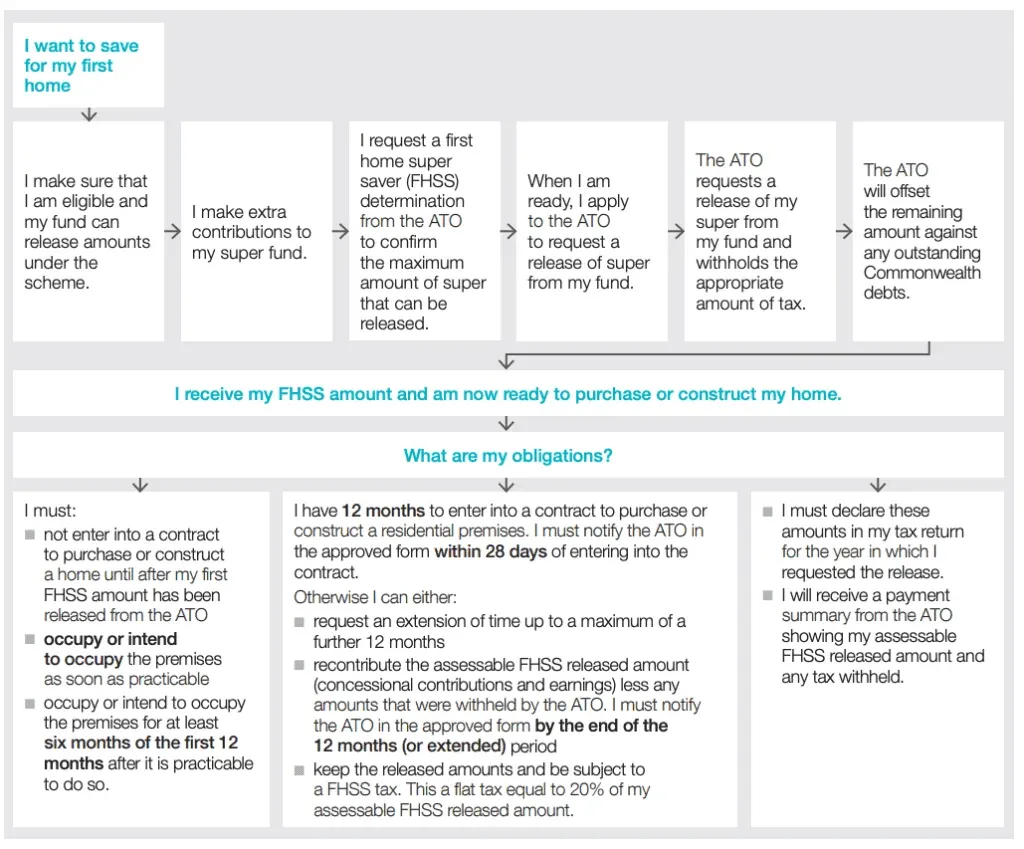

The First Home Super Saver Scheme (FHSSS) can be a powerful way to boost your home deposit using tax-effective super contributions, but its rules are more complex than many first-home buyers realise. From strict timelines and tax implications to contribution ordering and deemed earnings, understanding how the scheme actually works can make the difference between maximising your benefit or facing unexpected costs.

This guide, written by an expert mortgage broker in Brisbane, breaks down everything you need to know about the FHSS, including advantages and the hidden pitfalls so you can decide whether FHSSS truly suits your home-buying strategy.

Let’s dive in