If you are new to property investment, you have probably heard the term’ negative gearing,’ but it can be confusing to understand. What does it mean? Is it good or bad? How can negative gearing help me to grow my investment portfolio? In this article, we will provide a simple, plain English explanation of negative gearing and answer some of the most common questions people have about it.

What is Negative Gearing?

Negative Gearing is an investment strategy that involves purchasing a property that has holding costs greater than the rental income it generates. While this means you are making a loss, you can claim the loss in income as a tax deduction.

A property investment strategy based on negative gearing relies on increasing property values to offset the losses made from holding the property.

Negative Gearing vs. Positive Gearing – What’s the Difference?

Negative gearing means you are paying more interest and costs than the rental income you are receiving. Positive gearing is the opposite – it’s when the interest and total costs of your property are less than the income you make, giving you a monthly profit. Negative gearing may not make a lot of sense if you’re looking purely at the cash flow generated from your investment property. However, negative gearing has other benefits that can make it a winning part of your investment strategy.

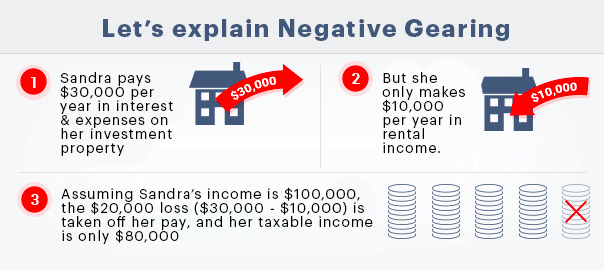

An Example of Negative Gearing

Let’s walk through a simple example of someone who owns a negatively geared unit. Sandra is renting out an apartment. Her income and expenses could look something like this:

Annual Income | Annual Expenses | ||

Rent | $30,000 | Loan at 4.50% | $28,000 |

|

| Management Fees | $2,500 |

|

| Council Rates | $1,500 |

|

| Body Corp Fees | $2,000 |

|

| Depreciation | $12,000 |

|

| Insurances | $500 |

Total Income | $30,000 | Total Expenses | $46,500 |

Total Income / Loss | -$16,500 | ||

You’ll note that we’ve included depreciation in this example. While you don’t directly pay for depreciation, you must pay to maintain the property, so we’ve included it in our calculations. In this example, Sandra’s property is negatively geared by $16,500 per year:

The next thing we need to do is look at her tax returns. Any loss from an investment property can be deducted from your taxable income. For this example, we’ll assume that Sandra is making $110,000.

The $16,500 loss will be deducted from her income, so she will pay tax on only $93,500. This would reduce her tax payable by $5,362.50. When we factor this into her annual losses for the property, the total loss per year would be $11,137.50. The other benefit is the depreciation cost for the property – Sandra wouldn’t physically have to fork out $12,000 per year, so she would actually be up around $862.50 per year from her tax refund. That means that after her negative gearing benefits, the property is actually slightly positively geared. However, this is looking at an ideal situation. If the property has any vacancies and her rental income gets reduced, or her interest rates increase, the property can quickly become negatively geared. But the real benefit of negative gearing is capital growth. What happens if Sandra’s property increases in value by 4% in 1 year? Depending on how much capital Sandra has invested, this can translate into a very good return on investment:

Cash invested | Borrowing | Purchase Price | Capital Gains | Return on cash |

$250,000 | – | $250,000 | $10,000 | 4% |

$100,000 | $150,000 | $250,000 | $10,000 | 10% |

$25,000 | $225,000 | $250,000 | $10,000 | 40% |

However, it goes both ways. If the property value decreases, then it compounds the losses:

Cash invested | Borrowing | Total Invested | Capital Gains | Return on cash |

$250,000 | – | $250,000 | -$10,000 | -4% |

$100,000 | $150,000 | $250,000 | -$10,000 | -10% |

$25,000 | $225,000 | $250,000 | -$10,000 | -40% |

What Expenses Can You Claim On An Investment Property?

Depreciation

There are two different deductions that are available to you, and they work quite differently.

- The depreciation of furniture. You can write that off a lot more aggressively. So you’re looking at effective life, which is the life of the furniture. Let’s just use a fridge for example, it could be four years. You pay a thousand dollars for a fridge, and you can claim a $250 deduction each year for four years.

- The depreciation of capital. It works differently because it is on the house itself. This depreciation is at a flat 2.5% over 40 years. So it’s not a massive deduction but it’s consistent for the time that you’re renting out the property.

To be able to claim depreciation, the ATO now requires you to get a quantity surveyor’s report, and that’s a report that tells you what you’re allowed to claim based on the assets in the house. That quantity surveyor’s report is going to cost you money, but that’s fully deductible. So basically, you can claim a deduction on getting a deduction, which is pretty cool.

Interest

Interest is your second biggest deduction nine times out of ten. So, the interest on the home loan that you have paid throughout the year is a great deduction. Sometimes you can get a win on that by making prepayments of interest. We don’t see it very often anymore, but it is a nice little windfall. But you’ve got to consider the year-on-year effect of that interest because if you do a prepayment, what you’re effectively doing is you’re bringing next year’s deduction forward a year. So you just have to be careful with that — you want to do it when your tax rate is at its peak, or maybe you just want to double down on your refund so you do it that year.

Repairs

Another potentially big expense is repairs. So you could one year have a repair of $100 fully deductible. You might have to go out and do some pretty significant repairs one year. They can really add up, and you can get a really good deduction in that instance. We’d probably just disclaim you’ve got to be really careful with repairs as they can transition into what’s called renovations or improvements. Once it falls into that realm, it goes under this quantity surveyors report concept we discussed earlier. Remember, a repair is 100% deductible, but if it falls under a renovation, it falls under that depreciation rule and ultimately is depreciated over a period of time.

Other expenses you can write off for negative gearing

- Council rates

- Body corporate fees for your townhouses and apartments

- Insurance

- Bank fees

- Water rates

- Utilities

What Are The Benefits Of Negative Gearing?

The main advantage of negative gearing is that you can offset the loss from owning a property that is not generating enough rent to pay for its expenses. This decreases your taxable income, which means your tax liability will decrease. This is an especially useful benefit for those with a high income. Tax benefits can assist with your short-term cash flow while you are waiting for the property to increase in value. Depending on the amount of cash you have invested in the property and the capital growth, this strategy can deliver a high return on investment.

What Are The Downsides Of Negative Gearing?

The main downside for property investors is that a negative gearing strategy relies on capital gains. If the property value decreases, then the investment will make a loss. This problem is compounded if you are highly leveraged and own multiple properties.

The other main downside is for people who are looking to buy a home to live in. Negative gearing can inflate property values since investors are willing to buy property that won’t generate an income. However, the impact of negative gearing is small in comparison to other factors, such as zoning regulations and interest rate cuts.

What Are The Negative Gearing Changes In Australia in 2024?

Negative gearing has always been a hot topic in the Australian property market. There have been talks for years about reform, but it never seems to go anywhere. Like it or not, Australians love property investing and negative gearing is unlikely to go away any time soon.

Bonus: 5 Massive Changes Affecting Landlords and Renters in 2024

Being a landlord is not just an investment like shares; it means providing housing for another human being. The following 5 reforms have been implemented to help make renting a fairer arrangement for tenants and landlords. So what are the reforms?

- Rental bidding. Rental bidding is where the property goes to the highest bidder – effectively pricing out most people from the rental market. Rental bidding is now illegal everywhere in Australia.

- Minimum standards for dwelling. This means that rental properties will have to meet certain basic standards before they can be rented out. So, for example, heating, safety and, in some cases, security.

- Property modification. Most of the time, landlords don’t allow tenants to make modifications such as hanging a picture or planting a vegetable garden at the back. This reform will allow people to make (reasonable) modifications as long as they put the property back to what it was when they initially leased it out.

- Pet inclusions. This is a huge one because many people have pets, and they form part of their family. With this new reform, landlords will have to establish grounds for refusing pets instead of just saying ‘no’.

- More secure leases. This applies more to New South Wales, where landlords could easily get rid of tenants without establishing grounds for eviction. Now, they have to give valid reasons, for example, if they are moving back into the property.

These reforms differ slightly from state to state, so make sure you check the specific reforms in your state.

Negative Gearing Frequently Asked Questions

Negative gearing is an investment strategy where the costs of owning a property (like mortgage interest, maintenance, and other expenses) exceed the rental income it generates. This loss can be claimed as a tax deduction, potentially reducing the investor’s overall taxable income.

Negative gearing occurs when the costs of owning an investment property exceed its rental income, resulting in a loss. Positive gearing is when the rental income is higher than the property’s expenses, resulting in a profit.

The main benefits of negative gearing include potential tax deductions, which can lower your overall taxable income, and the possibility of long-term capital growth on the property investment.

Yes, the main risks include relying on capital growth to offset losses, potential changes in tax laws, interest rate increases, and the possibility of the property value decreasing.

While anyone can technically use negative gearing, it’s generally more beneficial for high-income earners due to the tax advantages. It’s important to consult with a financial advisor to determine if it’s suitable for your situation.

Negative gearing allows you to deduct the loss from your investment property from your taxable income, potentially reducing your overall tax liability.

No, negative gearing can apply to various types of investments, including commercial properties and shares. However, it’s most commonly associated with residential property investments in Australia.

Claimable expenses typically include mortgage interest, property management fees, repairs and maintenance costs, council rates, insurance, and depreciation.

The holding period depends on individual circumstances and market conditions. Many investors aim to hold the property long enough to benefit from capital growth, which could be several years or more.

There’s no legal limit on the number of properties you can negatively gear. However, lenders may have their own restrictions based on your financial situation.

If your property becomes positively geared, you’ll start making a profit from the rental income. This profit will be added to your taxable income rather than being deducted from it.

No, negative gearing only applies to investment properties. You cannot negatively gear your primary residence.

Depreciation on the building and its fixtures can be claimed as a tax deduction, potentially increasing the negative gearing benefit without affecting your cash flow.

While there have been discussions about potential changes, as of now, there are no concrete plans to significantly alter negative gearing laws in Australia.

Recent reforms in some states affect areas like minimum property standards, pet inclusions, and more secure leases. These may impact the costs and management of negatively geared properties.

Lower interest rates can reduce the negative gearing benefit as they lower borrowing costs. However, they may also stimulate property price growth, which can be beneficial for long-term capital gains.

Lenders typically consider the rental income from an investment property when assessing your borrowing capacity. The tax benefits of negative gearing may also be considered, but this varies between lenders.

Yes, it’s possible to use negative gearing within an SMSF, but there are strict rules and regulations. It’s crucial to seek professional advice before pursuing this strategy.

While negative gearing can provide annual tax benefits, when you sell a negatively geared property, you may be liable for CGT on any capital gains. However, if you’ve held the property for more than 12 months, you may be eligible for a CGT discount.

Yes, this can happen if rental income increases, interest rates decrease, or you pay down the loan principal. As the property’s income starts to cover or exceed its expenses, it moves towards neutral or positive gearing.

Is Negative Gearing Right for You?

All investments come down to your individual situation and circumstance. If you are looking to purchase an investment property in Brisbane or across Australia, our team at Hunter Galloway can help.

Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again