Getting ANZ home loan pre-approval is one of the best ways to know exactly how much you can borrow before you start house hunting. It gives you confidence when making offers and shows sellers you’re a serious buyer. In this guide, we’ll break down how ANZ pre-approval works, how long it lasts, and the mistakes that can still lead to rejection — even after you’re approved.

Let’s dive in

Pre Approval Basics

A pre approval is an indication from a bank that they are comfortable lending you a certain amount of money, subject to a couple of terms and conditions.

Different banks call pre approvals by different names., ANZ refers to a pre approval as an Approval in Principle (AIP) or an Approval Subject To (AST). Don’t get confused; all these different terms mean the same thing.

An in principle approval means that the bank is happy to approve your loan provided you meet all of the principles they outline. These usually include a bank valuation, credit and LMI approval.

ANZ Pre-Approval in Principle: What It Means and Why It Matters

Getting an ANZ Pre-Approval in Principle (also called Approval in Principle or pre-approval) is a great first step when buying a home. It gives you an early indication of how much you may be able to borrow — helping you plan your budget and search with confidence.

But not all pre-approvals are created equal. Knowing the difference between a Pre-Approval in Principle and a Fully-Assessed Approval can save you time, stress, and even money down the track.

Let’s unpack what each one means, the benefits, and what to watch out for.

What Is an ANZ Pre-Approval in Principle?

An ANZ Pre-Approval in Principle is a conditional approval that gives you an estimate of how much you could borrow, based on the details you provide.

You can apply online or through an ANZ branch — and in most cases, you’ll receive an instant or same-day result.

However, it’s important to note that this approval is based only on self-reported information. ANZ has not yet verified your payslips, bank statements, or credit report.

That means it’s a guide — not a guarantee. You can use it for early planning but not to make firm offers or bid at auction.

Key Features of a Pre-Approval in Principle

Instant or same-day approval

Based on self-reported income and expenses

No credit check or document verification

Not reviewed by ANZ’s credit team

Useful for budgeting, not for buying

Benefits of Getting ANZ Pre-Approval

While it’s not a final approval, ANZ’s Approval in Principle still offers valuable advantages for buyers:

Confidence when house hunting – You’ll have a clear idea of your borrowing limit.

Valid for 90–180 days – ANZ’s pre-approval remains active for up to six months.

Simple and quick – Apply online and get an answer in minutes.

Helps you plan your next steps – You’ll know your price range before attending open homes or auctions.

This early assessment can make the home-buying process less overwhelming — but you should still confirm your details with a broker to avoid surprises later.

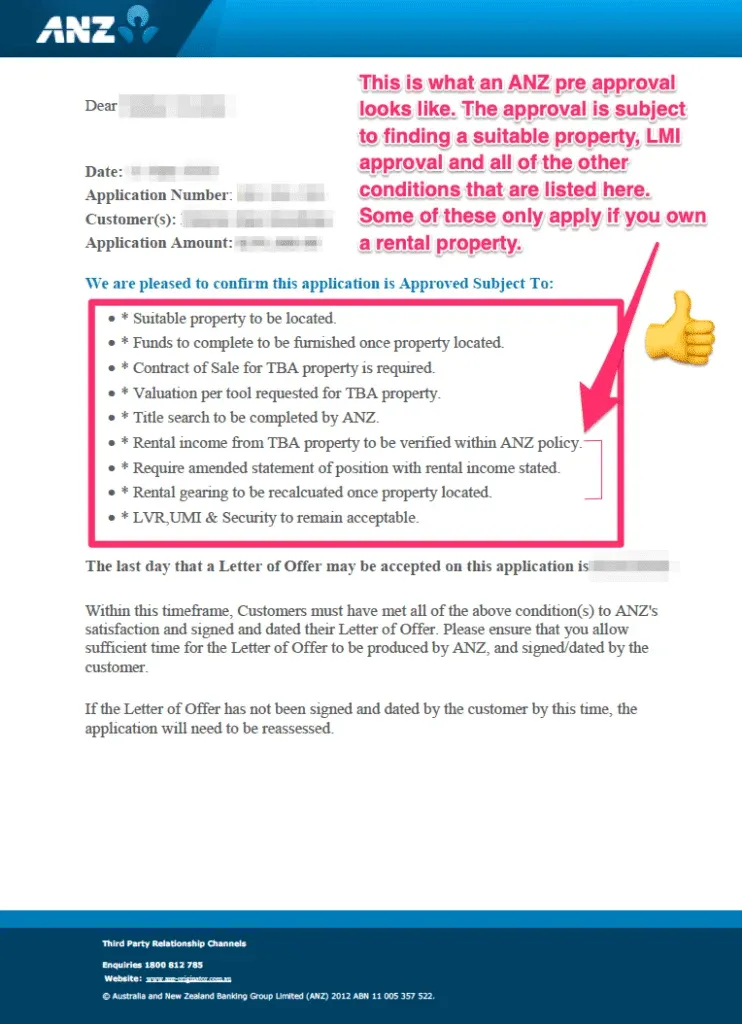

Common Conditions in an ANZ Approval in Principle

Every pre-approval from ANZ comes with a few conditions. These conditions must be met before your loan becomes formally or unconditionally approved.

Typical ANZ conditions include:

Finding a suitable property that meets ANZ’s lending criteria.

Providing proof of funds — showing your deposit and savings.

Submitting a signed Contract of Sale once you’ve found a property.

Property valuation by ANZ’s approved valuer.

Title search to confirm legal ownership.

Rental income verification if you’re buying an investment property.

If your income, debts, or savings change during this time, ANZ may review or even decline your final loan.

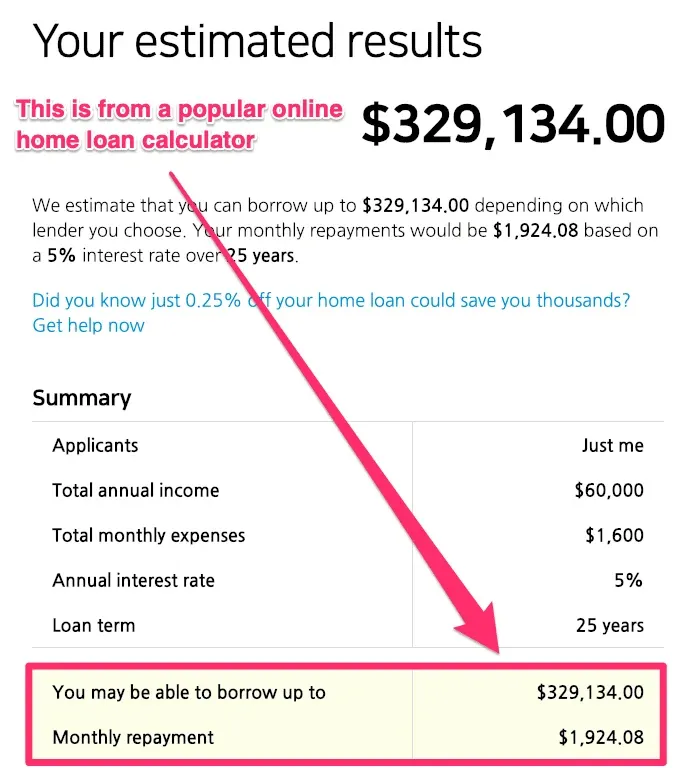

Case Study: The Benefits Of An Approval In Principle

Joanne is single, earns $60,000 per year, and has no credit cards or other loans.

She contacted us last year after missing out on a unit in Brisbane because she didn’t have her finance organised.

A pre approval is more reliable than online calculators.

Based on an online calculator, Joanne thought she could only borrow up to $329,134.

Joanne made an offer on a property at what she thought was the maximum she could borrow. Unfortunately, the vendors knocked back her bid because it was $10,000 under what they were after.

A few days after Joanne had her offer knocked back, she got in touch with Hunter Galloway to arrange an approval.

After running the figures through our calculator, Joanne discovered she could borrow as much as $369,971.

(That’s $40,837 MORE THAN ANZ)

As you can see from the table, different banks lend substantially different amounts.

In Joannes’ case, Westpac could potentially lend her over $20,000 more than ANZ would consider.

These figures fluctuate regularly, but the point is without a pre approval you’ll never know exactly how much a bank is willing to lend you, which means, like Joanne, you may miss out on the perfect property.

But with a pre approval, you can make more competitive offers with fewer days for finance, therefore giving you a better chance of getting your offer accepted.

A Fully-Assessed Pre-Approval (sometimes called a Formal Conditional Approval) goes a step further. Instead of relying on what you input online, ANZ’s credit assessment team manually reviews your full financial situation.

This includes:

Verifying your income with payslips or employer confirmation

Checking your credit file and repayment history

Assessing your living expenses and existing debts

Confirming property details if you’ve found one

Once approved, ANZ confirms that your financial position meets their credit policy — giving you far greater confidence to make an offer

Pre-Approval in Principle vs Fully-Assessed Approval

Feature

Pre-Approval in Principle

Fully-Assessed Approval

Turnaround Time

Instant or 30 mins

1–3 business days

Document Verification

No

Yes

Credit Check

No

Yes

Reviewed by Credit Team

No

Yes

Accuracy

Basic Estimate

Highly Reliable

Validity

Short-Term

90 Days

Suitable for Auctions

No

Conditional Only

Why Fully-Assessed Approval Is Better

A Fully-Assessed Approval offers stronger buying confidence because your application has been reviewed by ANZ’s credit specialists, not just a computer.

This means:

You’re far less likely to be declined later.

Real estate agents will take you seriously.

You can make an offer with peace of mind.

In contrast, a Pre-Approval in Principle is ideal for early budgeting but not for major commitments like bidding at auction or signing contracts.

Can You Use ANZ Pre-Approval in Principle at Auctions?

No. You should never bid at auction with only a Pre-Approval in Principle.

Because ANZ hasn’t verified your documents or credit report, your actual borrowing capacity might differ from the estimate. If the figures don’t match — or the property doesn’t meet ANZ’s lending criteria — the bank could decline your application after the auction.

If you’re serious about bidding, always upgrade to a Fully-Assessed Approval first.

What About ANZ’s Buy Ready Service?

ANZ’s Buy Ready service gives quick property value estimates and market insights — perfect for research and comparison.

However, these tools don’t replace full property market research.

At Hunter Galloway, we go one step further by providing CoreLogic RP Data reports — trusted by banks and backed by verified sales data — so you can make informed property decisions with confidence.

Why It’s Better to Work With a Mortgage Broker

When you apply directly through ANZ’s online system, you’ll often get a computer-generated pre-approval that hasn’t been checked by a real credit assessor.

Working with a mortgage broker like Hunter Galloway means:

Your application goes directly to ANZ’s credit team for full review.

You get accurate borrowing figures based on verified data.

You can compare 30+ lenders to find the best fit for your situation.

We make sure your pre-approval is real, reliable, and auction-ready — giving you confidence to buy safely.

Key Takeaways

ANZ Pre-Approval in Principle is fast but not guaranteed.

Fully-Assessed Approval provides stronger confidence and smoother progress to full approval.

Always check whether your approval has been reviewed by ANZ’s credit team — not just a system.

The documents required for an approval in principle are more or less the same as those required for unconditional approval. So whether you are buying a home or applying for a pre approval, you’ll need to get together the following for ANZ to complete their assessment:

A completed ANZ Home Loan Application form (our brokers help you with this)

Identification documents, like a driver’s licence or Australian passport

If you are employed full-time or part-time—One most recent payslip (no more than 60 days from the date of the signed application form) plus evidence of income credited to a transaction account for the last 3 months.

If you are self-employed—Income evidence is required in the form of copies of personal and all associated company/trust/ partnership tax returns for the most recent financial year, accompanied by ATO assessment notices (most current year’s figures no more than 18 months old)

Copy of bank statements or accounts showing your deposit funds.

If you receive rental income—a lease agreement, rental statements from the real estate agent or tax return.

These documents are fairly standard across the board and will be used to verify your income.

If you receive a bonus or income from a second job, the bank might also ask for your PAYG Annual Summary (also called a group certificate).

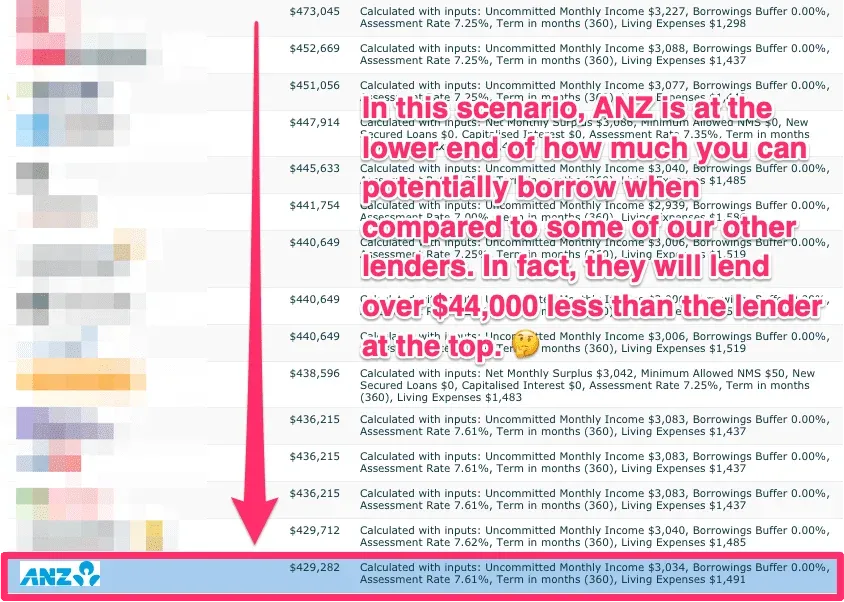

ANZ’s credit criteria are subject to change at any time, and all lending is up to credit verification and satisfactory approval. However, as an indication, we have run the following scenario through their borrowing calculator:

A single person living in Brisbane (In the 4000 postcode)

Figures as of 28 December 2022 are subject to credit criteria and will change without notification.

We ran the figures through our serviceability calculator and got the following results:

In this scenario, ANZ is at the lower end of how much you can potentially borrow compared to some of our other lenders. In fact, they will lend over $44,000 less than the lender at the top!

Check to see if you are eligible for a home loan

How Long Does ANZ Pre-Approval Take? (And What Can Delay It?)

When you apply for ANZ pre-approval, you’re completing the first steps of the home loan process. The great news? It doesn’t have to take long. Below, we’ll look at typical turnaround times, what can slow things down, and how to make your pre-approval happen faster — especially when working with a mortgage broker.

Typical Turnaround Times: Online vs Broker-Submitted

ANZ’s turnaround times vary depending on how you apply:

Online applications: Using ANZ’s Quick Start form takes less than five minutes, and you’ll usually get a callback within 24–48 hours.

Broker-submitted applications: When you apply through a mortgage broker, your pre-approval usually takes 3–5 business days — but it’s more detailed and accurate.

Fully assessed pre-approval: ANZ broker applications are often fully assessed by the credit team, meaning your income, expenses and liabilities are properly verified upfront. This reduces the risk of surprises later.

In short, you could receive an approval in principle within 1–3 business days for simple cases, or up to a week if your application is more complex.

Why Using A Broker Is Often Better

Working with a mortgage broker to get an ANZ pre approval can make a huge difference. Here’s why:

Full assessment upfront: Brokers submit your documents directly to ANZ’s credit team for a comprehensive review — unlike instant online tools that rely on estimated data.

Higher accuracy: Because your broker checks every detail before submission, you’re less likely to get conditional approval that later falls through.

Faster communication: Brokers have direct access to ANZ’s internal assessment team and can follow up on your file daily.

Less stress: You don’t have to guess what paperwork or evidence is needed — your broker ensures it’s complete and compliant with ANZ, ASIC, and APRA requirements.

In fact, ASIC recommends seeking professional mortgage advice to ensure you understand loan terms and lender requirements before committing.So, while online pre-approval might seem faster, a broker-assisted pre-approval is usually more reliable and fully verified, which saves you time later when you’re ready to buy.

What Can Delay Your ANZ Pre-Approval?

Even the best applications can be slowed down by a few common issues:

Missing or incomplete documents: ANZ requires proof of income, identity, expenses, and debt. Missing items always cause delays.

Credit issues or complex situations: Self-employment, irregular income, or previous defaults often require manual checks.

Employment verification delays: ANZ must confirm your job details with your employer before approval.

Non-standard properties: If your property type is outside ANZ’s standard lending policy, valuation may take longer.

High application volumes: Like all banks, ANZ can slow down during peak periods.

The Bottom Line

If your documents are ready and your finances are straightforward, ANZ pre-approval can take as little as 1–3 business days. However, for a more accurate, fully assessed, and reliable approval, working with a mortgage broker like Hunter Galloway is your best option.

You’ll get expert guidance, fewer delays, and a pre-approval that truly reflects what you can borrow — helping you shop for a home with confidence.

One of the biggest advantages of ANZ pre approvals over other banks is that their approvals in principle are valid for 6 months! This is much more than other banks whose pre approvals are only valid for 3 months.

The only drawback is that once your approval in principle expires, your mortgage broker will need to submit an entirely new application.

If your pre-approval expires before you have found the right home to buy, your mortgage broker will have to make an entirely new application.

When Should I Get A Pre-approval?

You should only get a pre approval if:

You are looking at buying a home in the next 3-6 months

You have a lease due for renewal soon

You have at least 8-10% in savings to cover deposit and stamp duty costs

You have a stable job and income.

You shouldn’t get a pre approval if:

You aren’t looking at buying for another 6+ months

You have just renewed your lease for another 6-12 months

Overall, ANZ is not a bad lender, with good products and offers that ultimately depend on your situation.

The only mistake we suggest avoiding is going ahead with them (or any bank) without first understanding what the market can offer.

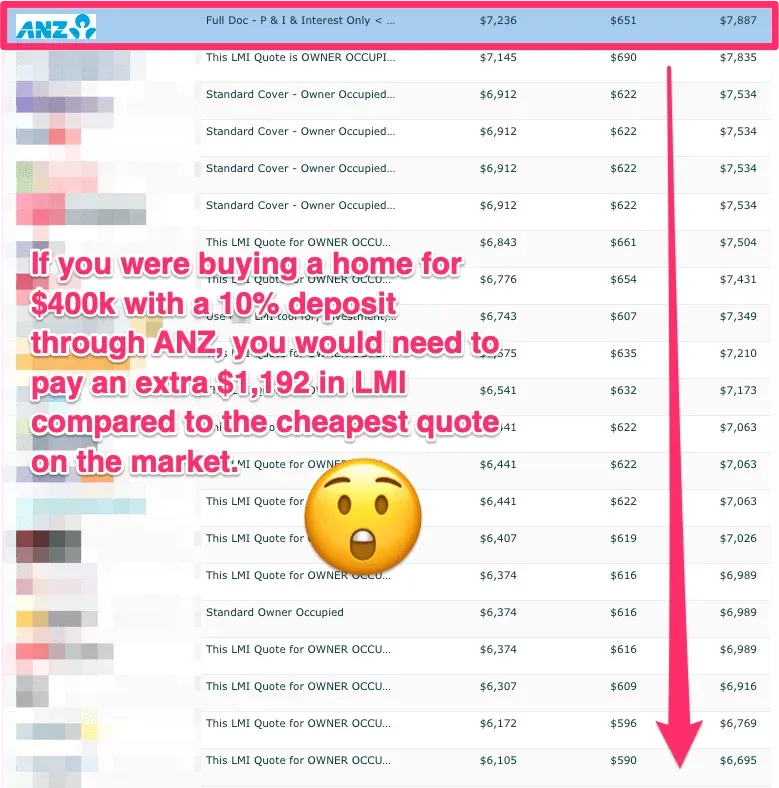

Case Study: The phone call that put $1,192 into Dave's pocket

Dave had found a home to buy and went straight back to his childhood bank, ANZ, to get a loan.

He’d signed a 21-day contract, so he had a little time up his sleeve for finance approval.

ANZ got all of Dave’s information, quoted the rates that were advertised on their website and sent him the forms to sign.

A mutual friend of Dave’s suggested he chat with us just to run a second set of eyes across the loan offer before he signed his life away…

We spoke to Dave on the phone and found out ANZ had quoted him $7,887 in Lenders Mortgage Insurance.

After quickly checking our system, we saw that we had another bank that would only charge $6,695 for LMI.

…$1,192 cheaper

In this example, buying a home for $400,000 with a 10% deposit would cost an extra $1,192 in LMI through ANZ compared to other lenders. The calculator is at December 2022, can change anytime and is subject to individual bank credit criteria and further conditions.

Not only that, this lender had a special for first-home buyers offering Dave a really sharp rate.

Dave decided to go with our lender, and use the $1,192 he saved on a couch for his new place!

A few simple tips can help you avoid some really common mistakes most home buyers make. Get a second set of eyes on your pre approval to make sure you have the best deal for your situation.

If you would like us to run our eyes over your bank’s offer or give you a second opinion, book a free assessment or call us on 1300 088 086.

Can ANZ Decline Your Home Loan After Pre-Approval?

The short answer is yes — ANZ can still decline your home loan even after giving you pre-approval. As we mentioned before, a pre-approval, or approval in principle, is not a guarantee that your loan will be fully or unconditionally approved.

Why ANZ Can Decline a Loan After Pre-Approval

ANZ, like all major banks regulated by APRA, assesses your loan using four key factors:

Your income and employment – Your ability to comfortably repay the loan.

Your living expenses and liabilities – How much of your income is already committed.

Your deposit and savings history – How much genuine savings you have.

The property itself – The asset that secures your loan.

If any of these change after pre-approval — such as a new debt, job change, or a problematic property — ANZ may decline your loan when it goes to full assessment

Common Reasons ANZ May Decline After Pre-Approval- (Explained)

1. Changes to Your Financial Situation

If you change jobs, take on new credit, or your income drops, ANZ may need to reassess your borrowing capacity. Even a small increase in credit card limits can impact your serviceability and trigger a reassessment.

2. The Property Doesn’t Meet ANZ’s Lending Criteria

Banks can be a bit more critical on units compared to regular houses. Check with your mortgage broker on the specifics of your potential new home to confirm it meets your bank’s credit policy.

Even if you are eligible, the property might not be. Banks use strict property criteria set by their credit policy and APRA’s responsible lending guidelines. Here are some common property issues that can cause a rejection:

Apartments smaller than 40 square metres

Units in high-density inner-city buildings (especially above 4 storeys)

Properties in high-risk postcodes with oversupply

Off-the-plan purchases with uncertain valuations

Properties too close to power lines, service stations, or on heritage listings

Buildings where ANZ already has significant lending exposure

We’ve seen buyers knocked back for reasons as small as “too close to power lines.” It pays to check before signing.

3. Your Pre-Approval Expired

ANZ pre-approvals typically last 90 days.If this period lapses and your financials or lending criteria change, ANZ may require a full reassessment before proceeding.

How to Avoid Getting Declined After Pre-Approval

You can reduce the risk of rejection by taking these steps:

Keep your finances stable — avoid new loans, credit cards, or job changes until settlement.

Check your property first — ask your broker to confirm the property fits ANZ’s criteria before making an offer.

Stay within your budget — don’t push the limits of your borrowing power.

Submit updated documents early — this keeps your file current and speeds up final approval.

A mortgage broker can often spot potential red flags early, saving you time and disappointment. At Hunter Galloway, we do a property and policy check with every pre-approval, so you know exactly where you stand before making an offer.

The Bottom Line

Even with ANZ pre-approval, your home loan isn’t guaranteed until it becomes unconditional. Changes to your income, debt, or property type can still cause a decline. That’s why it’s always safer to work with a mortgage broker who can get your fully-assessed pre-approval reviewed by ANZ’s credit team — before you sign a contract.

ANZ pre-approval is typically valid for 90 days. If it expires, you may need to resubmit updated documents.

Does ANZ do hard or soft credit checks for pre-approval?

ANZ performs a full (hard) credit check, which may slightly impact your credit score.

Can I extend my ANZ pre-approval?

Yes — ANZ may allow an extension if your financial situation hasn’t changed. Your broker can request it on your behalf.

Will ANZ recheck my expenses before final approval?

Yes — ANZ will reassess your spending and debts to confirm your position before final sign-off.

Can I switch properties after ANZ pre-approval?

Yes — as long as the new property meets ANZ’s criteria. High-risk locations or unusual properties may need reassessment.

Do I need a deposit before applying for ANZ pre-approval?

ANZ generally requires evidence of genuine savings, usually at least 5% of the purchase price.

Can self-employed borrowers get ANZ pre-approval?

Yes — but you’ll need at least 1–2 years of financials such as tax returns and business statements.

How We Can Help You

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one person operations, we havean entire team of experts dedicated to help make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment onlineto see how we can help.

Our team of home loan experts is here to help you buy a house in Australia.

The information provided in this article is intended to provide illustrative examples based on stated assumptions and your input. Calculations are meant as estimates only, and it is advised that you consult with a mortgage broker about your specific circumstances

Why Choose Hunter Galloway As Your Mortgage Broker?