A lease is a legally binding agreement. If a tenant breaks the lease before the end of the term (the fixed-term agreement) without sufficient reason, they are breaking the lease. This is also called breaking the rental agreement.

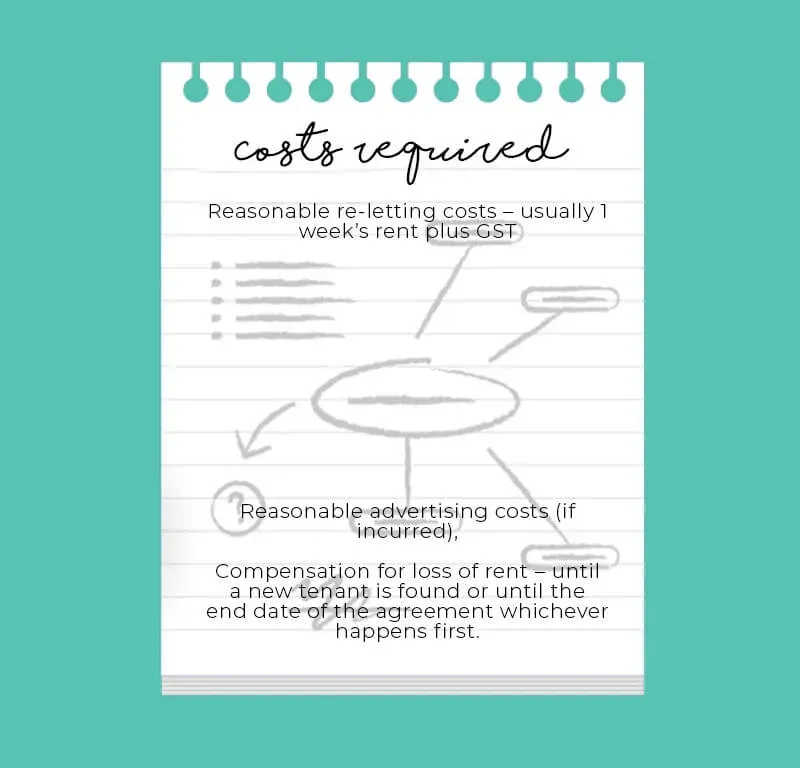

The bad news: breaking a lease may require you to pay compensation to the owner or property manager. This could continue until the end of the original lease or until the property is re-let, because of potential loss of rent.

The good news: there are a few ways around this.

Usually, a homebuyer finds the perfect property and is ready to move. But sometimes, they still have 2, 3, or 6 months left on their lease.

Under the lease agreement, if you leave with 2 months remaining, you technically owe the owner or property manager for those 2 months of rent, even if you’re no longer living there.

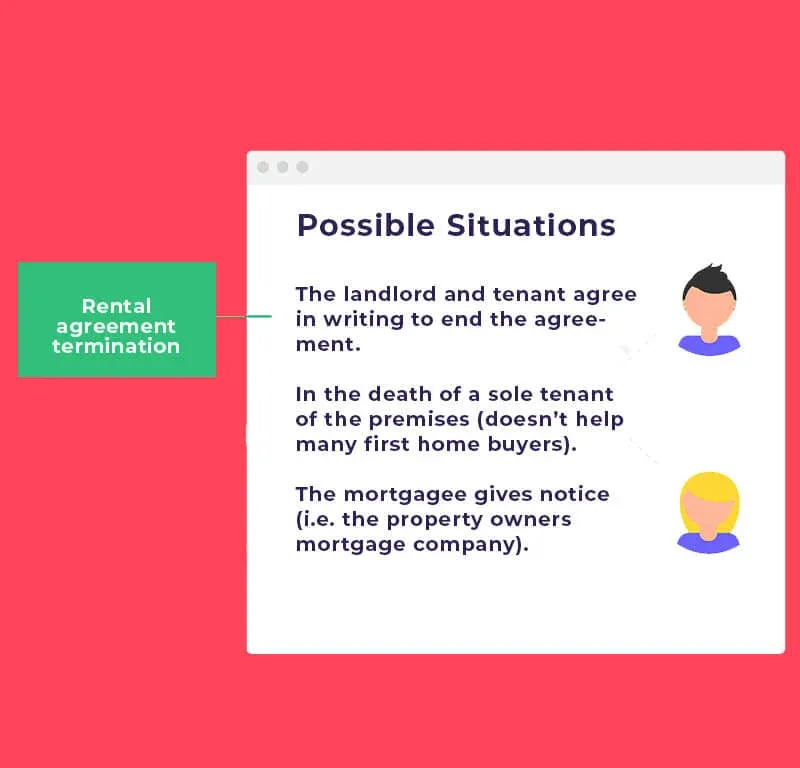

It is possible to end a rental agreement immediately in the following cases:

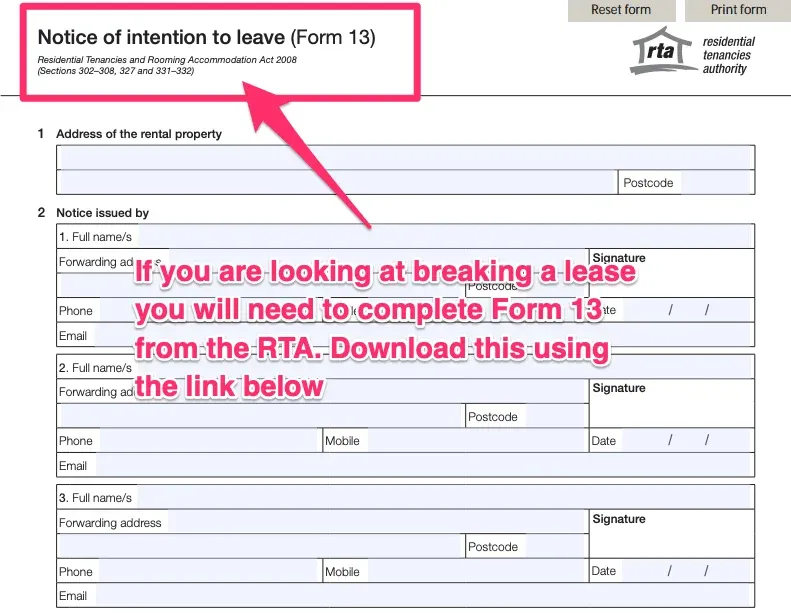

Realistically, first-home buyers usually only have option 1 available if they want to break the lease without paying compensation. More on the costs and strategies is covered below.

People break leases all the time, so if you need to break your lease, don’t worry — it’s completely doable.