As I mentioned earlier, your borrowing power is a combination of your income and your deposit. The more you can pay upfront (given you have some emergency savings kept aside) the less you’ll need to borrow, and the lower your repayments will be.

In general, people say 20% is the benchmark for a deposit, but at Hunter Galloway, we find that creditworthy borrowers with good income can get by with an 8% to 10% deposit.

We will review the full amount you will need for a deposit shortly—including stamp duty—but if we just look at the bank deposit required for a $300,000 purchase, a 5% deposit is $15,000 or a 20% deposit is $60,000

Purchase Price

$300,000

$400,000

$500,000

$750,000

5%

$15,000

$20,000

$25,000

$37,500

10%

$30,000

$40,000

$50,000

$75,000

15%

$45,000

$60,000

$75,000

$112,500

20%

$60,000

$80,000

$100,000

$150,000

Tip: Keep in mind that settlement costs, like stamp duty, and other fees, like mortgage registration and bank fees, can add thousands of dollars to your total upfront costs and are typically around 0.5 – 1% for first home buyers in Brisbane or 2 – 5% for regular home buyers.

Aim to have about 8-10% of the property purchase price in savings.

Your deposit is usually payable in two parts. Your holding deposit is paid when the contract is signed. This is usually $1,000 to $5,000. The balance of the deposit (the bank deposit) is payable on finance approval. This is usually 5-10%.

Not everyone has this amount of money saved up. If that’s you, don’t stress too much. Your dreams of owning a home don’t need to come to an end just yet—it is possible to buy a home with a small deposit, or even no deposit at all!Here’s how:

How to Buy With No Deposit at All

If you have a strong income, and not a lot of savings, it might be possible for you to buy without any deposit at all.In fact, in some situations, you can borrow up to 105% of the purchase price.

Here are some ways that you can buy a home without a deposit:

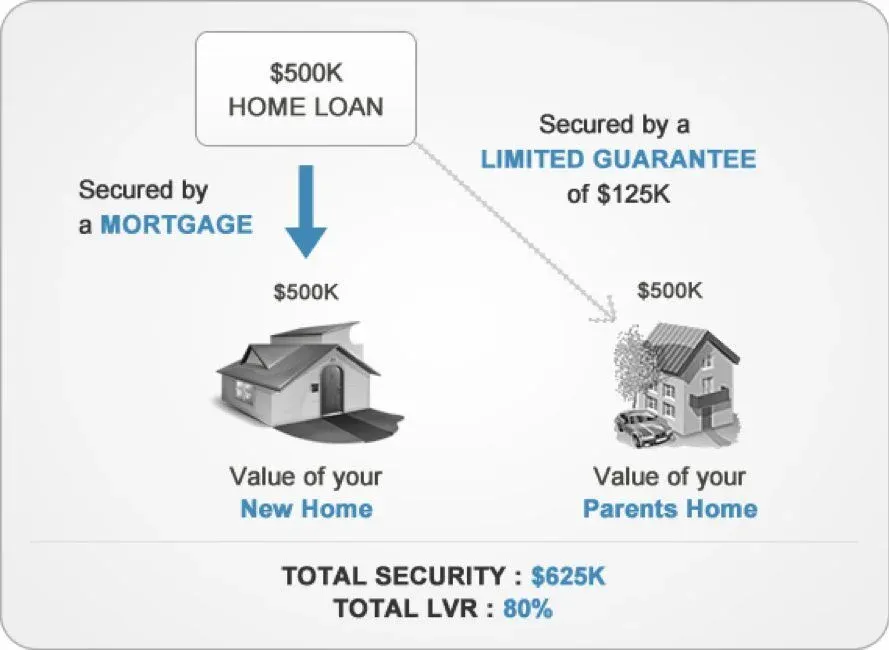

Buying a property with your parents as a guarantor lets you borrow up to 105% of the purchase price! This means you don’t need any savings as your parents provide a guarantee secured on their property.

The idea is for you to get into the property market sooner. Once you have paid off part of your loan or your property has increased in value you can remove the guarantee.Guarantor loans have become very popular in recent years as they cost less than standard home loans, they allow you to buy without a deposit and some lenders now allow you to limit the size of the guarantee.

For example, if you want to buy a house, you ask your parents for help. They might not have enough cash to offer, but you can use their house as security. This method was not allowed in the past, but now a number of lenders have introduced policies that allow a person to use another property as a security.

Example of a typical guarantor home loan structure

They allow your immediate family members to offer their house as a co-security. In other words, the financial institution will accept that property as a substitute for a cash deposit.

Using the property as co-security has its pros and cons. The advantage of using this policy is that there is no need for mortgage insurance, which saves a lot of money. On the other hand, the drawback of signing up for this policy is that your immediate family members get stuck with you.

They are eventually released from this obligation once you pay down the loan amount or if the value of property increases. This option will allow you to buy a home with no deposit if you are buying a home for the first time and entitled to get a first home owners’ grant. It will also enable you to cover your costs, such as legal expenses or transfer costs.

Around 50 – 60% of first home buyers receive help from their parents; gifted funds work if your parents can give you 5 – 15% of the purchase price. And while this isn’t available for everyone, it might help you get your foot in the door.

In Queensland, you may be eligible for the first home owners’ grant which is currently $15,000 that the government will give you towards your first home purchase.

To be eligible you need to be a first home owner, and you need to either buy or build a brand-new home that is below $750,000. The good news is you can use this $15,000 towards your deposit! So, for example, on a $300,000 property, you need to provide 5% deposit, or $15,000—so the first home owners’ grant can help you get into the property market without any deposit at all.

The QLD first home owners’ grant is still $15,000 and can be used towards brand-new purchases (or constructions).

Bear in mind that when you apply for a no deposit home loan, lenders apply very strict criteria, including having good credit, with a well-maintained repayment history, stable income sources such as a regular job and consistent payments, as well as a common property type—banks don’t like strange properties like caravans or removable houses.

If you are planning on using one of the options above, make sure to sort out your finances as early as possible. If you are relying on a deposit being gifted from your parents, getting a guarantor loan or relying on the first home owners’ grant, there can be a bit of back and forth to have the funds available and ready in time for settlement. You’re much better off being prepared and avoiding the stress of worrying if the money is going to make it into your bank account in time.

A bank might be able to lend you a large amount but should you borrow it all? This is the reality: it’s not always about what you can borrow but what you should borrow.

Understanding what you should borrow is important so you can continue to live within your means and still have some spare cash left over for your weekly avo on toast!

There are a number of added costs when it comes to buying a house besides stamp duty and other settlement costs and fees, such as council and water rates, maintenance and repairs, and the added risk of interest rates rising.

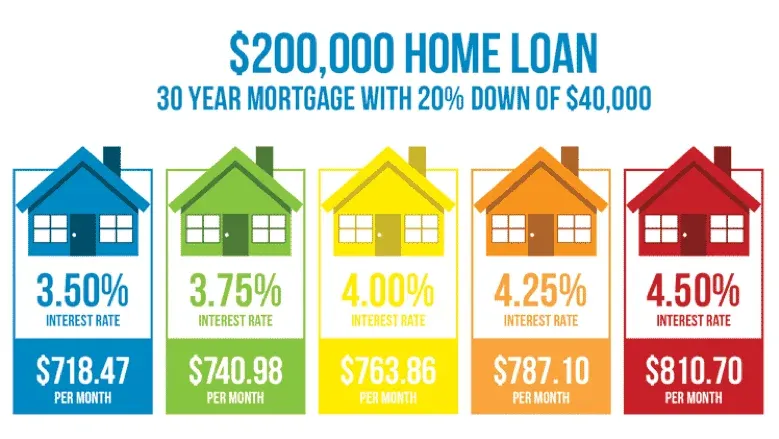

As you can see above, based on a relatively small mortgage of $200,000 a 1% increase in interest rate will increase repayments by almost $100 per month or over a 10% increase in the total repayment amount.

If you borrow too much, you run the risk of overextending and getting the wrong home loan.

I personally found it hard to accept how expensive some properties were when I first started looking—and this is completely common and normal.

Every home buyer knows the feeling—you’re looking for a home that fits your budget, but there’s that much more expensive property that looks so much more appealing!

Your first home doesn’t need to be your home forever.

Buying a home that’s way out of your price range could well derail your finances in the future. It’s human nature for us to want a little more than we can afford, and there’s always a real estate agent who’ll talk you to the next level.

But don’t be tempted—the bank has usually offered you a borrowing limit for good reasons based on your ability to repay the loan.

Spending more than you can sensibly afford leaves you exposed to potential financial shocks, including rises in interest rates. You must also allow for changes in your future circumstances.

I’ll show you how to “have your smashed avo and eat it too” in the SEARCH section of the book. You’ll learn how to set up your property search for success, including how to expand your search to find a house that gives you everything you need without a big price tag.

For now, just keep in mind that there’s no sense sacrificial your financial and mental health for that “perfect” house. If you can come up with a reasonable budget now—and you stick to it— you can focus on houses within your budget and avoid the heartbreak.