Did you know that 77.3% of Australian homebuyers now choose a mortgage broker? This record-high preference, confirmed by the MFAA, shows that most buyers find brokers essential for navigating today’s complex market.

The data is clear. Partnering with a professional is the smartest way to secure your financial future.

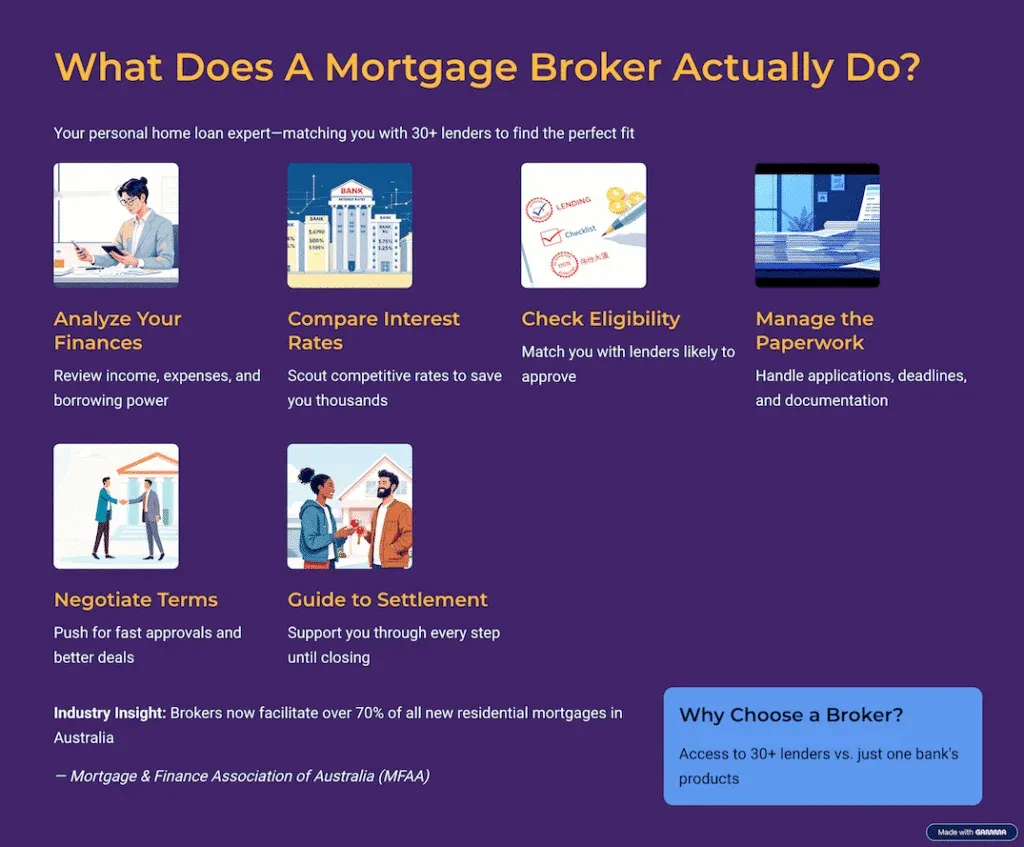

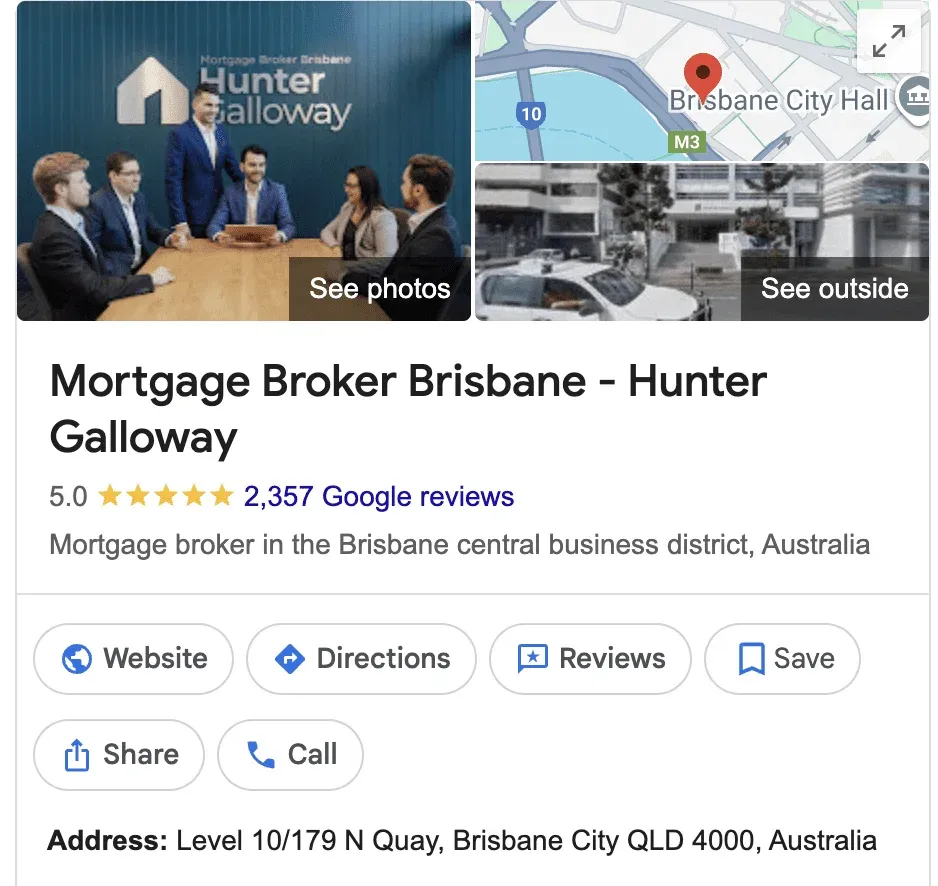

However, finding the right mortgage broker in Brisbane is just as important as the loan itself. You need an expert who simplifies the application process while providing stress-free, professional advice.

In this expert-written guide, you will learn how to find a broker who truly works for you.

Let’s dive right in.