These are three terms that you’re almost certain to come across as you plan on buying your first home. It’s important to know what these mean.

Understand LVR, LMI and Genuine Savings

What is LVR?

LVR is the loan-to-value ratio. It is the percentage of the money you borrow for a home loan compared to the value of the property. It is calculated as the loan amount divided by the home value. The banks use LVR to determine if they will approve your home loan.

Typically, if your LVR is above 80% you will need to pay LMI or lenders mortgage insurance to cover the bank in case you default on your loan.

In the example below an $80,000 loan for a $100,000 property purchase would mean an 80% LVR. As the LVR is 80% and below it would not have LMI, or lenders mortgage insurance, payable.

An example of 80% LVR, this was calculated by dividing the loan amount of $80,000 by the home value of $100,000 times 100.

Read More: Try the LVR Calculator

What is LMI?

LMI or lenders mortgage insurance is a one-off fee payable by you, the borrower, to cover the bank–it’s insurance that covers the bank. While it benefits you by being able to buy a home with less than a 20% deposit, it doesn’t cover you and is just for the bank.

LMI stands for lenders mortgage insurance.

This cost is a sliding scale–the smaller your deposit, the more insurance you’ll pay. On a $600,000 home with a 10% deposit ($60,000), you’ll be asked to pay insurance of around $10,000.

This amount varies a lot between different banks, sometimes adding up to a significant extra cost.

Let’s look at this scenario across seven different banks:

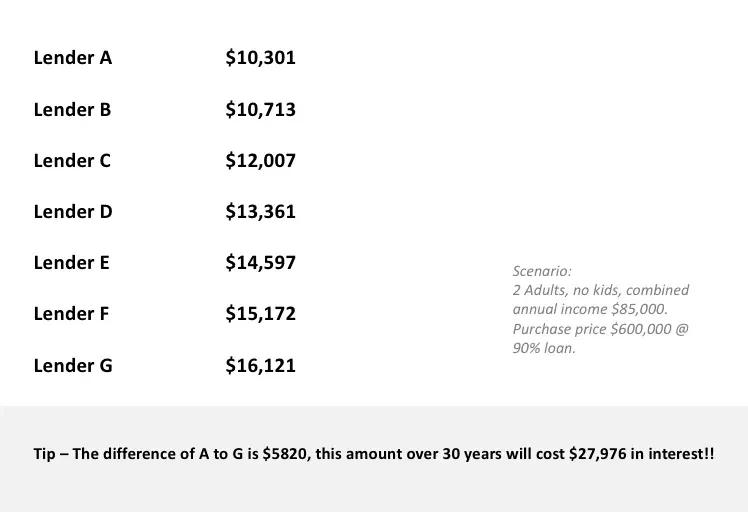

Lenders Mortgage Insurance (LMI) costs vary greatly between lenders.

As you can see, Lender A costs $10,031 in lenders mortgage insurance compared to Lender G who costs $16,121 for the exact same borrower, and same purchase amount.

That’s almost $6,000 in extra costs!

The best way to get around this is to look at different lenders or ask your mortgage broker to compare not only the rate but the limit amount.

In some circumstances, you can arrange to have the LMI waived if you work in a certain profession. The best way to know if you’re eligible for an LMI waiver is to speak to a mortgage broker. If you want to know more about LMI and your options, get in touch with us here.

Read more: LMI Calculator – Try it out yourself!

What are genuine savings?

In recent times most lenders have introduced mandatory genuine savings policy. Genuine savings show the bank that the applicant has a bit of skin in the game, a bit of hurt money that you have saved up yourself.

Most lenders like to see 5% of the property purchase price saved in a bank account for 3 months but there are a few exceptions to this rule.

- ✅ Be currently renting, and have at least 6 months clean rental history

- ✅ Lenders consider the following forms of genuine savings

- ✅ Savings held or accumulated over 3 months

- ✅ Shares or managed funds held for 3 months or greater

- ✅ Equity in real estate or property

- ✅ Term deposits held for 3 months or greater

- ✅ Funds held in First Home Super Saver Scheme (FHSSS)

- ✅ Some lenders allow exceptions if rent has been paid for the last 3 months or greater

The majority of lenders agree on what makes up genuine savings, but where they differ is when genuine savings are required. Some lenders only need to see genuine savings if you have less than a 10% deposit (90% LVR) whereas others want to see it if you have less than a 15% deposit (over 85% LVR).

To play it safe you can assume genuine savings is required when lending over 85-90% of the property value.

The lender generally wants to see 5% of the purchase price held for 3 months or longer – in some cases (particularly for investment properties) lenders require greater than 5% of the purchase price as genuine savings.

Keep in mind that the lender only requires 5% (of the purchase price) held for 3 months or longer. Which means funds for stamp duty and other costs do not have to be held for 3 months or greater.

For example, if you’re purchasing a property for $500,000 then genuine savings of 5% of this purchase price is $25,000. You’d need to hold $25,000 for 3 months or greater to meet the genuine savings policy plus hold enough funds to cover stamp duty/other costs applicable. Also be aware that lender mortgage insurance will be applicable.

Can I use what I pay in rent as genuine savings?

If you have good rental history, some lenders will consider making an exception to the genuine savings policy and consider deposit from other sources like gifted funds from your parents that don’t need to be held for over 3 months.

To use rent as genuine savings you need to:

- ✅ Be currently renting, and have at least 6 months clean rental history

- ✅ Be currently renting via a licensed property manager (i.e. not a private rental, or living at home with your parents)

- ✅ Ensure the tenants on the lease are the same as the people who will be on the home loan application

Good news is if you can fit these criteria, the rent you have paid over the past 6 months will be considered instead of showing genuine savings and therefore you can use deposit sourced from ’non-genuine’ savings like a gift from your parents.

You will need a copy of the rental ledger, or reference letter from your property manager as evidence to use rent as genuine savings.

Read More: What is genuine savings?

If I rent, do I still need a deposit?

You will still need to provide a deposit for your home loan even if you are renting.

We recommend you have been 8-10% of the property purchase price in savings, or you can work with less if you have a guarantor.

Now that we’ve covered these few key financial terms, let’s look at your borrowing power in more detail.