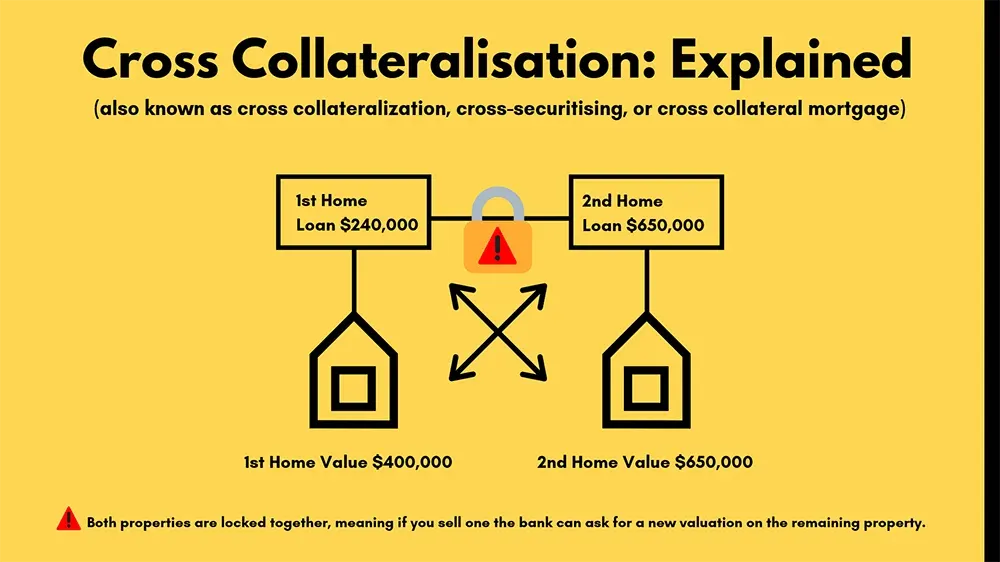

Cross-collateralisation can be a powerful tool for property investors, but it also comes with hidden risks that many buyers overlook. By tying multiple properties to one loan, you may unlock higher borrowing capacity — but you also limit your flexibility if you want to refinance, sell, or change lenders later.

This guide, written by an expert mortgage broker in Brisbane, explains how cross-collateralisation works, when it might suit you, and the key pitfalls to avoid.

Let’s dive in.