Deposit calculator [How much do I need to buy a house or home loan?]

Loan approval rate of 97%*

Variety of options due to direct access to 30+ Australian banks & lenders

Highest-rated Mortgage Broker in Brisbane — 2,400+ Google reviews

Free for you, and you won't pay more — the lender pays us

35+Years of

experience

Based on

2,400+ reviews

Mortgage Broker of the Year in 2017, 2018, 2019 and 2024

Access to 30+ banks and lenders in Australia

Thousands of families helped into their homes

*Based on all applications processed through Hunter Galloway, 2024–2026.

Deposit calculator [How much do I need to buy a house or home loan?]

The information provided in this calculator is intended to provide illustrative examples based on stated assumptions and your inputs. Calculations are meant as an estimate only and it is advised that you consult with one of the team here at Hunter Galloway – Mortgage Broker Brisbane about your specific circumstances.

Planning to buy a home in 2026? The first step isn’t browsing real estate listings—it’s knowing your numbers. Our Home Loan Deposit Calculator helps you instantly estimate how much cash you need to save, factoring in hidden costs like Stamp Duty and Transfer Fees. Whether you’re aiming for a standard 20% deposit or using a First Home Buyer scheme with just 5%, this tool gives you the real bottom line in seconds.

We should point out that this is a really simple calculator.

So if you’re not super technical, you’ll love the calculator and simple steps in this guide.

Let’s get started.

How Do I Use The Deposit Calculator?

We designed this tool for speed and simplicity. Here is how to check your buying power in seconds:

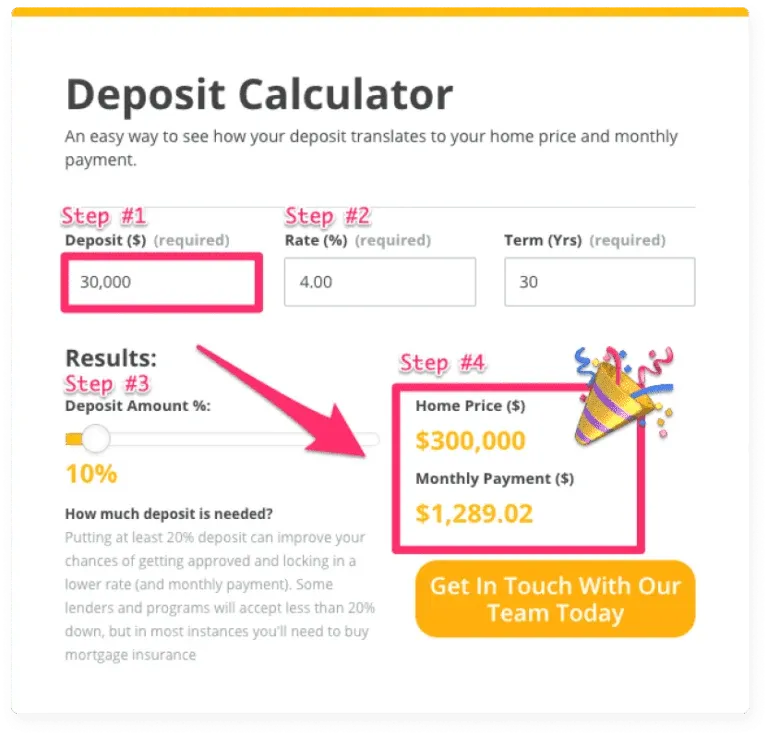

Step #1: Enter your savings

Input the total cash you have available for your deposit. In this example, we used $30,000.

Step #2: Adjust the variables

You can change the loan term (usually 30 years) and the interest rate.

Pro Tip: Use a rate of around 6.0% to get a realistic estimate for 2026.

Step #3: Choose your deposit size

Select the percentage of the property price you want to pay upfront.

Aiming for 20%? This avoids Lenders Mortgage Insurance.

Buying sooner? select 5% to 10%. In this example, we chose 10%.

Step #4: See your results

The tool instantly calculates your potential purchase price and monthly repayments.

Based on a $30,000 deposit (10%), you could target a $300,000 property. Your estimated repayments would be approximately $1,620 per month (assuming a standard variable rate).

Important Note:

This calculator provides an estimate based on your savings only.

Your final borrowing limit depends on your income and expenses (your Borrowing Capacity).

To get your exact number, chat with our team on 1300 088 065 or book a free assessment.

A house deposit is the upfront contribution you pay to secure a home loan. It lowers the risk the bank takes when lending you money.

Think of your deposit in two parts:

The Bank Deposit: The minimum percentage of the purchase price the bank requires (usually 5% to 20%).

The Transaction Costs: Extra savings you need for fees like Stamp Duty and solicitors.

So, how much do you actually need?

Most first home buyers should aim for 8% to 10% of the purchase price in total savings.

This covers your minimum 5% bank deposit plus the “hidden costs” like government fees and conveyancing.

Let’s look at a 2025 example:

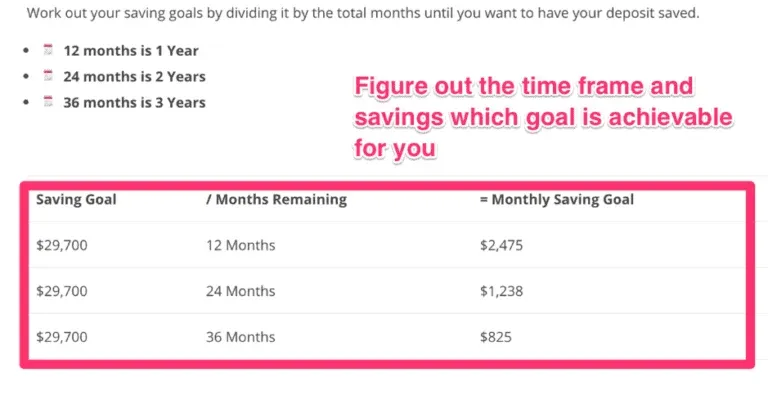

If you want to buy a home for $600,000, you should aim for $60,000 in savings (10%).

Bank Deposit (5%): $30,000

Costs & Buffer: $30,000 (covers Stamp Duty, transfer fees, and legal costs)

You can calculate this manually:

Purchase Price x 0.10 = Recommended Savings Goal

$600,000 x 10/100 = $60,000

The easiest way to get your exact number? Use our deposit calculator above.

How Does My Deposit Affect My LVR?

You will often hear mortgage brokers talk about “LVR.”

It stands for Loan-to-Value Ratio, and it is one of the most important numbers in finance.

Simply put, it is the percentage of the property’s value you need to borrow.

How it works:

Purchase Price: $500,000

Your Deposit: $50,000 (10%)

Your Loan: $450,000 (90%)

Your LVR:90%

The "Risk Scale"

Banks use your LVR to measure risk.

Lower Deposit = Higher LVR: This is higher risk for the bank.

Higher Deposit = Lower LVR: This is safer for the bank.

Because high LVR loans are riskier, banks often charge extra fees or higher interest rates to protect themselves.

The “Golden Number”: 80%

In the Australian mortgage market, 80% LVR (a 20% deposit) is the magic number.

If you can keep your loan at or below 80% of the property value, you generally avoid paying Lenders Mortgage Insurance (LMI).

Crossing this line means thousands of dollars in extra insurance costs.

LVR changes your interest rate

Your deposit size doesn’t just affect your upfront costs; it affects your monthly repayment too.

Many lenders now use “Tiered Pricing.” This means they reward “safe” borrowers with lower interest rates.

LVR under 60%: Often unlocks the absolute lowest rates (“Green Tier”).

LVR under 80%: Standard competitive rates.

LVR over 80%: Often attracts a slightly higher interest rate plus LMI fees.

Expert Tip: If you have a 10% deposit, you can still buy a home today.

While you might pay a slightly higher rate than someone with a 20% deposit, getting into the market sooner is often the smarter financial move.

Don’t guess the difference. Get a qualified mortgage broker to calculate the real cost of paying LMI versus the cost of renting for another two years.

Is Stamp Duty Part Of My House Deposit?

Yes, Stamp Duty is a government tax that forms part of your total “upfront costs.”

Crucial Rule: You generally cannot borrow Stamp Duty from the bank. It must be paid from your own cash savings.

This means if you have a 5% deposit for the loan, you often need another 3-4% in savings just to cover the Stamp Duty.

But here is the good news, many state governments have slashed Stamp Duty for first home buyers. In some states, you could pay $0 in Stamp Duty, saving you tens of thousands of dollars.

You can use our Stamp Duty Calculator to get the exact figure for your situation, but we have included a summary table below to show you where the concessions currently sit.

State

First Home Buyer Concession?

Stamp Duty Waived Up To

Stamp Duty Discounted Up To

QLD

Yes

$700,000 (Established)

Unlimited (New Builds)*

$800,000

NSW

Yes

$800,000

$1,000,000

VIC

Yes

$600,000

$750,000

WA

Yes

$430,000 – $500,000

$530,000+

SA

Yes (New Homes Only)

Unlimited (New Builds Only)

–

TAS

Yes

$750,000

–

ACT

Yes (Income Tested)

$1,000,000

–

NT

Limited

House & Land Exemptions

–

Note: QLD currently offers a full concession on eligible new homes regardless of value.

Note: WA thresholds can vary by region (e.g., Metro vs Regional).

Let’s look at a real-life example:

Imagine you are a first home buyer purchasing a townhouse in Brisbane (QLD) for $650,000.

Standard Stamp Duty: You would normally pay around $24,000.

Your Cost: Because the purchase is under the $700,000 threshold, you pay **$0**.

That is an instant $24,000 saving that stays in your pocket!

However, if you bought that same property in a state without a full waiver for that price, you would need to have that cash ready before settlement.

Always check with a mortgage broker to confirm your specific eligibility, as these government rules change frequently.

How Much Deposit Do I Need For A $300,000 House?

Let’s look at a real-life example for a $300,000 home in Queensland.

The Good News:

If you are a first home buyer, your Stamp Duty is $0 (waived).

The “Hidden” Costs:

Even with the stamp duty waiver, the government still charges a Transfer Fee and a Mortgage Registration Fee. You also need to budget for professionals to check the property and handle the paperwork.

Here is the breakdown of what you need to save on top of your bank deposit:

Transfer Fee: $840 (Paid to Titles QLD)

Registration Fee: $240 (Paid to Titles QLD)

Conveyancing: $1,500 (Estimate for legal fees)

Building & Pest: $600 (Don’t skip this!)

The Total Cost:

To buy this $300,000 home safely, we recommend aiming for 8% of the purchase price (approx. $24,000).

This ensures you have your 5% bank deposit plus a safety buffer for all costs.

Your Savings Goal Breakdown:

Bank Deposit (5%): $15,000

Fees & Costs: $3,180

Safety Buffer: $5,820 (For moving costs or unexpected expenses)

TOTAL:$24,000

Not a First Home Buyer?

If you have owned a home before, you are not eligible for the waiver.3 You would need to pay approximately $3,000 in Stamp Duty (Home Concession rate).

This means your total required savings would jump to around $27,000.

Note: Government fees change annually (usually in July). Use our stamp duty calculator for the most up-to-date figures.

How Much Deposit Do I Need For An $800000 House?

With property prices rising, $800,000 is now a common entry point for family homes in Brisbane, Melbourne, and Sydney.

But as the price goes up, so does the deposit hurdle.

The Breakdown: 5% vs 10% vs 20%

Here is exactly how much cash you need to save for an $800,000 purchase:

5% Deposit (Minimum):$40,000

The Catch: You will likely pay a high LMI fee (approx. $32,000) unless you use a government scheme.

10% Deposit (Standard):$80,000

The Benefit: Your LMI fee drops significantly (to approx. $16,000), and you are seen as a lower-risk borrower.

20% Deposit (Gold Standard):$160,000

The Goal: You pay $0 LMI and unlock the lowest interest rates.

Warning: The "Stamp Duty Cliff"

At the $800,000 price point, your location matters huge amounts for your upfront costs.

In NSW: Good news! As a first home buyer, you currently pay $0 Stamp Duty on homes up to $800,000. Your focus is just the deposit.

In QLD: If you buy an established home for $800,000, you are over the $700,000 concession cap. You will pay full Stamp Duty (approx. $21,000) on top of your deposit.

Exception: If you build a brand new home in QLD, the stamp duty is $0.

The Smart Strategy for $800k:

If you don’t have $160,000 saved (and who does?), look into the First Home Guarantee.

As of late 2025, the price caps have increased (e.g., to $1,000,000 in Brisbane and many capital cities).

Result: You can buy that $800,000 home with just a $40,000 deposit and pay $0 LMI, saving you over $30,000 in fees.

Why Is Knowing My House Deposit Important?

Your deposit is the anchor of your entire property purchase.

If you don’t know your numbers, you are essentially flying blind.

Why you need clarity right now:

Set a Realistic Budget: Stop guessing. Knowing your deposit helps you target the right suburbs and property types.

Unlock Borrowing Power: Your savings balance directly influences how much the bank is willing to lend you.

Avoid “Hidden Cost” Shock: You ensure you have enough leftover for Stamp Duty, legal fees, and moving costs.

The Bottom Line: Your savings usually set your borrowing limit. Without this exact figure, it is impossible to start a serious property search. Lock in your deposit number first, then start scrolling the real estate listings.

House Deposit Amount Examples

You are probably scrolling through real estate apps asking, “How much cash do I actually need for a $600,000 or $800,000 home?”

In the 2026 market, prices have moved up, and so have deposit targets.

The “Standard” Route (Paying LMI):

If you have less than a 20% deposit, most banks will charge Lenders Mortgage Insurance (LMI).

The Minimum: We typically recommend having 8% to 10% of the purchase price in genuine savings.

The Math: This covers your 5% bank deposit + Stamp Duty + Fees. The LMI fee is then usually “capitalised” (added) on top of your loan, up to a maximum of 95% LVR.

The “Smart” Route (Government Schemes):

As of late 2025, the Australian Government First Home Guarantee Scheme has expanded with unlimited places and no income caps.

The Win: You can buy with just a 5% deposit and pay $0 LMI.

The Catch: You must buy a property under the price cap for your region (e.g., $1,000,000 in QLD Capital Cities).

Deposit Breakdown Table (2026 Estimates)

Our calculator gives you the exact down to the dollar figure, but this guide shows the gap between “Avoiding LMI” vs “Getting in Early.”

Purchase Price

20% Deposit (No LMI – Ideal)

10% Deposit (LMI Capitalised)

5% Deposit (Govt Scheme – No LMI)

$450,000

$90,000

$45,000

$22,500

$550,000

$110,000

$55,000

$27,500

$650,000

$130,000

$65,000

$32,500

$750,000

$150,000

$75,000

$37,500

$850,000

$170,000

$85,000

$42,500

$1,000,000

$200,000

$100,000

$50,000

Note: The “5% Deposit” column assumes you are eligible for the Government 5% Deposit Scheme and have additional funds/waivers for Stamp Duty. Without the scheme, a 5% deposit would incur LMI costs.

The short answer is yes, but you usually need a little help.

While most banks want to see “genuine savings,” there are strategic ways to enter the market with $0 of your own savings.

If you are lucky enough to have family support or work in a specific profession, you can bypass the traditional savings grind entirely.

Here are the most common “No Deposit” strategies:

The Family Guarantor (Most Popular): Your parents use the equity in their home as security for your loan. This allows you to borrow 100% of the purchase price (plus costs) and pay $0 in Lenders Mortgage Insurance.

Gifted Funds: Your parents or close relatives gift you the cash for the deposit. Most lenders now accept “non-genuine savings” (gifts) if the loan-to-value ratio is low enough or if you pay LMI.

First Home Owners Grant : In Queensland, the $30,000 grant (available until June 30, 2026) can form a huge chunk of your funds. Note: This is usually paid at settlement, so you may still need a small amount of cash to sign the initial contract.

Medical & Legal Professionals: Doctors, dentists, and some legal pros can often borrow 95% to 100% of the property price with NO LMI due to their stable income profile.

Buying with a Partner: Teaming up with a sibling or friend to split the deposit requirement in half.

Generally speaking, you should aim for 8% to 10% of the purchase price.

While lenders only require a 5% bank deposit, you need that extra buffer to cover “sunk costs” like Stamp Duty and legal fees.

The "Genuine Savings" Rule

Most banks want to see that you have held at least 5% of the purchase price in your own bank account for 3 months or longer. This proves you have the financial discipline to handle a mortgage.

If you are currently renting, we have huge news.

Many lenders now accept 12 months of rental history as proof of genuine savings.

The Benefit: You don’t need to wait 3 months to build up a savings history in a bank account.

The Proof: You just need a rental ledger showing on-time payments.

The Minimum Deposit Tier List:

20% Deposit: The “Gold Standard.” You pay $0 LMI and get the lowest interest rates.

8-10% Deposit: The “Safe Zone.” Covers your 5% deposit + costs. You will likely pay LMI.

5% Deposit (Government Scheme): The “Fast Track.” Eligible buyers can purchase with just 5% and pay $0 LMI (now with unlimited spots available!).

Important: Even if you use a 5% deposit, costs like Stamp Duty cannot be borrowed. You must have cash ready for these fees (unless you qualify for a waiver).

Your borrowing capacity is the absolute ceiling of your property budget.

It is the maximum amount a bank will lend you based on your income, expenses, and current debts.

Why does this matter?

If you don’t know your limit, you risk falling in love with a home you simply cannot buy.

A quick personal story:

When I bought my first place, I set a mental budget of $450,000 – $500,000. I spent months on realestate.com.au looking at 3-bedroom houses on the Gold Coast.

I finally called a broker, confident in my plan. The reality check was brutal.

Because of my income and small deposit, the bank would only lend me $297,000.

I was shattered. I had to pivot from a house with a yard to a smaller apartment in the outer suburbs.

The Lesson:

Don’t shop blind. Find your borrowing capacity first to save time and align your expectations with reality.

How to boost your borrowing power

If your number is lower than you hoped, don’t panic. Here are proven ways to increase it:

Slash Credit Card Limits: Banks assess your limit, not your balance. A $10,000 card limit can reduce your borrowing power by up to $50,000. Close them or reduce the limit to the bare minimum.

Declare All Income: Don’t minimize your earnings to save on tax. Lenders need to see every dollar of overtime, bonuses, and allowances to maximize your loan size.

Split the Load: Buying with a spouse or partner allows you to combine incomes and split living expenses, significantly boosting your serviceability.

Clean Up Your Credit: Pay off any defaults and ensure your credit score is healthy. A clean file gives you access to more lenders.

Shop the Right Lender: This is our secret weapon. Borrowing capacity can vary by $50,000 to $100,000 between different banks because they all calculate “living expenses” differently.

Lenders Mortgage Insurance (LMI) is a one-off fee banks charge when your deposit is less than 20%.

Think of it as an “insurance policy” for the bank—it protects them if you default, but you pay the premium.

LMI Cost Reality (2026 Estimates):

LMI isn’t cheap. It is calculated based on your loan size and deposit percentage.

For a standard home buyer purchasing a $600,000 property with a 10% deposit:

Loan Amount: $540,000

Estimated LMI Cost:$10,000 – $14,000

You usually don’t have to pay this upfront. Most lenders will “capitalise” it (add it) to your loan, meaning you pay it off over 30 years with interest.

Can I avoid LMI?

Yes! Apart from saving a full 20% deposit, there are two major “cheat codes” to bypass this fee:

1. The "Professional" Waiver

Certain high-income professions are statistically lower risk. If you work in these fields, you can often borrow up to 90% or 95% of the property price with $0 LMI:

Aside from your deposit and LMI, there is a minefield of “hidden costs” that can derail your budget if you aren’t prepared.

If you know what they are now, you can factor them into your savings plan and avoid a nasty surprise at settlement.

Here are the main ones you need to budget for:

1. Government Fees

The government always finds a way to squeeze in a few extra fees.

Mortgage Registration Fee: In Queensland, this is currently $224 (2025/26 financial year). It pays for the government to register the mortgage on the property title.

Transfer Fee: This covers the cost of transferring the title from the seller to you. On a $600,000 home, you should budget approximately $1,700.

2. Stamp Duty (The Big One)

Good news for 2026: If you are a first home buyer in Queensland, you currently pay $0 Stamp Duty on established homes up to $700,000.

Buying a brand new home? The concession caps are even higher (sometimes unlimited!).

Not a first home buyer? Stamp Duty is a major cost. On a $700,000 existing home, an investor or second-home buyer would pay around $24,000.

You need a solicitor to review your contract, run title searches, and handle the settlement.

Budget:$1,300 – $2,200.

Tip: Don’t just pick the cheapest option. A good solicitor can save you thousands by spotting issues in the contract or strata report before you sign.

4. Building & Pest Reports

This is the best “insurance” you will ever buy. It has saved us from buying absolute dumps that looked perfect on the surface.

Budget:$500 – $700 for a combined Building & Pest inspection.

Tip: If the report finds major structural issues or termites, you can often use it to negotiate the price down—or walk away entirely.

5. Strata / Body Corporate Fees

If you buy an apartment or townhouse, you will pay quarterly fees to maintain the complex (pool, gardens, insurance).

Important: Before you buy, get a Strata Report. Check the “Sinking Fund” balance. If it’s empty and the roof needs replacing next year, you will be hit with a “Special Levy” that could cost thousands.

6. Council & Water Rates

Once you own the home, you pay the council rates.

Budget:$2,000 – $3,000 per year depending on your council (e.g., Brisbane City Council vs. Gold Coast).

7. Home & Contents Insurance

Critical Rule: You must have insurance effective from 5:00 PM on the day you sign the contract. Do not wait until settlement!

If the house burns down the day after you sign, you are generally liable.

Hunter Galloway Client Perk: We work with Allianz to provide our clients with 90 days of free cover until settlement to keep you protected.

8. Moving Costs

Don’t forget the physical cost of moving your life!

Local Move:$1,200 – $2,500 for a standard 3-bedroom house.

Interstate Move:$4,000+ depending on distance and volume.

By now, you are probably realizing that buying a home involves some serious upfront cash.

The good news? You don’t need to win the lottery to get there.

If you implement just a few of these high-impact strategies, you can supercharge your deposit and get into your home sooner.

1. Attack the "Micro-Costs"

When I was saving, I became laser-focused on where my daily cash was leaking. I don’t want you to live on 2-minute noodles, but subtle swaps add up fast.

Lunch: Swap the $25 café lunch for leftovers. (Save $125/week)

Caffeine: Ditch the $6 barista oat latte and brew at home. (Save $30/week)

Socializing: Swap dinner dates for coffee catch-ups or beach walks. (Save $100+ per outing)

Parking: Park 10 minutes away and walk. It’s free exercise and keeps $20 a day in your pocket.

Result: These small tweaks alone can free up an extra $200 to $300 per week. That is $15,000 a year!

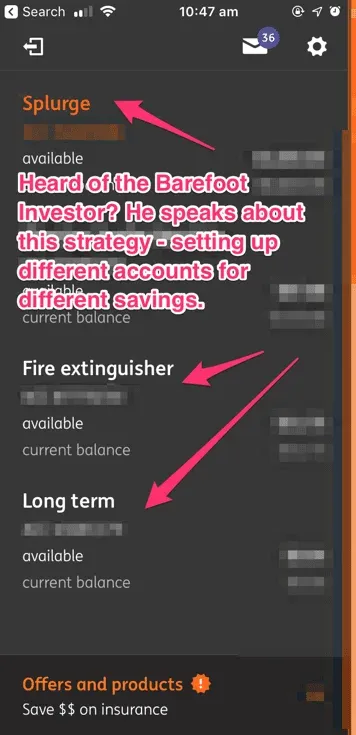

2. The "Buckets" Strategy

Don’t just dump everything into one account. It is mentally easier to save when you separate your money.

Open a dedicated High-Interest Savings Account strictly for your house deposit.

Label it “My First Home” (psychology works!).

Automate it: Set up a transfer the day you get paid so you never see the money.

Pro Tip: Keep a small separate “Sanity Fund” for holidays or treats. If you deprive yourself 100%, you will burn out before you reach your goal.

In the current 2026 market, the answer is a resounding YES.

If you are going to an auction, pre-approval is mandatory because auction purchases are unconditional—there is no cooling-off period.

But even for private sales, a pre-approval is your golden ticket. It tells real estate agents you are a serious buyer who can move fast.

Why you shouldn't "wing it":

Risk of “Deposit Disaster”: Imagine winning an auction, paying a $20,000 non-refundable deposit, and then having the bank reject your loan on Monday morning. You would likely lose that $20,000 instantly.

Speed Wins: In a competitive market, the buyer with their finance sorted usually wins the deal over the buyer who “needs to check with their bank.”

Budget Confidence: It gives you a hard limit so you don’t waste time looking at homes you can’t afford.

The Golden Rule: Never bid at an auction without a written pre-approval in your hand.

The First Home Super Saver Scheme is designed to help you speed up the time it takes to save a deposit towards buying your first home.

The First Home Super Saver Scheme (FHSSS) is essentially a “Government Hack” that lets you save for your deposit using your superannuation fund.

Because super is taxed at a lower rate (15%) than your regular income (which can be up to 45%), you can save thousands of dollars in tax and boost your deposit faster.

How it works in 2026:

You make voluntary contributions to your super fund (like salary sacrifice). You can then apply to withdraw these funds—plus associated earnings—to buy your first home.

The Limits:

Yearly Cap: You can contribute up to $15,000 per financial year.

Total Cap: You can release a maximum of $50,000 in contributions across all years.

Am I eligible?

To use the FHSSS, you generally need to meet these criteria:

Age: You must be 18 years or older.

History: You have never owned property in Australia before.

Intent: You must plan to live in the property for at least 6 months within the first 12 months of buying it.

Important Tax Note – When you withdraw the money, the ATO will withhold a small amount of tax (your marginal rate minus a 30% offset). This typically leaves you much better off than saving in a standard bank account.

BONUS: The Pros And Cons Of Buying With A Small Deposit

Is it better to jump in now with a 5% deposit or wait until you have 20%?

There is no “perfect” answer, but there is a clear cost to waiting.

The Pros: Why buying sooner wins

The biggest advantage is simply getting into the market.

If you wait to save a bigger deposit, property prices often rise faster than you can save.

Real-Life Example (Albany Creek, QLD):

We helped a couple buy a home in Albany Creek three years ago for $750,000.

They had a small 5% deposit and paid Lenders Mortgage Insurance (LMI).

Fast forward to 2026, and we revalued that property at over $1.1 million.

The Result: They made $350,000 in capital growth.

If they had waited three years to save a “perfect” 20% deposit, the house would have been out of reach. They would have needed to save an extra $100,000 just to keep up with the price rise!

The Cons: What to watch out for

Buying with a small deposit does come with some downsides:

Lenders Mortgage Insurance (LMI): If you don’t use a government scheme, LMI can cost anywhere from $10,000 to $30,000. This is “dead money” that protects the bank, not you.

“Risk Pricing” on Interest Rates: Banks often charge higher interest rates for risky loans.

Deposit > 20%: Lower rate (e.g., ~5.79%)

Deposit < 10%: Higher rate (e.g., ~6.29%)

This small difference adds up to hundreds of dollars a month in extra interest.

Stricter Property Rules: With a small deposit, banks are pickier. They may refuse to lend on small apartments (under 40sqm) or properties in high-density postcodes because they are seen as higher risk.

The Verdict?

You can often bypass these “Cons” completely.

By using the Government 5% Deposit Scheme (now with unlimited places!) or a Parental Guarantor, you can buy with a small deposit without paying LMI or higher interest rates.

Expert Tip: Don’t guess which option is best. Speak with our team to compare the cost of “buying now” vs “waiting.”

Deposit Calculator Frequently Asked Questions

Can I use a personal loan for my house deposit?

Generally, no. Most major lenders in Australia do not accept borrowed funds like a personal loan for a deposit because it increases your debt level and risk. However, some specialist lenders may allow it if you have a high income, but you will typically pay a much higher interest rate. A better alternative is often a gifted deposit from family or using a Guarantor Loan.

Is the deposit I pay to the real estate agent refundable?

It depends on which deposit you mean:

The Holding Deposit: Yes, the initial “expression of interest” deposit (usually $1,000) is typically fully refundable if you do not sign a contract.

The Contract Deposit: No. Once the contract goes unconditional (after cooling off), the full deposit (e.g., 5-10%) is not refundable. If you back out, you lose this money.

Does rent assistance or a cash gift count as "Genuine Savings"?

Rent Assistance: No, government benefits generally do not count as genuine savings.

Rent Payments:Yes. Many lenders now accept 12 months of rental history (showing on-time payments) as proof of genuine savings instead of cash in the bank.

Cash Gifts: A cash gift is usually considered “non-genuine savings.” Most banks will still require you to hold at least 5% of the purchase price in your own name for 3 months, unless you are using a specific “non-genuine savings” loan product or a Guarantor.

Is $30,000 enough for a house deposit?

Yes. Under the Australian Government 5% Deposit Scheme, $30,000 is a full 5% deposit for a $600,000 home. Without the government scheme, $30,000 is still a valid 5% deposit for a $600k property, but you would need to budget extra funds for Lenders Mortgage Insurance (LMI) and Stamp Duty (if not waived).

How much do I need to earn to borrow $800,000?

In the 2026 market (with interest rates around 6%), a single applicant or couple typically needs a combined annual income of roughly $180,000 to $200,000 to borrow $800,000. This assumes you have no other large debts (like car loans) and average living expenses. .

How do you calculate your deposit?

The formula is: Purchase Price × Deposit Percentage.

Example: $500,000 × 0.10 (10%) = $50,000.

Don’t Forget: You must add “transaction costs” (Stamp Duty + Legal Fees) on top of this figure to get your Total Required Savings.

How much deposit for a $500,000 house in Australia?

5% Deposit (Minimum): $25,000 (Plus LMI costs, unless using a Government Scheme).

10% Deposit (Standard): $50,000 (Reduced LMI).

20% Deposit (Ideal): $100,000 (No LMI + lower interest rate).

What is the 20% deposit of $950,000?

A 20% deposit on a $950,000 home is $190,000. By paying this amount, you avoid Lenders Mortgage Insurance (LMI) entirely. However, you should also budget for Stamp Duty, which on a $950k property can be significant depending on your state.

Can I buy a house with a $10,000 deposit?

It is difficult, but possible in two specific scenarios:

Shared Equity / Help to Buy: Some government schemes allow eligible buyers (like single parents) to buy with a 2% deposit. On a $500,000 home, that is just $10,000.

Guarantor Loan: If your parents act as guarantors, you can borrow 100% of the purchase price + costs, meaning you technically need a $0 deposit (though having some savings is always safer).

Next Steps And Getting Your Home Loan.

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one person operations, we havean entire team of experts dedicated to help make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment onlineto see how we can help.

Our team of home loan experts is here to help you buy a home in Australia

Note: The information provided in this article is intended to provide illustrative examples based on stated assumptions and your inputs. Calculations are meant as estimates only, and it is advised that you consult with a mortgage broker about your specific circumstances

Why Choose Hunter Galloway As Your Mortgage Broker?

Mortgage Broker of the Year

in 2017, 2018 and 2019

The highest rated and most reviewed

Mortgage Broker in Brisbane on Google

97% loan approval rate

across all applications we processed, 2024–2026

We have direct access to 30+ banks

and lenders across Australia

We promise to get back to you within 4 business hours

![How much deposit do I need for a home loan?]](/api/media/file/deposit-calculator-8.webp)