So, what happens if your settlement is delayed, and what are some of your rights and things that you can do when it happens? Well, in this section, we will break it down by state because every state is a little bit different.

Note: This isn’t legal advice. You should consider your personal situation and speak to a lawyer.

Queensland: Unfortunately, it’s one of the harshest states in Australia. In Queensland, one of two things happens. Number one, the seller will agree to extend your settlement, and it’ll be fine – you can push it back a couple of days if everyone’s pretty happy. Number two, which is the worst case, is if you’ve determined a settlement date on the contract, the seller can choose to terminate the contract altogether. That means that they can take your deposit. So, if you put down 5% or 10% of the property’s purchase price on the contract, they can actually take that if your settlement is delayed.

Western Australia: They’re a little bit more lenient than Queensland. They generally have a rule that gives you a three-day leniency on the settlement date. So, if you can’t make it on Monday, they might push it back three business days, but then they will start charging you penalty interest for every day that you’re late. Again, the conditions will depend on your contract, so check it out with your lawyer.

New South Wales: They will charge you penalty interest for every day that you’re late. Then, they can issue what’s called a notice to complete. This document says that you must settle on a certain date, or the contract will be terminated, and you’ll forfeit your deposit. The number of days in the notice to complete is usually about 14 days, so at least you’ve got a bit of breathing space there, but obviously, it is not a situation you want to get to, and you want to resolve quickly.

Victoria: In Victoria, it’s similar to New South Wales. They will charge you penalty interest, which can be up to 10% every day that you’re late. So you can end up racking up thousands of dollars in extra penalty fees that you wouldn’t otherwise have to pay if your settlement wasn’t delayed.

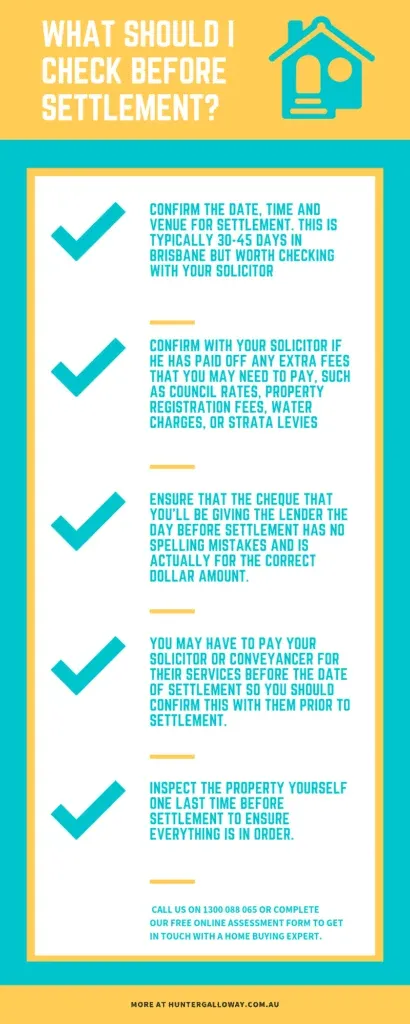

The final inspection is your last chance to check the property before you hand over the money. Once settlement happens, it is very difficult to get the seller to fix anything.

We recommend doing this inspection 24 to 48 hours before settlement.

Use this checklist to make sure you don’t miss anything:

Tip: If you find a new issue that wasn’t there when you signed the contract (like a hole in the wall from moving furniture), take a photo and send it to your solicitor immediately. They may be able to withhold a small amount of funds at settlement to cover the repair.