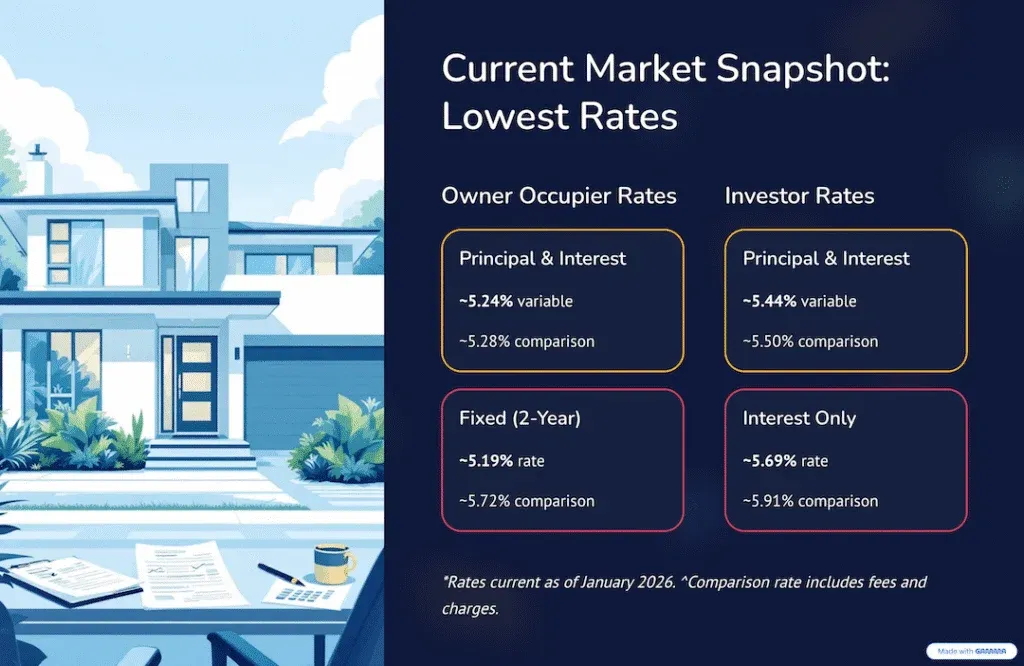

To understand where interest rates are heading in 2026, we must first look at the road behind us. The last 12 months have finally provided some relief to Australian households, but the recovery journey is far from over.

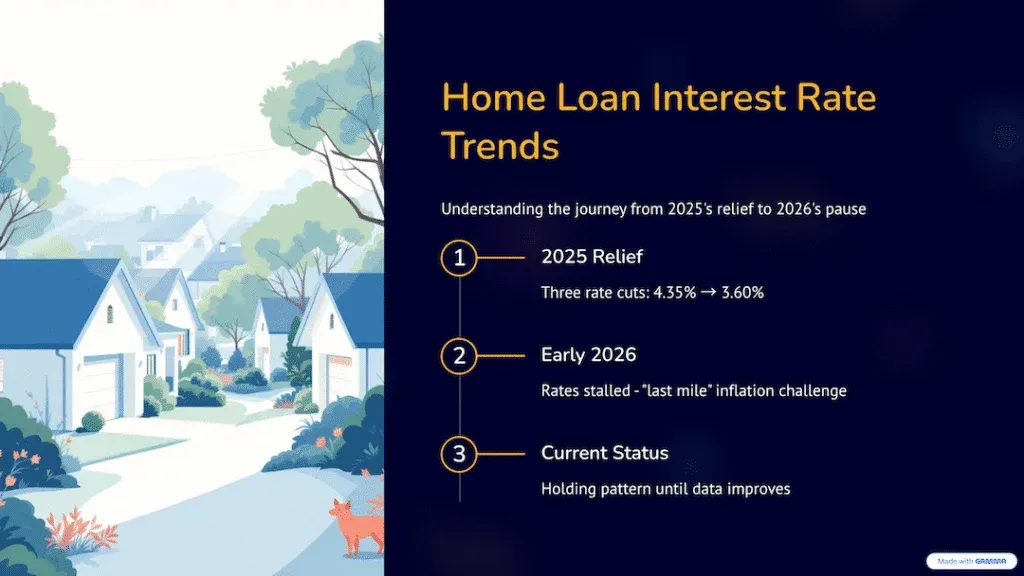

2025 marked a significant turning point as the tide finally turned for borrowers. After the Reserve Bank of Australia (RBA) held the cash rate at a painful 4.35% for an extended period, they finally shifted gears to support the economy.

We witnessed three distinct rate cuts throughout the year, which signaled a major change in monetary policy. These strategic moves successfully brought the official cash rate down from its peak of 4.35% to 3.60%.

Fortunately, most lenders passed on these savings to customers, giving homeowners some much-needed breathing room. This reduction helped lower monthly repayments for thousands of families across the country.

However, the consistent downward trend we enjoyed has hit a noticeable speed bump in early 2026. Economists refer to this challenge as the “last mile” problem in the fight against inflation.

Reducing inflation from its peak of 7% down to 4% was relatively straightforward for the central bank. But crushing that final percentage to get back inside the RBA’s strict 2–3% target band is proving to be much more difficult.

Prices for essential services—such as insurance premiums, rent, and medical costs—remain stubbornly high. Consequently, the RBA has hit the pause button to ensure that inflation does not reignite before they cut further.

We are currently in a calculated holding pattern until economic data improves. The aggressive series of cuts we saw in 2025 is likely finished for the time being.

Future interest rate movements now depend entirely on the quarterly inflation data released by the ABS. If inflation remains sticky, rates will stay put, but if it cools down, the cutting cycle could resume later this year.