Underquoting—also known as ‘bait-pricing ‘—is when an agent knowingly lists the price of a property as lower than the true value of the home or less than the price the seller is willing to accept. They then hold bogus auctions, knowing fully well that they are going to reject every bid and then sell the house for a much higher price.

Underquoting is illegal, but it can be very difficult to prove if you don’t have the evidence. So here is a step-by-step guide on how you can get the evidence to prove underquoting.

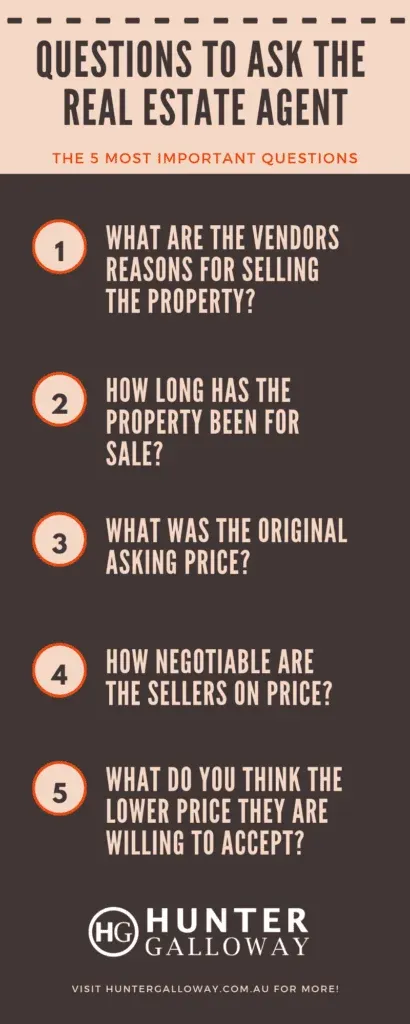

Step 1 – If you suspect a property is being underquoted, then ask the agent pointed questions about the price. Do they think it is a fair price? What is the reserve, and what do they think the home will sell for? Make sure to use emails or text messages so you have written evidence with a timestamp. They might give you vague answers, but that’s okay.

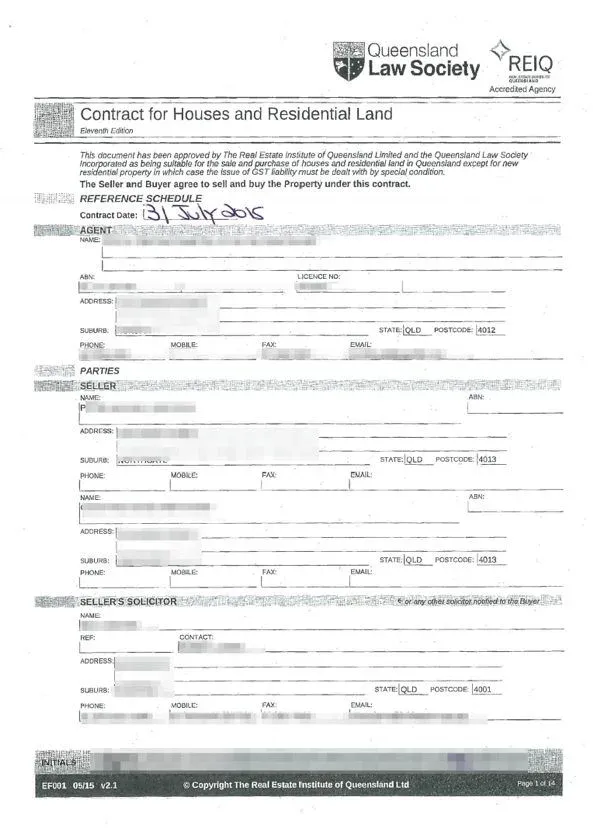

Step 2 – Get a copy of the contract and make an offer above the asking price. It is perfectly acceptable to do that even for properties that are going to auction. For example, if the property is listed for $500,000, you can make an offer of $550,000—that’s 10% above the asking price. To make it even more interesting, you can add two dollars. So, make an offer for $550,002. Make sure to put this in an email, quoting whatever conversations you have had, and then ask them to take your offer to the seller. They have to do it because they cannot just ignore an offer. Of course, at this point, the agent, who knew the value of the house was actually $900,000, has already started sweating.

Step 3 – But you can make it even harder by including, with your written offer, a personal check with a deposit of 8-10%. Personal cheques are fast and easy, and don’t have the hassle of bank cheques. This is assuming they had given you the contract. But even if they didn’t, you can still make your offer ‘in good faith.’ They cannot reject a good-faith offer.

Step 4 – On the off-chance that the seller accepts your offer, then congratulations, you have just gotten yourself a bargain.

Step 5 – However, the likely scenario is that the seller will reject the offer—after all, no one in their right mind would accept an offer that is almost $400,000 less than the value of their property. Once this has happened, ask the agent to increase the advertised price to a price above your offer. Be sure to remind them about the additional $2. So they can’t re-advertise the property and increase the price to $550,000. It has to be above $550,002. If, after, say, two days, the price hasn’t been updated, send them an email asking why the listing is not yet reflecting your rejected offer, since this is against underquoting laws.

Step 6 – At this stage, the agent may increase the listing to $560,000 because it is crazy to list a property for $550,003. If they do that, then start the process again and make another offer 10% above the new asking price plus $2. Keep doing this until the day of the auction

Step 7 – On auction day, ask the agent what the reserve is. They probably won’t tell you, but when the property finally sells, it means the reserve has been met. Take note of the final selling price of the property.

Step 8 – Now, you have enough evidence to lodge a complaint with the Consumer Affairs department in your state. Use the initial advertised value, your rejected offers, and what the property finally sold for. Here, you want to show that the advertised price was too low because of the leaps and bounds the property price went up by before the auction. Also, if the agent tried to ignore your offer or slow down the process in any way, then you can present that as well. Include all the conversations you had via text and email. This is why it is important to have all conversations in writing.

You can report underquoting in each of the states using the following links:

QLD: https://www.qld.gov.au/law/your-rights/consumer-rights-complaints-and-scams/make-a-consumer-complaint

NSW: https://www.fairtrading.nsw.gov.au/help-centre/online-tools/make-a-complaint

WA: https://www.commerce.wa.gov.au/consumer-protection/how-lodge-formal-complaint

TAS: https://www.cbos.tas.gov.au/topics/products-services/problems/resolve-problem-complaint/complaint-process

SA: https://www.cbs.sa.gov.au/

NT: https://consumeraffairs.nt.gov.au/for-consumers/consumer-conciliation-request

VIC: https://www.consumer.vic.gov.au/contact-us/resolve-your-problem-or-complaint/overview