This is a complete guide to home renovation loans in 2025, written by expert mortgage brokers in Brisbane. We’ll cover some of the most important trends in renovating your home in 2025. You’ll learn the following:

- How renovation loans work

- How to renovate on a budget

- Different ways of financing your home renovation

- Dozens of home improvement loan best practices

- …and one advanced technique to get your renovation loan quicker

So, whether you want to add value to your home or just want to make some improvements, you’ll love this guide.

Let’s dive right in.

Renovation Loan Basics

Renovating can be a great way to improve your home’s look, feel and functionality. It can improve energy efficiency and the livability of your home.

But it’s no secret that renovating can be a shortcut to increasing the value of your property.

Here’s why…

Renovating can cost less than buying a new property. And the best part is that you get your own say on it.

The good news is that qualifying for a home renovation loan can be easy, and we will show you how.

How Much Can I Borrow?

How much you can borrow for renovations usually depends on the type of renovation you want to do. There are about five different categories that your renovation loan can fall into, and knowing these categories will help you get your finances sorted.

Scope of renovations | Builder Involved | Maximum Borrowing | Example |

Non structural, or minor renovations | Not necessary | 90% LVR based on current property value | Painting inside of house, or adding air conditioning |

Structural, or major renovations | Yes | 95% LVR based on ‘as if complete’ value | Adding a new room, lifting a house, adding a new kitchen. |

House rebuild | Yes | 95% LVR based on ‘as if complete’ value | Demolishing a house and completely rebuilding it. |

Adding a granny flat | Yes | 95% LVR based on ‘as if complete’ value | Building an external house, or granny flat extension. |

All of the above | Yes | 105% LVR based on current property value plus the help of a guarantors property. | Only available with the help of a guarantor. |

As you can see, the scope of your renovations will largely determine how much the bank will lend you.

Will the loan be paid in stages like a construction loan?

How your renovation loan is paid out depends on the size of the job and the scope of the work.

You can control payments if the loan is for non-structural minor renovations and is less than $100,000. This means you will pay the builder or contractor for the job on completion.

For larger jobs like a complete rebuild or lifting a house, the bank will be looking for progress payments to be made — in the same way they would pay out a construction loan.

When should I apply for a renovation loan?

If there’s one thing we’ve learnt in the industry, it’s that the banks make all the rules.

To get the upper hand, we recommend you apply in advance to take some stress off yourself.

Now, there are two ways that applying for a renovation loan can go.

Number 1 – Jane’s situation.

Jane has a lot of equity in her property. She applies to release equity, using the current value of her home (before renovations). This should take about a week or two to get approved.

Number 2 – Charles’ situation (the more realistic situation)

Charles has very little equity, so he has to allow 2 to 3 weeks for the renovation loan to be approved. He will need a signed building contract and will rely on the ‘on completion’ value of his property.

So, it is important to apply for a renovation loan way before you begin the renovation.

What Are The Most Popular Types Of Renovations?

There are many types of renovations, but the type of renovation you choose will be determined by the amount of money you are able and willing to spend.

That said, here are the most popular types of renovations.

Non-structural or minor renovations

As mentioned above, non-structural and minor renovations will rely on the existing equity in your home. We will arrange a bank valuation to determine the current value of your home, and you can borrow up to 90% of this amount.

In other words, if your home is worth $500,000, you can borrow up to $450,000. If you have paid down $100,000 and still owe $400,000, you’ll have $50,000 towards your renovations.

Cosmetic renovations

Think of this as a facelift, but for your house—It’ll look new and fresh, but nothing has really changed underneath.

Cosmetic renovations include painting the house, covering the floor, cleaning up and restyling the garden and so on.

If a large surface area like the floor has dirty old carpet, changing this can give you the best bang for your buck. The best part is it’ll also improve the entire feel of the home without too many costs involved.

Kitchens and bathrooms

Kitchens and bathrooms are the areas that have the most significant impact on a person’s impression of a home.

The kitchen is considered the heart of a home, so having a fresh and updated kitchen can affect your home’s overall look and feel.

In fact, the kitchen is one of the first things you should look at when buying a home because it is one of the more expensive parts of the house to renovate.

Getting a swimming pool

In Australia’s balmy Sunshine State, all the locals are looking for this. Getting a pool installed in the backyard can add value to a home, at least where weather permits maximum use of it anyway.

There’s no doubt in Queensland, a swimming pool is a great addition to a home. But if you’re in Tasmania, maybe not so much.

Structural or major renovations

Structural renovations mean your renovation game will need to step up a notch.

Here, we’re talking about knocking down walls and switching up rooms, maybe even changing how the actual house flows. This type of renovation can be a costly way to do things and is not the most desirable form of renovation due to the fuss around it.

In the case of a structural renovation, the bank will arrange an ‘on completion’ valuation, taking into account the major structural renovations you are doing.

So if your home was worth $500,000, but you are getting $100,000 worth of structural renovations to add an extra bedroom and update the kitchen – it’s possible the bank will value the ‘as if complete’ home at $600,000 – and let you borrow up to 90% based on this amount.

House Extension

More space!

I recently turned my garage downstairs into two extra bedrooms, and we’ve appreciated having the extra space.

A house extension is a major renovation. But one thing you need to do before you go ahead and throw in some new walls is to get council approval.

Types of Renovation Loans

With shows like The Block, there has been a massive increase in renovations.

But the reality is that renovating can be a consuming and tiring process.

Getting your finances sorted will help make the process a little easier and ensure that your funds will be approved.

Your renovation loan type can make or break your entire application.

So, it’s crucial to nail this step. To help you with that, here are a handful of strategies for renovation loans and how they work.

How do renovation loans work?

As we explained earlier, setting up your finance as early as possible will help you increase your chances of everything going smoothly. It will also give you a more precise budget so you know how much you can spend.

Understanding how exactly a renovation loan works is an essential part of the process so that you can anticipate and prepare for each step of the way.

Renovation loans work in many different ways, and the type of renovation loan you get comes down to your personal circumstances.

So, in this section, we will go through the different types of renovation loans that you can apply for.

These are the 5 types of renovation loans you need to know about.

Type 1: Home equity loan or increase your existing home loan.

This one is our go-to for those with equity in their current home. For already established homeowners, you can borrow up to 90% of the value of your house.

But what’s the risk? If your renovations cost more than the equity in your home, it can get a little messy as you run out of money.

The solution? Do a cost analysis and stay strictly within your budget to streamline the process.

The benefit of a home equity loan is that It allows you to spread the costs over a long period and potentially borrow up to 90% of the value of your home.

In some cases, you’ll have access to more favourable rates—better than credit card and personal rates.

Type 2: Construction loan

A construction loan is almost similar to a home equity loan, but the major difference is that the final value of your home after renovation is considered. You also won’t have access to the total loan upfront. Instead, it will be dripped out over a time frame. So, if you’re looking for a bulk sum of money at your disposal, this isn’t that kind of loan.

Type 3: Line of credit

A line of credit is terrible! Don’t use it!

It’s basically a credit card-type facility with a higher interest rate and only has interest-only repayments.

With a line of credit, interest is only paid on the money you use, and as you pay down your balance, you can continually re-borrow the funds without going through the hassle of reapplying.

You can get the same benefit from doing a home equity loan as per type 1 but at a lower rate.

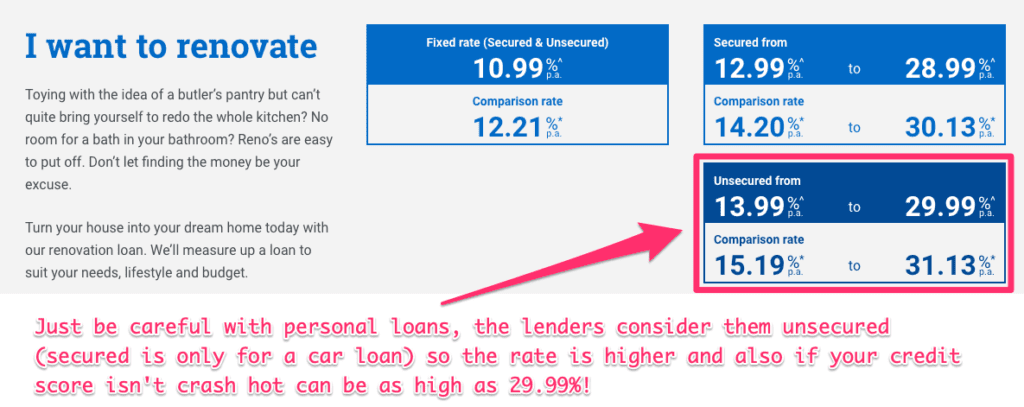

Type 4: Personal loan

If just a few cosmetic renovations are what you have in mind, then a personal loan could be all you need.

You’re looking at around $30,000 max, but the catch is interest rates on personal loans are higher than standard home equity loans. So proceed with caution and do your research.

Like using credit cards, we suggest extreme caution before jumping into a home reno with a personal loan.

While many guides might say that a personal loan can help you get the renovations started quicker, they ‘forget’ to mention that the advertised interest rate is more of a starting rate – rather than the final rate. You may end up paying a higher rate.

If you’re considering a personal loan, speak with our expert mortgage brokers or give us a call at 1300 088 065 to see what your options are.

Type 5: Credit cards

Caution ahead!

If you’re considering making just a few minimal renovations, this one could benefit you. However, interest rates are often much higher on credit cards than mortgage rates.

We are talking up to 21.45% interest rates here.

So, while lots of different guides suggest you use a credit card, you should give it a second thought before jumping in.

You only benefit from credit cards if the project is small because then it could work out better in the long term due to all the establishment fees you’re skipping out on. You can also refinance the credit cards (like I did) if you have increased your property’s value.

Banks That Do Renovation Home Loans

While you would expect all banks to be able to help with renovations, it isn’t always the case.

Some banks like ING and online lenders like UBank cannot do structural renovations or construction loans.

Here are a few banks that will consider loans to help with improving your home:

- Commonwealth Bank: How to Finance Your Renovation

- NAB: Renovating Your Home

- ANZ: Home Rennos

- Suncorp: Renovating from Equity

To understand what type of loan will best suit you, speak with our team of Expert Mortgage Brokers on 1300 088 065 or get in touch here.

Time To Crunch The Numbers

Now it’s time to show you how to crunch the numbers.

Specifically, we will share 6 strategies that can make your renovation dreams a reality.

1. Decide on the scope of your renovation.

2. Budget calculators will become your best friend.

Jump online and use one of the many budget calculators to help you get intimate with the costs of your renovation.

Usually, if you are new to renovations, what you may want to do may be way out compared to your budget.

So be realistic about what you can afford because blowing your budget isn’t on the agenda today!

3. Break it down now (we're talking costs, not dance moves)

It is essential to break down your budget before you begin renovating your home because it ensures that you stay within your limits and don’t end up spending more than you can afford.

Research the cost of everything.

Every. Little. Thing.

Research labour costs, products and different materials, and even the cost of every washer and bolt. If you do this, there will be fewer surprises once you begin the work.

4. Get a professional eye on it.

This is key.

They are professionals for a reason, so don’t go ahead without their tick of approval. Let them review your renovation plans before you finalise your budget to ensure you haven’t missed anything.

The best thing I did was sit down and have a chat with my friend, who is an architect. She helped manage my expectations and gave me a few hacks to help maximise the space I had available.

A professional will be able to assess any potential risks or issues that may arise during the renovation process. They can also suggest solutions to these potential problems so that you can factor them into your budget.

Another great reason to talk to a professional is that they can also offer some cost-saving tips while maximising the efficiency and quality of the renovation. So you might end up using less than you had budgeted. Sweet!

5. Three is the magic number (when it comes to quotes)

Don’t walk away without getting 3 separate quotes from every trade. That includes builders and any tradespeople you’ll engage with.

Why?

Getting 3 (or more) quotes allows you to compare prices and services. You will be surprised that the quotes will vary massively, and you’ll thank yourself in the long run.

Multiple quotes can help you assess the experience and qualifications of the tradespeople you want to hire. You can also use multiple quotes as a negotiation tool.

In short, getting 3 quotes before hiring anyone for a renovation project can help ensure you get the best possible deal.

Another option is to chat with family and friends to see if they’ve got any connections or have had good experiences with tradespeople in the past and start there.

6. Always leave a buffer.

Leave a buffer of 10 to 20% on top of your final budget. This buffer means you’ve got a contingency plan in place for unanticipated costs such as overruns from contractors, additional materials or sudden changes in the scope of your renovation, e.g. someone can accidentally drill through a pipe, and now a cosmetic renovation suddenly turns into a major renovation.

Overspending is so easy to do, so keep ‘beer budget’ in mind so you don’t miscalculate.

Remember, it is better to overestimate expenses and have some change left over than to underestimate expenses and end up going over budget.

If you need a place to start, check out Your Home, which is a government site that goes through the process of renovating a home.

Renovating On A Budget

With rising interest rates and inflation, you might be wondering if it is possible to renovate on a budget. The answer is…

YES!

It is possible to renovate on a budget. However, the real question to ask is:

How can you renovate on a budget while still being able to make all the changes that you want?

That’s what this section is all about.

How you can renovate on a budget

First, pay professionals for essential jobs.

This includes all electrical, plumbing and structural work. Trying to do these jobs by yourself to save money may actually end up costing you more in the long run.

Get at least three quotes, and remember, just because something is cheaper doesn’t mean it’s the best option for you. You need to find someone with a good balance between price and quality.

Speak to previous clients to get testimonials and ensure your money will be well spent.

Throw a working bee party.

If you’ve got some odd jobs, why not throw a working bee partying? Your network around you can help, and in return, you provide the drinks and a BBQ. (But make sure you are working and not just partying.) There are heaps of jobs you can smash out together, like:

- Painting

- Fencing

- Polishing floorboards

- Tiling

- Landscaping

Make the most of YouTube and DIY lessons.

YouTube is good for more than just funny cat videos. It is full of a wealth of information. Some even call it a university. You can learn anything on YouTube—from how to put up curtains to changing the entire window. So, get lost in the world of DIY online…

If that’s not your thing, you can check your local hardware store. Often, they have lessons and workshops for the community to engage in to learn how to use tools and get design ideas.

Shop around for materials.

Go to auctions and discount stores to try and save on supplies and materials. Also, ask for trade prices or see if there are any discontinued sales.

Some renovations will lead to massive savings in the future, like energy-efficient technology. So consider the following…

- LED lights

- Good quality insulation (to keep cool from Queensland’s sun)

- Rainwater tanks (you’ll be thankful if a drought comes)

- Solar panels (say goodbye to Origin Energy bills)

Get creative…

My wife is a stickler for some nice mood lighting, and you’d be surprised how much a room changes when the right lighting is installed.

Here are some ways you can get creative with renovating on a budget:

- Think of making minor changes like swapping out baths and basins or giving the place a new lick of paint.

- Head over to a showroom or paint shop to get some expert ideas on how to clean up your home’s appearance on a low, low budget.

- You can get some wallpaper and create an accent wall or paint an accent wall or DIY backsplash.

- You could add a pop of colour by painting furniture or accessories.

- Switch out small fixtures such as cabinet knobs, drawer pulls and light fixtures.

- The simplest thing you can do is add curtains, throw pillows and area rugs.

My Case Study: Advanced Tip And Renovation Loan Best Practices

When I did renovations on my place, I wanted to try to save some money and not get a builder involved.

So, I tried being a bit dodgy by using a combination of a personal loan and credit card to do the renovations.

I got a personal loan for $30,000 and used some of my savings and credit card to do the renovations on this place, which I had bought for $425,000.

Once I had finished the renovations, I got the bank to do a new valuation.

And lucky for me, the property’s value had increased to $500,000!

(Winning)

So I was able to increase my loan and pay out the personal loan.

But a word of warning:

If you cannot do this, you can be stuck with a personal loan and pay much higher interest rates than your home loan. Worse still, you could be stuck with these expenses on your credit card, paying 21% interest!

Next Steps And Getting Your Renovation Loan Approved.

Are you looking to renovate your home? At Hunter Galloway, we understand that renovating can be daunting, so we take some of the hassle out of it by finding you the loan that best suits your needs.

From researching your options to finding the most competitive rates, we’ll take care of the financial side of the equation. We’ll help you select the right loan for the renovation and keep you informed of the process every step of the way.

Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please call us on 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again