Removing A Guarantor from Mortgage – Ultimate Guide

Loan approval rate of 97%*

Variety of options due to direct access to 30+ Australian banks & lenders

Highest-rated Mortgage Broker in Brisbane — 2,400+ Google reviews

Free for you, and you won't pay more — the lender pays us

35+Years of

experience

Based on

2,400+ reviews

Mortgage Broker of the Year in 2017, 2018, 2019 and 2024

Access to 30+ banks and lenders in Australia

Thousands of families helped into their homes

*Based on all applications processed through Hunter Galloway, 2024–2026.

Removing A Guarantor from Mortgage – Ultimate Guide

Removing a guarantor is one of the final steps to gaining full financial independence — but knowing when and how to do it can be confusing. Whether your property has grown in value, your income has improved or your guarantor needs to access their own equity, there comes a time when the guarantee must come off.

In this guide, written by an expert mortgage broker in Brisbane, we’ll show you exactly how to remove a guarantor from your home loan — even if you’re not quite at 80% LVR yet.

How Long Does A Guarantor Stay On A Mortgage

According to DFA, The bank of Mum and Dad is officially Australia’s ninth-largest lender and has about $34 billion in loans, making it bigger than HSBC, AMP and Bank of Queensland. Over 60% of first home buyers in Australia are getting financial help from their parents either through gifts or as guarantors on loans.

The way the banks see it, your guarantor is being placed onto the loan for the entire 25 to 30-year loan term and will continue until the bank approves your request to remove it. This is the default setting for guarantor loans.

In other words, if you did nothing after your loan was settled, your parents’ property would guarantee your loan until you either sell your home or pay it off in 25 to 30 years’ time.

The bank of Mum and Dad is officially Australia’s 9th largest lender.

When Can You Remove A Guarantor From A Loan?

Realistically you should aim to remove the guarantor within 5 years or once you are in a financial position to remove it. But this comes down to your personal situation—how quick you have been able to pay down the guarantor portion and your property’s value.

Overall the best time to remove a guarantor is when you owe under 80% of your property’s value. This is done for the following reasons:

You avoid Lenders’ Mortgage Insurance fees and could save thousands

You could qualify for better interest rate discounts

The process involves less paperwork

Being able to remove the guarantor usually comes down to how much you owe.

An example of 80% LVR

For example, if you initially borrowed $420,000 which is a Loan To Value Ratio (LVR) of 105% (because it included stamp duty, settlement fees and other costs), on a $400,000 purchase, and you have since paid down the loan to $320,000, you can now refinance your loan because the LVR is 80%.

On the other hand, if you had only paid the loan down from $420,000 to $405,000 but your property value had increased to $450,000 you could still refinance with a 90% LVR loan but you will need to pay lenders mortgage insurance (LMI) which is a one-off premium charged by the lender to protect the lender. LMI is compulsory if you are borrowing with an LVR of more than 80%. For that reason, we recommend waiting to remove your guarantor until your LVR is under 80%.

When You Must Remove A Guarantor (Even If You’re Not Ready)

Most borrowers plan to remove their guarantor once their property reaches 80% LVR. However, sometimes life throws a curveball and you are forced to act sooner than expected. Below are the most common situations where the guarantor must be released immediately, even if you don’t feel financially ready.

Situations That Trigger a Mandatory Guarantor Release

They want to sell or refinance their own property. The bank will not allow the sale or refinance while part of the property is tied to your loan. You’ll need to refinance or reduce the guaranteed amount.

There is a divorce or separation. This applies to either you as the borrower, or the guarantors themselves. The guarantee cannot stay in place when ownership or liability changes.

The guarantor becomes seriously ill or passes away. In this case, their estate becomes liable for the guarantee. It’s best to act quickly to avoid legal or family complications.

Their borrowing capacity is being affected. Many guarantors struggle to get their own loan approved because the bank still counts your guarantee as a liability against them.

What To Do If You’re Forced to Remove the Guarantor

If one of these scenarios applies, you have a few options:

Refinance into your own name if your equity position is strong enough.

Request a reduced guarantee amount if you are close but not quite at 80% LVR.

Use a term deposit guarantee instead of a property guarantee as a temporary solution.

Seek legal advice if the guarantor is undergoing separation or estate issues.

The key is not to panic.

We help clients through this situation all the time. Even if you don’t qualify for full removal today, there is usually a plan B that keeps everyone protected. Let us know your scenario and we’ll guide you through the cleanest exit path.

What Happens If You Can’t Remove the Guarantor Yet? (Plan B Options)

Not quite ready to remove your guarantor? Don’t stress — there are still smart strategies you can use to reduce their liability while working your way towards full independence.

Here are your best Plan B options if your lender says “not yet”.

Option 1: Ask to Reduce the Guaranteed Amount

Even if you can’t remove the guarantee completely, most banks allow you to scale it down. For example, instead of guaranteeing 100% of the shortfall, you could request the lender to limit the guarantee to a smaller portion, such as $50,000–$80,000. This gives your guarantor more flexibility, and it’s easier to remove later.

Option 2: Make Extra Repayments or Lump-Sum Contributions

Fast-track your exit by paying down the loan faster.

You can:

Increase your regular repayments

Put tax refunds or bonuses straight into the loan

Use offset accounts to reduce interest and increase equity

Even an extra $200 per month can shave months or years off your guarantor obligation.

Option 3: Boost Your Valuation With Renovations

Sometimes your income isn’t the issue — it’s your property value.

You can do small cosmetic upgrades like:

Painting and landscaping

Updating flooring or cabinetry

Converting unused spaces

These upgrades can uplift your valuation enough to hit 80% LVR sooner. We can order a free upfront valuation to check before you spend anything.

Option 4: Switch to a Lender With Better Valuation Policies

Not all banks value properties the same way.

In some cases, another lender may see your property as worth $50k–$100k more, instantly putting you in a stronger position.

We run multi-lender valuation comparisons to find the best outcome — without damaging your credit score.

You’re Closer Than You Think

Even if full guarantor removal isn’t possible today, there’s nearly always a path forward. The key is taking proactive steps now, rather than waiting for the bank to force your hand.

What Are The Steps In Removing A Guarantor From The Mortgage?

The exact process of removing a guarantor from the mortgage varies from bank to bank. But in general, you will need to go through these steps:

1. Contract your mortgage broker to review your financial situation

2. Arrange a bank valuation.

3. Confirm the total loan amount.

4. Make sure you meet the lender’s criteria.

5. Submit a partial release, or internal refinance.

6. Wait 5-8 days for the bank to process.

7. Complete property release or internal refinance.

8. All done, your parents can pick up their title from the bank.

The biggest difference in the process is in step #5: If you have an 80% LVR loan, you can submit a partial release.

If you have a 90% LVR loan, you will need to complete an internal refinance and the loan will be subject to lenders mortgage insurance approval.

More on that below…

Guarantor Removal Eligibility Checklist (Can You Qualify Today?)

Still unsure if you’re ready to remove your guarantor? Use this quick checklist to see if you meet the bank’s minimum requirements. If you can tick most of the boxes below, there’s a good chance you’re already eligible — and we can help you confirm it.

You’ll typically qualify for guarantor removal if:

You have at least 6–12 months of clear repayment history – No late or missed repayments during this period.

Your Loan-to-Value Ratio (LVR) is within the bank’s limit – Most lenders require 80% LVR, while a few allow removal up to 90% (sometimes with LMI).

Your income and employment are stable – Payslips, BAS statements or financials should show consistent earnings.

There are no arrears, declined payments or hardship arrangements on your record.

A bank valuation confirms your property is worth enough to stand on its own.

What Are The Fees Involved In Removing A Guarantor?

Banks will charge some administrative, and possibly government fees to remove the guarantor. But these are usually under $500, provided you aren’t paying lenders mortgage insurance.

The good news, is some banks are offering up to $4,000 in refinance cash backs which can help offset any costs in removing your parents guarantee, contact our brokers today to see if you are eligible.

Your mortgage broker can help you remove a guarantor from your loan.

Your bank will let you know if there are any other application or valuation fees involved.

Removing a Guarantor from Mortgage with an 80% LVR loan

Removing a guarantor with an 80% LVR is great because you will avoid paying a Lenders Mortgage Insurance (LMI) premium. LMI can run into the tens of thousands of dollars so, if you can avoid paying it then that’s good.

Different banks charge different fees to release your mortgage.

Here’s exactly how it works:

Your loan repayments need to have been made on time and be up to date for the last 6 months.

Your loan must be less than 80% LVR.

Your income, employment and credit history need to meet the bank’s current policy. Remember, every time you look to remove the guarantee, you are doing an application with the lender, so they’re going to assess you based on your income as of application day.

The bank will complete a valuation on your home.

From here, different banks have different processes.

For example, St George Bank can complete the valuation and then remove the guarantor without changing your loan structure by doing a partial release.

On the other hand, other banks like CBA who set up guarantor home loans as two separate loan accounts will need to internally refinance your home loan to remove the guarantor.

If this is all sounding too hard, don’t worry give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Removing a Guarantor from Mortgage with a 90% LVR home loan

The initial steps and process in removing a guarantor with a 90% LVR home loan are similar to the ones above However, by removing a guarantor with a 90% home loan you are effectively refinancing and removing the guarantee.

Here’s exactly how it works:

Your loan repayments need to have been made on time and be up to date for the last 6 months.

Your loan must be less than 90% LVR.

Your income, employment and credit history need to meet the banks, and LMI current policy.

The bank will complete a valuation on your home.

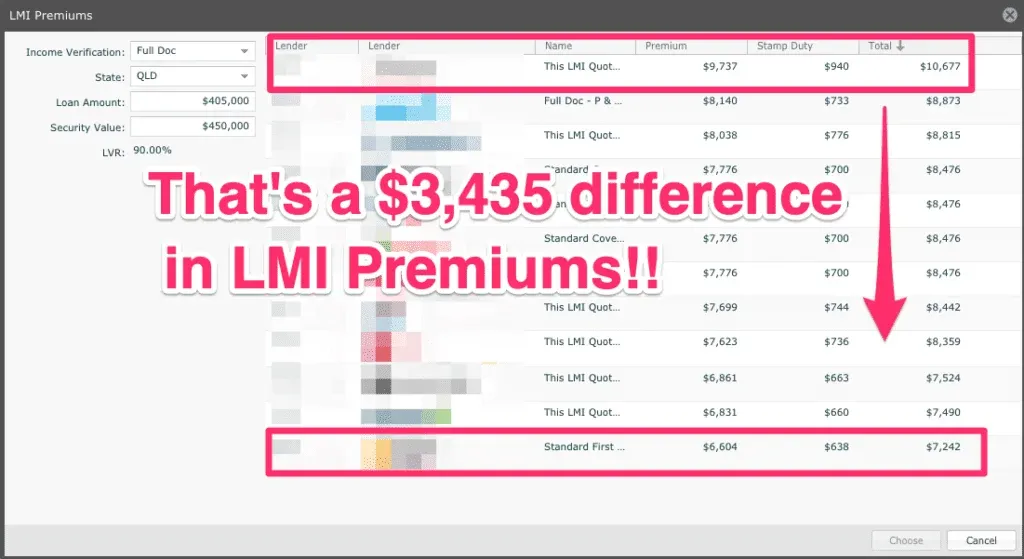

The biggest problem we see at this stage is that different banks will value homes at different amounts. We have seen up to a $130,000 increase in valuations on the same property by different banks.

At Hunter Galloway, we can order an upfront valuation with more than one lender to help you find the lender with the highest property valuation.

The second item to be aware of is that different banks also charge different Lenders Mortgage Insurance premiums.

In the same example, if you were refinancing the $405,000 against a property that was valued at $450,000 you could pay as little as $7,242 in Lenders Mortgage insurance or as much as $10,677, depending on your lender!

In this situation, there is a $3,435 different in LMI costs between banks!

That’s a $3,435 difference in Lenders Mortgage Insurance premiums. It definitely pays to look around and we can help you do that.

Again if this is all sounding complicated, don’t worry give us a call on 1300 088 065 or get in touch online to see how we can help.

When Will I Have To Pay Lenders Mortgage Insurance?

Lenders Mortgage Insurance needs to be paid if the value of your mortgage is over 80% of your property’s value. So, If you have less than 20% equity in your home you will need to pay lenders mortgage insurance.

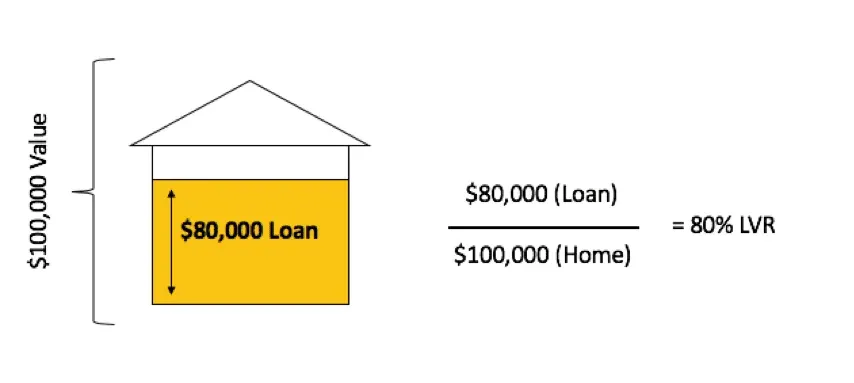

To calculate your LVR, or Loan to Value Ratio just divide your loan amount by your estimated property value.

For example, if you owe $405,000 to Commonwealth Bank and your home is worth $450,0000:

$405,000 / $450,000 = 0.90

0.90 x 100 = 90% LVR

In this case, you would need to pay lenders mortgage insurance.

On the other hand, if you owe $360,000 to Commonwealth Bank and your home is valued at $450,000:

$360,000 / $450,000 = 0.80

0.8 x 100 = 80% LVR

In this case, the LVR is equal to 80% so you do not need to pay Lenders Mortgage Insurance.

What If My Guarantor Situation Changes And I Have To Remove Them?

Keep in mind that your parents or relatives have done you a massive favour by providing their guarantee and helping you into the property market. So, it’s good to remove them as soon as possible because having their guarantee in place can hold back their future plans.

For example, they might not have enough equity to purchase an investment property with the guarantee in place or you might have a brother or a sister who will also need a guarantor.

Can My Guarantor Sell Their Home?

They can. But, you must keep in mind that there is a second mortgage registered on their property. So, when they sell their home, that second mortgage either needs to be paid out by the guarantor or you’ll need to refinance your property so that you can add that second mortgage back onto your property.

However, if your guarantor is selling their property just after you have set them up, you might not have enough equity in your property to refinance your loan.

While it is possible to place a portion of the sale proceeds as a term deposit during the time your guarantor is looking for a new home, it all comes down to your individual situation which we can discuss with you.

Give us a call on 1300 088 065 or get in touch online to see how we can help.

This situation where your guarantor wants to sell their home is tricky and we recommend you chat to us before they list their home.

Can I Sell My House If I Have A Guarantor Loan?

Absolutely. Once again, remember that if you have borrowed 100% of the purchase price and you under-sell your property, the remainder will be left on the guarantee’s property. So, make sure your selling price covers the full debt.

What Happens If I Get Divorced And Have A Guarantor Home Loan?

We can look at refinancing your guarantor home loan to remove one of the borrowers and have you as the only owner and borrower on the home loan while leaving the existing guarantee as is .

It is also possible to refinance your existing guarantee with a new guarantor as well.

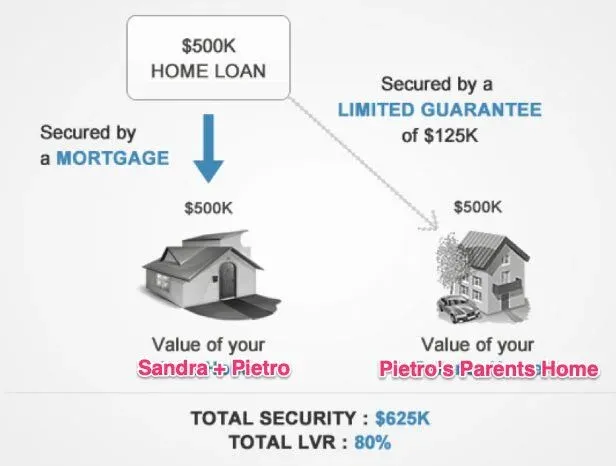

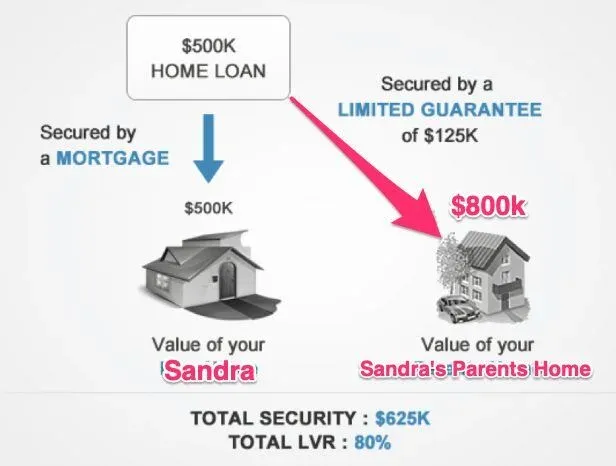

Case study: Sandra and Pietro bought their home with the assistance of Pietro’s parents. They have gotten divorced, and Sandra is going to get the property as part of the separation.

Sandra not only needs to remove Pietro from the loan and title, but also needs to refinance Pietro’s parent’s guarantee.

Fortunately, Sandra’s parents are happy to go on as new guarantors, so she completes a refinance to remove Pietro and his parents, and add Sandra’s parents on.

Sandra’s parents’ home is worth more than Pietro’s parents home, but this doesn’t matter as the limited guarantee of $125k is removed from Pietro’s parents home, and put onto Sandra’s parents home.

If you need to pay out your ex or are needing to refinance your home loan after a divorce contact us on 1300 088 065 and we can assist with removing your guarantee.

Case Study: Using A Parents’ Home As A Guarantor In 2025

Thomas used his parents’ home as a guarantee for his own loan instead of paying a deposit. After 3 years, Thomas’ property has increased significantly, and he can now refinance using his property equity to remove the guarantor.

Home value 2022: $700,000

Initial home loan (including guarantor): $700,000

Initial LVR: 100%

We ordered a bank valuation for Thomas in 2025, and his home was valued at $820,000. This allowed him to refinance and remove the guarantor with the same bank with minimal paperwork.

Current home value 2025: $820,000

Current home loan (including guarantor): $656,000

Current LVR: 80%

With his LVR reduced from 100% to 80%, Thomas was able to qualify for better interest rate discounts and lower overall loan repayments.

BONUS: 3 Pitfalls To Avoid With Guarantor Home Loans.

Before you set up a guarantor loan — or if you already have one — it’s important to understand the risks. Many families run into problems not because of anything they did wrong, but because of how the bank structures the guarantee behind the scenes.

Here are the three biggest pitfalls to watch out for.

Pitfall 1. Standalone vs Cross-Collateralised Guarantees

Not all guarantor loans are set up the same way. There are two methods lenders use when securing the guarantee:

Standalone Guarantee (Best Option)

Example: You’re buying for $800,000

$640,000 (80%) is secured against your property

$160,000 (20%) is secured against the guarantor’s property

Once you pay down the guaranteed portion, the guarantor is released

This setup is clean, transparent and easy to exit.

Cross-Secured Guarantee (Risky Setup)

Some lenders don’t separate the securities. Instead, they link both properties together behind the scenes. You may think your guarantor is only guaranteeing $160,000, but in reality, they could be tied to $200,000 or more.

Even worse — when you try to remove them, the bank may revalue your home and ask for more repayments than expected.

Always ask your lender or broker whether the guarantee is standalone or cross-collateralised, and whether the bank adds a buffer over 20%.

Pitfall 2. Hidden Encumbrances (A Silent Loan Killer)

Even if the guarantor believes their property only has one loan, there may be other charges hidden behind it — especially if they own multiple properties with the same bank.

We recently helped a client whose guarantors thought they had one $800,000 loan secured against their property. A quick title search showed only one mortgage, so everything looked fine.

But at settlement, the bank revealed there was actually a $1,000,000 priority notice tied to the property — meaning their equity was already locked up elsewhere.

The result? The guarantor loan collapsed, because there wasn’t enough available equity.

Lesson: Before signing anything, make sure:

The guarantor requests a full security summary from their bank

All other properties or loans are disclosed

The guarantee is not cross-secured with any other loan

Pitfall 3. Guarantor Wants to Sell or Retire — But Can’t

Many guarantor loans run for 30 years, but parents or relatives may want to sell or downsize sooner.

Here’s the issue:

If the guarantor sells before being released, the bank will hold the guaranteed amount from their sale proceeds

Example: They sell for $800,000, but $160,000 is locked in a term deposit until you refinance or remove the guarantee

So instead of walking away with $800,000, they only get $640,000 in hand.

If your guarantor is planning to retire or sell in the next few years, talk to your broker early. A revaluation or refinance may allow you to release them before they sell.

Key Takeaway

Most of these issues can be avoided before settlement — but once the documents are signed, they’re harder to unwind. If you’re unsure how your guarantor loan is structured, we’re happy to review your setup and check for hidden risks.

Bonus: Buying A House With A Friend

Many first-home buyers or investors consider buying property with a friend or partner. However, one common mistake is entering a jointly and severally liable loan.

This type of loan means that if your co-buyer can’t or won’t pay their share, the bank can hold you responsible for the full mortgage. In the worst-case scenario, the bank could repossess the property, and a default could be listed on your credit file. A default can affect your borrowing capacity for up to 7 years.

How Property Share Can Help

A safer option is a Property Share arrangement. Property Share allows you to split the cost of buying a home with friends or family while keeping control over your own finances.

Key points of Property Share:

All borrowers own the property jointly and guarantee each other’s loans

A maximum of 2 home loan applications per property is allowed, but each application can include multiple loan products (e.g., split loans)

You can manage repayments individually while benefiting from collective ownership

Benefits of Property Share

Faster deposit savings: Pooling funds reduces the time it takes to save a deposit. The average deposit savings period is now 11.4 years.

Higher borrowing power: Combined income allows you to afford a larger or better property than buying alone.

Flexible finances: You maintain control over your own repayment strategy.

Access to loan features: You can still use redraw facilities, offset accounts, and lines of credit.

Get Expert Advice

Before buying a property with friends or family, it’s essential to talk to a mortgage broker. A broker will help you choose the right loan structure and avoid future financial risks.

FAQs About Removing A Guarantor From Mortgage

Can I remove a guarantor without refinancing my entire loan?

Yes — if your LVR is below 80%, most banks allow a partial release where only the guarantor portion is removed without restructuring your loan.

What happens if my guarantor dies before I remove them?

Their estate remains liable for the guarantee until the loan is refinanced or released. It’s important to act quickly and speak to your lender or broker.

Can a guarantor force me to remove them from the loan?

They can request release, but the bank will only remove them if the borrower meets the lender’s refinance criteria.

Does removing a guarantor affect my credit score?

No — the removal itself doesn’t impact your score, but applying for refinancing generates a credit enquiry.

Can I replace one guarantor with another?

Yes — this is common in divorce or family change scenarios. The loan is refinanced to swap guarantors.

How long does guarantor removal take?

Once approved, the bank typically processes the release within 5–10 business days.

What happens if a guarantor sells their house?

If your guarantor sells the property being used as security, the bank will usually insist on removing or replacing the guarantee before the sale can settle. You’ll either need to refinance the loan in your own name (if your LVR is low enough), reduce the guaranteed amount, or provide a new guarantor. In most cases, the guarantor won’t be able to complete the sale until the bank is satisfied that their security is no longer required.

Speak To Guarantor Home Loan Experts

If you would like to chat about removing your guarantor or arranging a new guarantee, we’d be delighted to help you out, speak with one of our experienced mortgage brokers to walk through the next steps with you.

Unlike other mortgage brokers who are just one-person operations, we havean entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 orbook a free assessment onlineto see how we can help.