YTD Calculator Australia: Your Guide To Calculating Annual Income From Payslip

Loan approval rate of 97%*

Variety of options due to direct access to 30+ Australian banks & lenders

Highest-rated Mortgage Broker in Brisbane — 2,400+ Google reviews

Free for you, and you won't pay more — the lender pays us

35+Years of

experience

Based on

2,400+ reviews

Mortgage Broker of the Year in 2017, 2018, 2019 and 2024

Access to 30+ banks and lenders in Australia

Thousands of families helped into their homes

*Based on all applications processed through Hunter Galloway, 2024–2026.

YTD Calculator Australia: Your Guide To Calculating Annual Income From Payslip

When applying for a home loan, knowing your Year-to-Date (YTD) income is crucial. Lenders use it to estimate your annual earnings based on what you’ve earned so far this financial year. This figure can fluctuate due to your pay cycle, job changes, unpaid leave, or commission, so understanding how it’s calculated helps you know your borrowing power.

Expert tip:YTD calculations are aligned with guidance from theAustralian Taxation Office (ATO). They ensure lenders see a consistent view of your income before approving a home loan. Working with a licensed mortgage broker like uscan help you navigate unique income situations and present your application in the best possible light.

What Is YTD Income and Why Do Lenders Use It?

Year-to-Date (YTD) income shows the total earnings you’ve received so far in the current financial year. Lenders use this figure to estimate your annual income and assess your ability to repay a home loan. It can include your base salary and, depending on the lender, regular overtime, commissions, and allowances. Understanding your YTD income helps you present an accurate financial picture and increases your chances of loan approval.

YTD Calculator

A Year-to-Date calculator (YTD calculator) helps you annualise your salary based on income earned in part of the year. It’s also known as an income annualisation calculator.

In simple terms, your YTD income represents what you would earn over 12 months if your pay rate stayed the same.

Lenders often use the YTD figure and compare it with your ATO Income Statement from the previous financial year. Usually, the lender will take the lower of the two figures to assess your ability to repay a loan. For example, if your YTD annualised income is $120,000 but your ATO statement shows $100,000, they may use $100,000 when calculating borrowing power.

However, some lenders—especially when working with experienced mortgage brokers—may accept the higher figure if you provide a compelling reason. This flexibility can make a real difference when applying for a home loan

Why Your Income and Debt-to-Income Ratio (DTI) Matter

The higher your income, the more confident a lender will be in approving a larger loan. One key metric lenders use is your Debt-to-Income ratio (DTI), which measures how much of your income goes toward debt.

DTI above 6 (for example, a $700,000 loan with a $100,000 income) signals higher risk.

While this doesn’t automatically block approval, lenders may scrutinise applications more closely and look for strong compensating factors such as:

High income

A strong savings history

Low Loan-to-Value Ratio (LVR)

YTD Calculator is especially helpful if you have started a job in the middle of the financial year.

How Do I Use The YTD Calculator?

Using the Year-to-Date (YTD) income calculator is simple and helps you estimate your annualised salary accurately. Follow these steps:

Get your most recent payslip. This provides your YTD gross income and pay period dates.

Enter your job start date. If you’re unsure, an approximate month and year is fine.

Enter the end date of your latest payslip. For example, if your pay period was 01/03/2024 to 31/03/2024, enter 31/03/2024.

Enter your YTD gross income from that payslip.

Press calculate to estimate your yearly gross income.

Expert tip: These calculations are aligned with ATO guidance on income reporting. Your YTD figure is only an estimate and may differ from what lenders use. Always confirm your calculation with your mortgage broker or lender to avoid errors.

If you have any questions about using the calculator, contact our team online or call us on 1300 088 065.

Understanding Payslip Components and YTD Figures

Your payslip contains key information lenders use to verify your YTD income. Knowing what to look for ensures your loan application is accurate.

Key components to check:

Gross Pay: Total earnings before taxes and deductions.

Deductions: Amounts withheld for tax, superannuation, and other contributions.

YTD Gross Income: Total gross pay earned so far this financial year.

Pay Period Dates: Start and end dates for your payment cycle (weekly, fortnightly, or monthly).

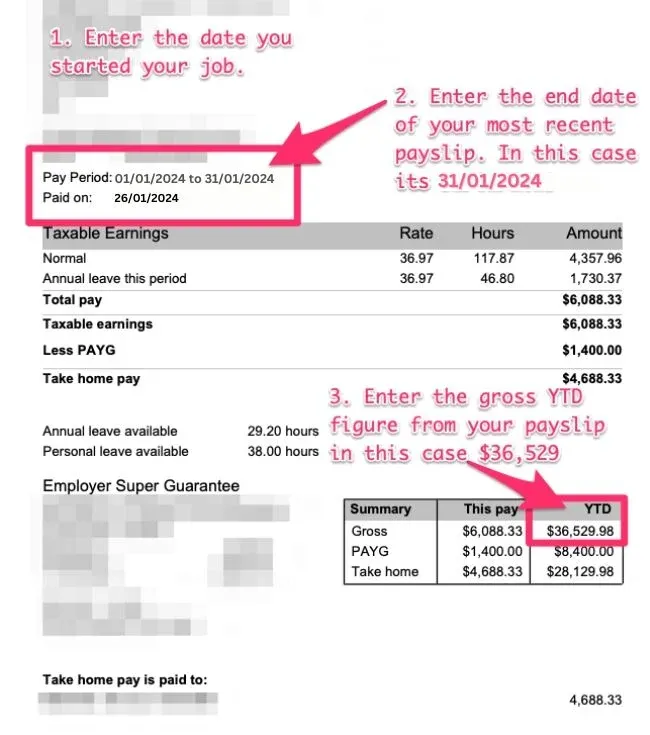

Example: If a payslip shows a YTD gross income of $36,529 for the period from 6 August 2023 to 31 January 2024, it means you earned $36,529 since starting your employment during this financial year.

Important: Not all payslip items count toward YTD income for lending purposes. Bonuses, overtime, and commissions may be treated differently depending on the lender’s policies. For accurate calculations, check with your mortgage broker or refer to ASIC’s MoneySmart guide on income.

Being familiar with these components helps you:

Gather the right documents for your application

Avoid errors when entering information into the YTD calculator

Improve your chances of securing the best loan terms

“Always double-check your YTD gross income and deductions on your payslip. Small errors can affect your borrowing power”

How Lenders View Different Types of Income

Lenders treat income types differently when calculating your borrowing power. The table below shows typical practices:

Income Type

% Typically Accepted by Lenders

Required History / Notes

Example Use in Loan Assessment

Base Salary

100%

Current employment, payslip required

Core income for all loan calculations

Overtime

50–100%

Usually 6–12 months consistent history

Used as supplementary income

Commission

50–100%

12–24 months track record, may vary

Can boost borrowing capacity

Casual / Temporary

0–75%

6–12 months consistent work, may vary

Depends on lender discretion

Expert Tip: Always confirm with your mortgage broker which income types your chosen lender will consider. Policies can differ significantly.

Here Is An Example Of Using The YTD Calculator

We’ve also included a salary payslip to show you where the information comes in this example:

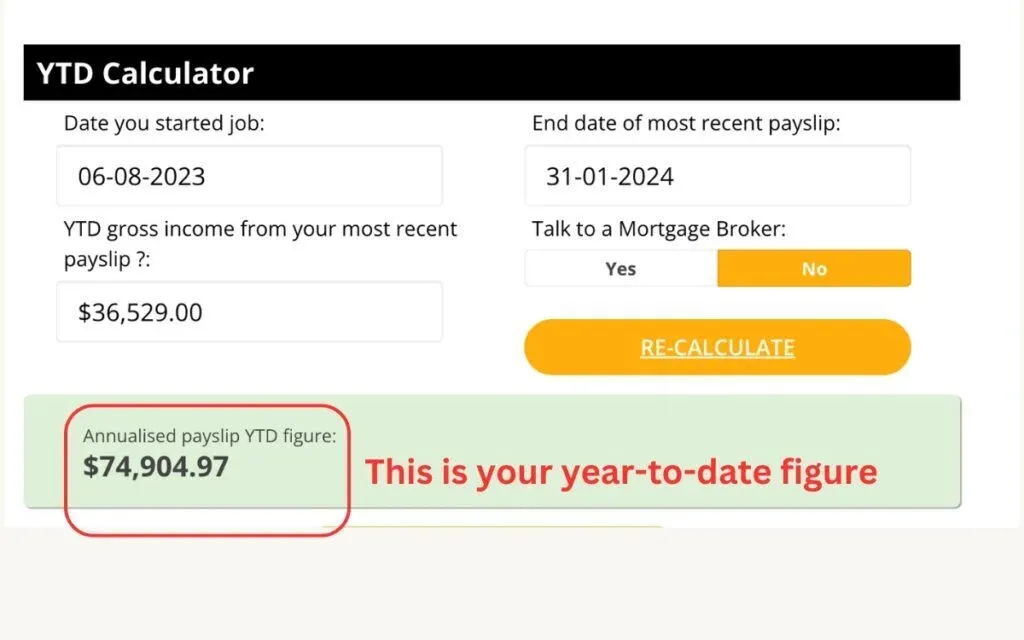

1. Enter the date when you started your job: 06/08/2023

2. Enter the end date from your most recent payslip: 31/01/2024

3. Enter the YTD gross income from your most recent payslip: $36,529

4. Press calculate on the calculator to calculate your yearly gross: $74,904.97 per year!

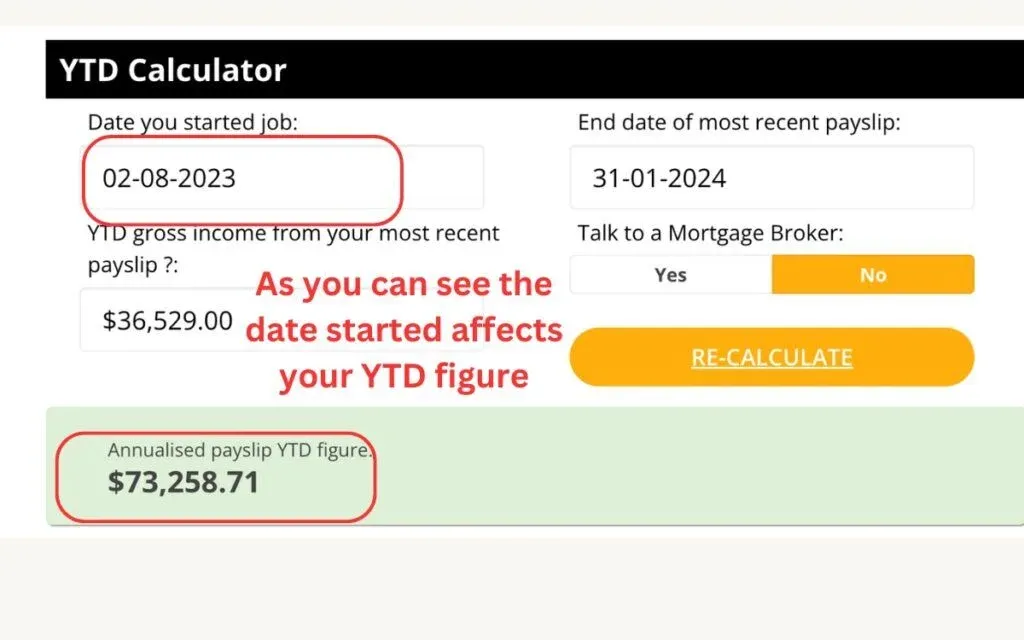

Why Does It Need To Include The Start Date

The year to date income is calculated by financial year, which in Australia begins on the 1st of July of each year.

Our calculator looks at the months you have worked in the current financial year and annualises this to get the yearly figure.

If you started your job after 1 July, simply annualising your YTD income without accounting for the shorter period worked will result in an inaccurate, lower annual salary estimate. Including your precise start date allows the calculator to correctly pro-rata your earnings over a full 12 months.

How Is YTD Calculated From July To September?

Using the YTD calculator to determine your annual income is trickier in the first few months of the financial year. The new financial year begins on the 1st of July, and most payslips will have their YTD figure reset on this date.

So, if you’re calculating your YTD income in July, August, or September, there isn’t much history to go on. A small amount of unpaid leave or a few days of overtime could dramatically increase or decrease your annualised income calculation.

In these months, some lenders will rely more heavily on your employment contract and your ATO Income Statement from the previous financial year to establish a stable income figure. These documents will show a full 12 months of income or the date that you started with your new employer in the previous financial year. Either way, it allows the banks to get a more accurate idea of your annual income.

How To Double-Check The Calculator’s Results

While our YTD calculator provides a quick estimate, it’s helpful to know how to manually verify your results. This ensures your income is accurate and aligns with lender expectations.

Why the Start Date Matters

The start date tells us how many days you’ve worked this financial year. This is essential for annualising your income correctly, especially if you started mid-year. Even a small error in the start date can affect your estimated annual income, so accuracy is important.

Manual Calculation Formula

Annualising based on days worked is more precise than using months. Use the following formula:

Annualised Income= YTD Gross Income ÷ Number of Days Worked ×365

Step-by-Step Instructions:

Find your YTD gross income on your latest payslip.

Count the number of days worked since starting this financial year.

Apply the formula above to calculate your annualised income.

Example:

YTD Gross Income: $36,529

Days Worked: 150

36,529÷150×365≈88,833

Your annualised income is approximately $88,833.

Why This Matters

Lenders use annualised YTD income to determine your borrowing power. Ensuring your manual calculation aligns with the calculator result gives you confidence in your loan application and helps your mortgage broker present the most accurate information to lenders.

How To Calculate YTD Income On A New Job?

If you started a new job in the middle of a financial year, you might have noticed your year-to-date income figure looks a little low. And that’s nothing to worry about—it’s the exact reason why we use a YTD calculator to calculate your annual income rather than just taking the number from your payslip.

For example, if you started a job on the 1st of February 2024, and you have a payslip dated 1st March 2024 with a year-to-date figure of $5,000, we’re not going to assume that you’ve only earned $5,000 for the entire financial year. Annualising this figure calculates your YTD income as $65,187.

If you have just recently started a new job, be aware that you may find it a little more difficult to get your home loan approved. Lenders typically do not like to lend to people who are still on their probation period, as they see it as a higher risk. However, we can help you get a policy exception with some lenders, which will give you more flexibility in getting a loan.

If you are employed casually, the YTD income is especially important. As a casual worker, your income could vary from week to week, depending on:

how many hours you’ve been rostered on

overtime

other allowances.

If they just looked at your last couple of payslips and annualised those figures, your estimated income could be much higher or lower than it actually is.

The YTD calculator will annualise your income to understand how much you will be making in that year.

If you are a casual worker, most banks will need you to have been in the job for at least 6 to 12 months. Some lenders are even stricter.

Some lenders require two previous years’ ATO Income Statements to verify a stable casual income history. Others are more flexible. We work with several lenders who will accept casual employment even if you’ve only recently started your job.

If you’d like to know more, please call us on 1300 088 065 orfill in our free assessment form, and one of our mortgage brokers will give you a call to discuss your situation.

Commission income, along with other types of supplemental income, is usually treated differently than your base income. However, they will still usually accept this as part of your income when assessing your application, especially if you have at least a 1-2 year history of receiving commission.

Most banks will let you use all of your commission income towards your loan application if you have a 20% deposit. If you have less than a 20% deposit, they may accept a lower commission (sometimes as low as 50%).

However, we work with several lenders who will accept a higher amount of your commission income. If you’d like to know more, get in touch with our mortgage brokers on 1300 088 065 orfill in our free assessment form.

Common Questions About How To Calculate Year To Date Earnings

Does YTD mean last 12 months?

YTD stands for “Year to Date” and measures your earnings from the start of the financial year to the current date. It does not always cover the last 12 months. Instead, it reflects income within the current tax year for accurate reporting and loan assessments.

What is gross pay YTD?

Gross pay YTD is your total earnings before tax and deductions from the start of the financial year. This figure includes regular wages, overtime, bonuses, and commissions. Lenders use gross pay YTD to estimate your annualised income for home loan purposes.

How do I calculate income from pay stub?

To calculate income from a pay stub, find your YTD gross income and divide it by the number of months worked. Multiply this monthly figure by 12 to annualise it. This method helps confirm the results from an online YTD income calculator.

What is year to date earnings?

Year to date earnings show the total amount you have earned from the beginning of the financial year until now. They include salary, overtime, bonuses, and allowances before tax. Lenders often use YTD earnings to verify your income stability.

How to calculate monthly income from YTD?

Divide your YTD gross income by the number of months you’ve been paid in the financial year. The result is your average monthly income before tax. This figure is helpful for budgeting, loan applications, and income verification.

What does YTD mean on my payslip?

On a payslip, YTD shows the cumulative total you have earned since the start of the financial year. It helps track your income progress and deductions over time. This figure is also used in home loan assessments to annualise your earnings.

What is year to date take home?

Year to date take home is the total net income you’ve received after all taxes and deductions. It reflects your actual banked earnings since the start of the financial year. This is different from gross YTD, which is before tax.

When does YTD start?

In Australia, YTD typically starts on 1 July and runs to the current date. Other countries may align YTD with the calendar year starting 1 January. Understanding the start date ensures accurate income calculations for tax and loan purposes.

Why does my YTD income differ from my actual annual salary?

Your YTD income shows earnings so far, annualised to estimate your full-year salary. If you started your job mid-year, took unpaid leave, or changed pay rates, this figure may differ. Lenders look at both YTD and your employment history to assess consistency.

How does unpaid leave or maternity leave affect my YTD income?

Unpaid leave reduces your total earnings for the year, which lowers your YTD income. This can impact your borrowing power if lenders use YTD figures to annualise your income. Providing proof of your return-to-work date can help reassure lenders.

Can I use income from multiple jobs in my YTD calculation?

Yes, you can combine YTD income from multiple jobs. You will need to provide recent payslips from each employer, and lenders will often want to see a 6-12 month history in each role to consider the income stable

Bonus: Tips For Getting A Loan When You Have A Unique Income

When it comes to getting a home loan, every case is unique. Here are some types of unique income and how you can get a home loan if you have these types of income:

Maternity leave

Many banks may decline the loan because a lot of people who go on maternity leave may not even come back to work. However, if you provide a return-to-work letter from your employer, some banks can consider your return-to-work income. Keep in mind that if you return to work, the lenders require you to do it within 12 months and return to the same role, not a different one.

Casually employed

Since casual work is not always guaranteed, most lenders will need you to be in the role for 6 months. There are one or two lenders that can think outside the box. For example, suppose you are an IT contractor, or you’re in the film and television industry, where the nature of the industry requires you to move from contract to contract. In that case, some banks will actually consider one day in a role, providing it makes sense. So keep that in mind. If you’re casually employed, there isn’t always a hard no if you’re less than six months in the role.

In most cases, lenders will want you to have 2 years’ tax returns, which can be very hard, especially if you have just started your business. There are some lenders who can consider 1 year’s financials provided you have 18 months of ABN history. The good news is that there are others that will waive it completely. In most cases, they require a 20% deposit, but it’s on a case-by-case basis.

On a probationary period

Most providers and lenders will want you to pass your probation period, which is typically 6 months in Australia but can be 3 months in some cases. If you are doing a really good job, you can ask your employer to pass your probation early. If your employer says no, then a few lenders will look at other things, such as whether you have 2 years of employment history in the same industry. There are even some lenders who will grant your application even if you are on probation. It’s just a matter of talking to the right mortgage broker.

Working in multiple jobs

The first thing lenders will want to consider is whether or not it’s sustainable. So, for example, if you are working 40 hours at job 1 and 40 hours at job 2, most lenders will say it is not sustainable because you will eventually burn out. In this case, they will consider only a portion of your income. The banks will also want to see that you have been in both roles for a minimum of 12 months.

In conclusion, having a unique income should not disqualify you from getting a home loan. There are so many lenders with so many different policies, and a no from one lender isn’t a no from all of them. The right mortgage broker will be able to find a solution for you.

How Will A Bank Look At My Income?

Do you realise that only a handful of banks will use 100% of your extra income, such as overtime, shift allowances, bonuses, casual income, andmaternity leave income?

Our team at Hunter Galloway can help you gain a detailed understanding of YTD income and will help you find the right lender.

Unlike other mortgage brokers, who are one-person operations, we havean entire team of experts dedicated to making your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 orbook a free assessment onlineto see how we can help.

Our team of home loam experts is here to help you buy a home in Australia

Disclaimer: Lending policies and eligibility criteria vary between lenders. This article is for informational purposes only and does not constitute financial advice. Always consult a licensed mortgage broker or financial professional before making decisions about your home loan.

Why Choose Hunter Galloway As Your Mortgage Broker?

Mortgage Broker of the Year

in 2017, 2018 and 2019

The highest rated and most reviewed

Mortgage Broker in Brisbane on Google

97% loan approval rate

across all applications we processed, 2024–2026

We have direct access to 30+ banks

and lenders across Australia

We promise to get back to you within 4 business hours