Are you looking to upgrade your home but feeling the pressure of needing to sell before you can buy? A bridging loan allows you to secure your new property immediately, providing the breathing room to sell your existing home for the best possible price.

As expert mortgage brokers, we have dissected the fine print from Australia’s top lenders to give you the most comprehensive and transparent breakdown of bridging finance available.

What Is A Bridging Loan?

A bridging loan is a loan that will allow you to buy a new house before selling the existing one without necessarily making more payments on the total loan.

Selling a property can take much longer than expected, and relying on the money from the sale to buy a new home adds extra pressure.

Instead of having to rely onmatching up settlement dates, a bridging loan covers the in-between period by loaning you money while you sell your current property and buy a new one.

For example, you are living in your existing house. Then, suddenly, you see the house of your dreams, and you want to buy it. You already have the deposit for the new home but haven’t sold your existing one. In addition, your income might not be enough to technically support both loans for your existing home and the new one.

A bridging loan means that you can still have your existing home and get a loan on the new one. Essentially, it will give you more time to sell your existing property, which means that you can be fully moved into your new home before your existing property is even sold!

How Do I Qualify For A Bridge Loan?

Bridging loans are great, but you must meet the following criteria to qualify for one:

Income. You must provide evidence of your income, employment and expenses—this process is similar to a traditional home loan refinance.

Equity. You need to have enough equity in your existing home. If you’ve owned your property for some time and paid off part of the loan, the property value has increased, and you now have equity. The amount of equity required varies between lenders, but generally, having at least 20% will make the bridging loan possible.

Your current property must be on the market. While you don’t need to have sold the property for the banks to approve your bridging loan, you must have put your existing home on the market to sell with a real estate agent. Many banks require that you already have your house on the market before approving your bridging loan. So, if your property needs some fixing up and a bit of repair, you must have that sorted before applying for a bridging loan.

To qualify for a bridging loan, you must have proof of income, enough equity in your home and evidence that your current property is on the market.

It is important to know that there is a maximum bridge term when purchasing an existing property. Some banks will provide a 3, 6 or 12-month bridging period. A bridging period is the maximum time frame you have to sell your old property.

To discuss your bridging loan scenario, speak with ourMortgage Brokers and see how you can upgrade your home without having to sell it today.

There are also a few limitations to be aware of with bridge loans, including:

Some banks do not allow bridge loans for construction.

Bridge loans are not available for strata title and company purchases.

Some banks do not allow redraw during the bridging period.

Some lenders charge higher interest costs.

These restrictions differ from bank to bank.

How Much Is A Bridging Loan?

Some banks will charge a higher interest rate if you want a bridging loan, which can be up to 1% higher.

You also need to factor in the extra interest charges you will pay on the total debt while you are holding both properties during the bridging period.

For instance, if it takes you 6 months for your original property to sell, you will need to pay 6 months of additional interest. Based on a 3.50% interest rate on a $500,000 loan, this would cost you an extra $8,750. We go through this in a detailed bridging loan scenario below.

How Do The Banks Calculate A Bridging Loan?

Regardless of the type of bridging loan, the banks will be calculating your figures based on two scenarios:

With an End Debt: This is common if you are upgrading your home, and it assumes you will have a loan after you sell your existing property and buy a new property. The scenario with an end debt is the most common when you are looking at upgrading your home, and so some banks will want to make sure you can afford the loan based on the end debt or final position after you’ve sold your existing home.

With No End Debt: This is common if you are downgrading or downsizing your home. This scenario assumes you will not have a loan after you have sold your existing property and bought a new one. In the case of a bridging loan with no end debt, the banks are not concerned with your income because the sale of your original home completely pays out the bank’s loans. This scenario only really happens when you are downgrading or downsizing your home to a smaller one.

What Type Of Bridging Loan Can I Get?

There are two types of bridging loans that you can get: a closed or an open bridging loan.

An open bridging loan

An open bridging loan is when the sale of the current property hasn’t been finalised. It is great for buyers who have found what they’re looking for but haven’t yet sold their property.

This is the most common scenario of a bridging loan when you are upgrading or downgrading your existing home, which you haven’t yet sold.

A closed bridging loan

A closed bridging loan is when you have an agreed date for when your property will be sold. This gives the lender a clear outcome of when the remaining part of your bridging loan will be paid off.

A closed bridging loan is less common because if you have already agreed on a date to sell your existing property, you could line up the settlement to happen simultaneously with the new home purchase.

Buying At Auction With A Bridging Loan

If you are looking to buy in competitive markets like Sydney, Melbourne, or Brisbane, you’ll likely find that the best properties are sold at auction. The problem? Auctions require you to sign an unconditional contract on the spot—there is no “subject to finance” clause.

This is where a bridging loan becomes a powerful tool.

Becoming a "Cash Buyer"

A bridging loan essentially turns you into a cash buyer. Because the loan is secured against both your existing home and the new property, you can bid with the confidence that your finance is sorted, even though you haven’t sold your current home yet. This prevents you from missing out on your dream home just because your sale settlement dates don’t align perfectly.

The Critical Step: Bridging Pre-Approval

You cannot just walk into an auction with a standard pre-approval. Bridging finance is more complex because the bank needs to assess the risk on two properties.

Before you raise your paddle, you must have a formal Bridging Pre-Approval. The lender will need to see:

A conservative estimate of your current home’s value (often capped at 85% of market value).

The maximum “Peak Debt” you can service.

A clear exit strategy (your plan to sell).

Without this specific approval, you are bidding blind.

Pro Tip: The Deposit Gap

It is important to remember that a bridging loan funds the settlement (the final 90-100% of the purchase price), which happens 30 to 90 days after the auction. It does not provide the cash you need on auction day.

If your cash is tied up in your current home’s equity, you will likely need a Deposit Bond to pay the 10% deposit immediately after the hammer falls. (See our section below on Bridging Loans vs. Deposit Bonds).

Bridging Loan Case Studies

In this section, we will show you 3 bridging loan scenarios and explain all the jargon you will hear throughout the bridging process.

One of the case studies is a detailed one that will help you decide what type of bridging loan is right for you. So, if you need help working out if bridging is right for you, these will come in handy.

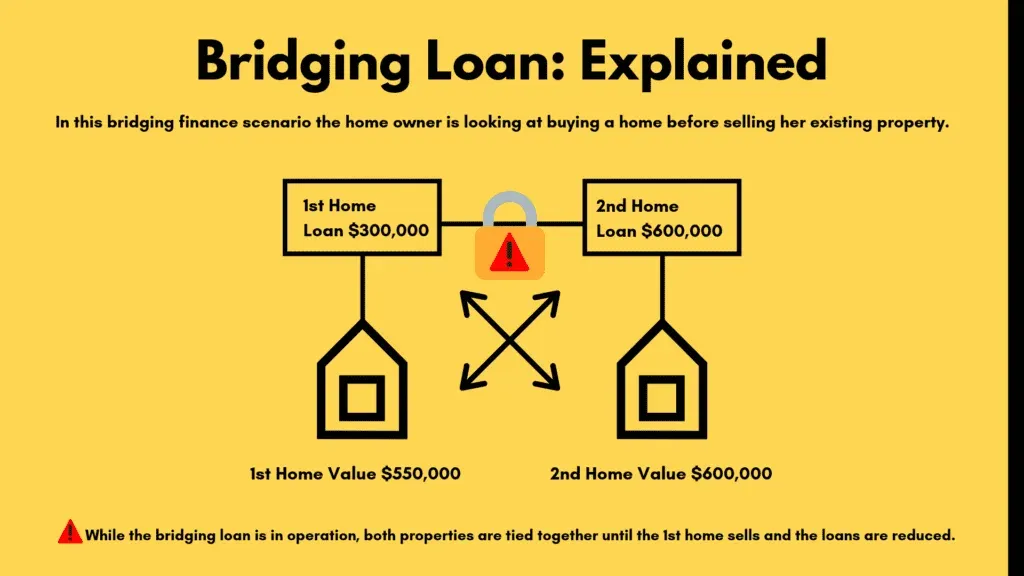

1. A simplified bridging loan case study

Camille wants to take out a bridging loan because she’s found the perfect home to move into but doesn’t want to be forced to sell her existing home quickly.

First, let’s go through the high-level figures and some jargon so you can understand how this will work.

Camille’s existing home is valued at $550,000, and she wants to upgrade and buy a new home for $600,000.

Her existing loan is $300,000, and she doesn’t want to contribute any savings, so she needs to borrow the full amount for the new property – $600,000.

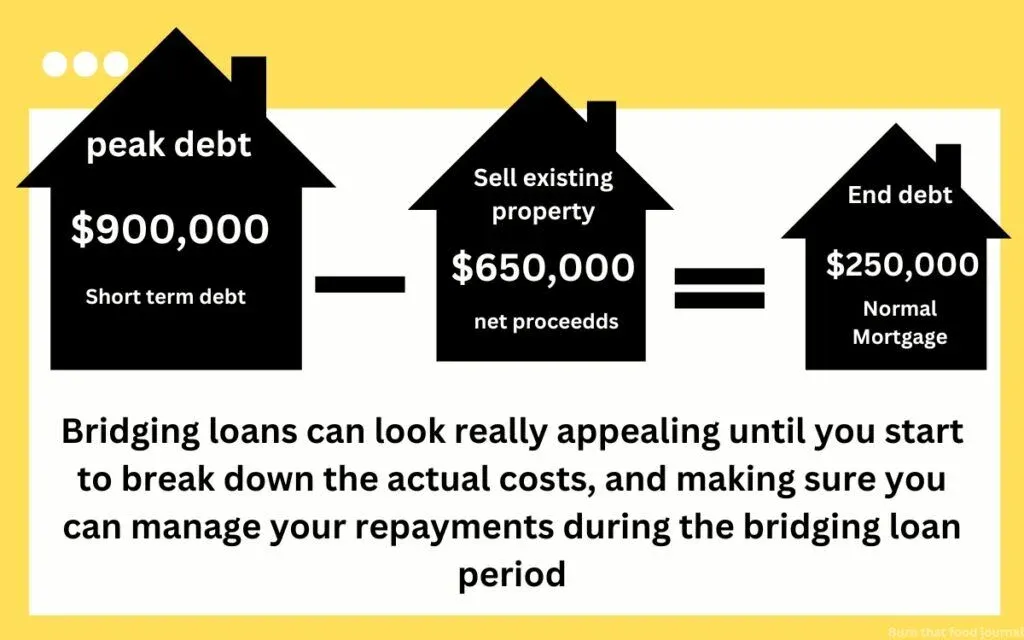

To work out her peak debt, add them together: $300,000 + $600,000 = $900,000

Camille eventually sells her existing home for $650,00

This leaves her ongoing loan balance as $900,000 – $650,000 = $250,000

The benefit of a bridging loan for Camille is that she didn’t need to be in a rush to sell her existing home, and that extra time helped her sell her original home for $50,000 more than the bank had valued it! Now, keep in mind these figures are very rough. We aren’t taking into account real estate agent’s fees, interest costs and stamp duty, which we will go through now.

2. A comprehensive bridging loan case study

Let’s look at Camille’s scenario again, taking into consideration all costs and charges.

Camille’s existing home is valued at $550,000, and she wants to buy a new home for $600,000.

Her existing loan is $300,000, and she would like to borrow the full amount for the new property and stamp duty.

In Camille’s scenario, she couldn’t afford to make repayments on the peak debt, so she would like to add the interest to the loan during the bridging period. This is also known as capitalising interest.

We also need to factor in selling costs to pay the real estate agent and stamp duty costs on the new purchase.

So, in the real world, this scenario would look like this:

Camille would still like to borrow $600,000 towards the new property and owes $300,000 on her existing property = $900,000

Additional costs to factor into a bridging loan:

Stamp Duty on new Purchase (QLD) = $14,746

Plus 12 months’ interest during Bridging Loan = $24,482*

Total Peak Debt = $939,228

*Keep in mind that the bank will calculate 12 months’ interest but only charge you for the interest you need. In other words, if you sell the property within 3 months, you will only pay 3 months’ worth of interest.

Then, to work out what the end loan would be, we need to factor in some of the costs of the sale of the property:

The banks include a fairly large buffer here in case the property sells for less or the selling costs blow out a little.

Valuation of existing home $550,000 (the bank will work on this figure, as we don’t know what the property will sell for in the future at this stage).

Plus 15% margin (a just-in-case margin the bank puts in) = $82,500

Plus, selling costs $15,750

End debt = $487,478

If Camille ends up selling the property for $650,000 instead of $550,000 (which is what the bank had valued the property), the end debt would be $100k less or $387,478.

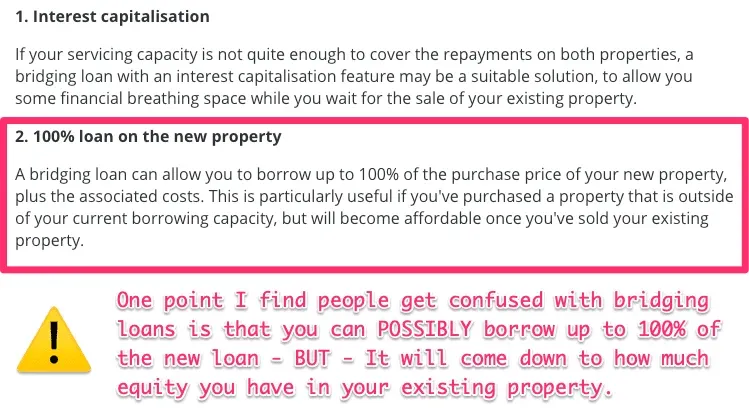

With the bridging loan’s peak debt going over 80% LVR, she would have to payLMIon this amount, which would cost an additional $8,600.

How can you avoid LMI on a Bridging Loan?

The only way to avoid this is to keep theLoan to Value Ratio (LVR) under 80% during the bridging period.

LMI is calculated on the PEAK debt – your maximum borrowing amount – not the END debt.

In Camille’s scenario, she could avoid LMI by:

Contributing $20,000 towards reducing the loan amount, or

Looking at a lower-priced property to upgrade into.

Getting a higher valuation on her existing property

Get in touch withour team of mortgage brokers to run your bridging loan scenario. Our team are experts and can give you options across various banks. Give us a call on 1300 088 065.

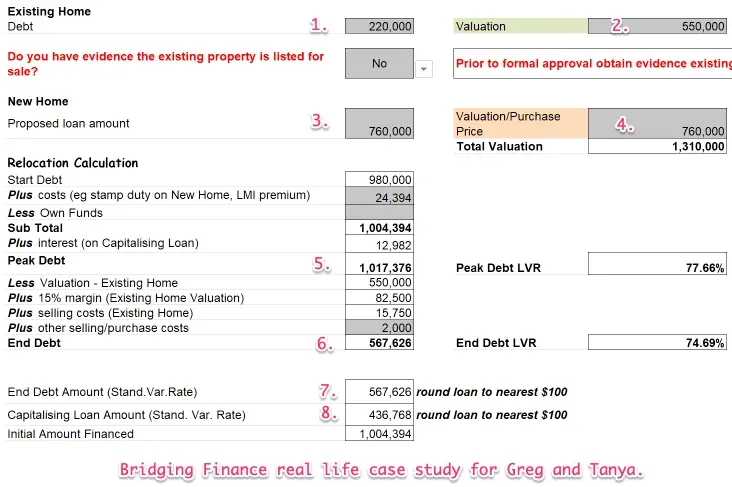

3. Upgraders Bridging loan case study: family has outgrown the home

Tanya and Greg bought their home when they first got married, but 3 kids later, they were starting to run out of space.

They had also found the perfect home to move into, but having lived in their existing home for over 10 years, they knew it needed a bit of paint before putting it on the market.

Greg had some mates who could come around and tidy up their existing home for a fraction of the price if they had some time to get everything done, so bridging seemed like the right option.

(Plus, Tanya hated moving, so she wanted to move once and only once into the new home)

How a Bridging Loan Made Sense

Tanya and Greg had concerns about having to manage two mortgages while Greg took his time to tidy up their old place.

We were able to look at a lender that capitalised or added the interest during the bridging loan period, which means they weren’t going to be put under mortgage stress.

The other benefit was Greg and Tanya didn’t need to move out to a rental house and waste money on that while they found a new home to move into.

Win-Win.

Let’s look at the numbers behind the bridging finance calculator.

The bank valued Tanya and Greg’s existing home at $550,000, and they had found a new home to purchase for $760,000.

They had already chosen a real estate agent and knew they could sell their existing home easily within 6 months.

They wanted to be able to borrow the full amount towards the new purchase of $760,000.

Existing Home Loan of $220,000

Existing Home Valued at $550,000

New purchase

New Purchase Home Loan $760,000

New Home Value – $760,000

This is when some of our bridging finance terms come in:

Peak Debt $1,017,376 (this includes capitalised interest and costs)

End Debt $567,626

And then, the bank will split this up as follows to make it easy to clear the loans once the original property is sold.

End Debt $567,626 (this is the loan that will remain)

Capitalising loan amount of $436,768 (this loan is cleared when their original property is sold)

The benefit of this structure is that Greg & Tanya are only making repayments on the end debt of $567,626 from the settlement. This is only $1,176 per fortnight, compared to if they had to make the repayments on the peak debt (which would be $2,108 per fortnight!).

Once the original property was sold

The great news is their original property sold for $556,000, meaning their capitalising loan of $436,768 was cleared, and the extra funds were paid towards their end debt to save interest!

Check to see if you are eligible for a home loan

Bridging Loan Checklist

Bridging loans can be great for the right people in the right situation, but they don’t always work out so well. We’ve created a helpful checklist that you can use to see if you will qualify for a bridging loan.

Ask yourself these questions to see if you will meet the bank’s criteria for a bridging loan:

Is the property being sold In a Metro Area (i.e. not regional) – Yes/No

Have you been in your job for at least 3 months – Yes/No

Do you have more than 20% equity in your existing home – Yes/No

Is the maximum peak debt LVR 90% or less – Yes/No

Will there be an end debt – Yes/No

Can you afford to make repayments on the end debt – Yes/No

Is there one property being sold – Yes/No

Do you have evidence the property is being listed to be sold – Yes/No

Do you plan on selling your existing home within 12 months or less – Yes/No

If you answered yes to these questions, you are more than likely able to qualify for a bridging loan.

Some banks can help if you have less than 20% equity in your existing property, but you will have to paylenders mortgage insurance on the peak debt amount.

To discuss your bridging loan scenario, speak with ourMortgage Brokers and see how you can upgrade your home without having to sell today.

Pros And Cons Of Bridging Loans

As you’ve seen so far, bridging loans are good for some but not as great for others.

Here is our comprehensive list of the pros and cons of bridging loans.

Pros of a Bridging Loan

Flexibility to buy a property immediately without waiting for a loan

Capitalised interest is possible, so you will only need to maintain repayments on the end loan and not be stressed with two mortgages.

Gives you time to wait for the right buyer on your current property instead of having to settle for a quick sale.

Saves you from having to move into a rental while you wait to find a new home to buy.

Unlimited P&I repayments. If you want to reduce your interest, you can make repayments on the loan if you wish.

Depending on the bank, you will only pay standard fees and charges compared to a regular home loan. There are no additional discharge fees or break costs.

Cons of a Bridging Loan

Two valuations are required – your current property and the new property you want to buy will need to be valued. Property valuations can cost between $200-220

Paying interest on two properties while you sell. The bank calculates daily and charges to the loan monthly. So, if your property takes a long time to sell, more interest will accrue.

Not selling the property on time can be a sting. Higher interest rates can occur, and you’ll need to pay P&I on peak debt to service the loans if it takes you more than 6-12 months to sell the property. This can cause financial stress.

No redraw facility is available.

Cannot switch lenders during the bridging loans.

To discuss your bridging loan scenario, speak with ourMortgage Brokers and see how you can upgrade your home without having to sell today.

Best Bridging Loans in Australia

Now that you know what you want, it’s time to find the right lender for you.

Not all banks can offer bridging loans, and the ones that do bridging loans call them by different names.

We’ve broken down the different banks and the names that they refer to them by.

Some of these banks require a minimum of 50% equity in your existing property, so chat with ourMortgage Brokers on 1300 088 065 to understand what bank will best suit you.

While all these banks offer bridging loans, they all come with different costs and advantages.

As we mentioned, the best bank for you will depend on your individual situation. Speak with our team ofMortgage Brokers to understand what bank will best suit you.

Common Bridging Loan Issues We See

Sellers always overestimate how much their existing property is going to sell for and then fall short of the payment for the bridging loan. So be aware of this and do adequate research on sales in the market at the moment.

Sellers struggle to sell their property within the bridging period, adding extra stress and costs to the loan. As we mentioned above, not all banks will require you to make repayments on the peak debt during the bridging loans.

Make sure you are aware of what your bank offers before going down the bridging loan path.

What Happens If My Home Doesn’t Sell in 12 Months?

This is the single biggest fear for anyone taking out a bridging loan: What happens if the clock runs out?

It is a valid concern. Bridging loans are not open-ended; they have a strict expiry date, usually 12 months from the day of settlement. If you haven’t sold your property by then, things can get complicated.

The "Fire Sale" Clause

You need to be aware that the bank holds the mortgage over your property. If the bridging period expires and you haven’t sold, the bank technically has the right to step in, take possession of the property, and sell it themselves to recover the debt.

This is often referred to as a “fire sale.” The bank’s priority in this scenario is recovering their money quickly, not getting you the highest market price. While banks generally view this as a last resort, it is a contractual reality you must understand.

Default Interest Rates

Before a forced sale happens, you will likely be hit with financial penalties.

If your loan goes beyond the agreed term (e.g., 12 months), the bank may switch your interest rate from the standard bridging rate to a “default rate” or “penalty rate.” These rates are significantly higher—often jumping by 2% to 4%—which can rapidly erode the equity you have left in your home.

How to Protect Yourself

The best way to avoid this scenario is to be realistic from day one.

Choose the Longest Term: Even if you think your home will sell in 3 months, apply for a 12-month bridge. It gives you a safety buffer.

Price It Right: Don’t chase an unrealistic “dream price” for 6 months. If the market is softening, listen to your real estate agent and adjust your price early.

Communicate: If you are approaching month 11 and haven’t sold, talk to your lender immediately. If you can prove you have lowered the price to meet the market, some lenders may grant a short extension at their discretion.

How Much Can I Borrow Using A Bridging Loan?

How much you can borrow is dependent on the following 4 factors:

1. Existing equity In your home

Usually, lenders will add an interest rate buffer of 6 months to assess your ability to pay off the bridging loan. When it comes to adding a buffer, the property that is being sold will be reduced by 15% as a “fire sale” buffer for the projected sale.

This lower price can have an impact on your borrowing power, as the lender will be considering a property price lower than your projected outcome to maintain a conservative approach.

2. Will you have an end debt?

If you are upgrading your home, you will likely have some lending left over after you sell your original property.

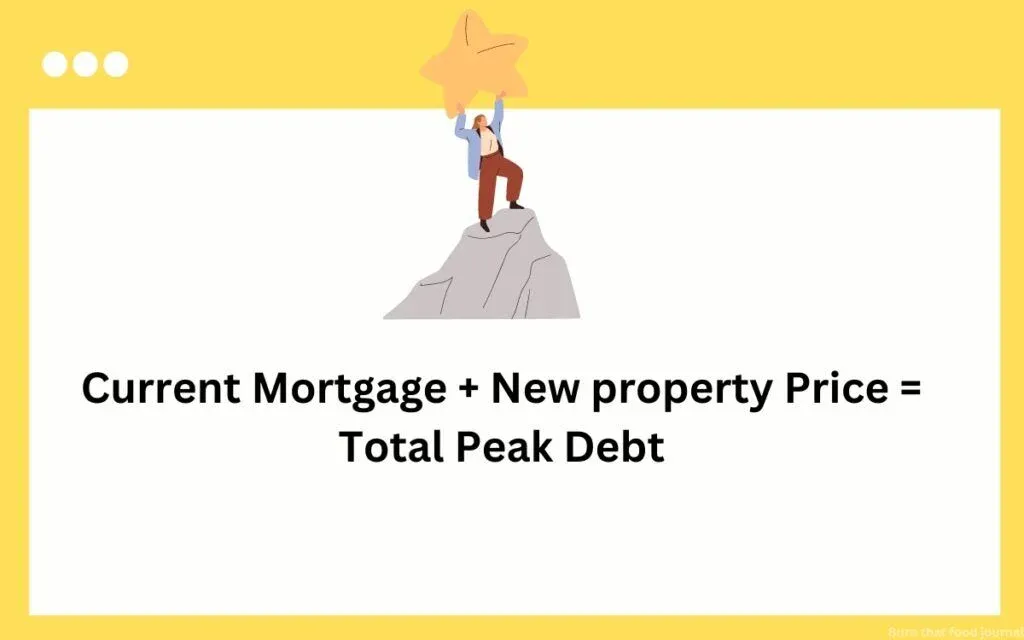

3. What the Peak Debt will be

Your peak debt is the combination of your new property price plus what’s left of your current mortgage. Once you have this, on average, you will be able to borrow up to 90% of the combined property values.

Current mortgage + New property mortgage = Total peak Debt

4. Existing property on the market

Most banks will want to see evidence that you have listed your existing home for sale on the market, either by an engagement letter from a real estate agent, a draft contract of sale or seeing the property listed online.

Wait, I Don’t Understand How Bridging Loans Actually Work

Let’s take a few steps back and outline it simply.

A bridging loan is getting finance to fill the gap between buying and selling a property. So instead of selling a property and waiting for that money to come through, you’ll have finance before and then can pay it back.

You will need a valuation to get the figures for your existing and new homes.

Your peak debt will be worked out as follows:

Current mortgage + New property price = Total peak Debt

Your eligibility will be assessed, and then this figure left is called an “ongoing balance”, which is the principal of the loan.

Both properties will be used as security, but the loan will be combined.

During this interim, many lenders allow interest-only repayments on the peak debt so that you can hold off paying principal and interest repayments and not need to manage two loans.

Once the property is sold, your repayments will begin as normal, and any compounded bridge loan interest will be added to your new loan.

Current mortgage + New property mortgage = Peak debt

Would you like to learn about your situation?

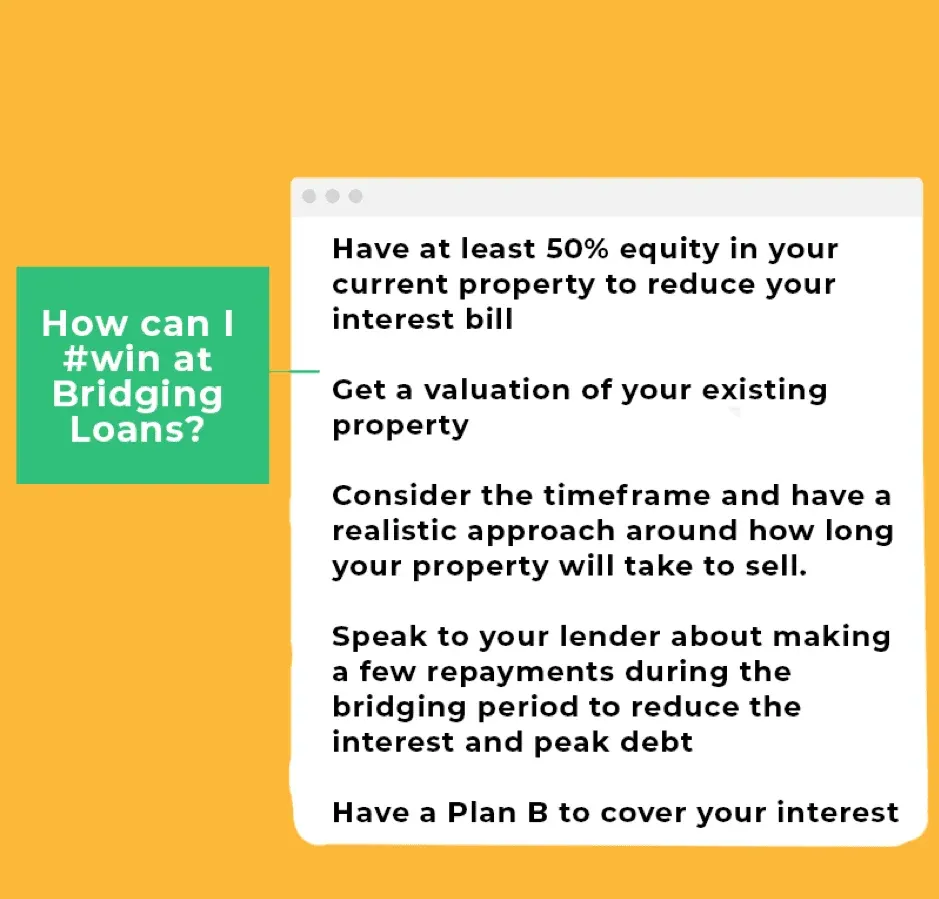

How Can I Win At Bridging Loans?

To win at Bridging Loans, follow these steps:

Have at least 20-40% equity in your current property to make bridging possible.

Get a valuation of your existing property. Research and be realistic about how much it will sell for.

Consider the timeframe and have a realistic approach to how long your property will take to sell. Remember, settlement alone can take 6 to 8 weeks.

Speak to your lender about making a few repayments during the bridging period to reduce the interest and peak debt.

Have a Plan B to cover your interest while you’re trying to sell – can you get short-term tenants in your property for extra income, or can you move back home or with a friend for a little while to save money?

Why You Should Avoid Bridging Loans - A Case Study

Now that we’ve covered the basics, let’s dive deeper into why you might want to think twice about a bridging loan.

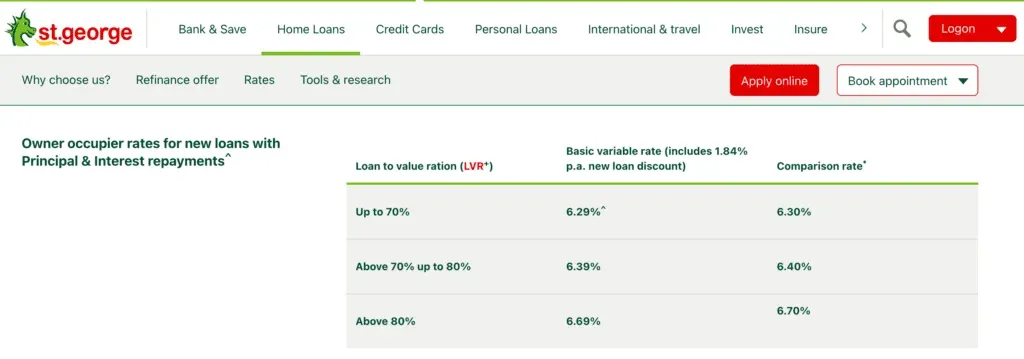

We will use St George as our reference point, one of the many banks offering bridging loans. However, the principles we discuss are common across lenders.

When you first apply, the interest you’ll hear about pertains to your end debt – essentially, what you’ll owe after the sale of your home. As we can see here, rates are starting from 6.29%.

But here’s the catch. Banks charge a different interest rate for the bridging period; as you can see, these rates start from 9.05%.

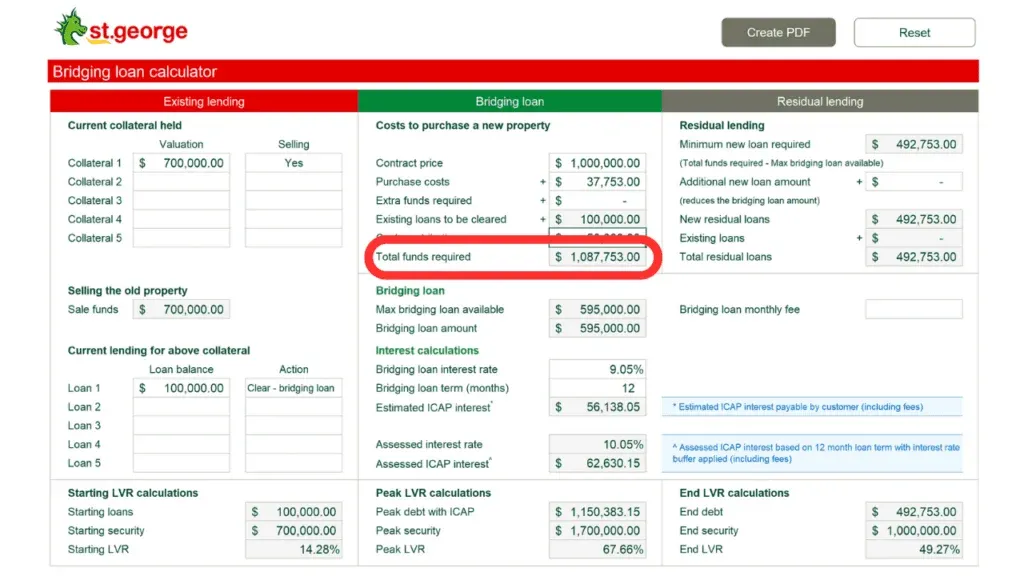

Let’s say you have a house worth $700,000 with an outstanding mortgage of $100,000. You want to buy a property priced at $1,000,000, factoring in all relevant fees and charges. With $50,000 in your savings, the total amount needed to finalise the purchase is close to $1.09 million.

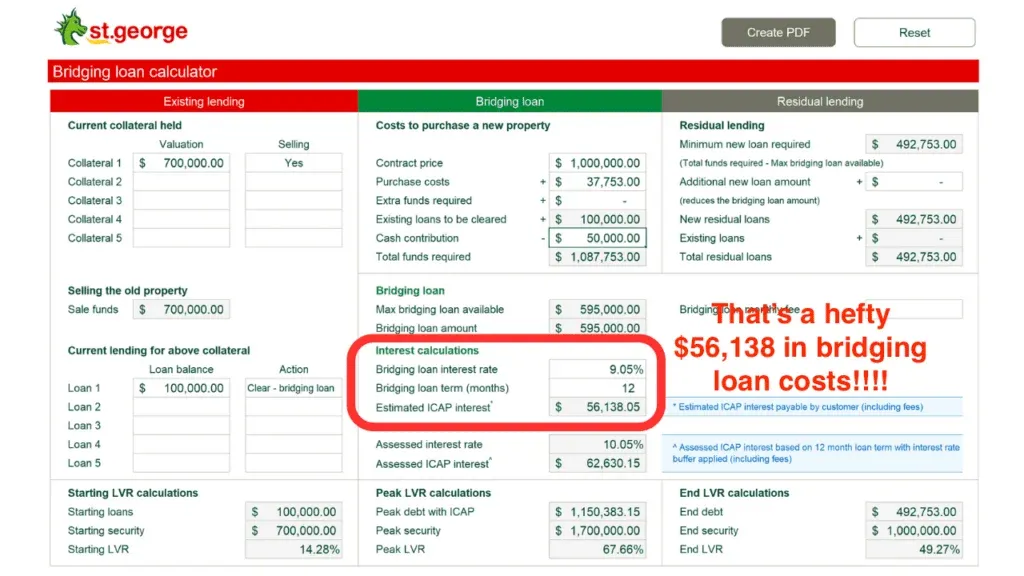

Now, here’s the kicker. As highlighted before, the bank charges a 9.05% interest rate for their bridging loan facility. When you calculate this interest over a year, it amounts to a hefty $56,000!

And that is the real reason you’ll want to avoid a bridging loan!

Even if you have the bridging loan for just a few months, it will still cost you $15,000 for the convenience. When you consider everything, there’s simply no justification for going that route.

Bridging Loans vs. Deposit Bonds: What’s the Difference?

It is very common for homebuyers to confuse bridging loans with deposit bonds. While both are tools to help you buy a new home before selling your old one, they serve completely different purposes in the buying timeline.

Understanding the difference can save you thousands in fees and ensure you don’t get caught out when signing a contract.

The Key Difference

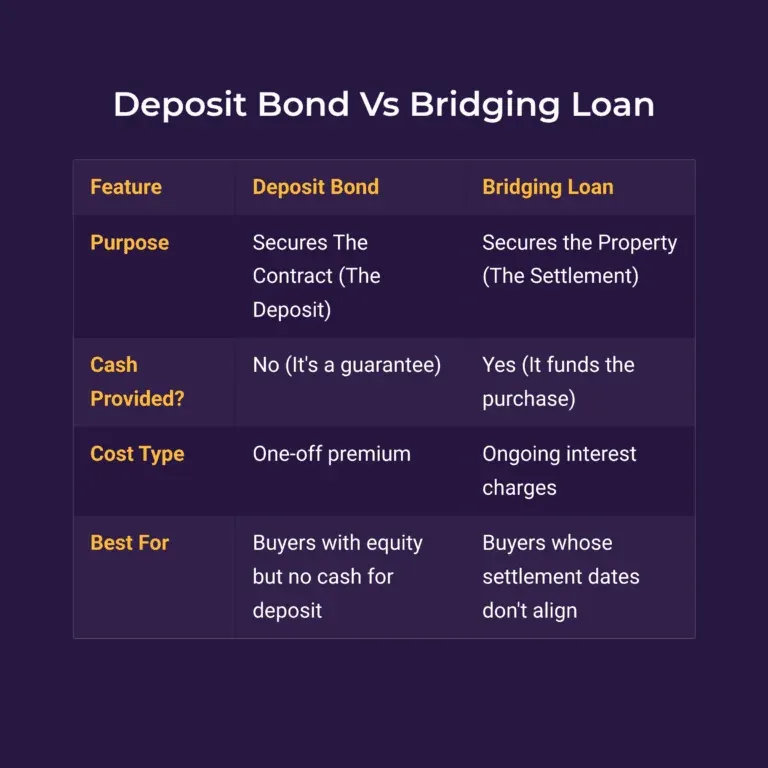

Think of a Deposit Bond as an insurance policy and a Bridging Loan as the actual funding.

A Deposit Bond guarantees the seller that the 10% deposit will be paid at settlement. It is a substitute for cash on the day you exchange contracts. It does not lend you actual money; it simply acts as an “IOU” backed by an insurer.

A Bridging Loan is a credit facility that pays the entire purchase price (the remaining 90-100%) plus stamp duty on the day of settlement. It pays out your old loan and funds the new one.

When Do You Use Which?

You might actually need both, depending on where your cash is sitting.

Use a Deposit Bond when you have plenty of equity in your current home, but you don’t have access to liquid cash (savings) to write a cheque for the 10% deposit required to sign the contract today.

Use a Bridging Loan when the settlement dates don’t match up. For example, if you need to pay the seller for the new house on March 1st, but your old house won’t sell until May 1st, the bridging loan covers that gap.

Cost Comparison: Fees vs. Interest

The costs for these products are calculated very differently:

Deposit Bond: You pay a one-off fee (premium), usually calculated as a percentage of the deposit amount (e.g., ~1.3%). Once paid, there are no ongoing costs.

Bridging Loan: You pay interest on the total peak debt for every day the loan is open. As mentioned in our case studies, this can add up if your property takes a long time to sell.

Summary Table

What Can I Do Instead Of A Bridging Loan?

Many opt for a bridging loan simply because they are unaware they have other choices.

Here are 4 strategies that will achieve the same result without the hefty price tag.

1. Subject to sale

Whether you buy or sell first. Include a subject-to-sale clause. For instance, if you’re buying, condition your offer on the sale of your current home. This means that finance will be subject to the unconditional sale of your home.

2. Extended terms

Consider opting for an extended settlement duration. In this case, you’d agree to sell or buy a home with a longer settlement period.

For example, if you get an offer to sell your home with a 30-day settlement, try to extend this to 90 days. This gives you a three-month runway to find and finalise your next purchase.

3. Simultaneous settlement

This approach might be uncommon, but it’s entirely feasible!Simultaneous settlement involves buying and selling at the same time. Essentially, the funds from your sale directly facilitate your purchase. It’s a great option as it allows you to avoid all fees, such as rental or bridging.

Before listing your property for sale, know exactly the type of home you’re looking to buy. Be specific with what you’re after, and have no more than three suburbs on your shortlist. You will need to be a suburb expert to pull this off because the clock starts ticking the moment you list your property for sale.

4. Selling your home first

Another approach is to sell your home before buying a new one.

The biggest challenge is once you’ve sold your property, you’ll need to secure another place to stay, whether a rental or moving back with family. This transition often brings added expenses.

However, there are ways to navigate this:

One solution is to arrange a rent-back agreement on the property you’re selling. This means the new owners would lease the property back to you for a predetermined duration.

Alternatively, you can establish a rental contract for yourself before selling. This ensures the ongoing lease agreement is honoured. But a word of caution: this might make your property less appealing to potential buyers, especially if the rent is below the market rate.

Bonus: Bridging Finance For Downsizers & Retirees

One of the most common questions we get is, “Can I get a bridging loan if I am retired and don’t have a regular salary?”

The short answer is: Yes.

If you are an empty nester looking to downsize from a large family home to a manageable apartment or a lifestyle village, bridging finance is often the perfect solution.

The "Exit Strategy" Approval Process

Many retirees worry they won’t qualify for a loan because they no longer have a payslip. However, bridging finance for downsizers works differently from a standard mortgage.

In this scenario, banks are less concerned with your income servicing (your ability to make monthly repayments from a salary) and are focused entirely on your Exit Strategy.

Since you are downsizing, the sale of your large original home will typically cover the purchase of your smaller new home in full. This creates a “No End Debt” scenario. Because the bank knows the loan will be fully extinguished once your property sells, they are willing to lend based on the equity in your current home rather than your pension or superannuation income.

Skip the Stress of Moving Twice

For many over-60s, the physical and emotional toll of moving house is significant.

Without a bridging loan, you would typically have to:

Sell your family home.

Move into a rental property (moving all your furniture twice).

Wait to find a new home.

Move again.

A bridging loan allows you to bypass the “middle-man” rental. You can take your time to find the perfect retirement property, move in comfortably, and then prepare your old home for sale at your own pace—vacant and perfectly styled to achieve the highest possible price.

Bridging Loan Frequently Asked Questions

Can I use a bridging loan to pay the 10% deposit?

No, typically a bridging loan is used for the settlement of the property, not the initial deposit exchange. Most buyers use a Deposit Bond or a temporary equity release to pay the 10% deposit before the bridging loan kicks in at settlement.

How long does it take to get a bridging loan approved?

Bridging loans generally take 2 to 4 weeks for approval. Because the bank requires valuations on two properties (your current home and the new one), the process is slightly slower than a standard mortgage application.

Is it possible to get a bridging loan for construction?

Yes, but it is restricted. A “Construction Bridging Loan” allows you to build a new home while living in your current one. However, fewer lenders offer this, and they often require a larger equity buffer to cover the construction period (often 12 months+).

What is the maximum term for a bridging loan?

Most lenders offer a maximum bridging period of 12 months for buying an existing property. If you are building a new home, some lenders may extend this to 24 months to accommodate construction delays.

Do I have to make repayments during the bridging period?

Usually, no. Most bridging loans allow you to capitalise interest, meaning the interest is added to your loan balance rather than paid monthly. You only start making full repayments once your old home sells and the residual debt is finalized.

Can I rent out my old home while it is on the market?

Yes, you can, but it depends on the lender’s policy. However, in a bridging scenario, the goal is to sell the property vacant to maximize appeal. Renting it out might restrict viewings and delay the sale, which adds to your interest costs.

Do bridging loans have higher interest rates?

Yes. The interest rate on the “Peak Debt” (the total combined loan) is often higher than a standard variable rate. However, once your property sells and you revert to the “End Debt,” your rate usually returns to a competitive standard home loan rate.

Can I get a bridging loan if I am retired?

Yes. This is often called “Downsizer Bridging Finance.” Since there is usually no “End Debt” (because the sale covers the new purchase), banks focus on the equity in your home rather than your regular income.

How much equity do I need for a bridging loan?

Generally, you need at least 20% to 50% equity in your current home. If your total Loan-to-Value Ratio (LVR) exceeds 80% across both properties, you may need to pay Lenders Mortgage Insurance (LMI), which can be costly.

What happens if I sell my home for less than expected?

If your home sells for less than the bank’s valuation, your “End Debt” will be higher than calculated. You must be able to service this higher residual loan. If the sale price doesn’t cover the Peak Debt, you will need to cover the shortfall from savings.

Are there exit fees for bridging loans?

Most modern bridging loans are variable rate products and do not have specific “exit fees” for paying them out early. In fact, banks want you to pay them out early by selling your home. Always check your specific loan contract for discharge fees.

Can I use a bridging loan to buy an investment property?

Yes, but the structure is different. If you are keeping your original home as an investment, you technically aren’t “bridging” (selling one to buy another); you are simply accessing equity. Bridging specifically refers to the intent to sell the original security.

Next Steps And Getting Your Home Loan

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one-person operations, we havean entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call at 1300 088 065 orbook a free assessment onlineto see how we can help.

Our team of home loan experts is here to help you buy a home in Australia.