Navigating mortgage broker fees in Australia shouldn’t feel like a guessing game. While most first-home buyers pay $0 out of pocket for expert advice, understanding the commission structures and the Best Interests Duty (BID) that protects you is essential for a stress-free journey.

This guide, written by an expert mortgage broker in Brisbane, breaks down the latest 2026 industry standards to ensure you secure the best deal without hidden costs.

Understanding Mortgage Broker Fees: How It Works

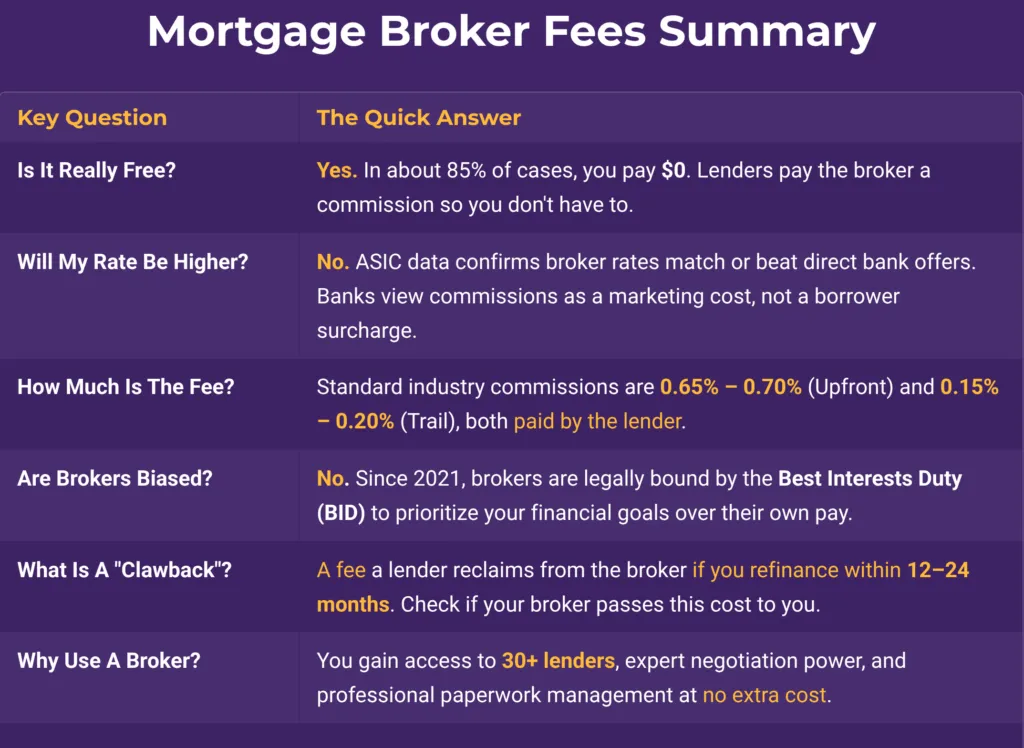

Mortgage broker fees include any money a broker earns for arranging your home loan. Most Australian first-home buyers pay nothing out of pocket for this service. Instead, lenders pay brokers a commission after your loan settles.

What Are Mortgage Broker Fees?

Broker fees represent the payment for professional credit assistance and loan management. Brokers act as licenced experts connecting you with the right Australian lenders.

Lenders reward brokers for finding new customers and managing the complex application process. This system ensures you receive expert guidance without paying a traditional consulting fee. Consequently, the lender pays the broker so you don’t have to.

Why Do Brokers Receive Commissions?

Brokers spend hours researching loan options and calculating your borrowing capacity. They handle the heavy paperwork and liaise with banks until settlement.

Lenders cover these costs as part of their customer acquisition strategy. This payment is similar to what banks pay their own internal loan officers. Most importantly, this commission does not increase your interest rate. Authoritative ASIC data confirms that broker-negotiated rates remain competitive with direct bank offers.

While rare, a small percentage of brokers may charge a direct “fee for service.” However, the standard commission model remains the most common choice for first-home buyers. This structure keeps brokers motivated to find you the best long-term mortgage deal.

Types Of Mortgage Broker Fee Structures

Not all broker fees work the same way. While most Australian brokers rely on lender-paid commissions, you should understand the different structures you might encounter.

How Do Brokers Get Paid?

Lenders typically pay brokers for the work involved in sourcing and managing your loan. This allows you to access expert advice without a direct service fee. Below are the industry averages for broker commissions in 2026.

| Payment Type | Industry Average Rate | Example ($500,000 Loan) | Paid By |

| Upfront Commission | 0.65% – 0.70% (+ GST) | $3,250 – $3,500 | Lender |

| Trailing Commission | 0.15% – 0.20% (+ GST) | $750 – $1,000 (per year) | Lender |

| Brokerage Fee | $0 (Standard) | $0 | Borrower |

Upfront and Trailing Commissions

Lenders pay the Upfront Commission shortly after your loan settles. This is a one-off payment for the broker’s work in preparing and submitting your application. By law, your broker must disclose the exact dollar amount in your Credit Proposal Disclosure.

The Trailing Commission is an ongoing monthly payment. Lenders pay this based on your remaining loan balance. This payment incentivises your broker to provide “life-of-loan” support, such as helping with rate reviews. If you refinance or pay off the loan, this payment stops immediately.

Brokerage Fee (Borrower-Paid)

Most Australian brokers do not charge customers directly. In fact, MFAA data shows the vast majority of brokerages offer their services for $0. However, a small minority may charge.:

- Complex Scenarios: Specialist loans requiring extensive manual work.

- Small Loans: When the commission does not cover the broker’s operational costs.

- Fee-for-Service: Some independent brokers rebate all commissions and charge a flat fee.

Always check your Credit Quote early to confirm if any out-of-pocket fees apply to your journey.

Hidden Costs and Clawbacks

Brokers must remain transparent, but “indirect costs” like Clawback Fees can surprise borrowers. Lenders pay commissions expecting the loan to stay active for at least two years. If you refinance or close the loan too early, the lender “claws back” the commission from the broker.

- Year 1: Lenders often reclaim 100% of the commission.

- Year 2: Lenders typically reclaim 50% of the commission.

While most brokers accept this as a business risk, some include a clause in their contract. This may require you to reimburse them for the clawed-back amount. We recommend asking your broker about their clawback policy before you sign your agreement.

Case Study: How Alex Bought A Brisbane Apartment For $0 In Broker Fees

Meet Alex, a first-home buyer in Brisbane. He saved a solid deposit for a $600,000 apartment. Because he has a 20% deposit, he avoids Lenders Mortgage Insurance (LMI).

Alex needs a $480,000 home loan. He decides to use a mortgage broker recommended by a friend. Naturally, Alex asks: “How much will your service cost me?”

The Initial Consultation and Loan Choice

The broker explains there is no direct fee for their service. Instead, the lender pays a commission after the loan settles.

Alex’s broker compares options from a panel of over 30 lenders. They identify a major bank offering a competitive rate and $0 application fees. The broker even negotiates to waive the $395 annual package fee.

Breaking Down the Broker Commission

The chosen bank pays the broker an upfront commission of 0.65% (plus GST). They also pay a 0.15% (plus GST) annual trailing commission.

- Upfront Payment: The bank pays the broker $3,432 at settlement.

- Ongoing Trail: The broker earns roughly $59 per month in the first year.

Alex pays none of these costs. The lender covers everything as a business expense. Consequently, Alex receives expert guidance and paperwork support for free.

Best Interests Duty in Action

Transparency is key to a successful loan journey. Alex receives a disclosure document detailing the exact commission amounts.

He notices another lender offered a higher commission of $3,600. However, that loan had a much higher interest rate. The broker prioritised Alex’s savings over their own pay. This move aligns with the Best Interests Duty (BID) legal requirement for brokers.

Long-Term Support and Passive Savings

Fast forward three years into the mortgage. Alex has paid his loan down to $440,000. The broker still receives a trail commission, now roughly $660 per year.

In exchange, the broker provides proactive service:

- They monitor interest rate movements regularly.

- They recently negotiated a 0.20% rate reduction with the bank.

- They ensure Alex’s loan features, like the offset account, remain effective.

The Outcome: A Win-Win for First-Home Buyers

Alex successfully secured his first home with lower fees and a better rate. He paid $0 in broker fees throughout the entire process.

The broker earned a fair commission for their expertise and ongoing management. This typical Australian model ensures first-home buyers get professional help without added financial stress.

Lender-Paid vs. Borrower-Paid Mortgage Broker Fees

In Australia, lender-paid commissions are the standard. This differs from countries like the US, where borrowers often pay points directly. Understanding these two models helps you navigate the market with confidence.

The Lender-Paid (Commission) Model

The primary advantage of the lender-paid model is the independence it provides you. Because the lender covers the broker’s payment, you receive professional advocacy without a direct service fee. This model grew rapidly in the 1990s to improve market competition.

Unlike bank staff, brokers remain independent of any one bank’s sales targets. This freedom allows them to prioritise your needs over a specific lender’s monthly quotas. Essentially, you hire an expert negotiator who works for you, but the bank picks up the bill.

Lenders view these commissions as a strategic customer acquisition cost. Consequently, they do not add this cost to your interest rate. In fact, an ASIC report confirms that broker-negotiated rates match or beat direct bank offers.

If you visit a bank, they pay a loan officer a salary. If you use a broker, they pay a commission instead. Either way, the bank pays to secure your business. Using a broker simply ensures you have an advocate throughout that process.

The Borrower-Paid (Fee for Service) Model

A “fee-for-service” model is uncommon but does exist. Some independent brokers charge a flat fee and rebate the lender’s commission to you.

This model typically applies to:

- Sophisticated investors with complex portfolios.

- Very small loans that don’t generate enough commission.

- Specialist private lenders who do not pay broker commissions.

Always check your Credit Quote for potential fees. Ask your broker: “Do you charge me directly, or does the lender pay you?”

Do Different Commissions Influence Advice?

Commission rates are remarkably similar across major Australian lenders.

Because the difference is minimal, brokers prioritise your satisfaction over tiny commission gaps. Furthermore, brokers must legally follow the Best Interests Duty. This law requires them to prioritise your financial needs above their own pay.

Industry bodies like the MFAA also enforce strict transparency standards. Lenders must disclose any “soft dollar” benefits, such as gifts or trips. Most professional brokers have moved away from these to avoid conflicts.

Aggregator Influence and Ownership

Your broker likely belongs to a larger aggregator or franchise network. Aggregators provide brokers with access to a wide panel of lenders.

Sometimes, a major bank owns a stake in an aggregator. While this might encourage brand familiarity, it cannot override the law. Your broker must still recommend the best product for your specific situation.

You can ask your broker if they have any ownership ties. A transparent broker will gladly explain their network structure.

The Bottom Line on Broker Pay

The standard Australian model means you pay nothing directly. The lender pays the broker, and you get expert support.

By law, your broker provides a Credit Proposal Disclosure. This document shows the exact dollar amount the lender pays them. This level of transparency ensures you are never kept in the dark.

Case Study 2: A Broker Charges A Fee for A Complex Scenario

While most first-home buyers pay $0, some unique situations require a “fee-for-service” model. This usually happens when a loan requires extensive manual work or falls outside standard lending criteria.

The Scenario: Charlotte’s Complex Employment

Charlotte is a self-employed contractor with only one year of tax returns. She is also a first-home buyer looking to purchase a $500,000 property. Most major banks require at least two years of financial history for self-employed applicants.

Charlotte’s broker identifies a specialist “alt-doc” lender that accepts her specific financial situation. However, this specialist lender does not pay a standard commission to brokers.

The Fee Structure

Because the lender pays no commission, the broker charges Charlotte a one-off professional service fee of $2,500. The broker discloses this fee upfront in a Credit Quote before Charlotte signs any documents. This ensures total transparency about the costs involved.

Why the Fee Was Worth It

Charlotte agrees to the fee because her alternative was waiting another year to enter the property market. During that time, property prices in her area were rising by roughly 5% annually.

The broker’s expertise provided several benefits:

- Access to Niche Lenders: The broker found a lender Charlotte could not access through a standard bank branch.

- Policy Knowledge: They knew exactly which lender would accept one year of financials without a “decline” affecting her credit score.

- Strategic Application: The broker packaged Charlotte’s bank statements to prove her income consistency and ability to service the loan.

The Outcome

Charlotte secured her home loan and settled on her property successfully. While she paid a $2,500 fee out of pocket, she avoided a potential $25,000 price increase if she had waited another year.

This case demonstrates that a broker fee can sometimes be a strategic investment. It provides access to credit for borrowers who do not fit the “standard” bank mold. Always ensure your broker justifies any direct fees with a clear explanation of the extra value provided.

Check to see if you are eligible for a home loan

Mortgage Broker vs. Going Direct To A Bank

Choosing between a broker and a bank is a major decision for first-home buyers. Both paths offer different experiences, but the financial outcome is often surprisingly similar. Let’s compare the costs and benefits to help you decide.

Cost Comparison: Broker Fees vs. Bank Fees

Using a mortgage broker generally adds zero extra cost to your loan application. As we noted, lenders pay brokers via commission rather than charging you a service fee.

If you go directly to a bank, you still face standard bank charges. Here are the common costs you will encounter:

- Application or Establishment Fees: Lenders often charge between $0 and $800 to set up a loan. Brokers frequently negotiate with bank managers to waive these fees entirely for their clients.

- Annual Package Fees: Many “all-in-one” loans cost $300 to $400 per year. These fees remain the same whether you use a broker or go direct.

- Valuation Fees: Some banks charge to assess your new property’s value. A broker can often find lenders who offer free valuations as a promotion.

Will You Get A Better Interest Rate?

A common myth suggests banks charge higher rates to cover broker commissions. This is simply not true.

In fact, ASIC research shows broker customers receive interest rates equivalent to or better than direct bank customers. Banks value broker business because it reduces their own marketing and staffing overheads.

If you walk into one bank, you receive one quote. Conversely, a broker compares dozens of lenders to find the lowest rate available. They often access “broker-only” specials that banks don’t advertise to the general public.

The Summary: Which is Cheaper?

For most Australian home buyers, using a broker is cost-neutral or even saves money. You benefit from their negotiation power and industry relationships without paying for their time.

Unless a broker charges a specific “fee-for-service” for complex cases, they remain a free resource. They provide expert guidance while the lender picks up the tab.

Pros Of Using A Mortgage Broker

Beyond saving you from direct professional fees, mortgage brokers offer several strategic advantages. Here is why most Australian home buyers choose the broker path.

1. Access to a Massive Lender Panel

A broker acts as your one-stop shop for comparing home loans. Instead of calling five different banks, you gain access to over 30 lenders at once.

Brokers use real-time tools to compare interest rates, fees, and borrowing capacity across the market. This variety increases competition for your business. Consequently, you are more likely to find a lender that suits your unique financial situation.

2. Expert Guidance and Total Convenience

Buying your first home involves a steep learning curve. Your broker acts as a personal guide through every step.

They calculate your borrowing power and manage all communication with the bank. Furthermore, they liaise with settlement agents and real estate agents to ensure a smooth process. At Hunter Galloway, we make home ownership stress-free and uncomplicated for you.

3. Strategic Loan Structuring

Brokers do more than just find low rates; they build your loan strategy. They explain the nuances of fixed versus variable rates. They also help you decide if an offset account or redraw facility fits your goals.

Your broker outlines all upcoming costs, including government fees and Lenders Mortgage Insurance (LMI). This ensures you are never caught off guard at settlement.

4. Superior Negotiation Power

Brokers maintain strong relationships with bank Business Development Managers (BDMs). They know how to negotiate sharper rates that are not advertised to the public.

If one lender offers a better deal, your broker can push your preferred bank to match it. They also track the latest cashback offers and fee waivers. This negotiation power often saves you thousands over the life of your loan.

5. Higher Approval Success Rates

Every lender has different credit policies. A broker knows which banks are more lenient toward specific employment types or expenses.

They package your application professionally to highlight your strengths. By matching you with the right lender first, they prevent unnecessary credit declines. This expertise is a lifesaver for buyers with complex financial profiles.

Why 75% of Australians Choose Brokers

Current data shows that over 74% of all new Australian home loans are written by brokers. This record-high market share proves that borrowers value choice and expert support.

The MFAA confirms that brokers are now the preferred choice for navigating complex lending environments. Clearly, the combination of $0 fees and expert advocacy offers unbeatable value for first-home buyers.

Cons And Considerations Of Using A Mortgage Broker

While using a broker offers many benefits, you should consider the potential downsides. We believe in total transparency so you can make the right choice for your mortgage.

1. Limited Lender Panels

Brokers cannot access every single lender in the Australian market. Some small credit unions or boutique banks only deal with customers directly.

If you want a specific “direct-only” product, a broker might not be able to help. However, most brokers have a panel of over 30 lenders. This usually covers the vast majority of competitive home loans. Always ask your broker for their lender list to ensure a broad selection.

2. Managing Potential Conflicts of Interest

The commission system could theoretically influence a broker’s advice. Some lenders might offer slightly higher commissions than others.

Fortunately, as we’ve mentioned before, the Best Interests Duty (BID) now makes it illegal for brokers to prioritise commissions over your needs. Good brokers rely on long-term referrals and happy clients. Consequently, they focus on finding you the best deal rather than chasing a small commission bump.

3. Varying Service Quality

Like any industry, the skill levels of individual brokers vary. An inexperienced broker might struggle with complex applications or provide poor advice.

To mitigate this risk, research your broker’s reputation and reviews. Ensure they are members of professional bodies like the MFAA or FBAA. Furthermore, check that they hold a valid Australian Credit Licence (ACL). Choosing an expert firm ensures you receive high-quality guidance.

4. Documentation Is Still Required

Some buyers believe a broker removes all the work. You must still provide payslips, bank statements, and identification.

A broker cannot bypass these lender requirements. However, they do manage the paperwork once you provide the files. They package your application professionally to improve your chances of success. This simplifies the process, but you remain an active participant.

5. Extra Communication Layers

Adding a middleman can occasionally slow down communication. If the bank needs more info, they tell the broker, who then contacts you.

This extra step might cause minor delays if the broker is not proactive. Most expert brokers use automated systems to keep you updated in real-time. If you prefer direct control over every bank interaction, going direct might suit you better.

6. Brokers Don't Control Final Approval

A broker facilitates the loan but cannot approve it themselves. The final decision always rests with the lender’s credit team.

If your financial profile doesn’t meet bank criteria, a broker cannot force an approval. However, they do pre-empt potential issues before you apply. This strategic matching significantly increases your odds of a “yes” compared to applying blindly yourself.

Pros Of Going Direct To A Bank

While most Australians choose brokers, some borrowers prefer dealing directly with their bank. There are specific situations where this path might feel more comfortable for you.

1. Leveraging Existing Banking Relationships

You might already have a strong history with a specific bank. Private banking clients often enjoy personalised service from a dedicated bank manager.

Dealing directly allows you to build on that established trust. However, you can often still use a broker to access your own bank’s products. This gives you professional advocacy while maintaining your existing banking relationship

2. Access to Exclusive Retention Offers

Some banks offer “loyalty discounts” to keep their current customers. Occasionally, these special rates are not published to the broader broker network.

If you have significant assets with one lender, you might negotiate a unique deal. While brokers can usually match these offers, a direct conversation sometimes yields a tiny benefit. These cases are rare, but they do happen for long-term loyal customers.

3. Direct Communication and Privacy

Going direct means you speak straight to the lender’s staff. Some borrowers feel this makes communication faster because it removes the middleman.

Privacy is another factor for some individuals. If you are very private, you might prefer sharing financial data with only one institution. Keep in mind that both brokers and banks must follow strict Australian privacy laws.

The Reality of Direct Bank Approvals

Dealing with a bank manager doesn’t always mean faster approval times. Banks follow the same internal credit assessment processes for all applications.

In fact, some lenders prioritise the broker channel to manage high application volumes. You won’t receive a “discount” or rebate for cutting out the broker. The bank simply keeps the money they would have paid in commission.

Which Path Should You Choose?

Using a broker is usually the best move for first-home buyers. You get expert support, more choices, and $0 professional fees.

Going direct makes sense if you are 100% certain one bank is your best option. However, a broker might find a better loan elsewhere that saves you thousands. Ultimately, brokers save you time by doing the comparison work for you.

Legal And Regulatory Insights On Mortgage Broker Fees

The Australian mortgage broking industry operates under strict regulations. These laws ensure brokers act ethically and remain transparent about their pay.

Following the 2018 Royal Commission, significant reforms transformed how brokers serve you. These changes provide powerful protections for every borrower.

The Best Interests Duty (BID)

Since January 2021, brokers must legally follow the Best Interests Duty. This law requires brokers to put your interests ahead of their own.

Your broker cannot recommend a loan just to earn a higher commission. If a conflict of interest exists, they must resolve it in your favour. This duty ensures you receive the best mortgage for your specific needs.

Mandatory Disclosure of Commissions and Fees

Transparency is a legal requirement in Australia. Your broker must provide several key documents throughout the process:

- Credit Guide: This document lists their licence details and lender panel.

- Credit Proposal Disclosure: This shows the exact dollar amount the broker earns from your loan.

- Ownership Disclosure: Brokers must reveal if a bank or aggregator owns their business.

These disclosures prevent “hidden” costs from surfacing later. You will always know exactly what your broker earns from the lender.

Eliminating "Soft Dollar" Incentives

In the past, lenders offered brokers bonus trips or expensive gifts. Today, the industry has banned or strictly limited these “soft dollar” benefits.

Lenders also cannot pay volume-based bonuses for hitting sales targets. Consequently, commissions remain the primary way brokers are paid. This shift reduces potential bias and keeps the focus on your loan.

Royal Commission Recommendations: What Changed?

The Hayne Royal Commission originally suggested a “borrower-pays” model. This would have forced you to pay your broker directly.

However, the government rejected this to keep the industry competitive. Instead, they bolstered regulations while maintaining the lender-paid commission model. This decision ensures first-home buyers still access expert advice for $0 upfront.

Industry Standards and Licensing

All brokers must operate under the National Consumer Credit Protection (NCCP) Act. They must hold an Australian Credit Licence or be a registered representative.

You can verify your broker’s details on the ASIC Professional Registers. Furthermore, most reputable brokers belong to the MFAA or FBAA. These bodies enforce high codes of practice and ongoing education.

Your Rights and Protections

If you ever feel overcharged or misled, you have clear avenues for help. Brokers must belong to the Australian Financial Complaints Authority (AFCA).

AFCA provides a free service to resolve disputes between consumers and financial firms. This ensures you have a voice if things go wrong.

Consumer Protections Summary

As a first-home buyer, you enjoy these core protections:

- Full Transparency: You see all commission dollar amounts upfront.

- Legal Advocacy: Your broker must prioritise your financial goals.

- Standardised Pay: Commission rates are similar across most lenders.

- Dispute Resolution: You have free access to AFCA for complaints.

You can move forward confidently with a licensed mortgage broker. They have clear legal duties to you, and their pay is fully regulated.

Would you like to learn about your situation?

Common Myths And Misconceptions About Mortgage Broker Fees

Misunderstandings about how brokers earn money can hold you back from getting a great deal. We want to clear the air by tackling the most common myths head-on.

Myth 1: Mortgage brokers are always free.

The Reality: Most brokers are free for borrowers, but exceptions exist. Generally, lenders pay commissions so you don’t have to pay out of pocket.

However, some brokers charge fees for complex scenarios or very small loans. If a broker charges a fee, they must disclose it in a Credit Quote. Always check for any upfront costs before you start the process.

Myth 2: All brokers get paid exactly the same way.

The Reality: Most brokers receive upfront and trail commissions, but business models vary. While the structure is similar, different lenders pay slightly different rates.

Additionally, a small minority of brokers use a “fee-for-service” model. Some might even rebate commissions back to the client. Understanding your specific broker’s approach ensures there are no surprises during your journey.

Myth 3: Using a broker costs more than going direct to a bank.

The Reality: Using a broker is usually cost-neutral or even cheaper than a bank. Lenders do not penalize you for using a broker.

Banks treat commissions as a marketing and distribution expense. Consequently, interest rates for broker-led loans are on par with direct bank offers. In many cases, brokers find lower rates that you might miss on your own.

Myth 4: I can negotiate a better rate if I cut out the broker.

The Reality: Brokers are professional negotiators with access to “bottom-line” rates. They know exactly how much “wiggle room” a lender has at any given time.

As an individual, you may not know the bank’s lowest possible offer. Furthermore, some wholesale lenders only offer their best rates through the broker channel. Cutting out the middleman could actually mean leaving money on the table.

Myth 5: Brokers only recommend loans that pay them the most.

The Reality: This is now illegal under the Best Interests Duty (BID). Brokers must legally prioritise your financial needs over their own commission.

Moreover, commission rates across major Australian lenders are very similar. A broker’s long-term success depends on your satisfaction and future referrals. Recommending a bad loan for a tiny commission bump would destroy their reputation and business.

The "Loyalty Tax" Warning

Staying with one bank too long often leads to a “loyalty tax.” Banks rarely offer their best rates to existing customers without being prompted.

Your broker provides “life-of-loan” service by monitoring your rate regularly. They proactively request rate reviews or suggest refinancing when it benefits you. This ongoing support can save you thousands of dollars over the years.

Conclusion: Navigating Your First-Home Loan with Confidence

We’ve unpacked the complexities of broker compensation to give you peace of mind. Here is a summary of what we learned:

- Lenders Pay the Professional: In most cases, you pay $0 out of pocket. Lenders pay brokers commissions for securing your business and managing the paperwork.

- Commissions Don’t Raise Rates: Upfront and trail commissions come from the lender’s margin. They do not increase your interest rate or loan costs.

- Total Transparency is Mandatory: Any broker-charged fees must be disclosed upfront. While rare for first-home buyers, transparency ensures there are no surprises.

- Brokers Drive Competition: Using a broker is often cost-positive. They find lower fees and negotiate better rates by making lenders fight for your loan.

- Legal Protections Exist: The Best Interests Duty ensures brokers prioritise your needs. Modern regulations strictly oversee commissions to prevent conflicts of interest.

Your Journey, Your Control

Common fears about “hidden fees” or biased advice are largely unfounded in today’s regulated market. With roughly 75% of Australians choosing brokers, it is clear where the value lies.

As a first-home buyer, you should feel comfortable asking questions. A good broker will gladly explain exactly how they get paid. Remember, you are in the driver’s seat. If a recommendation doesn’t feel right, you can always walk away.

Knowledge is Power

Ultimately, the goal is securing a loan that fits your budget and long-term goals. Whether you choose a broker or go direct, you now have the knowledge to discuss fees with confidence. Thousands of Australians have successfully entered the property market using brokers to simplify the process and save money. You can too.

Why Choose Hunter Galloway?

At Hunter Galloway, our services are completely free for all home loan and investment loan clients — the lender pays our commission once your loan settles, so you pay nothing for our guidance or application work.

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please* give us a call on 1300 088 065 or* book a free assessment online to see how we can help.

Our team of home loan experts is here to help you buy a home in Australia