So you’ve just signed your contract and secured pre-approved funds, but a low bank valuation is threatening to derail your purchase. This common issue affects many homebuyers, so before you panic, understand that there are clear, actionable steps you can take. This article will not only explain how to resolve a low valuation but also show you how to avoid one in the first place by understanding the factors that influence a bank’s assessment.

What Is A Valuation?

A property valuation is an assessment of the value of a property. Valuations typically consider several factors, including the condition of the property, comparable sales in the local area, and the state of the property market.

Typically, a valuer will look at:

- Size of the property

- Number and type of rooms

- Fixtures and fittings

- Areas for improvement

- Location

- Building structure and condition (including faults)

- Standard of presentation and fit-out

- Ease of access, such as good vehicle access and a garage

- Planning and restrictions and local council zoning

- Recent sales in the area and other market conditions

Why Do I Need A Property Valuation?

1. Applying for a home loan

There are 3 main reasons that you would need a property valuation:

When you want to buy a new property or refinance your home loan, the banks will want to do a valuation. They do this to ensure that they aren’t lending you more money than the property is worth.

The property acts as a security against the money that the bank lends you. If you are no longer able to make your repayments and they need to repossess your home, they may need to sell your home quickly to recover their money. If they lend you too much money compared to the property’s value (known as the Loan to Value Ratio), they will not be able to cover their losses.

2. Buying or selling property

If you’re buying or selling a property, a valuation can help you get an idea of what the property may be worth. If you’re buying, it will help you position your offer so you’re not over- or under-bidding on the property. If you’re selling, it will help you price your property competitively compared to other similar properties for sale in your area.

3. Understanding the equity you have in your home.

Equity is simply your personal interest in a property. It increases over time as you pay down your home loan or when your property value increases. It is important to know how much equity you have as it forms part of your net worth. A property valuation can help you know how much equity you have. You can also withdraw part or all of your equity in the future to do renovations or buy an investment property.

Methods To Determine Property Value

So what are the things that you need to do when trying to determine how much your property is worth? Here are some methods that you can use to get a property value in today’s market.

1. Using the 'Sold' section for property valuation

The first and best way of doing it is just looking at the sold section on real estate websites like realestate.com.au and domain.com.au. It’s as simple as going on the website, clicking your suburb and updating the filters to match your property. If you’ve got a 2 bedroom apartment, click 2 bedrooms, 2 car space: you can even put the internal square meterage Etc. You can then go through the properties to see how much similar properties to yours have sold.

Remember to compare with the most recent sales. If you compare it to sales from 3 or 4 years ago, it won’t be right. But if you are looking at sales from a few months ago, you can be pretty confident with your estimate.

So, looking at sold price is a quick and easy way to value your property, and you don’t even need anyone to help you.

2. Automated valuations and their pitfalls

The second way is to look at automated valuations, which are basically computer-generated valuations. You can use a couple of online tools like On The House. We also have access to RP Data and CoreLogic, so if you need help with that, contact us, and we can help you.

Now the big Pitfall with these is that they are automated. They’re called Automated Valuation Models (AVMs) and are not always accurate. In fact, we suggest using it as a guide at best, as they will give you a large deviation. For example, it may say your apartment is worth between $500,000 and $800,000, which is a pretty big gap.

AVMs also don’t factor in the property’s condition, how old it is, if it’s a brand new building or an old one, the area it’s in and if it’s close to a train line or main road. All this is stuff that really does make a difference with the sale value.

So the key in using RP data is to take them with a grain of salt because, a lot of times, they are not the most accurate.

3. Asking a real estate agent

The 3rd method is asking a real estate agent. Real estate agents can be pretty overly optimistic, so if you go out and ask a real estate agent to appraise your house, very rarely are they going to tell you it’s worth less because you’re probably not going to want to sell with that agent if they’re going to get you fifty thousand dollars less than the bank valuation…

However, the positive thing with getting a real estate agent to appraise your property is that they can factor in the current market conditions, which the bank valuation and even the online sales won’t do. If the agent is saying well, we’ve found that the property market is going up 2 to 3 per cent a month, they might factor that in and say the previous sales are saying $550,000, but we think we can get you $570,000 to $600,00. That could be a fair estimate but don’t go in there with your rosy-coloured lenses— you need to realize agents can be really optimistic.

4. Bank Valuations

A bank valuation is performed by an independent valuer on behalf of the bank. They use the figure provided by the valuer to calculate the Loan to Value Ratio (LVR). LVR is an important aspect of the banks’ assessment of your home loan. The higher the LVR, the higher the risk. If your LVR is over 80%, they will typically require you to purchase Lenders Mortgage Insurance (LMI) to protect them if you default on your loan repayments. However, there are some cases where they will waive the LMI requirement up to 90% of the property value.

Bank valuations are typically more on the conservative side of things and look at the home’s value over a longer-term because they are looking to protect their money.

Now the caveat here is different banks have different ways of valuing properties. You may have seen online some of the bigger banks, like CBA and NAB, have their own automated valuation models, which can be massively optimistic. They can be hundreds of thousands of dollars or more than what the property is potentially worth in the current market because it’s using such a big data set.

In other cases, they can be completely wrong. We’ve had some situations where people have built a nice 4-bedroom brand-new home, and because the bank’s model thinks it’s still a block of land, the valuation is completely wrong.

The Different Types Of Bank Valuations

There are several different types of bank valuations. The bank or lender will typically choose a more comprehensive valuation method if there is a higher perceived risk to the bank. Here are the different types of bank valuations:

Full valuation

Full valuations are the most comprehensive method. During a full valuation, the valuer will inspect the property inside and out and write up a bank report. They will include photos, property details, and the reasoning behind their assessment.

Kerbside valuation

A kerbside valuation involves a physical inspection of the property, but only from the outside. They will take into account recent sales and the external condition of the property, but not any special internal features such as recent renovations.

Desktop valuation

Desktop valuations are still performed by humans, but they don’t involve any physical inspection of the property. The valuer will look at the known property details and comparable sales data to assess the property value.

Automated valuation (AVM)

An automated valuation is the least comprehensive method. Like a desktop valuation, an AVM uses the known property details and comparable sales. However, it uses a statistical computer valuation rather than a professional valuer to estimate the value.

How Long Does It Take To Value A Property?

The typical turnaround time for a property valuation is three to four working days. Delays can occur if there are issues with the sellers’ agent giving the valuer access to the property or during busy times when valuers can be booked out several days in advance.

Check to see if you are eligible for a home loan

When Should I Get A Bank Valuation?

The best time to get a bank valuation is after you have agreed on a final purchase price (either by private treaty sale or auction) but before submitting your application to the bank.

Why should I do a valuation before applying for a loan?

Doing your valuation before applying for your loan has several advantages:

- It protects your credit score: Every loan application leaves an enquiry on your credit file. If you have too many enquiries in a short period of time, it can affect your credit score and make it harder for you to get your loan approved.

- It will improve your chances of your loan being approved: if the bank’s valuer gives you a low valuation, it could mean that your loan would be rejected. If we do an upfront valuation, we try your application with a different bank or lender.

- Your loan application will be approved faster: An upfront valuation can speed up the approval process since we won’t need to wait for the bank to arrange a valuation.

Why should I wait until I have a final purchase price?

The purchase price of your home gives the valuer an anchoring point. They can compare your purchase price against their assessment of the home’s value, and more often than not, they will value the home at the same price as you paid for it.

If you order the valuation before you have agreed on a final purchase price, the valuer may be more conservative in their estimation. This could cause you issues if your purchase price is higher than the valuer’s estimate.

What can I do to estimate the value before agreeing on a final purchase price?

There are a few options for estimating the value of a property that don’t involve using a bank valuer. We covered them above. You can also use a buyers’ agent to assist you with purchasing the property. Alternatively, you can use comparable sales and some other tools to value the property’s market value yourself.

Can I Provide My Own Valuation To The Bank?

The short answer is no. Most banks require that the valuation is ordered through them to prevent fraud or other issues. They will typically use an independent valuer (someone not employed directly by the bank) to provide an unbiased estimate of how much the property is worth.

How To Avoid A Low Bank Valuation When Buying A Home

The best way to deal with a low bank valuation is to avoid getting one to begin with. This may be a bit late if you’ve already received a low valuation, but if you’re not at that stage yet, then here’s what you can do to avoid it.

Do your own value estimation before agreeing on a purchase price.

Researching the market value of your property is a critical part of the home buying process. If you don’t know what the property is worth, you’re basically pulling a number out of thin air. And that’s a recipe for disaster – if you’ve paid well above the fair market value for your home, there’s not much you can do to challenge the valuation.

We can assist you by providing an RP Data report which gives an automated estimate of the value of your property. Combined with your research looking at recent sales on Domain and realestate.com.au, this should give you a fairly accurate picture of what the property is worth.

Be careful when buying an off-the-plan apartment.

If you’re buying an off-the-plan apartment, it’s a good idea to remember that the lender can only value the finished property. Completion may be well over a year after signing the contract and placing a deposit.

There is a risk that property values in the area may change over the construction period. The bank valuation may be lower than your purchase price if they do.

There is also a risk that the dimensions of the finished apartment may vary from the plans. This situation may result in a bank valuation that’s less than the purchase price.

Unregistered land can also be risky.

A similar situation may occur in new estates when developers offer unregistered land for sale. The developer may need several years to build the infrastructure necessary to register the land.

In this case, the lender will need to reassess your application before settlement. Over the time since you paid your deposit, values in the area may have changed, resulting in a valuation lower than your purchase price.

What To Do If The House Valuation Is Less Than Your Offer

If you have received a bank valuation that is less than the offer you have submitted (or bid at auction), the first thing to do is: don’t panic.

This is known as a valuation shortfall, and it’s not uncommon. There is no hard and fast rule on bank valuations. A valuation is the opinion of a single individual at a certain point in time. It’s quite common to have three different people value the same property at the same time, in the same market, and have three different valuations.

You could receive a valuation shortfall if:

- The valuer is relying on outdated comparable sales data.

- The market is rising quickly, and the valuer has failed to factor this in

- The lender used a less comprehensive valuation method, which doesn’t consider the property’s full value.

You have several options to resolve this issue. If you’re applying directly with a bank, you can attempt to do this yourself. Still, we recommend using the services of a mortgage broker to assist.

Here at Hunter Galloway, we have assisted hundreds of people with valuation issues. We can usually get a good outcome thanks to our relationships with different lenders.

Generally speaking, here are your options to resolve a valuation shortfall (and this is how we do it here at Hunter Galloway):

1. Find out the reason for the low valuation

The most common reason for a low valuation is that the valuer did not find enough supporting evidence for comparable sales of similar properties. The less supporting evidence they have, the more conservative they tend to be with their estimates.

2. Challenge the valuation

Valuers can make mistakes, and sometimes you can challenge the property valuer directly. This approach is often unsuccessful because, as with everyone, valuers do not like to be told that they are wrong. It’s estimated that only 3% of clients are able to challenge a valuation successfully.

If you choose to contest the valuation, you’ll need to give at least three recent sales in the local area of homes with comparable quality to the valued property. These sales should generally be within the past six months to ensure their validity, but the more recent, the better.

3. Get valuations from other banks

Different banks will use different valuers for their valuation process. So if you can’t get your original bank or lender to increase their valuation, you can request a valuation from another bank. We can order up to another two valuations from other lenders to see if their valuation is more in line with your purchase price.

4. Negotiate with the seller

If you have submitted an offer under private treaty with a finance clause, you may be able to negotiate with the seller for a lower price.

For example, recently, one of our clients bought a one-bedroom unit in Brisbane, and they paid $350,000, which seemed like a good deal for one bedroom. We went and got three separate valuations— one came in at $315,000, one came in at $320,000, and the third one came in at $320,000. So that’s over $30,000 less than it was under contract.

Fortunately, the property was still subject to finance, so the buyer could go back to the selling agent and ask them to reduce the purchase price to $320,000.

This option is highly dependent on the market conditions. If the seller has other offers on the table at a price higher than the bank valuation, then they will not accept a price reduction.

If that happens, you can either walk away (if you have a finance clause) or accept that you will need to put in a higher deposit or borrow more money to complete the property purchase.

If you’ve bought at auction, you’ll need to find the money to complete the shortfall or risk losing your deposit.

What Happens If You Can’t Resolve The Valuation Shortfall?

So what do you do if you can’t find a lender who is willing to value your property at its purchase price?

You have a few options, depending on the LVR of the loan based on the bank’s valuation of the property.

If the new LVR is still below 80%, you can proceed with the loan.

If you have a sizeable deposit for the property (more than 20%) and the new, lower value doesn’t take you over that 80% level, then there aren’t any issues with getting your loan approved.

Let’s look at an example:

| Offer/Value | Deposit | Loan Amount | LVR | |

|---|---|---|---|---|

| Your Offer | $500,000 | $150,000 | $350,000 | 70% |

| Bank Value | $450,000 | $150,000 | $350,000 | 78% |

In this scenario, you have put in an offer for $500,000. You have a deposit of $150,000 and you would like a loan of $350,000, giving you an LVR of 70%. The bank valuation comes in at $450,000, giving you a new LVR of 78%. As this doesn’t take your loan above 80%, you will have no issues with getting your loan approved.

If you have a 20% deposit for the property and the new, lower value takes your LVR over 80%, then you may need to pay Lenders’ Mortgage Insurance if you can’t source extra funds to make up the shortfall. You should still be able to proceed with the loan application, but you will be up for additional costs to get the loan approved.

Let’s look at another example:

| Offer/Value | Deposit | Loan Amount | LVR | |

|---|---|---|---|---|

| Your Offer | $500,000 | $100,000 | $400,000 | 80% |

| Bank Value | $450,000 | $100,000 | $400,000 | 89% |

In this scenario, you have put in an offer for $500,000. You have a deposit of $100,000 and you would like a loan of $400,000, giving you an LVR of 80%. The bank valuation comes in at $450,000, giving you a new LVR of 89%. If you are unable to make up the additional shortfall, then you would need to pay LMI to proceed with your loan application.

If the new LVR is over 95% – you will need to find a way to cover the shortfall with extra cash

If the valuation shortfall takes your LVR over 95%, then you will need to find additional funds to cover the valuation shortfall. 95% is the maximum LVR that banks will accept (and not all of them go that high), so if you can’t make up the shortfall then your loan will be declined.

Here’s an example:

| Offer/Value | Deposit | Loan Amount | LVR | |

|---|---|---|---|---|

| Your Offer | $500,000 | $50,000 | $450,000 | 90% |

| Bank Value | $450,000 | $50,000 | $450,000 | 100% |

In this scenario, you have put in an offer for $500,000. You have a deposit of $50,000 and you would like a loan of $450,000, giving you an LVR of 90%. The bank valuation comes in at $450,000, giving you a new LVR of 100%. If you are unable to make up the additional shortfall, then your loan would be declined as there are no lenders who will loan you 100% of the property value. The only exception is if you’re getting a guarantor loan.

Options for making up the valuation shortfall

If you need to put a higher deposit to purchase the property, then you have a couple of options to do so:

Prove that you have additional funds

Let’s start with the most obvious option first. If you have access to additional funds, such as shares that you’re willing to sell, then you can go to your lender and prove that you have additional funds to cover the shortfall amount.

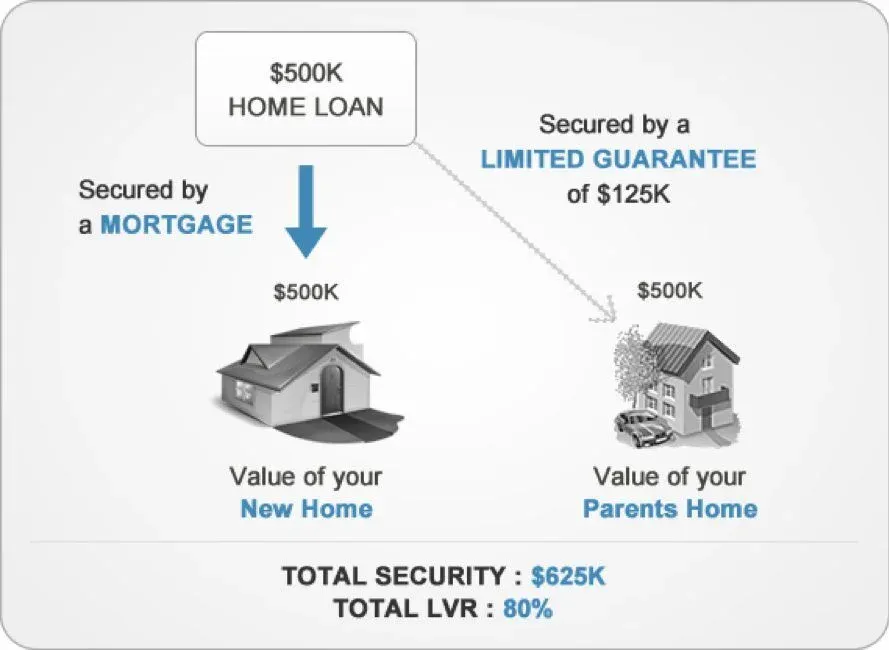

You may also be able to ask your parents or other relatives to gift you the money – the bank of mum and dad has been a great assistant to many of our clients over the years.

Use equity from another property

If you own an investment property, you may be able to refinance the loan on that property (or redraw funds from the mortgage to cover your shortfall.

If your parents or other family members own property, you could ask them to become a guarantor on the loan, which would allow you to borrow up to 105% of the property value.

Case Study: How We Were Able To Get A $110,000 Increase In A Client’s Property Valuation.

In January this year, Thomas and Kate reached out to us for some assistance with their home loan. They had just put in an offer for a lovely 3-bedroom home in a suburb in North Brisbane for $900,000.

The bank valuation came in significantly lower than their purchase price, at $790,000. With a deposit of $140,000, this would have taken their LVR to 96%. They didn’t have any additional funds, so without a better valuation they would have had to walk away from the contract.

We sourced valuation from two other lenders, providing additional supporting evidence of recent comparable sales. As you can see below, getting another valuer to take a look at the property resulted in a $110,000 increase in the value of the property.

| Date | Valuer | Amount | Difference |

|---|---|---|---|

| January 2022 | Bank Valuer 1 | $790,000 | – |

| January 2022 | Bank Valuer 2 | $800,000 | $10,000 |

| January 2022 | Bank Valuer 3 | $900,000 | $110,000 |

This was the same property, at the same time, but different valuers.

This is not unusual, although this was a higher increase than we see in most cases. And it just goes to show the value of sourcing alternative valuations if the original property valuer isn’t coming to the table.

If you’re in a similar predicament, we may be able to help. Get in contact with our brokers today to see if we can assist with arranging another valuation for you, or call us on 1300 088 065 to discuss your options.

Would you like to learn about your situation?

Case Study: How We Managed To get $20,000 Off The Purchase Price After A Bad Valuation

A few weeks ago, Sarah and Tom reached out to us at Hunter Galloway. They were ready to buy their first home — a backyard for the kids, a place to finally establish themselves — and they were looking in Hobart.

They’d first tried buying in 2022. Back then, the Hobart property market was red hot:

- Houses were selling in under 20 days

- Prices were rapidly increasing

- Every open home was packed

- Investors were outbidding them on every offer

After too many defeats, they gave up on buying a home.

The Market Has Changed

Since May 2022, Hobart’s property prices have peaked. Today:

- Properties sell in 53 days on average, compared to 28 days last year

- Prices have largely flatlined

- The average home value is 0.1% lower than this time last year

With these changes, Sarah and Tom decided to try again. After months of searching, they found the perfect home and made a strong offer. Their pre-approval was ready, and the seller accepted.

A Bank Valuation Hurdle

However, there was a problem.

When the bank conducted a formal valuation, they valued the property $20,000 below the contract price. Sarah and Tom didn’t have the extra deposit, and their dream home seemed out of reach.

Finding a Solution

Here’s the key: every seller has unique motivations. Some may be downsizing, relocating, or in a hurry to sell. Understanding this can give buyers an edge.

For Sarah and Tom, time was the key:

- They were already pre-approved, making them hassle-free buyers

- We helped them craft a careful counteroffer

Their final approach:

- Offer $20,000 below the initial price

- Reduce the settlement period from 6 weeks to 4 weeks

- Explain the situation honestly to the seller

This approach worked. By offering speed, certainty, and convenience, Sarah and Tom addressed the seller’s concerns about delays and potential re-listing. The seller accepted, and the sale went ahead smoothly.

Lessons for Buyers

If you’re buying in a declining market like Hobart or a peaking market like Canberra, you can leverage lower bank valuations to your advantage. Here’s why:

- More buyer choices – Sellers compete for fewer buyers

- Time pressures – Properties sitting on the market for months may appear undesirable

- Price uncertainty – Sellers worry about falling or flat prices

A lower bank valuation isn’t the end of the world. By understanding the property cycle and the seller’s perspective, you can negotiate smarter and still secure your dream home.

Frequently Asked Questions

How do banks assess property value?

Banks assess property value by reviewing recent sales in the area, inspecting the property, and considering market trends. They use conservative estimates to reduce lending risk. The valuation helps determine the maximum loan amount.

What is a bank valuation?

A bank valuation is an official assessment of a property’s market value performed for lending purposes. It ensures the bank does not lend more than the property is worth. This valuation can differ from a real estate agent’s market estimate.

Why do banks value property low?

Banks often value conservatively to protect themselves from market fluctuations. They prioritize risk reduction over full market potential. This can result in valuations lower than the sale price.

How to get a bank valuation of property?

You can request a bank valuation by applying for a home loan or directly through the bank’s valuation department. Provide property details and access for inspection. The bank then arranges an official valuation.

What happens if mortgage valuation is too low?

If a valuation is lower than expected, the bank may reduce your loan amount. You can negotiate with the seller or challenge the valuation. Sometimes, getting an independent appraisal helps support a higher value.

What is bank valuation vs market value?

Bank valuation is a conservative estimate for lending purposes. Market value reflects what buyers are willing to pay in the current market. They can differ, especially in rising markets.

Are bank valuations conservative?

Yes, banks usually take a cautious approach to avoid lending more than a property is worth. This means their valuations are often below potential market price. It protects both the lender and borrower.

How does a bank value a house?

Banks consider location, size, condition, and comparable sales. They also check market trends and recent property sales nearby. An inspector may visit to confirm property details.

Can you challenge a bank valuation?

Yes, you can challenge by providing evidence like recent sales, independent appraisals, or property improvements. The bank reviews the evidence and may adjust the valuation. Success depends on the strength of your supporting documents.

What happens after property valuation?

The bank finalizes your loan amount based on the valuation. You are notified if the value impacts your borrowing capacity. You then proceed with the home loan approval or renegotiation.

Bonus: Common Mistakes In Property Valuation

Real estate can be subjective, and people make common mistakes when valuing their homes. Here are some common mistakes we have seen.

Being influenced by an agent. An agent may contact you and say hey, I think your house is worth $2 million. But real estate agents can sometimes be too optimistic because they want you to list your house with them – and get a sale. Truly speaking, the real value of our home will be somewhere between what the agent thinks and the bank valuation. So don’t overly rely on the agent’s appraisal of your home.

Looking at the wrong comparison. Usually, the mistake comes when you are not comparing apples with apples. You need to look at similar houses in the same suburb with the same bedrooms and improvements etc. You should also compare similar land sizes. For example, if your house is sitting on 200 square meters and you compare it with a house on 600 square meters, you will get skewed results.

Making emotional decisions. This is especially true for those with an emotional attachment to their house. Maybe you ‘built it brick by brick’ or raised your family there. But this emotional attachment to the house can make you completely off in your property valuation.

Listening to the media. Sometimes you may think your property is worth more or less than it is because of listening to the media. This happened with covid. A lot of the media were saying property prices were going to tank, and people were so worried about what their properties were worth. Contrary to the media, property prices rose to record highs during Covid! So when considering what your property is worth, don’t let too many external factors, such as the media, influence what you think it is worth.

Next Steps And Getting Your Home Loan Approved.

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one person operations, we have an entire team of experts dedicated to help make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.