For many first home buyers, purchasing your first home is exciting, but even small oversights can cost you thousands or delay your approval. Along with choosing the right property, it’s essential to understand how lenders assess your finances, how to research your market carefully, and how to negotiate confidently. This guide, written by an expert mortgage broker in Brisbane, combines the key mistakes first home buyers often make together with essential homebuying tips — helping you move forward with clarity and confidence.

1. Going Directly To The Bank Without Using A Mortgage broker

Going directly to the bank can limit your options and cost you money. Mortgage brokers work with multiple lenders and can find deals that may not be advertised publicly. They also guide you through complex paperwork and negotiate better rates or loan features on your behalf.

According to the Mortgage & Finance Association of Australia (MFAA), 70% of first home buyers who used brokers found better deals than going directly to a bank. Home loan approvals are faster on average when brokers handle documentation and lender communications

Why Using a Broker Helps:

- Access to a wider range of lenders and home loan products.

- Expert guidance on loan structures, interest rates, and fees.

- Saves time and reduces stress during the approval process.

- Brokers can sometimes secure exclusive offers not available directly from banks.

Tips for First Home Buyers:

- Always compare options with a broker before committing to a bank loan.

- Ask about broker fees upfront — many are paid by the lender, not you.

- Use brokers to clarify confusing terms like variable vs fixed rates or offset accounts.

By skipping a mortgage broker, you might miss competitive rates, flexible loan features, or faster approval times. First home buyers who leverage brokers often save thousands over the life of their loan.

2. Not Paying Attention To Credit Score & Credit Report

Why Your Credit Profile Matters for First Home Buyers

Many first home buyers underestimate how much their credit score and credit report influence a home loan approval. Lenders don’t just care about your deposit — they look deeply at how you manage your credit. A good score boosts your chances, while a poor or messy credit file can block your path or force you into a more expensive loan.

In Australia, credit scores generally run between 0 and 1,200, depending on the credit reporting agency (Equifax, Experian or illion). Lenders often prefer scores in the “good” to “excellent” range — roughly 622–1,200, depending on the bureau.

How a Low (or Dirty) Credit Score Can Bite You

If you’ve got late payments, defaults, or too many credit applications, that raises red flags. Lenders may respond by:

- Offering higher interest rates, which can cost you thousands over time.

- Lowering the loan-to-value ratio (LVR) you can access, meaning you might need a bigger deposit or pay for Lenders’ Mortgage Insurance (LMI).

- Even declining your application — especially if your credit score falls in the “below average” band.

What Lenders Actually Look at

Here’s what they check:

- Payment history — missed or late payments count heavily.

- Outstanding debt — high credit-card balances or too many active accounts can reduce your score.

- Credit applications — each “hard inquiry” (like applying for a pre-approval) stays on your file and can hurt your score.

- Credit length — a longer credit history (even with low usage) helps.

Smart Moves: What First Home Buyers Can Do Now

Here are practical homebuying tips to clean up or build your credit profile:

- Pay all your bills on time. Automate repayments for loans, credit cards, and utilities.

- Reduce high-interest debt. Focus on credit card balances — the lower they are, the better your credit utilisation ratio.

- Avoid applying for new credit. Don’t open new lines (cards or loans) in the months before your home loan application.

- Review your credit report. Check for errors like old defaults, incorrect balances, or unrecognised accounts, and dispute them.

- Work with a broker. A mortgage broker (like us) can guide you to lenders who are more lenient with credit risk or who weigh other strengths in your application.

- Delay applying if needed. If your credit score is weak, wait 3-6 months to improve it. Small improvements can unlock better interest rates or terms.

The Payoff for Getting Your Credit Right

By improving your credit score and cleaning up your report, you’ll likely:

- Increase your borrowing capacity

- Qualify for lower interest rates

- Avoid unnecessary LMI or reduce how much you pay for it

- Gain access to better loan products with favourable terms

Bottom line: Don’t treat your credit report like an afterthought. For first home buyers, it’s one of the most powerful levers you have to unlock better borrowing power and cheaper home financing.

3. Not Getting A Pre-Approval

For first home buyers, skipping a home loan pre-approval is a costly mistake. Pre-approval gives you confidence and shows sellers you’re serious. Without it, you risk losing your dream home or your deposit.

Pre-approval is when a lender reviews your financials and agrees, in principle, to lend you a specific amount. Many buyers mistakenly put down a deposit—or even sign a contract—before securing pre-approval. Don’t fall into this trap.

First Home Buyer Case Study: Marley and Jet

Marley and Jet had saved diligently for a deposit and researched their borrowing capacity using online calculators. Confident they could borrow over $1 million, they aimed for a property around $800,000.

They skipped pre-approval to avoid affecting their credit score. After seven weeks of house hunting, they found a property they loved. Their $817,500 offer was accepted—only to discover their bank approved a maximum of $500,000.

This left them facing a significant shortfall and a stressful situation they hadn’t anticipated.

Why Pre-Approval Matters

Even strong financial positions can hide lending issues. Pre-approval:

- Confirms your borrowing capacity before you make an offer.

- Lets the bank review your income, bank statements, and credit history.

- Identifies potential issues early, reducing delays or surprises.

- Strengthens your position when negotiating with sellers.

Credit Score and Pre-Approval

Many first home buyers worry that pre-approval harms their credit. The impact is minimal if you:

- Apply with a single lender at a time.

- Limit applications to once every three months.

- Maintain stable financial habits.

This approach protects your credit while securing your pre-approval.

How Long Do Pre-Approvals Last?

A pre-approval is typically valid for 90 days, with some banks offering extensions if your financial situation remains stable.

Benefits include:

- Free assessment of your borrowing power.

- Confidence when making offers.

- Peace of mind knowing your finance is ready.

Next Steps for First Home Buyers

If you’re serious about buying your first home, start with pre-approval.

Hunter Galloway – Mortgage Broker Brisbane can guide you through the process, from pre-approval to settlement.

Top Homebuying Tips for Pre-Approval:

- Gather recent payslips, bank statements, and tax documents.

- Check your credit score and correct any errors.

- Avoid major purchases or credit applications before applying.

- Consider using a mortgage broker to access multiple lenders.

4. Stop Thinking You Need A 20% Deposit

Many first home buyers believe a 20% deposit is mandatory. While it lowers repayments and often secures better rates, it’s not essential.

For example, on an $800,000 property, a 20% deposit means saving $160,000—a long and stressful journey for most buyers.

Smaller Deposits Are Possible

- Many lenders now accept 8–10% deposits.

- Some even offer 5% deposits, though Lenders Mortgage Insurance (LMI) may apply.

- LMI is a one-off fee that protects the bank if the borrower defaults. [Learn more about LMI here.]

If 20% feels out of reach, aim for 8–10% instead. Use our Deposit Calculator to see how smaller deposits affect your home price and repayments.

First Home Buyer Case Study: Mia and Liam

Mia and Liam wanted to save a full 20% deposit to avoid LMI and cover costs like stamp duty.

After reviewing their finances, we discovered they could avoid LMI using just a 5% deposit on an $800,000 property by leveraging the First Home Guarantee Scheme.

This government-backed initiative allows eligible buyers to:

- Purchase a home with as little as 5% deposit.

- Have the government act as guarantor for the remaining 15%.

- Avoid costly LMI, saving tens of thousands in fees.

For Mia and Liam, this meant:

- Skipping 18 months of extra saving.

- Purchasing their home in just 11 weeks.

- Accessing a property sooner without straining their budget.

How the First Home Guarantee Helps

The First Home Guarantee opens pathways for buyers to:

- Bypass LMI and save significant costs (e.g., $44,000 on an $800,000 purchase).

- Buy with a smaller deposit, or in some cases, no deposit with a guarantor.

- Accelerate their homebuying journey with expert guidance.

Key Takeaways for First Home Buyers

- A 20% deposit isn’t required to buy your first home.

- Government schemes and smart mortgage structures can reduce upfront costs.

- Engage a mortgage broker to explore eligibility for grants, schemes, and lender-specific solutions.

- Starting the process early could surprise you with your eligibility now.

Read more: Can I get a home loan with no deposit?

5. Not Budgeting For Lenders Mortgage Insurance

Lenders Mortgage Insurance (LMI) is one of the most common surprises during the home loan process. LMI protects the lender, not you, when you borrow with a deposit under 20%. Because of this, it can add a significant cost to your upfront expenses or your loan balance.

Yet with the right strategy, you can plan for it, reduce it, or even avoid it.

What LMI Actually Covers

LMI is not insurance for your home. It is a risk fee charged by the lender. It protects them if you cannot repay the loan. Most banks apply it when your Loan-to-Value Ratio (LVR) is above 80%.

This means if you buy a $700,000 property with less than a $140,000 deposit, you’ll likely pay LMI. Many first home buyers don’t find this out until they’re deep into the application process.

How Much LMI Costs First Home Buyers

The cost depends on your loan amount, your LVR, and your lender’s pricing model. As a guide:

- A $600k loan at 90% LVR can attract around $10,000–$15,000 in LMI.

- A $700k loan at 95% LVR can push LMI above $20,000–$25,000.

- LMI increases sharply once you cross the 90% threshold.

Most banks let you capitalise the LMI, which means adding it to your loan. But this increases your repayments and interest costs over time.

Why Failing to Budget for LMI Causes Stress

Not budgeting for LMI often leads to:

- Needing a larger deposit than expected

- Being forced to choose a cheaper suburb

- Delays while saving more

- A smaller borrowing capacity

- Extra stress during the approval process

The good news is you can plan ahead and avoid surprises.

Smart Ways to Reduce or Avoid LMI

- Use Government Schemes- Schemes like the First Home Guarantee let eligible first home buyers purchase with a 5% deposit and no LMI.

- Increase Your Deposit Slightly – Sometimes adding 1–2% more deposit reduces your LVR enough to dramatically cut LMI. Even an extra $5,000–$7,000 can save thousands.

- Check for LMI Waivers – Some lenders offer LMI waivers for specific professions. This includes doctors, accountants, engineers, and select government employees.

- Compare LMI Providers – Different lenders use different LMI insurers. Because of this, the LMI fee can vary widely between banks. A mortgage broker can show you which lender has the lowest LMI for your situation.

Bottom Line: LMI Isn’t Always Bad — But It Must Be Planned For

LMI helps many first home buyers get into the market sooner, especially in rising markets. But the key is planning. When you understand the cost early, you can budget correctly, choose the right lender, and avoid unnecessary financial pressure.

6. Waiting (And Waiting, And Waiting) To Have Genuine Savings

Many first-home buyers delay their purchase, thinking they need years to build “perfect” savings. In reality, banks look for genuine savings, not just large lump sums or gifts.

Genuine savings show lenders you have skin in the game—money you’ve personally saved and managed responsibly. This gives them confidence you can handle mortgage repayments.

What Are Genuine Savings?

Banks typically require applicants to hold at least 5% of the property’s purchase price in an account for 3 months or more. This demonstrates financial discipline.

Examples of genuine savings include:

- Money saved over at least 3 months

- Shares or managed funds held for 3 months or longer

- Equity in property or real estate

- Term deposits maintained for 3 months or more

- Contributions via the First Home Super Saver Scheme (FHSSS)

- Some lenders accept consistent rental payments for 3+ months

Exceptions: Not Every Bank Requires Genuine Savings

Some lenders are more flexible and may waive the genuine savings requirement if you can provide:

- Rental history: A record of 6–12 months of on-time rent payments, verified by a rental ledger or letter from a licensed real estate agent

- Deposit size: If you have 10% or more, some banks won’t require genuine savings

Key Takeaways for First Home Buyers

- Genuine savings show lenders your ability to manage money responsibly.

- You don’t need to delay buying for years—strategic savings over 3 months can be enough.

- Gifts, bonuses, or tax refunds do not count unless held in your account long-term.

- Understanding lender requirements early can speed up loan approval and reduce stress.

For more details, see our article: Genuine Savings Explained.

7. Thinking Rent Money Is Dead Money

You may have heard people say, “Rent money is dead money.” The truth is, that’s a myth.

With median property prices in major cities rising, renting can sometimes make more financial sense than buying. Smart planning and strategy matter more than following old advice.

Let’s break it down with numbers.

Example: Renting vs Buying with an $800,000 Loan

- Salary: $70,000 per year

- Rent: $400 per week in a desirable suburb like Hamilton, Brisbane

- Annual rent: $20,800

If you buy the same property for $800,000 at 4.50% interest, your yearly interest payments alone would be roughly $36,000.

Add mortgage repayments, and you could be paying $50,000+ per year.

Other ownership costs include:

- Council and water rates

- Home and contents insurance

- Maintenance and repairs

- Strata fees (if a unit)

These can add another $5,000+ annually.

Effectively, buying could cost you $30,000 more per year than renting in this scenario.

Why Renting Isn’t “Dead Money”

By renting, you could invest the difference of $30,000 per year elsewhere—maybe in property, shares, or other income-generating assets.

This approach, called rentvesting, lets you enjoy your preferred location while building wealth strategically. It combines lifestyle and smart investment, especially for first-home buyers who want flexibility.

Of course, owning a home isn’t just about finances. Emotional and family reasons matter, too—but knowing the numbers helps you make an informed choice.

For more guidance on whether to rent or buy, check out our video below.

8. Relying On Online Calculators

It’s natural to jump online and use borrowing power calculators. They can give a quick snapshot of what you might afford.

You can check:

- Estimated monthly repayments

- Maximum borrowing power

- Different loan scenarios

But here’s the catch: these calculators are often inaccurate—sometimes by hundreds of thousands of dollars.

Why Online Calculators Can Be Misleading

Calculators rely on general assumptions about:

- Living expenses

- Existing debts, like credit cards or personal loans

- Income stability and bonuses

- Loan-specific fees and conditions

Banks take all these factors into account when assessing your application. Online tools cannot capture the full picture.

Example:

- Couple’s combined income: $140,000

- No credit cards or loans

- CBA Bank calculator: suggests borrowing $620,000

- Broker calculator: assuming $4,000/month in expenses, shows borrowing up to $800,000

That’s a $180,000 difference—enough to affect your property choice significantly!

Tips for First-Home Buyers: Maximise Your Borrowing Power

- Talk to a mortgage broker: They analyse your finances in detail and give a realistic borrowing figure.

- Consider all expenses: Banks factor in more than just your income. Don’t rely on calculators alone.

- Use professional tools: Our Borrowing Power Calculator or a Free Housing Affordability Report can provide more accurate results.

Getting expert guidance early ensures you target homes within your true budget and avoids disappointment later.

9. Looking For Your Forever Home

Buying your first home is exciting, and it’s easy to fall in love with the idea of a “forever home.”

But here’s the truth: most first-home buyers won’t stay in their first property forever. Life circumstances change—relationships, career moves, or starting a family can all prompt a move.

According to the ABS 2021 Census, one-third of people aged 20–29 moved home in the past year. Nearly 25% of people aged 30–39 changed addresses within the same timeframe.

Cotality shows that first-home buyers typically stay in their first home for 5–7 years before upgrading or relocating.

Why Chasing a Forever Home Can Backfire

Falling in love with a property too early can cloud your judgment. Real estate agents are experts at spotting emotional buyers.

- Emotions affect negotiation: Agents may push prices higher if they sense urgency or attachment.

- You might overlook fundamentals: It’s easy to ignore important criteria when smitten by charm or style.

Key Questions Before Making an Offer

Even if a house feels perfect, check these essentials first:

- Is the property size suitable for your needs now and in the near future?

- Are schools, parks, and recreation facilities nearby if needed later?

- Is public transport and shopping convenient?

- What’s your expected commute time?

- Is the neighbourhood safe, friendly, and well-maintained?

- Does the property have potential for growth in value?

The Stepping-Stone Approach

Think of your first home as a launchpad rather than a permanent destination. It’s an opportunity to:

- Build equity over time

- Learn about the property market

- Position yourself for a future upgrade

Remember, your first home doesn’t have to be perfect—it just has to be right for now. And if it isn’t the “one,” there’s almost always another suitable property nearby.

Buying with a clear head and realistic expectations can save you stress, money, and negotiation headaches.

10. Not Thinking About Life Changes

Many first home buyers make the mistake of focusing only on the property itself and forget to plan for life changes that may affect their home choice or loan structure.According to Cotality, homeowners who plan 5–7 years ahead are less likely to sell prematurely due to lifestyle misalignment. Lenders may approve larger loans if you demonstrate forward-thinking and stable income projections.

Key Life Changes to Consider:

- Starting a Family: Will there be enough bedrooms, bathrooms, and outdoor space in a few years?

- Career Changes: Relocation, promotions, or starting your own business may affect your income or commute.

- Lifestyle Shifts: Hobbies, pets, or elderly relatives moving in can change space requirements.

- Investing & Renovations: Planning ahead allows you to choose a property with potential for value growth or expansion.

Why Planning Ahead Matters:

- A property that works for a couple now might not suit a family in two years.

- Suburbs evolve—schools, transport links, and amenities may affect lifestyle and property value.

- Strategic loan structures, like flexible repayment options or offset accounts, protect you during major life transitions.

Homebuying Tips for Life Changes:

- Think beyond your current needs and visualize your home in 5–7 years.

- Factor in potential salary increases, career shifts, or family growth when choosing loan size.

- Consult a mortgage broker to align your loan structure with your life plan.

Planning with a long-term perspective prevents costly moves, stressful renovations, and financial strain. First home buyers who anticipate life changes make smarter, more confident decisions.

11. Not Knowing Who The Real Estate Agent Is Working For

Overextending means taking out a loan bigger than what you can truly afford. One common mistake first-home buyers make is trusting the real estate agent blindly. Remember: the agent is legally and ethically obligated to work for the seller, not you.

Even friendly agents with a helpful demeanor are still focused on getting the best price for their client. Sharing too much personal information can unintentionally weaken your negotiating position.

Why Over-Sharing Can Cost You

Many first-home buyers don’t realise how much the agent knows. For example:

- Telling an agent your small 5% deposit may make them prioritise offers with higher deposits.

- Sharing your pre-approval limit or excitement can encourage the agent to push your offer higher.

- Disclosing how much you love the property can reduce your bargaining power.

Even if it feels counterintuitive, hold back personal financial details until you’ve prepared your best offer.

Case Study: Dan and Jess

Dan and Jess fell in love with a charming Queenslander. The selling agent was friendly, and they felt comfortable sharing their pre-approval and deposit size.

What they didn’t know: the agent also had information about an elderly couple making a competing offer. Their own offer ended up $25,000 over their budget, and they missed out on the property.

The takeaway: agents can unintentionally (or strategically) use your personal info to prioritise other buyers.

Understanding the Multiple-Offer Process

When multiple buyers are interested, agents follow a multiple-offer process, which differs by state. For example, in Queensland:

- Agents must immediately inform the seller of all offers.

- They act according to the seller’s instructions to obtain the maximum sale price.

- They must treat buyers fairly and avoid misleading conduct.

Bottom line: agents are there to get the highest price for the seller, not to help you get a bargain

How To Work with Real Estate Agents Wisely

While agents work for sellers, they can still provide useful information if you know what to ask. Key questions include:

- Why are the vendors selling the property?

- How long has the property been on the market?

- What was the original asking price?

- Are the sellers ready to negotiate on price

By asking these questions, you gain insight without compromising your position.

Next Tips for First-Home Buyers

- Stay professional and strategic when interacting with agents.

- Keep your financial details private until your offer is final.

Read our guide on dealing with real estate agents to improve your negotiation confidence.

Check to see if you are eligible for a home loan

12. Champagne Taste, Beer Budget: Knowing Your Budget

When I bought my first home, I quickly learned the temptation of a property above my budget. Expensive houses always look appealing, but overspending can derail your finances.

Banks offer a borrowing limit for a reason — it reflects your ability to comfortably repay the loan. Buying beyond that limit can create long-term stress.

Even friendly real estate agents may encourage you to stretch beyond your means, but staying disciplined is key. Circumstances can change at any time, so stick to your budget.

Tip for First Home Buyers: Explore the Next Suburb Along

f your dream suburb is unaffordable, check nearby suburbs for more realistic options. Often, the next suburb along can offer:

- Similar amenities

- Lower median house prices

- Better value for first-home buyers

For example, if Paddington is out of reach, consider Herston or Fairfield:

Suburb | Postcode | Median Property Price (latest available) |

Paddington | 4064 | ~ $1,900,000 |

Herston | 4006 | ~ $1,515,000 |

Fairfield | 4103 | ~ $1,161,000 |

Red Hill | 4059 | ~ $1,800,000 |

Ashgrove | 4060 | ~ $1,700,000 |

Bardon | 4065 | ~ $1,720,000 |

Kelvin Grove | 4059 | ~ $1,260,000 |

Milton | 4064 | ~ $1,180,000 |

Spring Hill | 4000 | ~ $1,425,000 |

Using this method, you could find affordable suburbs like Kelvin Grove or Herston, giving you more buying power.

Expert Tip For Home Buyers: Median vs Mean House Prices

It’s important to understand the difference between median and mean house prices:

- Median house price: the middle point of all sold properties in a period (month, year, or decade).

- Mean house price: the average of all sold properties.

High-end sales, like $5–6 million homes in Paddington, can distort the median, making the suburb appear more expensive than most homes actually are. Use median house prices as a guide, not a strict rule.

Tools to Research Suburbs for First-Home Buyers

Several tools can help you find suburbs that match your budget:

- RealEstate.com.au & Domain: Check current listings and recent sales.

- CoreLogic Property Value: Offers insights including:

- Properties currently for sale in Brisbane

- Recently sold properties nearby

- Houses for rent

- Auction clearance rates

- Local schools & catchment areas

- Suburb demographics and neighbourhood info

- Market trends in Brisbane

We’ve also created an interactive map to simplify this research. Click here to access it now!

Stay Updated on the Market

For first-home buyers wanting regular property insights across Australia, subscribe to our weekly newsletter, Finance In Five, where we break down market trends, suburb analysis, and homebuying tips.

13. Ignoring Rental and Resale Value Of Your Home

Buying your first home isn’t just about living there—it’s also a long-term financial investment. Avoid the mistake of focusing solely on immediate needs and overlooking future value. Ignoring rental and resale potential can limit your options if you need to sell or rent later. While it is important to buy within your budget, you should also consider the value of your property.

Cotality data shows homes in high-growth suburbs can outperform the wider market by up to 20% over five years.

Rental yields in suburbs with strong schools or transport links are 1–2% higher on average than in more remote areas.

Why Rental and Resale Value Matter

Even if you plan to live in the property for years, its investment potential is important.

- Resale Potential: Homes in high-demand areas or with flexible layouts usually sell faster and at higher prices.

- Rental Income: Understanding rental potential can help cover mortgage repayments if your circumstances change.

- Market Flexibility: Properties near transport, schools, and amenities are easier to sell or rent in the future.

Key Factors to Consider

- Location: Proximity to public transport, schools, shops, and hospitals boosts rental demand and resale value.

- Property Type: 3+ bedrooms, modern kitchens, and updated bathrooms attract families and long-term tenants.

- Future Developments: Local council plans for infrastructure or zoning can significantly impact property value.

- Maintenance & Condition: Older homes may require costly repairs, which can reduce both rental yield and resale price.

Homebuying Tips for Value

- Think beyond your current lifestyle—consider what will make the property attractive to future buyers or renters.

- Compare potential resale prices with similar properties in the same area.

- Look for flexible spaces, like extra rooms or open-plan layouts, which appeal to a broader market.

By factoring in rental and resale value, first home buyers protect their investment and future-proof their property decisions.

14. Not Sticking To Your Budget

It sounds simple, but many first-home buyers lose control of their finances by ignoring a clear budget. Knowing your borrowing capacity and comfortable repayments is essential before you start house hunting.

Start by setting your initial budget — the amount you feel safe spending without straining your finances. Then define a “walk-away price”, which is the absolute maximum you’re willing to pay for a property. If the property exceeds this figure, you walk away.

Why First-Home Buyers Overspend

- Hot property markets create pressure to bid higher than planned.

- Emotional attachment to a property can cloud judgment.

- Real estate agents may subtly encourage buyers to stretch beyond comfort.

How to Stick to Your Budget

- Know your borrowing limit: Speak with a mortgage broker for an accurate figure.

- Calculate total costs: Include stamp duty, LMI, conveyancing, moving costs, and ongoing maintenance.

- Set clear limits: Separate “ideal price” from “walk-away price” before viewing any homes.

- Use suburbs strategically: Consider nearby, more affordable suburbs to stay within budget.

- Track spending emotionally: If a property excites you, pause and revisit your limits before bidding.

The Real Impact of Overspending

Even a small overspend can ripple through your finances. For example, adding $50,000 to an $800,000 loan at 6% interest over 30 years increases repayments by roughly $290 per month, or $104,000 over the life of the loan. Sticking to your budget protects your lifestyle and financial security.

Pro tip: Writing down your budget and walk-away price and sharing it with a trusted adviser or partner can keep you accountable.

15. Overpaying: Don’t Pay More Than a Property Is Worth

In a competitive property market, it’s easy to get caught up in the excitement and bid more than a home is actually worth. Real estate agents aim to get the highest price for their seller, and they can play buyers against each other. That’s normal—but it’s not your responsibility to overpay.

Common Ways First-Home Buyers Overpay

- Bidding Wars at Auctions – Auctions can push buyers into emotional bidding. Competing buyers might make you feel pressured to pay more than the property is actually worth.

- Ignoring Bank Valuations – Your lender will value the property before approving a loan. Overestimating a home’s worth without consulting the bank can create a shortfall, forcing you to cover extra costs from your own savings.

- Emotional Attachment – Falling in love with a property can cloud judgement. Buyers often ignore realistic pricing and overpay because “it feels like the one.”

- Overestimating Future Growth – First-home buyers sometimes assume a property will rise in value quickly. While growth can happen, paying more today based on potential future gains can backfire if the market stalls.

- Failing to Compare Recent Sales – Not checking recent sales in the suburb can lead to overpaying. Using old or irrelevant comparables inflates perceived value.

- Hidden Costs – Overpaying isn’t just the purchase price. Stamp duty, lender fees, insurance, maintenance, and renovations can all add thousands. Buyers who overlook these may stretch their budget too far.

- Upgrades or Renovation Hype – Some buyers pay extra for cosmetic improvements or potential renovation gains without proper cost analysis. Overestimating the value of upgrades can increase the purchase price beyond market value.

How to Protect Yourself From Overpaying

- Check the bank valuation: Lenders will assess the property and only lend up to its value.

- Set a “walk-away price”: Know the maximum you’re willing to pay and stick to it.

- Research comparable sales: Use recent data from similar properties in the area.

- Include finance conditions: Especially at auctions—without a finance clause, overpaying could cost thousands.

- Consult a mortgage broker: They provide realistic borrowing limits and help ensure you never pay more than a property is truly worth.

16. Smart Negotiation Strategies Most First-Home Buyers Don’t Use

Negotiation is where first-home buyers can save thousands, yet many skip this step. Knowing how to negotiate confidently can lower your mortgage repayments, reduce stress, and give you a stronger position in any market.

Even a small win, like $10,000 off the purchase price, can make a huge difference. Negotiation isn’t just about saving money—it’s about building leverage and protecting your investment.

Key Negotiation Tactics

- Spotting an Agent Bluff – Agents may pressure buyers with “other offers” or “price will rise tomorrow.” Watch for inconsistencies, and ask for evidence of competing bids.

- Requesting Key Information Before Making an Offer:

Always ask for:- Recent comparable sales (comps) in the suburb

- Property history and time on the market

- Building and pest reports (even preliminary ones)

- Adapting to Market Conditions:

- Slow Market: Low competition means you can negotiate price, settlement period, and inclusions.

- Hot Market: Focus on speed, flexibility, and attractive conditions instead of lowering price drastically.

- Using Building Reports as Leverage – Issues found in inspections—like minor structural or maintenance problems—can justify a discount or request for repairs before settlement.

- Presenting Yourself as the Best Buyer:

Strengthen your offer without increasing price:- Pre-approved loan or finance in place

- Flexible settlement dates

- Clear, professional communication

Example: Real Savings from Negotiation

Imagine you negotiate $10,000 off an $800,000 property. On a 30-year loan at 6% interest:

- Monthly repayment drops by ~$57

- Annual savings: ~$684

- Total savings over the life of the loan: ~$20,520

Homebuying Tips for Negotiation Success

- Research market trends and comparable sales. Knowledge equals power.

- Don’t reveal your maximum budget; keep your position flexible.

- Be polite but firm. Agents are more likely to work with confident, prepared buyers.

- Always have pre-approval ready—it shows you’re serious.

By mastering these negotiation strategies, first-home buyers can secure better deals, protect their investment, and avoid overpaying.

17. Overextending Yourself - My Story

Overextending means getting a loan bigger than what you can actually afford.

While the interest rates are low, you might be able to borrow much more than you could have done a few years ago when they were higher, but is this a wise thing to do?

The best way to answer this question is to tell you my story…

Waaaaayyy back in 2009 I was on my way to becoming a property mogul (in my own head). I had bought my second property, a small unit on Newton Street in Alexandria which I was planning on renovating and flipping for a massive profit—or so I thought…

It was around this time that the Reserve Bank of Australia (RBA) started increasing interest rates, and in the space of 6 months, my interest rate went from a barely manageable 6% to 7.50%.

This doesn’t seem like much, except for the fact that my monthly interest repayments went up from $3,500, which I could only just afford, to $4,375 per month—a jump of $875 per month! Finding that extra $875 was literally impossible and I was in deep deep mortgage stress.

I was earning around $70,000 at the time, and I had over $700,000 in debt! My debt to income ratio was way over 10 times which is WAY too high.

I used borrowed money and cash advance on my credit card to maintain my repayments. But ultimately, I had to sell my second property quickly to stop myself from getting into more and more debt. Not only did I make zero profit from this purchase but I risked losing my other property as well.

What I learnt: overextending is bad, and interest rates won’t always stay low.

Tip for first home buyers: How much to borrow

Fortunately, now the banks have dialled back how much they will lend to stop people from getting into the same mess I had found myself in. Always remember that Home loan repayments can change in the future.

So how much should I borrow?

As a general rule of thumb, 5 to 6 times or up to 30-40% of your income. For more details on this check out our First Home Buyers guide.

18. Changing Jobs During The Home Loan Application Process

Changing jobs during your home loan application is one of the easiest ways to delay or derail your approval. Most first home buyers don’t realise how closely lenders examine income history, job stability, and employment patterns. Even a positive career move can look risky to a bank if the timing is off.

Why Lenders Care About Job Stability

Banks want to see consistent income. They use this to calculate your borrowing capacity and assess whether you can manage repayments long-term. When you change jobs mid-application, lenders often pause everything until they can reassess your situation.

They may also request:

- A new employment contract

- Your first payslip

- A letter confirming your probation period

- Additional bank statements

- Updated servicing calculations

This slows the process and can affect your approval.

How Job Changes Can Impact First Home Buyers

Probation Issues

- Most new jobs come with a 3–6 month probation period.

- Many lenders prefer borrowers to have passed probation before approval.

- Some lenders accept applicants still in probation, but usually only if income is stable and the industry is consistent.

Industry or Role Changes

- Switching industries is seen as higher risk by lenders.

- Most lenders want 6–12 months of stable income in the new field.

- Moving from salaried work to contract or casual roles often triggers extra scrutiny.

Gaps in Employment

- Even short breaks between jobs can raise questions.

- Lenders may request explanations or extra documentation.

- This can slow down your approval and potentially delay settlement.

When a Job Change Might Be Okay

Some job moves are less risky:

- You move to a similar role within the same industry

- You receive a higher base salary (not just bonuses or commission)

- You stay on permanent full-time employment

- You avoid long gaps between jobs

These types of changes still require documentation, but they usually cause fewer issues.

High-Risk Job Moves During a Loan Application

These changes often trigger reassessments or declined applications:

- Switching to casual or contract work

- Relying heavily on commission or bonuses

- Changing industries completely

- Starting a new business

- Moving overseas or accepting remote work paid by an overseas employer

Banks often need a longer income history to rely on these income types.

Smart Homebuying Tips for Changing Jobs

- Delay job changes until after settlement if possible.

- Speak with your broker first if you must switch roles.

- Get employment letters early to speed up reassessment.

- Avoid probation during your application if you can.

- Plan ahead if your industry commonly uses contracts or fixed-term work.

What Hunter Galloway Does to Protect Your Application

We talk through your employment plans before you apply. This helps us match you with lenders who are flexible with probation, contract roles, or industry changes. If you must change jobs, we guide you through the documents needed so your application stays on track.

Bottom Line: Timing Your Job Move Matters

Changing jobs isn’t always bad — but timing is everything. For first home buyers, stability often matters more than salary. When you understand how lenders assess employment, you can avoid unnecessary delays and keep your home loan approval moving smoothly.

19. Getting The Wrong Loan Type

Choosing the wrong loan type is one of the biggest mistakes first home buyers make. Your loan structure affects your repayments, your flexibility, and how fast you build equity. Because of this, it’s worth slowing down and understanding the key loan options before signing anything.

1. Locking Into the Wrong Choice — Fixed vs Variable

Fixed Rate Loans

Fixed rates give you certainty. Your repayments stay the same for the entire fixed period. This helps with budgeting, especially if you’re new to home ownership.

However, fixed loans come with trade-offs. You often lose features like offset accounts. Break fees can also be huge if you refinance or sell early. Many first home buyers don’t realise fixed loans reduce flexibility when they need it most.

Variable Rate Loans

Variable loans give you more control. You can access features like offset accounts, redraw, and unlimited extra repayments. These features can save you thousands if you use them well.

But there is risk. Rates can move up or down. Even a 0.25% RBA increase adds pressure to your monthly budget. First home buyers with tight cashflow often underestimate these swings.

What Lenders See

Banks assess your borrowing power using a higher “buffer rate,” often 3% above your actual rate. This ensures you can afford repayments even during rate rises. Choosing the wrong rate type may limit or reduce your borrowing capacity.

2. Choosing Interest-Only When You Need Principal & Interest

Interest-only loans can seem attractive. They keep repayments low for a set period. Investors often use them to maximise cashflow.

But for first home buyers, interest-only structures often cost more in the long run. You delay paying down your balance. When the interest-only period ends, repayments jump sharply. Many buyers experience “repayment shock” because they didn’t plan ahead.

Principal and interest loans build equity from day one. They also come with lower interest rates compared to interest-only, which banks treat as higher-risk lending.

When Interest-Only Makes Sense

It can work for buyers with irregular income or buyers planning to convert the property into an investment later. But most first home buyers benefit from a principal-and-interest structure that reduces debt steadily and predictably.

3. Not Using an Offset Account to Reduce Interest

Offset accounts can be one of the most powerful tools for first home buyers. An offset account links to your variable loan and reduces the interest you pay. For example, keeping $10,000 in your offset reduces interest as if your loan balance was $10,000 lower.

Over a 30-year loan, even small balances can save thousands in interest. Yet many buyers choose loan types without offsets simply because they didn’t realise the long-term benefits.

Key Offset Benefits

- Reduces interest without locking your savings away

- Gives flexibility for emergencies or future purchases

- Helps cut years off your loan if used consistently

Many fixed-rate loans don’t allow full offset. This is why pairing your rate choice with your spending habits is essential.

Bottom Line: Loan Structure Shapes Your Homeownership Journey

The right loan type should match your goals, your income, and your financial habits. First home buyers often focus on interest rates alone. But structure matters just as much.

At Hunter Galloway, we help you compare the long-term costs and benefits of each loan type. That way, you avoid costly mistakes and start your homeownership journey with a loan structure that truly works for you.

20. Getting Your Home Loan Declined

Having your home loan rejected is far more common today than many first-home buyers realise. Lending standards are tighter, banks are more cautious, and even small issues can trigger a decline. The good news is that declines are usually avoidable once you understand what lenders look for.

Banks assess every application using the Five Cs of Credit. It’s the foundation of how they judge your risk as a borrower.

The Five Cs of Credit

Character – This is your financial reputation. Banks review your credit report, repayment history, defaults, late payments and the number of credit enquiries.

Capacity – This measures your ability to repay the loan based on your income, living expenses, debts and employment stability. Even strong incomes can be declined if job patterns look unstable.

Capital – This is your deposit. A larger deposit lowers the lender’s risk and strengthens your application. Smaller deposits mean tighter scrutiny and fewer lender options.

Collateral – This is the property you’re buying. Some properties are considered high-risk, such as very small units, unusual builds, rural homes or properties in declining areas. Even if you’re a strong borrower, a high-risk property can cause a decline.

Conditions – These are the loan details: loan amount, loan term, interest rate type, repayment structure and loan purpose. Some loan conditions increase lender risk and can lead to a decline.

Why Loans Get Declined Today

Banks now have:

- Stricter responsible-lending rules

- Higher scrutiny of living expenses

- More detailed income verification

- Stronger focus on job stability

- Tighter credit policies in uncertain markets

Even good borrowers can be declined if their application doesn’t fit current rules.

Home Buyer Tips If Your Loan Gets Declined

Check Your Credit File

At Hunter Galloway we can run a free credit file check for clients. This confirms active and closed accounts, missed repayments, defaults and incorrect listings. Fixing errors can significantly boost your chances on your next application.

Double-Check Your Credit Card Limits

Lenders assess credit limits, not balances. Even an unused $20,000 card can reduce your borrowing power by tens of thousands. Tools like BankStatements help confirm accurate limits for your application.

Clean Up Your Bank Accounts

Lenders assess 3–6 months of bank statements. Strengthen your profile by:

- Consolidating multiple accounts

- Avoiding overdrawn balances

- Reducing discretionary spending

- Closing unused credit cards

- Avoiding buy-now-pay-later services

- Keeping your transactions clean and predictable

These simple habits can turn a decline into an approval on your next attempt.

21. Walking Away From A Bad Bank Valuation

A bad bank valuation happens when the bank values the property for less than what you’ve agreed to pay.

For example, if you’re buying a home for $800,000 but the bank values it at $760,000, the bank will only lend based on the $760,000 value.

This means you must cover the $40,000 shortfall from your own savings, on top of your deposit and purchasing costs.

Why Bad Valuations Happen

Bank valuations don’t care about what the market feels, what the agent says, or how much competition there was at the open home.

They’re purely about risk.

Banks want to know:

- If we had to repossess this property, how long would it take to sell?

- Could we recover our money within 3–6 months?

If the bank thinks the property might take longer to sell or has a limited buyer pool, they may value it lower.

This commonly happens with:

- Apartments under 50m²

- Properties in oversupplied suburbs

- Homes with unusual layouts

- Prestige properties with a limited number of potential buyers

- Unique homes (heritage, heavily renovated, very old, unusual design)

If the bank considers the property harder to resell quickly, the valuation will drop to reflect that risk.

Example: Why Smaller Properties Get Hit

If you’re buying a 45m² apartment, the bank knows the buyer pool is mostly single individuals or investors.

Fewer buyers = higher risk = lower valuation. The same applies to units with no parking, properties in declining areas, or homes with structural issues.

The Real Problem With Low Valuations

A low valuation can instantly put your purchase at risk:

- Your loan amount may no longer meet the bank’s requirements

- Your deposit may no longer be enough

- Your LVR may rise, pushing you into higher mortgage insurance

- If you bought at auction, you could lose your deposit

This is one of the fastest ways first-home buyers lose thousands of dollars.

How to Fix a Bad Bank Valuation

You don’t always have to walk away from a bad valuation. There are three proven solutions to fix that problem.

1. Challenge the Valuation

Your broker can request a valuation review by supplying:

- Stronger comparable sales

- More recent sales

- Sales the valuer overlooked

- Evidence of upgrades or improvements

Sometimes this is enough to get the valuation increased.

2. Order a Second Valuation

Different banks use different valuation firms.

We regularly see huge differences between banks—sometimes over $130,000 on the same property.

If the valuation is too low, your broker can:

- Order a new valuation with a different lender

- Compare results

- Proceed with the lender that gives a better valuation

This alone can save your contract.

3. Renegotiate the Purchase Price

If the market is cooling or the seller is motivated, you may be able to negotiate the price back down to match the valuation.

This is most successful when:

- The property has been on the market for a long time

- There were no other strong buyers

- The seller needs a quick sale

The valuation came in significantly lower

Need Help With a Low Bank Valuation?

We handle valuation issues every week and know exactly how to fight them. Get in touch with our brokers and we’ll help you navigate your options.

22. Underestimating The Costs Of Buying A House In Brisbane

Buying a home isn’t cheap. The cost of the home itself is expensive enough. And on top of that, there are a lot of hidden fees which you need to pay for.

You may have heard that you can buy a home with as little as 5% deposit. And that’s true, You can get a home loan with a 95% LVR (Loan-to-Value-Ratio), which means that you give the bank a 5% deposit on the home loan.

But , you also need money for additional costs like:

- Lenders Mortgage Insurance.

- Costs of Borrowing (Home Loans).

- Government Fees in Brisbane.

- Stamp Duty in Brisbane.

- Council & Water Rates.

- Strata (Body corporate) Fees.

- Home & Contents Insurance.

- Legal Costs (Solicitor/Conveyancer Fees).

- Building & Pest Reports.

- Moving + Connection Costs.

- Home Loan Deposit need in Brisbane.

- BONUS TIP: Changes to monthly repayments.

Here is an example of the costs when buying a home in Brisbane for over $500,000.

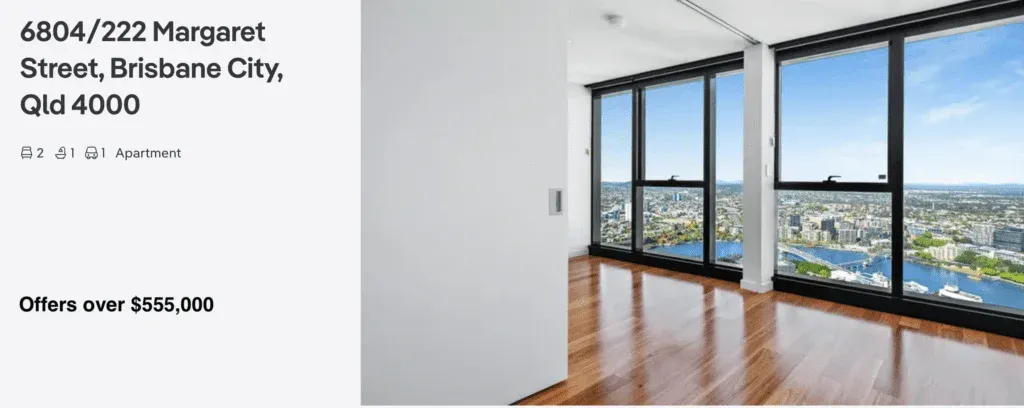

First Home Buyer Case Study: Simon

Meet Simon…

Simon isn’t a first home buyer, so he only gets a partial stamp duty concession on his home purchase and finds the perfect unit on Margaret Street in Brisbane for $555,000. He has around $75,000 in savings, so a little bit over 10%.

Simon wants to capitalise or add the Lenders Mortgage Insurance to the loan amount so he doesn’t need to pay this up front. Here is a calculation of his costs.

Property | New Home in Brisbane |

Purchase Price | $555,000 |

Loan Amount | $499,500 |

Lenders Mortgage Insurance | $9,080 |

Total Loan Amount | $508,580 |

Purchase Stamp Duty | $10,825 |

Transfer Fees | $1,517 |

Registration Fees | $187 |

Discharge of mortgage fee | $187 |

Costs of Borrowing | $400 |

$1,500 | |

Discharge Costs (if applicable) | $300 |

Other/Sundries: Contents Insurance Strata & Body Corporate Fees Building & Pest Reports Moving + Connection Costs | $2,000 |

Total Costs | $16,729 |

The total deposit amount required is the total costs, plus his 10% deposit

Total Costs | $16,729 |

10% home loan deposit | $55,500 |

Total Amount Required | $72,229 |

In this example, while Simon paid a 10% deposit or $55,500 once you factor in the stamp duty and other costs his deposit is actually closer to 12-13% meaning you need your bank deposit + around 3%. So if you are paying a 5% bank deposit, with stamp duty and other costs you will need closer to a minimum of 8%.

Solution:

There are so many hidden costs when buying a home. As a first home buyer it can be so hard to keep up, but what I’d recommend you do is read through the article here which outlines all 16 hidden costs you’ll likely face as a new homebuyer. For a comprehensive guide on the true cost of buying your first home, then see the video below as well as our guide here.

23. Trying To Time The Market

When it comes to buying your first home, everyone has an opinion—your parents, friends, workmates, and every commentator on TV or social media. But having an opinion doesn’t make anyone right.

The truth is simple: no one can accurately predict the market. Not the media, not the experts, and not even the banks.

It’s not about timing the market

It’s about time in the market.

Property moves in cycles—sometimes favouring buyers, sometimes favouring sellers. But knowing when those shifts will happen is impossible. Waiting for the “perfect time” or hoping prices will suddenly fall is just gambling with your future.

Instead of stressing about headlines saying the market is BOOMING or that a CRASH is coming, focus on your long-term goals. Property is a long game, and short-term noise shouldn’t derail your plans.

What the long-term data shows

ABS data from Brisbane house prices since 1986 shows something very important: Short-term dips happen, but long-term growth dominates.

Even during flat or falling periods, the 30-year trend is consistently upward.

If you want market updates, Herron Todd White’s Monthly Property Review is one of the clearest sources. Their Brisbane Property Clock shows where the market sits in the cycle—from Peak to Bottom and everything in between.

Right now, Brisbane is starting to decline, but again—your long-term strategy is what matters most.

But don’t ignore the market completely

You can’t time the market, but you still need to understand it.

Market conditions affect your negotiation strategy:

- Hot market? Be ready to move fast and put your strongest offer forward early.

- Slow market? You can take your time, negotiate harder, and even start with a low offer to test the waters.

And remember, conditions aren’t uniform. Brisbane might be booming overall, while a specific suburb is cooling—or the other way around. This is why suburb-level research is essential.

Key Tip For Homebuyers

Don’t let fear or media headlines stop you from moving forward. Focus on your long-term goals, know your budget, understand your chosen suburb, and buy when you are ready—not when the market tries to tell you.

Would you like to learn about your situation?

24. Getting Desperate Or Fed Up

I know exactly how it feels—I’ve been there myself.

When my (now) wife and I moved back to Brisbane from Sydney, we were desperate to buy. I had spent months researching properties from afar, but once we arrived, the pressure hit hard. We were staying with my in-laws, and suddenly it felt like there was a gun to my head to buy anything.

Honestly, if someone had offered me a tin shed behind a rubbish tip, I probably would’ve taken it. I was at full panic stations.

Back then, the market was nothing like it is today. At least properties stayed on the market long enough to think things through.

In the current market, homes sell within days—or even hours. It’s frustrating watching property after property disappear before you’ve even booked an inspection. It’s even worse when you get outbid by someone offering just a tiny bit more.

There’s only so much disappointment you can take before frustration turns into desperation.

And once you’re desperate, you become vulnerable to making rushed, emotionally driven decisions.

Don’t buy out of frustration

Missing out on a few homes can make you feel like “anything is better than nothing.” But that mindset is dangerous.

Buying a property in Brisbane isn’t cheap. You’re spending hundreds of thousands of dollars on something you’ll likely live in for 5–10 years. This is not the time to settle for a home that doesn’t genuinely meet your needs.

A rushed purchase often leads to buyer’s remorse—and expensive mistakes.

First home buyer tip: Consider a buyer’s agent

If you’re feeling burnt out, take a short break from house hunting.

Even better, consider working with a buyer’s agent.

A good buyer’s agent can:

- Source suitable properties before they hit the public market

- Handle inspections and shortlists

- Assess property values correctly

- Negotiate on your behalf

- Bid for you at auction

- Save you weeks of stress and running around

In Brisbane, buyer’s agents typically charge either a flat fee or a percentage of the purchase price. While it’s an upfront cost, they can save you time, money, stress—and help prevent rushed, regretful decisions.

25. Hesitating Too Much

Things move incredibly fast in a hot property market. If you hesitate for even a moment, someone else can swoop in and take the property right out of your hands.

At this point, you might be thinking, “Hang on… didn’t you just tell me not to be impulsive?”

Yes—absolutely.

But acting impulsively and acting decisively are two very different things.

Acting decisively is being prepared

Acting without hesitation means you’ve already done the work before you walk into an open home. You know:

- exactly what suburbs you want

- what features you need (and which ones are deal-breakers)

- how much you can afford

- your absolute walk-away price

- that you have a current pre-approval in place. Once you have all of that locked in, you’re not making an impulsive emotional decision—you’re simply recognising the right property and moving fast.

Acting impulsively is buying from emotion

This happens when you’re tired, frustrated, or scared of missing out. You see something “good enough,” panic sets in, and you rush an offer before fully thinking it through.

That’s not strategic—that’s emotional.

Success comes from clarity

When you’re clear on what you want, and you’ve done your homework, you can make confident decisions quickly. And in Brisbane’s market, speed matters.

Not ready yet? We can help.

If you’re unsure about your criteria or what you should be looking for, we’ve created a Buyer Brief Worksheet that helps you map out exactly what you want. This document gives you clarity, confidence, and the ability to act fast—without the risk of buying the wrong home.

26. Not Having the Right Clauses in Your Contract of Sale

The good news for Brisbane buyers is that we use a standardised Contract of Sale, which normally includes essential protections like a finance clause and a building & pest clause. These can give you time to secure approval, complete inspections, and walk away if something major is uncovered.

But here’s the catch:

These standard clauses don’t cover everything—and they don’t automatically protect your individual circumstances.

That’s why adding the right additional clauses is crucial.

Why clauses matter

Once you sign a contract, you’re legally bound.

If something changes—your finance hits a snag, the property has hidden issues, or you need more time—you can’t simply “fix it later.”

Despite what a selling agent might tell you:

Never sign first and ask for changes later.

Once the contract is signed, the terms are locked in. The seller has no obligation to allow amendments.

Even something as simple as changing the purchaser’s name requires a brand-new contract—which opens the door for the seller to renegotiate the price or refuse altogether.

What you should do

Before signing anything, ensure your solicitor or conveyancer has reviewed the contract and confirmed that:

- your finance and building/pest clauses are correctly worded

- any specific conditions you need are included (e.g., subject to sale, extended settlement, repairs, inclusions)

- no clauses have been altered or removed by the seller

- the timelines are realistic and achievable for your lender

- your interests—not the seller’s—are being protected

Key tip for home buyers

Never sign a Contract of Sale until you are 100% certain it protects you.

Getting this wrong can cost you your deposit—or force you into buying a property with major financial risks.

If you’re unsure which clauses you need, we can help guide you and connect you with trusted Brisbane conveyancers who specialise in first home buyers.

27. Not Taking Out Property Insurance

If there’s one thing you remember from this entire guide, let it be this: insurance.

The home-buying process might feel like it ends when you sign the contract—but the reality is, once the contract is signed, the property is technically your responsibility. This means any damage to the property before settlement can become your financial liability.

Why insurance matters

After the purchase price is agreed, you wait through the settlement period—often up to 30 days—before getting the keys.

Many first home buyers don’t realise that during this time, they are responsible for protecting the property. Without insurance, any fire, flood, or accidental damage could leave you out of pocket.

How home insurance rules differ by state and territory

- Queensland: Responsibility begins from 5pm the next business day after contracts are signed and exchanged.

- Victoria & New South Wales: Buyer is responsible for any damage from the settlement date.

- ACT, Tasmania & South Australia: Buyer must insure the property during the settlement period.

- Western Australia & Northern Territory: Buyer is responsible either on the date they gain possession or when the full purchase price is paid, whichever happens first.

First home buyer tip: Know when to insure

Rules vary across Australia, so it’s important to confirm exactly when you need coverage. In some cases, it’s even recommended to insure before settlement to avoid exposure to unexpected damage.

At the very least, in Queensland, insurance from the moment the contract is signed is a must. Don’t risk a nightmare situation—damage during settlement can be costly and preventable.

28. Being Too Cheap and Cutting Corners

At the risk of sounding like a broken record: property in Brisbane is expensive—really expensive. Cutting corners to save money can end up costing you far more in the long run. This is especially true for Building & Pest Reports.

Why skimping on reports is risky

I can say without hesitation that on five separate occasions, Building & Pest reports have saved me from buying properties that were essentially money pits.

One year, I spent over $2,000 on Building & Pest Reports. At the time, it felt like a huge expense—but it ended up saving me from a property that would have cost over $9,000 in repairs if I had gone ahead.

The lesson? Paying a little upfront can save you thousands later.

Choosing the right inspector

- Do your research: Check Google reviews or ask friends for recommendations.

- Avoid the seller’s recommendation: You want an independent, certified inspector to maintain objectivity.

First home buyer tip: Use a certified Building & Pest Inspector

Even minor issues found in the report can be used as leverage to negotiate discounts with the seller.

Don’t forget free reports

Some critical reports won’t cost you a cent:

- Flood Report: Shows your property’s flood risk. Use a guide like our FloodWise tutorial to interpret the results.

- Brisbane Town Planning Report: Reveals any active or pending development applications that could affect your property.

Knowledge is power. Understanding zoning, flood risk, and structural issues can give you a significant advantage in negotiations and help you avoid costly mistakes.

29. Not Shopping Around (and Skipping Property Inspections)

Finding your first property can feel like meeting your first love—pure electricity, excitement, and daydreams about your future life there.

You imagine wandering down the long hallways, sleeping in the majestic bedroom, or lounging in the cozy TV room… but don’t let emotions cloud your judgment.

Why taking your time matters

It’s easy to fall in love with a property at first sight, but rushing into a decision could be financially disastrous. Properties can have hidden issues behind beautiful facades—structural problems, water damage, or outdated wiring could all cost you thousands down the line.

Practical steps to avoid mistakes

- Shop around: Compare several properties before committing. What seems perfect at first might not offer the best value.

- Take inspections seriously: Don’t skip professional inspections, including Building & Pest reports. They’re critical in uncovering hidden problems.

- Use a property checklist: Bring a comprehensive checklist on your first inspection to note small issues, potential repairs, and negotiation opportunities.

Remember: this is a major financial decision. Taking a step back, evaluating all options, and inspecting carefully can save you from costly mistakes while still helping you find a home you love.

30. Not Realising Auctions Are Completely Different

If you’re planning to buy your dream home at an auction, you need to understand that this process is completely different from a standard private sale.

Auctions are final. There’s no finance clause, no “get out of jail free” card. Once the hammer falls and you’re the highest bidder, the property is yours. This means:

- Building and pest inspections must be complete before the auction.

- Finance must be secured beforehand—no exceptions.

A personal tip: I applied for three different homes before I found mine, and each had issues in the building and pest report. Because of these issues, I didn’t go ahead. Don’t underestimate how important these reports are—they can make or break a deal.

Auctions vs Private Treaty

- Private treaty: You can include clauses allowing you to back out if your finance isn’t approved or inspections reveal issues.

- Auction: If the reserve price is met and you win, you’re legally obliged to purchase the property—no way out.

How to prepare for auctions

- Attend a few auctions first to understand the pace and process.

- Get pre-approval for your loan.

- Finalise building and pest inspections.

- Research the property thoroughly before bidding.

For more guidance, check these resources:

- 12 Rules for Buying at Auction

- 11 Point Auction Bidding Checklist

- Understanding the Auction Market

- Buying at Auction

Key takeaway: At an auction, preparation is everything. The right research and pre-approval can make the difference between winning your dream home and walking away empty-handed.

Bonus: First-Home Buyer Tips To Build “Bank-Ready” Financial Profiles

Buying your first home is exciting, but lenders scrutinize every detail of your financial life. A “bank-ready” profile increases your chances of approval and can even secure better interest rates.

What a “Bank-Ready” Profile Looks Like

Lenders want to see consistency, reliability, and responsible money habits. Key indicators include:

- Credit Behaviour: On-time payments, low credit card balances, minimal new debt.

- Stable Income Patterns: Regular, consistent earnings—even casual or contract workers can demonstrate stability.

- Spending Habits: Controlled discretionary spending, regular savings, and predictable outgoings.

How to Quickly Clean Up Your Bank Statements (3-Month Action Plan)

Even small improvements can make a difference in how lenders view your finances.

- Month 1: Track every transaction and identify avoidable fees or discretionary spending.

- Month 2: Reduce high-interest debts and consolidate where possible.

- Month 3: Maintain a clear, positive balance; avoid large, unexplained deposits or withdrawals.

What Lenders Look for in Rental History & Living Expenses

Lenders use your rental history and living costs to gauge reliability and risk:

- On-Time Rent Payments: Demonstrates you can meet regular obligations.

- Consistent Living Expenses: Avoid erratic transactions or unexplained large withdrawals.

- Low Debt-to-Income Ratio: Shows you can comfortably afford repayments on top of current expenses.

Smart Ways to Show Financial Reliability as a Casual/Contract Worker

Even without full-time employment, you can present yourself as a strong candidate:

- Keep at least 6–12 months of income statements.

- Show continuous work within your industry, even if freelance or short-term.

- Maintain a buffer in your savings account—demonstrates capacity to handle unexpected costs.

- Consider an offset account or partial savings to show financial responsibility.

Pro Tip: Lenders like to see proactive financial management. Small steps—like consistent savings and responsible spending—can significantly improve your approval odds.

Buying Your First Home: FAQs

What are the criteria for a first home buyer in Australia?

First home buyers must be Australian residents, at least 18, and have never owned property. State grants or schemes may add extra requirements.

What are red flags when buying a house?

Watch for structural damage, pest issues, council notices, high fees, or declining suburb trends. These can affect resale and value.

Should I buy a house or an apartment?

Houses offer space, growth potential, and flexibility. Apartments suit lower budgets, city living, and low maintenance. Consider lifestyle and future goals.

What is Lenders Mortgage Insurance (LMI)?

LMI protects lenders if low-deposit buyers default. Usually required for deposits under 20%, with cost depending on loan size and lender.

What's the first step in the buying process?

Assess finances, check your credit score, and get pre-approval. This sets a budget and shows you’re serious to sellers.

How much deposit do first-home buyers really need in Australia?

Most lenders prefer 20%, but first home buyers can enter with 5–10% using LMI, the First Home Guarantee, or low-deposit lender policies.

Is it possible to buy a home on casual or contract income?

Yes. Lenders check consistent income over 6–12 months, low debts, and strong savings. Some specialise in non-traditional employment types.

Should first-home buyers use a buyer’s agent?

Not essential, but buyer’s agents help with negotiation, property evaluation, and avoiding mistakes. They’re ideal for limited time or knowledge.

Next Steps And Getting Your Home Loan

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one person operations, we have an entire team of experts dedicated to help make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.