One of the key advantages of a guarantor home loan is the potential to increase your borrowing power.

But what does this mean, and how does it work? Let’s break it down.

Borrowing power refers to the maximum amount that a lender is willing to loan you.

It’s calculated based on several factors, including your income, expenses, existing debts, and the number of

dependents you have.

Broadly speaking, the banks will lend between 5 to 6 times your income. So if you are earning $50,000 you

might be able to borrow up to $300,000.

For a more specific example, we have shown how much a single person could borrow if they were earning $75,000 per

year and had no credit cards, AfterPay or personal loans.

To find out what your borrowing power is, get in touch with our

team or call on 1300 088 065 and we can let you know.

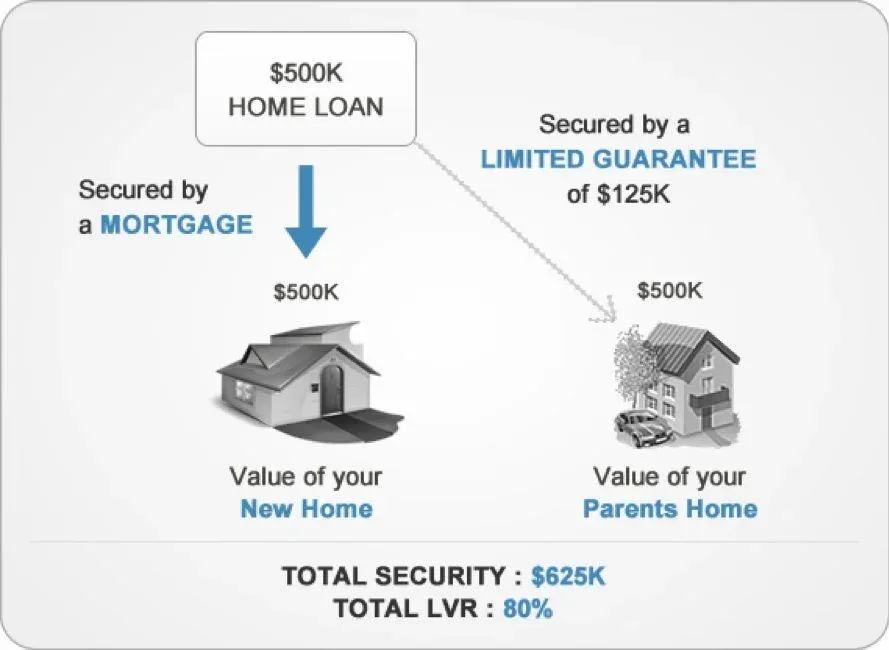

A guarantor can significantly boost your borrowing power in the following ways:

– Larger Loan Amounts: With a guarantor, you can potentially borrow up to 105% of the property’s

value. This can give you more options when house hunting and cover additional costs like stamp duty and conveyancing

fees.

– Avoiding LMI: Lenders Mortgage Insurance (LMI) is typically required when you borrow more than

80% of the property’s value. However, with a guarantor, you can avoid this cost, which can add up to thousands of

dollars.

– Better Interest Rates: Some lenders offer discounted interest rates for loans with a guarantor,

which can save you a significant amount over the life of your loan.