According to the Australian Bureau of Statistics, Australia has one of the highest levels of home ownership in the world.

This means that home loans are in hot demand!

As you know, setting up a home loan is about finding the best rate for you. If you don’t do your research properly and use a comparison rate to your advantage, you could be losing money each year on your loan.

So, here are some of the most common comparison rate mistakes and how to avoid them:

The main mistake we see buyers make before they speak to us directly is relying completely on the comparison rate to do all the work.

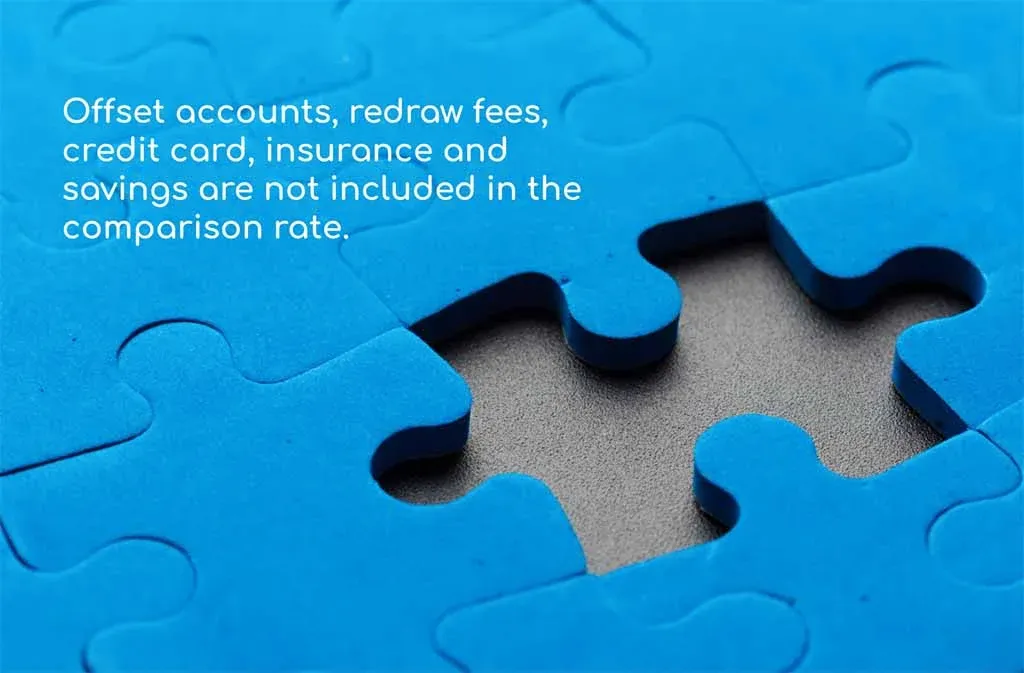

Remember that comparison rates are product-specific and do not include a particular loan’s features and other inclusions. This means offset accounts, redraw fees, credit cards, and insurance savings are not included in this number or comparison.

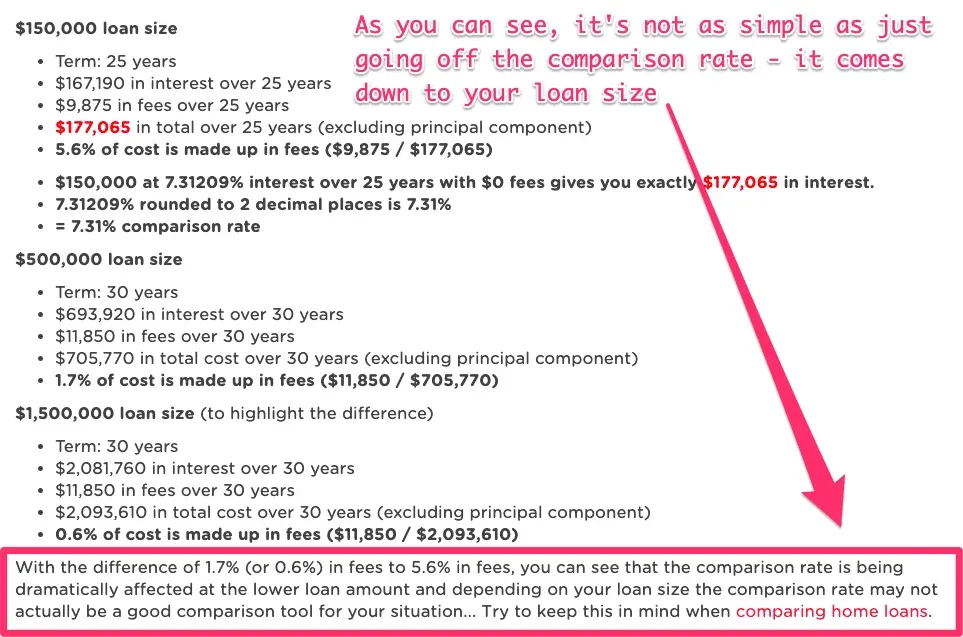

Comparison rates don’t look at different types of loans, which means that fixed-rate and variable-rate loans are dumped into the same category, together with the loan size.

So, the comparison rate you’re seeing is only for a $150,000 loan, not your specific loan size.

This is where problems can occur.

For example, fixed-rate loans can be misleading because it is assumed that once the fixed period is over, the rate continues as a standard variable rate.

But here’s the catch.

If you’re like most borrowers, once the fixed rate period is over, you will refinance. Refinancing saves you money because you can get the best available rate at the time.

…Usually, even lower than the regular one because the lender will offer you a deal.

Comparison rates can’t predict this.