated saving system

Once your bank accounts are all set up, the next step is to set up your automated payments.

First, contact your employer and tell them to put 100% of your take-home pay into your “Daily Expenses” account. Do it in writing.

Once that’s done, the rest is fairly straightforward.

Set up a recurring transfer from your Daily Expenses account into your other accounts every pay cycle. Here’s how to do it:

Splurge Account: 10% of your take-home pay.

Smile Account: 10% of your take-home pay.

Fire Extinguisher: 20% of your take-home pay.

Once that’s done, you’ve set up the most important part of the Barefoot Investor system.

You now have one account for your daily expenses, another account for guilt-free short-term spending, one for larger purchases that make you happy, and another for fixing your financial fires.

Barefoot Investor Calculator: Split Your Pay Into Buckets

Mojo Bucket

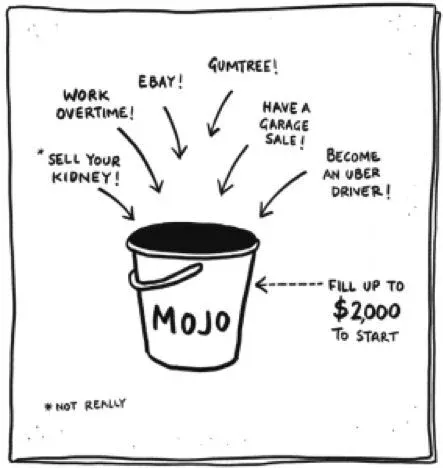

So now that you’ve got your core accounts set up, it’s time to step away and open a separate account. This one is called Mojo account.

This is your emergency money. You only use it for real emergencies, such as losing your job or getting sick. And no, a really good deal on a holiday getaway is not an emergency.

Having this money on hand for emergencies will change how you think about money. Once you know you’re covered in case of an emergency, a great weight will be lifted from your back.

Mojo account is recommended to be with a different bank.

You should set up this account at a completely different financial institution from your other accounts. You do this because you want to put this money out of sight and make it hard to get to. That way, you won’t be tempted to dip into this money unless you really need it.

You can choose any online bank with no fees for this account. Scott Pape recommends UBank USaver, but you can stick with your existing account as long as they don’t charge you any fees.

When it comes to Mojo, you need to start by gathering as much money as you can to save at least $2,000 to get you kickstarted into gear.

Whether it’s selling clothes, your old iPhone, or anything else lying around, it’s about building momentum. The goal? Gather enough to kickstart your Mojo account and give yourself a solid financial safety net.

Once you have the initial $2,000 in this mojo bucket, you won’t be adding to this account in the short term. It will come back into play once you’ve paid off your debts, saved a deposit, and bought a home.

After you’ve done all that, you will use your Fire Extinguisher money to build up a minimum of three months’ living expenses. Moving forward, the Mojo account will act like your credit card.

After that, you continue building your Mojo, which will then move into your Grow Bucket.

Grow Bucket

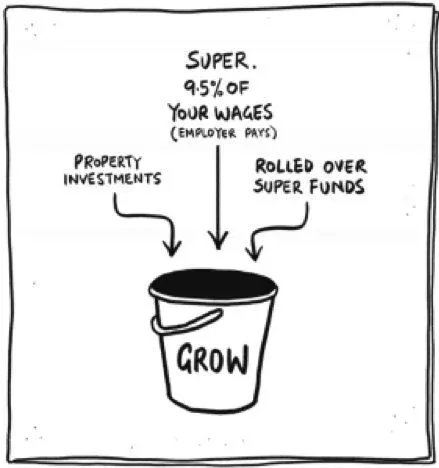

The third and final bucket – the grow bucket – is for building long-term wealth. The aim of this bucket is to get a little wealthier every day.

Thanks to the wonders of compound growth, every dollar you put into this bucket should double every 7 to 10 years or so. That might not sound like much, but over the course of your life, it can make you incredibly wealthy.

This bucket includes your super fund and any other investments you own. For now, it might just be your super, and that’s fine.

Your Grow bucket is outside the scope of this post – we’re focusing here on setting up your accounts. But it’s still a good way to think about your money.

In the Barefoot Investor system, the Grow bucket comes into play once you’ve bought your family home. Once you’ve done that, you will increase your super contribution to 15%.

And once your family home is paid off, you can use your Fire Extinguisher money to start investing. You can invest this money however you like. You can choose to keep it as savings, shares, property or cryptocurrency.

Case Study Of How The Barefoot Investor Accounts Work

Meet Sarah, a 29-year-old nurse living in Brisbane. She earns $85,000 a year before tax—around $66,000 after tax, or about $1,270 a week.

Sarah recently decided to take control of her finances and started using the Barefoot Investor bank accounts system. Here’s how it worked for her.

Step 1: All Her Income Goes into the Blow Bucket

Her weekly income of $1,270 flows into her main transaction account. From there, it’s automatically divided:

Daily Expenses (60%) – $762/week – This covers rent, groceries, petrol, bills, and all her essential living costs.

Splurge (10%) – $127/week – This is guilt-free money for anything she wants—maybe a massage after a long shift or a weekend brunch.

Smile (10%) – $127/week – Sarah is saving for a trip to New Zealand. This account is for life’s fun, big goals—like holidays, weddings, or a new laptop.

Fire Extinguisher (20%) – $254/week – Right now, she’s using this to pay off her $8,000 credit card debt and a $5,000 car loan.

Step 2: Paying Off Debt First

At $254 a week, Sarah will knock out her $13,000 debt in just over 12 months—without tightening her lifestyle too much.

Step 3: Saving for a Home Deposit

Once debt-free, Sarah plans to save a $50,000 deposit for her first apartment. At the same saving rate, she’ll reach that goal in around 3.8 years.

Step 4: Owning Her Home Sooner

After buying, Sarah will keep using the Fire Extinguisher to make extra repayments—cutting years off her mortgage and saving thousands in interest.

Step 5: Building Wealth

Eventually, her Fire Extinguisher becomes her Grow bucket—used to invest and build long-term wealth for retirement.

Why it works for Sarah

Sarah loves this system because it’s simple and stress-free. The money is sorted before she even sees it.

Even though the economy is uncertain, the Barefoot Investor method gives her clarity, confidence, and control. No spreadsheets. No overthinking. Just progress—week by week.

Yes, Scott Pape originally recommended ING because of its low fees and easy online setup. And honestly, it’s still a solid option. But it’s not the only choice. The key is finding a bank that lets you set up multiple accounts, has no monthly fees, and makes automation simple. ING ticks those boxes, but if another bank suits you better—go for it.

What bank accounts does the Barefoot Investor recommend?

“The Barefoot strategy uses three buckets for your money, which translate into five bank accounts:

Daily Expenses – for bills and necessities (Blow bucket)

Splurge – for fun spending (Blow bucket)

Smile – for big treats/long-term purchases (Blow bucket)

Fire Extinguisher – for debt or savings goals (Blow bucket)

Mojo – your emergency fund (separate bucket/account

(Once you’re debt-free, you’ll also start a Grow bucket for investments, but that comes later.)”

What is the Splurge account for Barefoot Investors?

The Splurge account is for guilt-free fun. That’s right—fun with zero regret. Use it for dinners out, a new outfit, a massage—whatever brings you joy. You’re meant to spend it. But once it’s gone, it’s gone. That’s what makes it guilt-free.

How much is in the Mojo account?

Ideally, your Mojo account should hold three to six months’ worth of living expenses – a common rule of thumb recommended by financial advisers.

What is the best bank for the Mojo account?

The best bank for your Mojo account is a different bank from your daily spending—so you’re not tempted to dip into it. Look for one with a high interest rate, no fees, and easy online access (but not too easy to access). Banks like Macquarie, ING, and UBank are all popular options.

What are the 4 buckets of money?

The Barefoot Investor breaks your money into four key buckets:

Daily Expenses – for bills and everyday costs

Splurge – for guilt-free spending

Smile – for saving towards fun goals

Mojo – your emergency savings

Once you’re debt-free and saving regularly, you’ll add a fifth: the Grow bucket, for long-term investing and wealth building.

How to set up the Barefoot Investor accounts?

ING gives out recommendation codes to get $75 when you sign up. Jump online and put in the code, and you’ll be able to set up your account. Otherwise, if you don’t have a referral code, you can simply go online and set up an account following theprompts here.

Once you’ve set up your bank account, your two cards will be mailed out to you.

As it’s an online bank, it’s really easy to do from the comfort of your own home. They also have good customer service if you call them.

How do couples set up their Barefoot accounts?

If you share finances with a partner, you have options. Many couples create joint Daily Expense and Smile accounts for household bills and shared goals, while keeping individual Splurge accounts so each person has their own fun money. The Fire Extinguisher can be joint if you’re tackling shared debts or savings (like a home deposit). The Mojo emergency fund is often joint, since you both rely on it. The key is communicating and ensuring you’re on the same page with percentages and goals

Bonus: Some Important Money Habits

As I have mentioned in this article, managing your money well is the best way to get financial freedom.

Here are some quick money habits you can pick up:

Live below your means. Simply put, this means you must spend less money than you make. But this does not mean you can’t spend money on things you enjoy. It just means being prudent about it.

Close down any unnecessary credit cards. Credit cards tempt you to buy things you can’t afford and may also negatively affect yourcredit rating.

Set good money (and life) goals. But don’t overwhelm yourself with too many goals. Start with one goal, e.g. I want to save $2,000 in my emergency fund. Once you have achieved that goal, move on to the next one.

Regularly review your progress to see if you are on the right track. Sometimes your goal may seem to be taking too long, which can be discouraging. But regularly reviewing your progress will reassure you that you are making steps in the right direction.

Find ways to make a little extra income on the side. You can freelance after work or get small jobs on the weekends. However, don’t forget to also set aside time to rest and relax.

Budget for big expenses like weddings, holidays, etc. Weddings and holidays don’t just happen suddenly. They usually take a few months to plan, giving you enough time to save for all the associated expenses.

Automate bill payments whenever possible. Automating bill payments is the best way to ensure that you don’t miss any payments, and this can save you money in penalties and prevent you from negatively affecting your credit score.

Create a budget and stick to it. Track your income and expenses to ensure you live within your means.

Pay off debt as quickly as possible. Paying off debt is one of the best ways to increase financial security. It helps you maintain a good credit score, but even better, it helps you save by reducing the interest you pay on your debts.

Next Steps And Getting Your Home Loan

Have you saved money for a house deposit, but don’t know where to start in buying a home?

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one-person operations, we havean entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 orbook a free assessment onlineto see how we can help.

Our team of home loan experts is here to help you buy a home in Australia

Choose a goal, enter your take-home pay and see an example way to split it. Change the amounts to fit your real budget.

General information only. This tool gives simple examples and rough time estimates. It does not know your full financial situation and is not personal financial advice or a home loan assessment.

Example figures are shown. Replace them with your own amounts.

Your take-home pay

$

Enter the amount that reaches your bank account after tax. If your pay changes, use a conservative average based on recent pay periods. If you plan with total household pay, use household figures consistently — don't mix one person's pay with household expenses.

$

Suggested example: $500 per fortnight (the "Main goal" share of the split below). Change this to an amount that suits your actual budget.

Your deposit goal

$

A 20% deposit may help you avoid Lenders Mortgage Insurance, subject to the lender's valuation and policy.

$

May include transfer duty, conveyancing, inspections, lender fees and moving costs.

$

🏠 Your rough home savings estimate

Rough time to reach the target: 8 years and 6 months

Deposit target (20% of $650,000)$130,000

Other buying costs entered$0

Total savings target$130,000

Saved so far$20,000

Still to save$110,000

Amount added each fortnight$500

15% of your savings target

This assumes the property price and your savings amount do not change. It does not include interest earned, changes in property prices, grants, government schemes, FHSS, lender valuation or loan approval.

Example 60/10/10/20 split

This is a starting example only. Change the percentages and amounts to match your actual expenses and priorities.

Spending moneyEveryday extras and fun$250/fortnight

Short-term savingsBigger purchases — holidays, a new couch$250/fortnight

Main goalTowards your home deposit$500/fortnight

Your current split totals 100%.

Start with your real essential costs. If they are more than 60% of your pay, increase the Essentials amount and reduce the other categories.

What Hunter Galloway can help with: Hunter Galloway is a mortgage broker. We can help assess borrowing power and provide credit assistance for home loans and refinances. What this calculator does not provide: personal budgeting, investment, debt-counselling, tax or legal advice. It is not a loan quote, recommendation, pre-approval or approval.

Planning to buy a home?

This savings estimate does not show how much you can borrow. Hunter Galloway can assess your income, expenses and debts and explain suitable home loan options.

Home loan assessment, subject to lender policy and approval. 1300 088 065

Important information. This calculator provides general information and simple mathematical estimates only. Using this tool is not personal financial advice, credit assistance, debt counselling, tax advice or legal advice. It is not a loan quote, recommendation, pre-approval or approval. The example income split may not suit your circumstances — actual results will depend on your income, expenses, debts, interest, fees, repayments, savings returns, property prices, buying costs and changes in your circumstances.

Hunter Galloway is a mortgage broker and may provide credit assistance for home loans and refinances separately, after assessing your circumstances and providing the required disclosures. If you are having difficulty paying debts or bills, contact the National Debt Helpline on 1800 007 007 for free and confidential financial counselling. For personal financial advice, speak with an appropriately authorised financial adviser. Your entered amounts stay in your browser and are not sent to us or to analytics. Hunter Galloway Finance Pty Ltd — Credit Representative 476903 authorised under Australian Credit Licence 389328.