Are you wondering what the process of buying a home for the first time in Australia looks like? Buying your first property is exciting, but it also comes with challenges like budgeting, understanding government grants, and planning for ongoing costs. This guide, written by an expert mortgage broker, will walk you through the step by step home buying process, show you strategies to stay within budget, and explain how to prepare for life after settlement. By the end, you’ll have the knowledge and confidence to make smart decisions on your first home purchase.

Let’s dive in

Quick Summary

Step 1. Decide to Buy: Evaluate if it’s the right time for you to buy a house versus renting.

Step 2. Consult a Broker: Determine your borrowing capacity and additional costs like stamp duty and fees.

Step 3. Government Grants: Determine Which Government Grants You Qualify For

Step 4. Choose a Home Loan: Work with a broker to find the best loan for your needs.

Step 5. Get Pre-approval: Secure a preliminary loan approval to strengthen your offers.

Step 6. Find the Right House: List essential features and research properties.

Step 7.Research: Check property prices and get flood reports.

Step 8. Inspect: Conduct thorough physical inspections and use checklists.

Step 9. Make an Offer: Use a straightforward template to submit offers.

Step 10. Hire a Conveyancer: Ensure legal protection in the buying process.

Step 11: Ask Questions: Ask some questions before signing contract of sale

Step 12. Sign Contract of Sale: Review and understand all terms and conditions.

Step 13. Sign Loan Contracts: Finalise your loan and property transfer.

Step 14. Move In: Arrange movers and take possession of your new home.

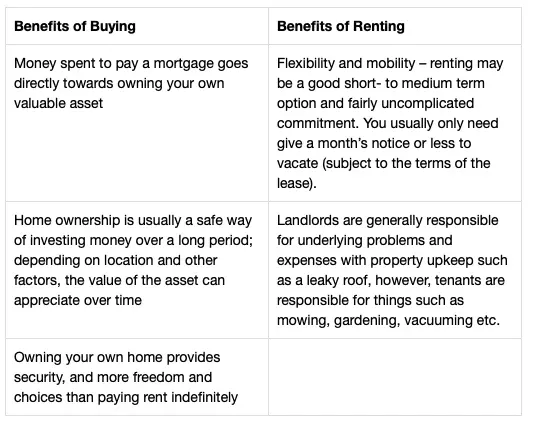

Step 1. How To Buy A House: Decide It's Time To Buy

Buying a house isn’t easy. It can be a long and expensive process—sometimes taking up to 12 months. On the other hand, owning a house is an incredibly rewarding experience.

It can help you build equity in a property, grow your wealth and give you security in owning your own place.

The first step in all this is just deciding if it’s time to buy, if it’s time to invest in property or if it’s better to keep renting.

Should I buy or should I rent? Each has its own benefits.

Realistically, there is no right or wrong answer for anyone; it is up to your personal preference… But the first step to buying a house is deciding you are ready to buy!

However, if you live somewhere where property prices are unaffordable, there is another strategy you can consider. This strategy is called Rentvesting and allows you to buy where you can afford whilst living where you like – giving you the best of both worlds.

Step 2. Talk To A Broker And See How Much You Can Borrow

A broker will help you determine how much you can borrow.

Sitting down with a broker is a smart next step. A broker can tell you how much you can borrow and factor in all the extra costs of buying a home, like stamp duty, solicitor fees, and other necessary expenses.

A Brisbane mortgage broker will help you determine your home-buying capacity. For example, if you’re buying an $800,000 home in Queensland, the additional costs in 2025 can come to around $20,000. This includes stamp duty, transfer duty, solicitor fees, and other miscellaneous charges.

So, in total, you’d need $820,000 to purchase the home. This means you need a 5% deposit ($40,000) plus the $20,000 in extra costs, giving a minimum savings requirement of around $60,000.

Talking with a broker can also make you aware of first-home buyer schemes you may be eligible for. For instance, you might qualify for a grant on a brand-new property, or you may be able to use the Home Guarantee Scheme to avoid paying Lenders Mortgage Insurance (LMI). We will cover these in more detail in a later section.

This quick conversation with a broker gives you a clear picture of your budget, repayments, and ongoing costs, ensuring your first home purchase fits comfortably within your finances.

Test Your Budget: Avoid Mortgage Stress

Buying a home is exciting, but it can also stretch your finances. Without planning, repayments may quickly become overwhelming. Mortgage stress happens when too much of your income goes to repayments. Financial experts suggest keeping housing costs below 30% of your income.

What Mortgage Stress Looks Like

Single income earner: On $80,000 a year, repayments above $2,000 a month can create pressure. This leaves little room for savings or emergencies.

Dual income couple: Earning $150,000 combined, higher repayments may feel manageable until interest rates rise. A sudden increase can quickly change affordability.

Unexpected costs: A car repair or medical bill can tip budgets into stress. Even small surprise expenses can disrupt your financial stability.

Why First Homebuyers Need to Be Careful

Many first homebuyers underestimate ongoing costs like insurance, utilities, and council rates. These small expenses add up and can increase your financial pressure.

Strategies to Stay Safe

Build a buffer: Keep three to six months of expenses in savings. This cushion protects you if income drops or costs rise.

Choose flexible terms: Pick a loan with redraw or offset features. These options give you breathing room when you need it most.

Stress test your budget: Calculate repayments if rates rise by 2%. This helps you see if your loan is still affordable.

Review spending often: Cut back on non-essentials when money feels tight. Regular reviews keep your budget under control and sustainable.

Recommended Income Allocation

Household Type

Housing (max)

Living Costs

Savings & Buffer

Lifestyle Spending

Single income earner

25–30%

35–40%

15–20%

10–15%

Dual income couple

25–30%

30–35%

20%

15–20%

Family with kids

25%

40%

15%

15–20%

Use these percentages as a guide to balance your budget and avoid financial stress.

Step 3. Determine Which Government Grants You Qualify For

Government schemes and Lenders Mortgage Insurance (LMI) options can ease the burden. Understanding these programs helps you maximise savings and reduce upfront costs.

First Home Guarantee (FHBG)

The First Home Guarantee (FHBG) lets eligible buyers purchase with a deposit as low as 5%. Normally, a small deposit attracts costly Lenders Mortgage Insurance (LMI). With this scheme, the government acts as guarantor, helping you avoid LMI and save thousands.

Family Home Guarantee

The Family Home Guarantee helps single parents enter or re-enter the property market. You can buy with a deposit as little as 2%. It applies to both new and existing homes, making it a flexible option for families.

State-Based Grants

Each state offers a First Home Owner Grant (FHOG) to boost affordability. These grants generally apply to new homes, off-the-plan purchases, or significant renovations.

NSW First Home Owner Grant – $10,000 for buying or building a new property.

Victoria First Home Owner Grant – Up to $20,000 for building or buying a new home in regional Victoria.

Queensland Great Start Grant – $15,000 towards a brand-new home, unit, or townhouse.

Western Australia First Home Owner Grant – $10,000 when you build or purchase a new home.

South Australia First Home Owner Grant – $15,000 for new builds or off-the-plan homes.

Tasmania First Home Owner Grant – $30,000 for building or buying a new home.

ACT First Home Owner Grant – $7,000 for eligible new homes.

Northern Territory First Home Owner Grant – $10,000 for a new home purchase.

These grants are usually paid directly to your lender at settlement, reducing how much you need to contribute upfront.

Combining Grants and Concessions

Many first-home buyers can combine grants and concessions to boost their savings. For example, a Queensland buyer might pair the First Home Grant with stamp duty concessions. However, not all programs can be stacked, so it’s important to check eligibility and speak with a mortgage broker to maximise your benefits.

Key Tip

Every scheme has unique eligibility requirements. These may include income caps, property value limits, and residency conditions. Check the rules in your state and get advice from a mortgage broker before applying.

LMI protects the lender if you default on your home loan. It’s usually required when your deposit is less than 20%.

Ways to reduce or avoid LMI:

Use a guarantor (often a family member) to secure the loan.

Combine government schemes like the FHLD with your deposit.

Consider smaller, manageable loans within your borrowing capacity.

Example: Borrowing $800,000 with a 5% deposit ($40,000) may attract LMI of approximately $16,000. Using the First Home Guarantee could waive this cost.

Step 4. Find A Home Loan That Works For You

In the old days, there was only one type of home loan, so you didn’t have any choice in what kind of loan you got.

Nowadays, there are literally hundreds of home loans available in Australia, all with different features and benefits.

Which home loan is right for you? There are hundreds to choose from.

At this point, you have already spoken with a Mortgage Broker, so they will work on your behalf to arrange a home loan through a bank.

As we mentioned above, a mortgage broker will look at what you want to achieve and find a home loan that works for you. They will also help you

work out a price range and budget for buying a home and give you an idea of what you can spend.

When it comes to choosing the right home loan for you, it is best to use a mortgage broker. So, if you haven’t already spoken to a broker, you need to speak with one at this stage.

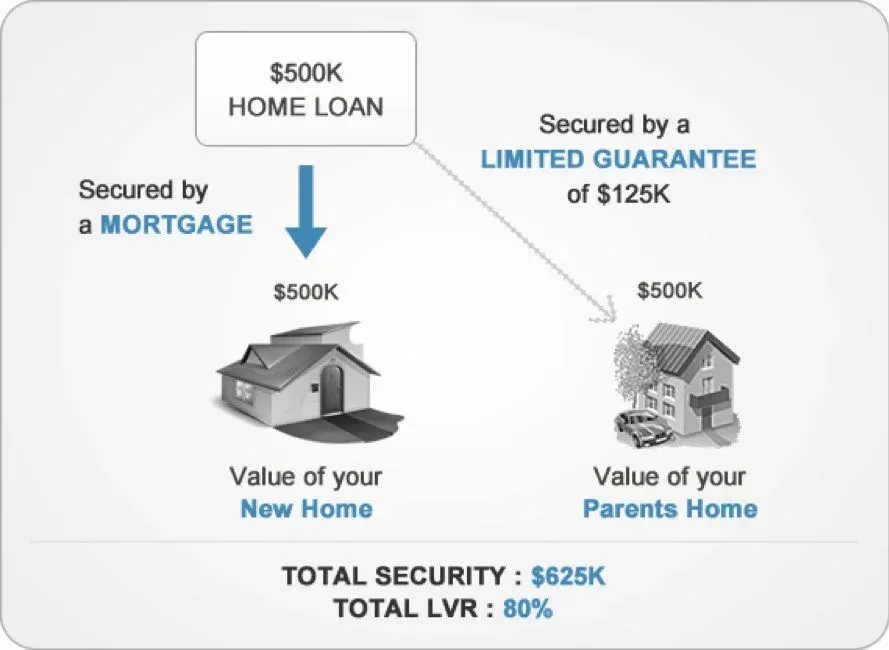

Guarantor Home Loan. Buying a property with your parents as a guarantor lets you borrow up to 105% of the purchase price! This means you don’t need any savings as your parents provide a guarantee secured on their property.

Gifted Funds. If you have a family member or relative who is willing to give you the deposit, you can buy a home effectively with no deposit!

First Home Owners Grant (Great Start Grant in Queensland) – In Queensland, you can purchase a brand new property or build a new home and receive $15,000 from the government, which can be used towards your deposit plus stamp duty benefits.

Example of a typical guarantor home loan structure

A pre approval can save the day but BEWARE! Not all pre approvals are the same.

A pre-approval is a conditional or preliminary loan approval from a bank that shows how much you can borrow. First home buyers often use it to understand their budget and make stronger offers. Depending on your lender, it may also be called conditional approval, indicative approval, approval in principle, or home seeker.

How Pre-Approval Works

To get a pre-approval, you provide your credit history and income details to your broker or lender. They review your documents and give you a clear guide on what you can afford. Essentially, it’s the bank saying they will lend you a specific amount, as long as your financial situation doesn’t change.

This helps you make competitive offers on properties and can shorten finance approval times, so you can secure your dream home faster.

Why Not All Pre-Approvals Are Reliable

Not all pre-approvals are the same. Some lenders issue system-generated approvals based only on a credit check. These are not fully reliable and may still result in your loan being declined later.

A fully assessed pre-approval is more dependable. Here, the lender verifies all your income, assets, and documents upfront, giving you confidence when buying a house.

Tips for First Home Buyers

Always ask your broker or lender if the pre-approval is fully assessed.

Check whether the pre-approval is conditional on certain documents or circumstances.

Use your pre-approval to make faster, stronger offers on properties.

Check to see if you are eligible for a home loan

Step 6. Find The Right House

Having a pre-approved loan allows you to think ahead and plan your property search wisely. This is often the hardest part of the process—trying to narrow down the type of property you want, the suburbs you like and what you want from that property.

Create a list of essential features that you definitely must have in your home. This will keep you focused on purchasing a home that is suitable for you and meets your requirements.

Property can be a largely emotional purchase, so you need to consider a few things before falling head over heels on a property:

What is your “why” for buying this property? Is it to live in, or will you rent it out in the short term? The main purpose of the property will determine the kind of property you buy.

Do you plan on staying in the property for a few years? Your first home is not likely to be your forever home; it is just your first step towards your future mansion!

Can you afford repairs and upkeep on the property? If it is an older Queenslander-style property, have you budgeted for ongoing repairs and maintenance? Will it need a new kitchen and bathroom in the short term? Will you be able to afford these costs?

If you bought the property, who would buy it from you in a few years? It’s good to start with the end in mind when buying a property. Always think about who you will sell it to in a few years. If it’s going to be a very narrow market like retirees, will this harm the property’s growth potential?

Regardless of what you intend to buy, carrying out market research is really important to identify the right price and reasonable quality of a product.

Because purchasing a home is a huge investment, you must conduct local market research to find out the current prices of the type of property you are looking for, as it will enable you to avoid paying above the market value.

You can use online tools to research the value of your home.

How to buy a house: Local Research Tools

Here are some online methods you can take to research the value of a property:

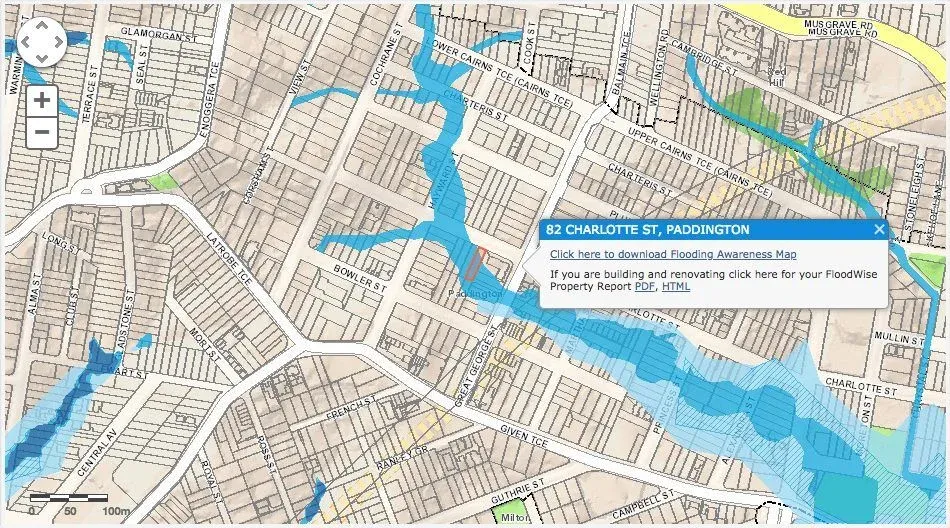

In addition to checking the value of your home, it is important to get a flood report to make sure you are not buying a property in a flood zone. If you do decide to buy the property anyway, then at least you will be aware of the risk.

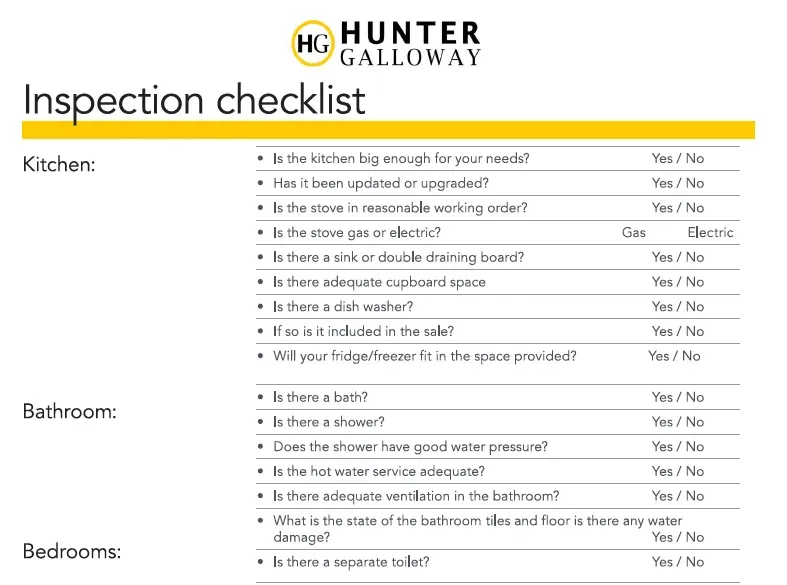

Step 8. Complete Your Property Inspection Checklist

There is no substitute for physical inspection when it comes to purchasing a home.

It allows you to see other attributes that you would have otherwise ignored while searching for a property, such as its locality.

Using a property inspection checklist can help you make sure the property ticks all your boxes.

Whenever you plan to visit a property, plan a building and pest inspection before making a purchase, as it will disclose the problems beforehand that would otherwise be costly to fix.

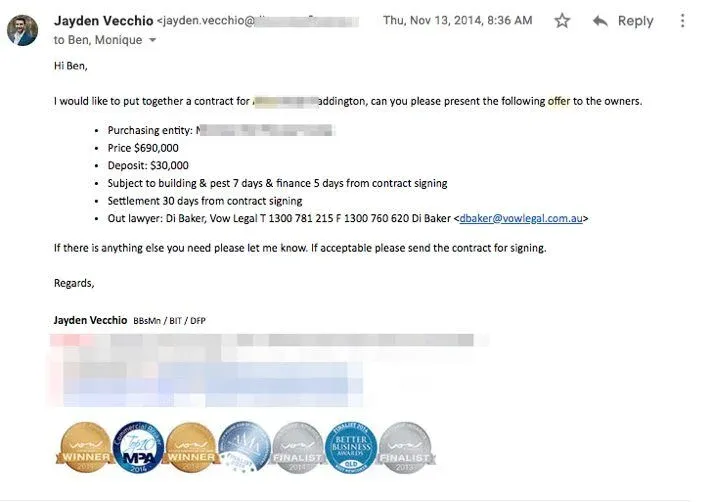

You do not need to sign a contract of sale to make an offer on a property.

If you send an offer in writing (via email, for example) you can get your offer accepted by the agent (and the sellers) before taking time to fill out the contract of sale.

You do not need to sign a contract to make an offer on a property

We have personally used this template to purchase properties in the past. It’s worth keeping your offer short and to the point, including:

Purchasing Entity: I.e. your full name, including middle names.

A conveyancer or solicitor looks after your legal interest in the home-buying process. Specifically, they will look through the contract of sale and ensure that there are protections in place to look after you.

Now, conveyancers are not going to be able to do much until you’ve identified and found the right property and you’ve got a contract you’re going to look to sign. However, it is worth being on the front foot and having them ready for that day when you need to make the call.

Our tip for a conveyancer is don’t go cheap.

When it comes to hiring a conveyancer, get the most qualified one.

It might sound like a great idea to save $200 on the conveyancer’s fees, but this can be extremely risky, especially since you are dealing with hundreds of thousands of dollars.

How to buy a house: don’t go cheap on conveyancers

We had a situation with a home buyer named Tim a couple of years ago who went really cheap. He was using a friend of a friend’s mom, who was a part-time conveyancer, to help with his first home purchase. It was all going well until the settlement day when his friend’s mom was off sick. Being the only conveyancer there, the settlement couldn’t be completed.

When it comes to choosing a conveyancer, check out their Google reviews, and if one conveyancer seems more legitimate but another one comes as recommended by a friend, it’s worth going with the safer option. You could be risking your $600,000 home over a $200 fee.

Step 11. Questions To Ask Before Signing The Contract of Sale

Ok, so you’ve made it this far, but…

Do you know what the Contract of Sale is?

The contract of sale is a legal agreement that contains terms and conditions agreed upon by both the seller and buyer in a clear manner.

It is prepared by a lawyer or in Queensland by a real estate agent and typically includes the following:

Name and address of the seller

Plan number, reference number, and address of the property

Fittings and removable items, such as appliances, blinds, or any other easily removable items, included in the sale

Deposit amount and purchase price of the property

Details about the settlement

Information about the property as to whether it is vacant or on lease

Sometimes, it includes reports, such as building inspections, pest inspections, etc.

It is very important to look at the terms and conditions of the contract before signing it as it may involve special conditions that aren’t in favour of the buyer. This is where your solicitor or conveyancer will come in.

Before signing a contract of sale, there are 5 questions you need to ask.

Keeping that in mind, here are five questions you should ask before signing a contract of sale:

Question 1: Are You Getting What You Are Looking For?

Buying a property in a real estate market doesn’t always go as planned. There are a lot of things you have to consider, and at times, you have to come to a compromise. But when you get your contract of sale, take a look at the following things.

Look at the copy of the registered plan that is normally attached to the contract and check if the property description is the same as inspected. If something doesn’t seem right on the plan, hire an independent surveyor to inspect the property and prepare a plan.

An unregistered or registered easement is what you should be looking at next. If the house has any easements, there might be restrictions on how you can use that portion of the land.

As discussed earlier, it’s important to get a clear idea about the fixtures you will be getting along with the property. These are things like light fittings, carpeting, pool equipment, stoves, blinds, or curtains. Clearly ask what is included in the contract of sale because it is not right to assume that everything you saw during the inspection will be included in the sale.

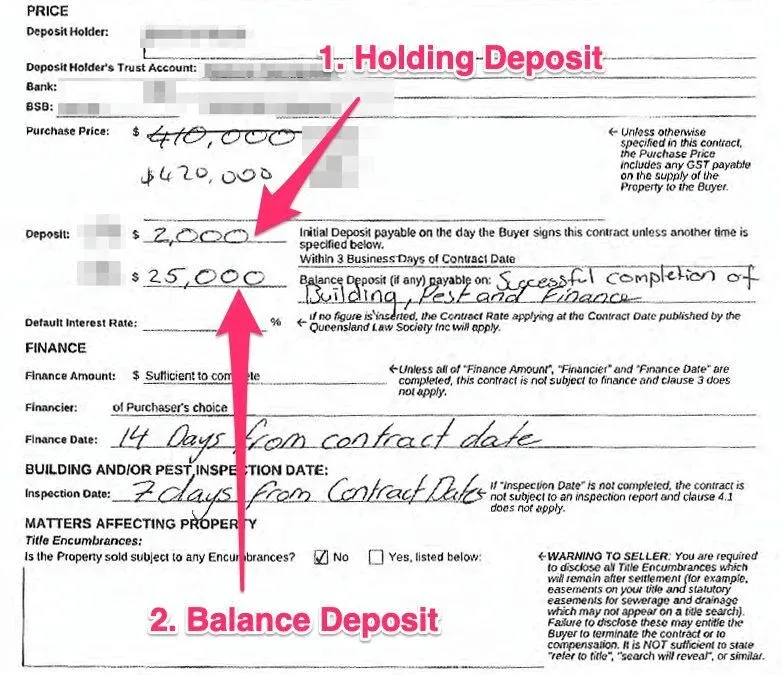

Question 2: How Much Deposit Do You Have to Pay?

This is the second question you should be asking when going ahead with the purchase. Buying a house is a big decision, and you should be fully informed before taking any steps toward it.

The amount of deposit you are required to pay will be included in the contract. In Queensland, it is divided into two parts:

The first is a holding deposit (also called the initial deposit), and is usually a small amount of $500 to $2,000 (or up to 0.25%) to secure the property.

The holding deposit shows you are serious about wanting to buy the property and needs to be paid within 3 business days of signing the contract of sale and can range from $10,000 to 5% of the purchase price…

The Deposit in Queensland is split into two parts on the contract of sale. (1) the holding deposit and (2) the balance deposit. Both need to be paid for the contract to become unconditional.

Question 3: Does the Contract of Sale Involve Any Special Conditions?

As discussed, you should definitely ask about any special conditions included in the contract of sale because these are the things you should be reading over and over again until you get a clearer picture. An example of special conditions can be things like paying a penalty to delay the settlement or a transaction being subject to tenancy.

As a buyer, you too can include special conditions in the contract, such as a satisfactory report of pest or building inspection, or sale is subject to selling your own property.

Termites are surprisingly common in Brisbane homes. So you add a building and pest condition to give you time to get a report completed.

It is crucial to choose a reasonable settlement period, keeping in mind your particular situation. For example, if you are in the process of selling your house and want to move to a new home by a particular date, it’s important to negotiate a settlement date that is suitable for you.

Normally, the settlement date can be 30 days, 60 days, or 90 days. Some sellers might not want to go with the longer settlement period, while others may not want a shorter period. So consult with your real estate agent as to what the seller’s motivation is.

Typcially settlements in Queensland are 30 days from contract signing, but you can extend this to 45 or 60 days depending on your situation (and the sellers willingness to accept it!)

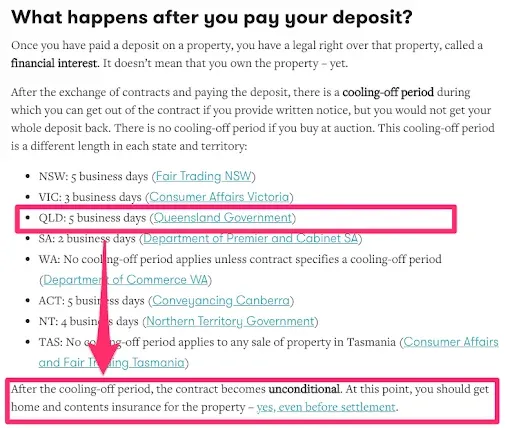

Question 5: Does the Purchase Involve Cooling Off Period?

The cooling-off period is mentioned in the contract of sale. You must be aware of what can happen if you plan to withdraw from the contract after signing it.

In Queensland, the cooling off period is 5 business days and gives you an opportunity to change your mind after signing the contract. But cooling off period does not apply when you buy a house at auction.

Also, find out about any financial penalties in case of withdrawing from the contract.

Buying a property comes with huge financial responsibility. Therefore, take your time, conduct due diligence, and ensure the terms and conditions are satisfactory. Speak to our team of experts today for more information.

If the owner likes your offer, they will accept your contract, and you will both put your names on the dotted line. The agent will contact you and say congratulations, you’ve got your new home; now it’s time to do everything else. At this point, you’ll forward your contract to your broker or conveyer.

Organise a build and pest inspection.

This is a good part of the process just for peace of mind. A building and pest inspector is a qualified Builder who’ll go and check out your new home, look in the roof, check for termites, white out damage, water damage, etc. and give you a bit of peace of mind that the place is in tip-top shape.

If they find something wrong, you can talk to your solicitor about cancelling the contract and seeing what that involves or try to negotiate the price down if it’s things that aren’t too big.

Take out insurance

Once you have paid your deposit on a property, you have legal right over the property called a financial interest… Make sure you get your insurance sorted ASAP.

From the minute you sign your contract of sale, you should take out insurance. This is because, once you sign the contract of sale, the property is now your responsibility, even if you haven’t got the keys yet. Insurance will protect the property from fire or flood damage,

Step 13. Sign Your Loan Contracts

Once you have taken all the steps mentioned above, the broker will forward a copy of the signed sale contract to a lending institution where arrangements are made for the property valuation.

If the result of the valuation is fine and other loan terms have also been met, the lender will grant full loan approval.

At this stage, the lender will grant full loan approval

This is where your broker and solicitor come into play as they transfer the property into your name and ensure the settlement occurs within a specified period.

After successful completion of the entire process, all you have to do is pack your belongings and wait for settlement (which typically takes 30 to 90 days).

Would you like to learn about your situation?

Step 14. Move Into Your New House

Woo, you made it! Time to arrange the movers and get the keys because you are now a homeowner!

Congratulations! You are now a homeowner!

Post-Purchase Planning: Budgeting Beyond the Deposit

Buying a home is just the beginning. Many first-home buyers focus on the deposit but overlook ongoing costs. Proper planning now prevents stress later.

Understand Your Ongoing Costs

Even after settlement, your home comes with recurring expenses:

Council rates: Local government charges vary by suburb and property size. Factor this into your monthly budget.

Home insurance: Protect your property from fire, flood, or storm damage. Policies differ, so compare quotes.

Strata or body corporate fees: If you buy an apartment or townhouse, these fees cover shared spaces.

Maintenance and repairs: Budget for general upkeep, small repairs, and unexpected costs like a broken hot water system.

Pay Off Your Mortgage Faster

Reducing your loan term saves interest and builds equity sooner:

Extra repayments: Add a little extra to your weekly, fortnightly, or monthly repayment. Even $50 helps.

Offset accounts: Link your savings to your mortgage to reduce interest. Your savings work harder for you.

Refinancing opportunities: Review your loan periodically. Lower rates or better features may help you save.

Plan Home Upgrades Wisely

Home improvements can increase value but strain finances if not planned:

Prioritise essential upgrades first, like plumbing or electrical safety issues.

Set a renovation budget and include a 10–15% contingency for surprises.

Avoid using credit cards or high-interest loans for renovations.

First-Year Homeownership Mini Checklist

Expense

Notes

Council rates

Estimate annual cost from your local council

Home insurance

Include building and contents coverage

Strata fees

Check quarterly or monthly obligations

Maintenance fund

Set aside 1–2% of property value

Utilities

Electricity, water, gas, internet

Emergency buffer

Keep 3–6 months of living costs

Bonus Infographic: Step-by-step Guide To Buying A House

As an added bonus, we have detailed the home-buying process in an infographic. You can use this as a checklist to help you go from finding to settling your new home.

Bonus: Tips To Buy A Home During The Affordability Crisis In Australia

Australia is currently experiencing its most severe housing affordability crisis in over two decades. Rising interest rates, escalating living costs, and stagnant incomes have made homeownership increasingly challenging for many Australians.

Mortgage Serviceability: A Growing Burden

According to ANZ, households nationwide now allocate an average of 49% of their income to service new mortgage repayments. In Sydney, this figure is even more alarming, with residents dedicating up to 74% of their income to housing costs.

Lengthening Deposit Saving Times

The time required to save for a 20% deposit has significantly increased. In Sydney and Melbourne, it now takes approximately 9–10 years, compared to 5–6 years in other capital cities.

Strategies to Enter the Property Market

Despite these challenges, several strategies can assist prospective buyers in entering the property market:

Leverage Government Schemes

First Home Guarantee: Buy with a 5% deposit, government guarantees the remaining 15%, no LMI required. (Housing Australia)

Family Home Guarantee: Single parents with a dependent child can buy with a 2% deposit. (NAB)

Regional First Home Buyer Guarantee: Buyers in regional areas can purchase with a 5% deposit. (NAB)

Consider Alternative Locations

Look beyond immediate suburbs to find more affordable options.

Emerging suburbs and regional areas may offer better value and growth potential.

Reevaluate Property Expectations

Your first home doesn’t need to be your forever home.

Choosing a unit or townhouse can help you enter the market sooner.

Building equity in a smaller property provides a stepping stone to future upgrades.

Expert Insights and Considerations

While these strategies provide pathways into homeownership, it’s essential to approach them with caution:

Market Risks: Experts warn that schemes like the Home Guarantee could inadvertently inflate property prices by increasing demand without addressing supply shortages.

Financial Implications: Buyers utilizing low-deposit loans may face higher interest rates and increased vulnerability to market fluctuations.

Long-Term Planning: Given the current economic climate, it’s crucial to assess your financial stability and long-term plans before committing to a property purchase.

Bonus: Common Mistakes To Avoid

Not getting a pre-approval.

A lot of people don’t realize that when the bank actually assesses your application, the number that you might have anticipated you could borrow can drastically change. If you’ve got a lot of over-time, unique incomes, allowances, commissions and bonuses, some lenders can take it on board, but if you’re not careful, they might not include that income, which can drastically change your borrowing ability.

So, getting a pre-approval in place is vital to knowing exactly how much you can borrow. However, you must also make sure that the pre-approval is fully accessed. You can find all the information you need to know about pre-approvals in this article.

Not understanding rentvesting

Rentvesting is purchasing a property that is in an affordable area and renting where you prefer to live. This trend continues to grow amongst young Australians, particularly because of the affordability crisis. You can literally buy an investment property way out in Perth if you’re living in Brisbane, continue living in the city in Brisbane and know that you’re getting your cake and eating it, too. You’ve got something that might be capital appreciating, where you can afford, and it won’t impact your lifestyle.

New doesn’t equal no problems.

A new house may sometimes have problems.

It can be pretty alluring to buy a brand-new property. It’s like buying a new car: You’re the first person to sit in it, and you think everything’s new, including the warranty. It makes a lot of sense, right? Not always. New buildings can have issues with concrete cancer, etc. So, you need to be diligent in checking out strata reports to make sure it’s going to make sense for you to buy new.

This is where an older block of units can be amazing. If they’ve been there for 30 years, they’ll likely be there for another 30 more.

Don’t skip the building & pest inspection

Another small mistake we see commonly made is skipping the building and pest inspection. If you can take some time off work, sit down when the Building and pest inspector is going through your new prospective home and understand what they’re seeing. If there are any issues, they’ll tell you on the spot, and you can potentially use any issues that the building and pest inspector flags to renegotiate the price down or if the issues are too big, you can walk away.

Not going through the house in detail

The building and pest inspector will not check every power point so make sure to check them yourself.

Once you buy a home, it’s your problem: The good, the bad and the ugly. With a home, you’re buying in the condition that you’re seeing it in. so if you’ve made an offer and it’s accepted, and you’ve still got your Finance clause or building and pest clause, take time to do a second inspection and go through the home in detail. Your building and pest inspector, unfortunately, isn’t going to check every power point and all the appliances.

One of the simple things you can do is turn on all the light switches in the house to ensure they work. If there are bulbs out, you can get this fixed up before you go unconditional in the contract. If there are power points, bring just a simple little socket. We’ve had some clients go as far as bringing a clock radio and testing power points to make sure they work because if they don’t, it’s going to be your responsibility to get an electrician in to fix it up.

Good Neighbours are Important

Good neighbours are important when buying a home.

As the saying goes, you can choose your friends but can’t choose your neighbours. When you’re buying a home, you’re hoping to be there for a couple of years, and a bad neighbour can turn a beautiful new home into a horrible experience.

So, the best way to guard against this is to look around the street on your first inspection. Have a walk around, and get a feel for your neighbours. For example, if there’s junk in the neighbour’s yard, it will likely be there when you move in. Also, try to drive by Friday or Saturday night just to get a feel for the potential neighbours and what kind of people they are. Are they big party animals? Are they quiet? It’s nice to know what you’ll be in for once you move in.

Check out the local area

Check out the convenience of food, public transport and groceries. This is something you may not think much about until you have kids and it gets more important later in life. Are there nice walking paths nearby? Can you walk or ride a bike to local shops, or do you have to pop in your car? A great tool to check this out is Walk Score. You can literally put in the address, and it’ll give you a quick score to tell you what amenities are available and how far they are from your house.

Skipping the bad photos

Nice looking photos often lead to bidding wars.

Usually, everyone is looking for good photos, and if the listing has good photos, it can lead to bidding wars. However, if there are really crummy photos, it could mean you’re the only person turning up because people usually give a wide berth to photos that are not good. So don’t skip the bad photos, as you may be able to get a good deal.

The difficult thing with real estate is it can take a couple of goes to find the right one. So you might go through a bunch of crappy photos which could turn out to be as crappy as the photos look in real life. You’re just going to have to go and check them out.

Well-maintained but poorly presented homes offer better value, so keep that in mind when you’re on the hunt.

Don’t take too long to make an offer

We’ve seen this time and time again: The market can move. During COVID-19, the market was really slow, and properties were sitting on the market for 2-3 months. You could take your time to casually check out a property online, do inspections, and make an offer—it was a real buyers’ market. You had the control.

In the current market, in many places around Australia, the days on market are under 30 days. 30 days means from when it’s listed to when it’s sold and potentially settled, so stuff is selling really quickly. Offers are being made before the first open home, and you need to be aware of this.

Not knowing who the real estate agent is really working for

There are some really good estate agents who are genuinely out there to help sellers and buyers and bring people together. But there are also a lot who aren’t like this.

You must remember that real estate agents aren’t licensed financial advisers; they can’t give you tax advice, they’re not registered tax agents, and they can’t talk to you about negative gearing and the benefits around that. Real estate agents aren’t the local Council or town planners, so take any advice about rezoning with a grain of salt.

At the end of the day, a real estate agent’s job is to sell the property for the most money in the least amount of time possible. Don’t take it personally; you just need to take it as it is and understand what you’re playing with.

Not factoring in extra costs.

It’s worth considering some common extra costs. A common one we see these days is body corporate or strata fees. Did you know this can drastically impact how much the bank will lend you? For example, if your body corporate is $10,000 per year, that can be a few hundred a week in what you have to pay towards a body corporate, and the bank expects that to come out of your pocket—in addition to the mortgage repayments.

Home Buying FAQs – Step by Step Guide

How much of my income should go toward a mortgage?

Financial experts suggest keeping mortgage repayments below 30–35% of your gross income. This protects you from financial stress caused by interest rate rises or unexpected costs.

What are the ongoing costs of owning a home?

Beyond mortgage repayments, budget for council rates, insurance, utilities, body corporate fees, and regular maintenance. These ongoing expenses can add up quickly, so include them when planning your first steps to buying a house.

Can I avoid paying Lenders Mortgage Insurance (LMI)?

Yes. You can avoid LMI by saving a larger deposit, using a guarantor, or checking eligibility for government assistance like the Home Guarantee Scheme.

What is a cooling-off period when buying property in Australia?

The cooling-off period is a set timeframe after signing the contract of sale where you may legally withdraw. The length and conditions vary by state.

When should I take out insurance on a home I’m buying?

Take out building insurance from the moment you sign the contract of sale. Even before settlement, the property becomes your responsibility.

Why are building and pest inspections important?

Inspections can uncover hidden issues such as termite damage or structural problems. They allow you to negotiate repairs, request a price reduction, or walk away if the property is unsafe.

What are strata or body corporate fees and how do they affect me?

These are payments made by unit or townhouse owners to maintain shared facilities like lifts, gardens, or pools. High fees can lower your borrowing capacity, as lenders see them as ongoing costs.

What should I consider when choosing a property location?

Check for public transport, schools, Walk Score, shops, and lifestyle amenities. A good location improves daily convenience and supports long-term property value.

What are the first steps to buying a house?

The first step in the step by step home buying process is saving a deposit, then checking your borrowing power. From there, get home loan pre-approval so you’re ready to make an offer.

How long does the process of purchasing a house take?

In Australia, the process usually takes 4–8 weeks from when an offer is accepted to settlement. Timing depends on loan approval, inspections, and contract conditions.

What government schemes are available for first-home buyers?

Programs like the First Home Guarantee, Family Home Guarantee, and state-based First Home Owner Grants help buyers purchase with smaller deposits and reduced costs.

What financial steps should I take before buying my first home?

Save at least 5–20% deposit, get pre-approval, understand stamp duty and legal fees, and budget for moving expenses. Following these steps makes buying a house smoother and less stressful.

Next Steps For Home Buyers Looking For Information

Our team here at Hunter Galloway is here to help you buy a home.

Unlike other mortgage brokers who are just one-person operators, we have an entire team of experts to help make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Our team of home loan experts is here to help you buy a home in Australia.