The most important factor in deciding when to buy a home is your personal situation. Every single person has a unique set of circumstances that drive their decision to buy a home.

It would be impossible to cover everything in this book, so I want to focus on the key points here and give you a few benchmarks to look at. You can measure yourself against these criteria to see whether you’re really ready to buy a home, or if you should sort a few things out before taking that first leap into home ownership.

Your employment

As we’ve mentioned earlier, your employment (and sources of income) is one of the most important factors that banks will be looking at to decide whether to offer you a loan (and how much they will offer). While there are workarounds for almost every situation, here’s what we recommend:

✅ You should have been in your job for six months: Banks like borrowers who have stable employment history, ideally at least six to twelve months in your current job. If you have just started a new job, that is ok if you have been in the same industry for at least 2 years.

✅You shouldn’t be planning on changing jobs until your loan has settled: If you are considering changing jobs at the same time as buying a new home you need to seriously reconsider one or the other. The bank would have assessed your income based on your previous job, and if it changes before your move into your new home they will want to reassess your entire loan application (and won’t necessarily say yes again!)

✅If you have had a decrease in income: This is fairly common for casual workers whose hours fluctuate week by week. You might have been working more hours earlier in the year, or even received a bonus and now you are being paid less. That’s ok, different banks assess this income differently – some banks will look at your weekly pay and multiple it by 46, other banks will just take your weekly pay and multiple it by 52 weeks in the year. A good mortgage broker will help you navigate this to find the best option for you.

✅ If you are self employed, or a contractor make sure your records are up to date: The banks will ask you for a little bit more information compared to a regular PAYG employee, so you may need to have your tax returns updated and ready to go for your home loan application. Most banks will require the most recent years tax returns before the ATO needs them. For example, while the ATO requires FY19 tax returns lodged by companies and trusts by 15 May 2019, the banks will start asking for this information from 1 January 2019! Better get that accountant crunching your numbers.

Your spending

When you apply for a home loan nearly all banks will want to see your last 3 months (some banks even want to see 4 months!!?) day to day transaction account statements.

As crazy as it might sound if you spend too much at Zara, Dan Murphy’s or even Sportsbet on the weekend it could affect your home loan application.

This is because the bank will look at your day to day spending habits from the past month, look at these costs and annualise them to determine what it costs you to live each year… And if you had a particularly expensive month, it could reduce how much the bank is willing to lend you!

Here’s what we recommend with living expenses:

✅ Know the bank will see every single transaction you’ve made over the last 3-4 months: I’ve seen banks come back and question a couple who spend money at Baby Bunting asking if they had an ‘undisclosed child’ (they had bought a gift for a friends baby shower)… And I’ve seen other loans declined for spending too much gambling (she had applied straight after Melbourne Cup). As crazy as it sounds, just be aware of this in the months leading up to applying for your home loan – tightening the belt for a few short months could be the difference between getting your home or not.

✅Let your Mortgage Broker know about any one off expenses: If you’ve recently gone on holidays, or had any large one-off expenses like aeroplane tickets let your broker know so they can make the bank aware it is a one off expense and won’t be ongoing… And ultimately won’t affect your ability to repay the loan!

✅Prove you can afford the loan, before you get the loan: The banks are increasingly looking for you to prove you have an existing history of keeping up your home loan repayments, even before you get your loan. In other words, they want to see that what you’ve been paying in rental + savings is the same as what your mortgage repayments will be. So if you have been paying $2,000 per month in rental, and saving $500 per month – and your new home loan repayments are $2,000 per month you will be fine. You have proven propensity to repay your loan!

Your credit

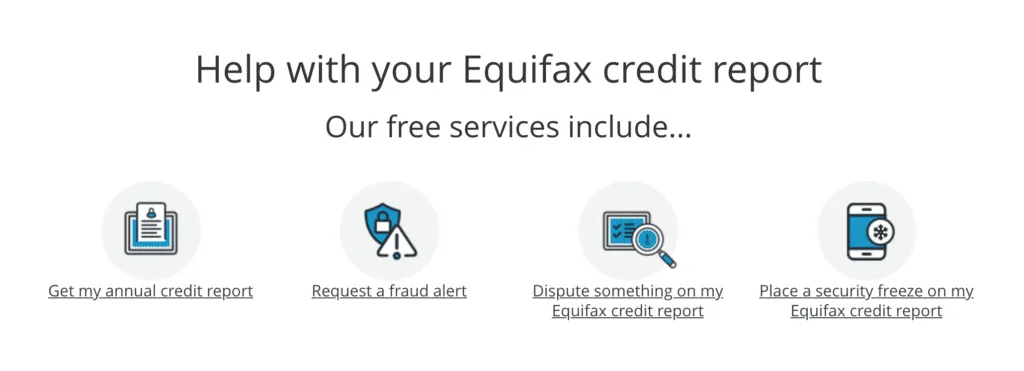

Your credit score is another critical factor in your ability to secure a loan at the best rate. If you have bad credit, it will be much harder to get a loan. If you do get approved for a loan, you’ll end up paying a much higher interest rate because the banks see you as a higher risk. You can check your credit score for free at Equifax you get one free report every 12 months! Here’s what we recommend for credit scores:

✅ Your Credit Score: A good credit score is between 622 to 725, a very good score is between 726 to 832 and an excellent score falls between 833 to 1200. If your credit score is below this check to see if you have missed any payments, or unpaid defaults on your credit file.

✅ Defaults: You will see default on your credit file if your repayments are more than 60 days late and the amount due was over $150. Check these details are correct and you did receive the notices listed. If you have settled the overdue amount make sure it is showing as ‘paid.

✅ Double check the Loans and Debts: Make sure these are your debts, the amount is correct and that there aren’t any duplicates.

✅ Your personal information: Check your information on the report is correct, like your name, gender, date of birth, current address, drivers licence number and current employer.

A late phone bill won’t impact you unless you go into default and getting a pay rise or changing jobs won’t negatively impact your credit score…

But according to Experian, “A score may go up or down because of new information. For instance, if you already have a very low credit score, a new default may not lower your score any further. Similarly, a default will stay on your credit report for five years even once you pay it off, and should there be other defaults on your file, your score may not necessarily increase. Likewise, if you already have a very high credit score, continuing to make your payments on time may not make your score go any higher. It’s important to note that there is no quick way to fix a credit score – repairing bad credit takes time.”

So make sure you keep paying those bills on time!

Your deposit

If you don’t have a decent deposit, you will find it harder to get a loan, and you will need to pay LMI in most cases. This adds a significant cost to your loan and is best avoided if you can. Here’s our recommendations for deposits:

✅ Have at least 8% to 10% in savings: While there are a handful of lenders who will do up to 95% LVR loans, the LMI costs and stricter credit criteria can make it more difficult to get your loan approved. Having 8% to 10% in savings will give you the maximum amount of options to buy your home.

✅If you are buying with the help of a guarantor: Make sure you take into consideration all costs. As we’ll cover shortly, buying a home costs more than just the purchase price and some stamp duty. You need funds for solicitor fees, moving costs, transfer duty and a bunch of other costs! Factor in another 0.5-1.00% to cover any incidental costs you might have when buying your home.

✅If you are just short on your deposit: Try asking your parents, or a relative to gift the deposit amount you are short. I’ve seen cases where $2,000 in extra deposit have saved $4,000 in LMI costs!