Positive Credit Reporting can be particularly beneficial for first-time homebuyers in Australia. Previously, those without an extensive credit history might have struggled to secure a home loan. Now, with CCR, lenders have access to a more comprehensive picture of an individual’s financial behaviour.

For example, a young professional who has been consistently paying rent and utilities on time, but hasn’t had a credit card or personal loan, can now demonstrate their reliability to lenders. This expanded credit profile can potentially improve their chances of securing a home loan.

However, it’s important to note that while CCR provides more information, first-time homebuyers should still focus on saving for a deposit and demonstrating stable income. Lenders will consider these factors alongside the credit report when assessing a home loan application.

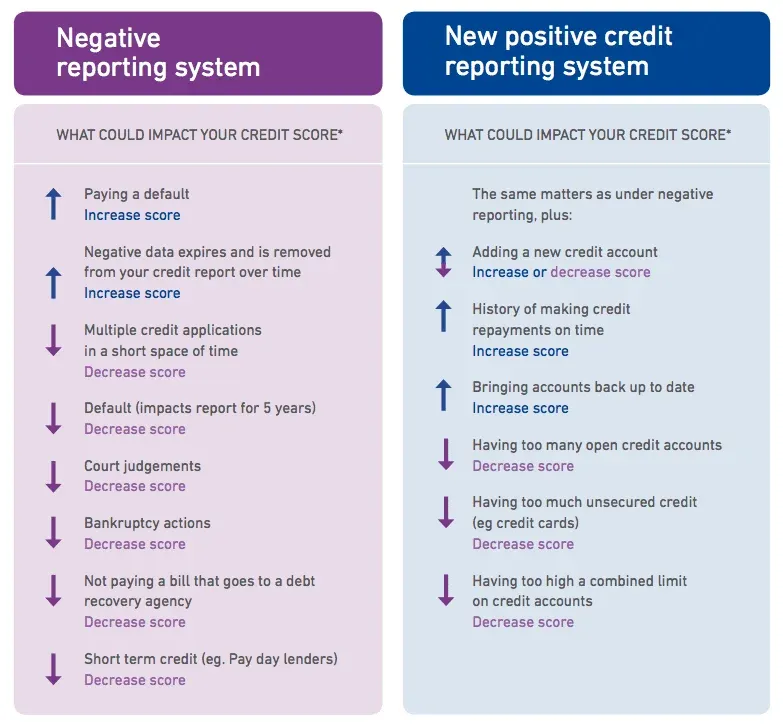

Comprehensive Credit Reporting (CCR) doesn’t just show lenders whether you’ve missed payments—it gives them a complete picture of your financial behaviour. This deeper insight can directly impact the interest rates you’re offered and your borrowing capacity when applying for a home loan. Understanding this connection can help you take actionable steps to improve your loan terms.

Here are some ways positive credit reporting can affect your interest rates and borrowing power:

Key Takeaway: Maintaining a clean and consistent credit history under CCR can translate directly into tangible financial benefits—lower interest rates, higher borrowing limits, and more flexibility when structuring your home loan.

Note: These figures are for illustrative purposes only. To find your true borrowing capacity, speak with a mortgage broker today.