1. Latest Market Update – November 2025

November 2025 has been a turning-point month. Prices are at record highs again, interest rates have finally stopped climbing, and government support for first-home buyers has expanded. The result is a market that feels busy, competitive — but also more predictable than it did a year ago.

Key Highlights

Prices Are Setting New Records

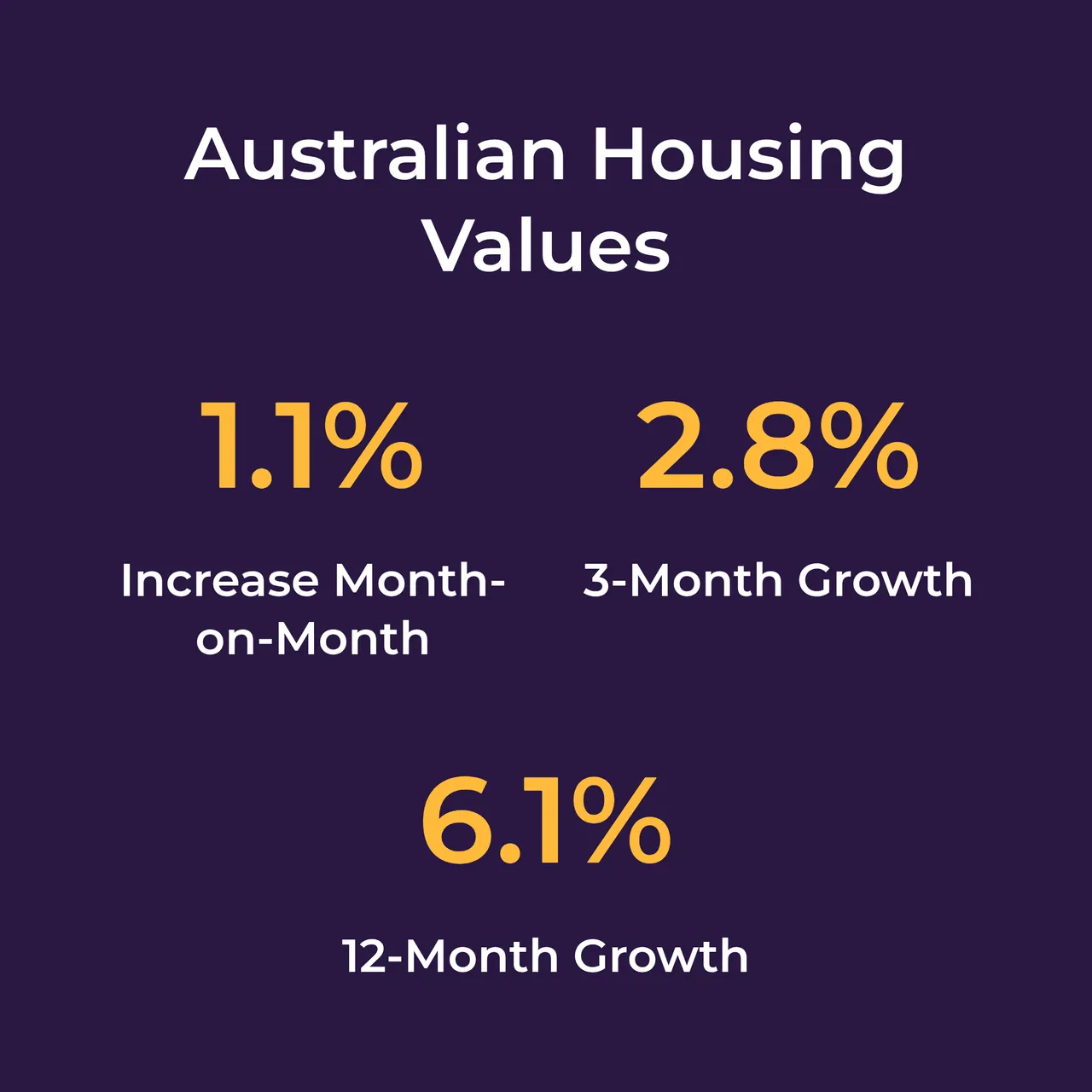

Australia’s housing market continues to climb. National home values rose 1.1% in October, with a strong 2.8% jump over the past three months — the fastest pace since 2023. Over the year, values are up 6.1%.

Instead of a boom, this feels more like a steady, grinding rise: not chaotic, but enough that waiting another six to twelve months could mean paying more.

Interest Rates Have Finally Settled

The RBA cut rates three times in 2025, bringing the cash rate to 3.60% by August.

New mortgage rates now sit around 5.7% — lower than last year’s highs but still far from the ultra-cheap ~3% loans of 2021.

Low Supply + Lots of Buyers

Listings are still well below normal levels. More people want to buy than there are homes available, and that imbalance is keeping upward pressure on prices.

For first-home buyers, this usually means you’ll see competition at open homes, especially for anything under $1m.

Renters Are Feeling the Squeeze

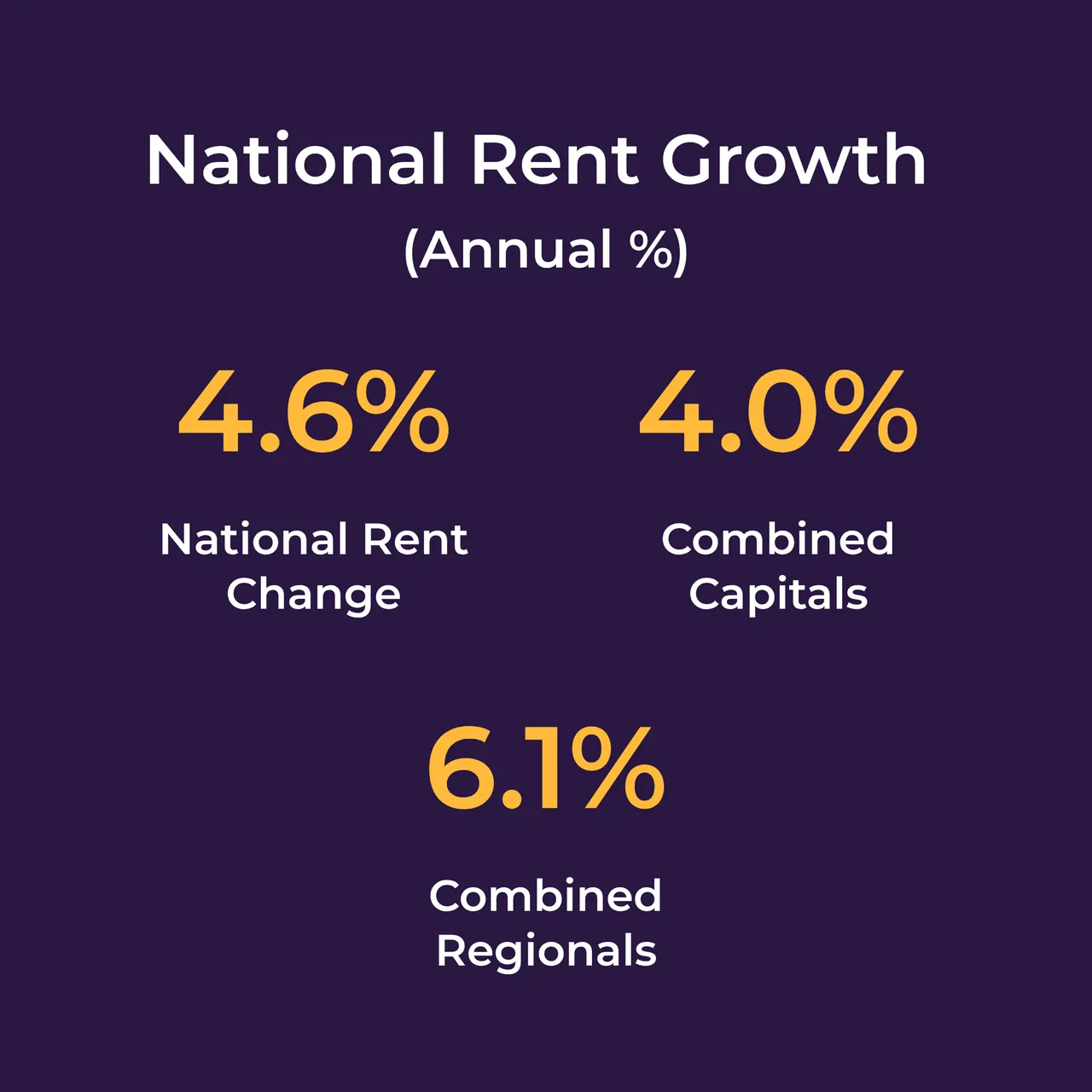

Vacancy rates remain extremely low — typically 1–2% nationwide.

Weekly rents average around $663, and in many cities it’s even higher.

This is pushing some long-term renters toward buying, even if it means stretching their budget, simply because the rent increases feel endless.

Big Changes to First-Home Buyer Schemes

The federal Home Guarantee Scheme has undergone its biggest expansion to date:

Unlimited places — no more rushing to secure a spot

Higher price caps, including Sydney increasing from $900k to $1.5m

Income caps removed, making more buyers eligible

For many young buyers, this changes the whole equation — a 5% deposit is now enough to enter markets that were previously out of reach.

What This Means for Buyers

When you put all of this together, 2025’s market is unusual:

it’s still expensive, but it’s also more stable; mortgage rates aren’t rising, but prices are; support for first-home buyers is increasing, but so is competition.

If you’re planning to buy, the next few months are likely to feel more predictable than the past few years — but still fast-moving if you’re targeting entry-level homes.

Australia’s housing market continued to heat up in 2025. Prices have climbed across almost every city, driven by low supply, steady demand and stabilising interest rates. This section breaks down what’s happening nationally — and what it means when you’re trying to get into the market for the first time.

2. National Market Overview: Prices, Trends & Affordability

Prices Are Rising Again

Home values have pushed higher throughout 2025. Across the country, prices rose 2.8% over the past three months and 6.1% over the past year, with most capitals now sitting at or near record levels.

Some cities are moving far faster than others.

Growth has been strongest in:

Darwin (15.4%)

Brisbane (10.8%)

Perth (9.4%)

Adelaide (6.7%)

Sydney (4.0%) and Melbourne (3.3%) are growing more moderately, but still trending upward.

For buyers, this means one thing: waiting is getting more expensive. Even though growth rates differ by city, almost every capital has now fully reversed the brief downturn of 2022–2023.

Why Prices Are Climbing

The big story in 2025 is a familiar one: too many buyers, not enough homes.

Four major forces are driving this:

Low Supply

There simply aren’t enough properties for sale or rent. Construction levels haven’t kept up with population growth, and high building costs have slowed down new projects. Fewer listings mean more competition for each available home.

High Demand

Australia’s population continues to grow, and many renters are actively trying to buy because rental conditions have become so tough. Even with higher interest rates than a few years ago, demand remains strong.

Government Incentives

Schemes like the First Home Guarantee — now with unlimited places and dramatically higher price caps — make it possible for more buyers to enter the market with smaller deposits. This keeps activity healthy at entry-level price points.

Stabilising Interest Rates

After the RBA’s cuts in 2025, borrowing feels more predictable. Rates are still much higher than 2021, but they’re no longer rising rapidly. This has restored confidence and allowed some buyers to re-enter the market.

Put simply: when supply stays low and confidence returns, prices rise. That’s exactly what we’re seeing through 2025.

3. Capital City Market Snapshots

Australia’s capital cities all behave differently. Some markets move fast, some are cooling, and some are quietly becoming first-home-buyer hotspots. Here’s what the market feels like in each city right now — and what that means if you’re planning to buy.

Sydney

Price Overview

Sydney’s market is still the most expensive in the country — and still rising. Values lifted 0.7% in October, 2.3% over the quarter, and 4.0% over the year, pushing prices to another record high.

A −2.9% median vendor discount shows how competitive things are: sellers barely need to negotiate.

Rental Market

Sydney rents are the highest in Australia, sitting around $790 per week. With vacancy rates hovering around 1–2%, securing a rental can feel impossible.

This pressure is one reason some long-term renters decide to buy sooner than planned.

Supply & Demand

Sydney’s biggest problem is simple: not enough homes. Geography, planning limits and constant population growth keep supply tight.

Entry-level houses under ~$1m attract fierce competition; apartments offer more choice but are still expensive by national standards.

First-Home Buyer Activity

First-home buyers make up a smaller share of Sydney’s market, mainly because deposits are so large.

Most rely on:

the expanded First Home Guarantee (cap now $1.5m)

NSW stamp duty exemptions up to $800k

family support (“Bank of Mum and Dad”)

Many young buyers choose apartments, townhouses, or move outward to more affordable Western Sydney suburbs.

Melbourne

Price Overview

Melbourne sits in a unique position: still a major city, still expensive — but currently more affordable than Brisbane, Perth or Adelaide.

Prices rose 0.9% in October, 1.6% over the quarter, and 3.3% annually, though values remain 1.4% below their 2022 peak.

Vendor discounts average −3.3%, suggesting a healthier balance between buyers and sellers.

Rental Market

Median rent is around $610 per week with vacancy at 1.4%. Renting is competitive but not the pressure cooker Sydney faces.

Apartment rents that plunged during COVID have now returned to normal levels.

Supply & Demand

Melbourne has consistently built more new homes than most capitals. This steady supply — especially in the outer suburbs and apartment corridors — has kept price growth moderate.

It’s one of Australia’s most affordable major cities relative to income, which is why so many first-home buyers target it.

First-Home Buyer Activity

Melbourne is arguably the first-home-buyer capital of Australia.

Top searched suburbs include:

Dandenong

Coburg

Wyndham

Craigieburn

Victoria’s incentives help: a $950k FHG cap, $10k new-home grant, and stamp duty reductions for lower-priced homes.

Brisbane

Price Overview

Brisbane continues its strong run. Values jumped 1.8% in October, 4.9% over the quarter, and 10.8% over the year, hitting record highs.

A −2.6% vendor discount shows buyers are competing hard — one of the tightest markets in Australia.

Median dwelling value is roughly $950k, with middle-ring houses in the $800k–$900k range and units around $500k–$600k.

Rental Market

Rents sit around $680 per week with vacancy at 1.7%. Yields are strong but still not enough to attract enough investors to fix the shortage.

Supply & Demand

Listings are very low — especially houses.

Demand is driven by:

population growth

interstate migration

lifestyle appeal

future 2032 Olympics infrastructure

Suburbs under $1m (Ipswich, Logan, Moreton Bay) are extremely competitive.

First-Home Buyer Activity

First-timers are active but face competition from investors and interstate migrants.

Queensland offers generous help:

$30k FHOG (new builds)

stamp duty concessions up to $500k

Many buyers choose house-and-land packages 20–40km out, or relocate to the Gold Coast, Sunshine Coast, or regional towns for better value.

Perth

Price Overview

Perth is no longer the “cheap city.” After several years of sharp growth, dwelling values now average about $842k, similar to Adelaide.

Prices rose 1.9% in October, 5.4% over the quarter, and 9.4% annually, all at record highs.

Vendor discounting is just −2.6%, meaning buyers move fast.

Rental Market

Rents are among the highest nationally at $720 per week.

Vacancy rates are around 1.3%, making Perth one of the tightest rental markets in Australia.

Supply & Demand

Listings are 30–40% below normal, while demand is fuelled by:

a strong WA economy

mining investment

high rental yields

interstate investors chasing returns

Labour and material shortages also slow new construction, worsening the squeeze.

First-Home Buyer Activity

WA is very supportive of new buyers:

$10k FHOG for new builds

Keystart loans with low deposits

stamp duty waived under $430k (discounted up to $530k)

Many first-home buyers build in outer suburbs, but must act quickly — well-priced homes don’t last long.

Adelaide

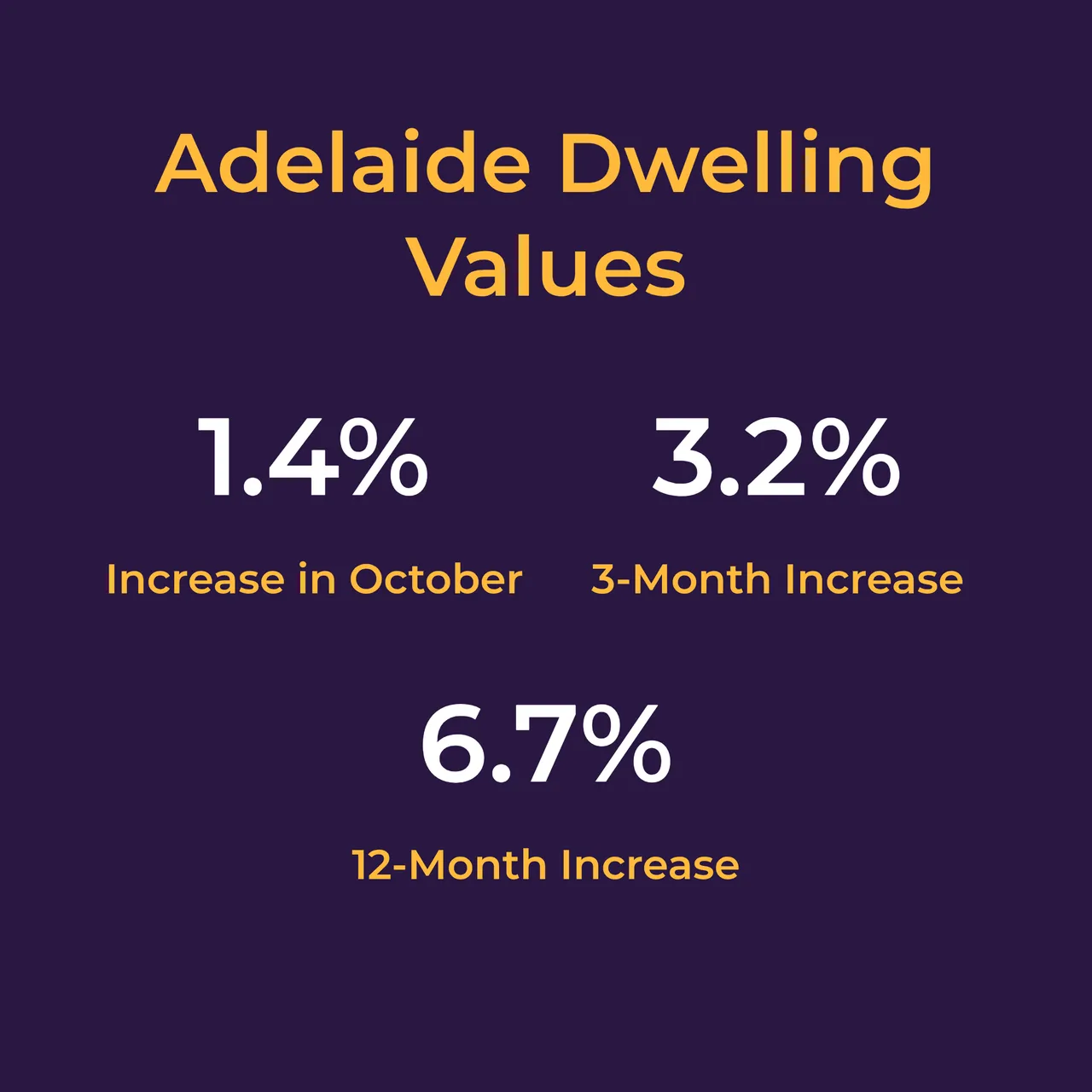

Price Overview

Adelaide remains one of the strongest-performing markets. Values rose 1.4% in October, 3.2% over the quarter, and 6.7% annually, reaching new highs.

Vendor discounting at −2.7% signals tight supply.

Median dwelling prices sit around $851k, with houses near $700k and units near $400k.

Rental Market

Vacancy rates are extremely low at 0.9%, and rents average $630 per week. Tenants face heavy competition for good properties.

Supply & Demand

Adelaide attracts steady interstate interest thanks to affordability and lifestyle — but its construction pipeline hasn’t kept up.

Desirable suburbs have very limited stock, making the market consistently competitive.

First-Home Buyer Activity

a $15k grant for new builds

some stamp duty concessions

Many first-home buyers target outer suburbs like Mount Barker and Munno Para.

Adelaide is still cheaper than Sydney or Brisbane, but affordability is tightening quickly — decisive buyers fare best.

Canberra

Price Overview

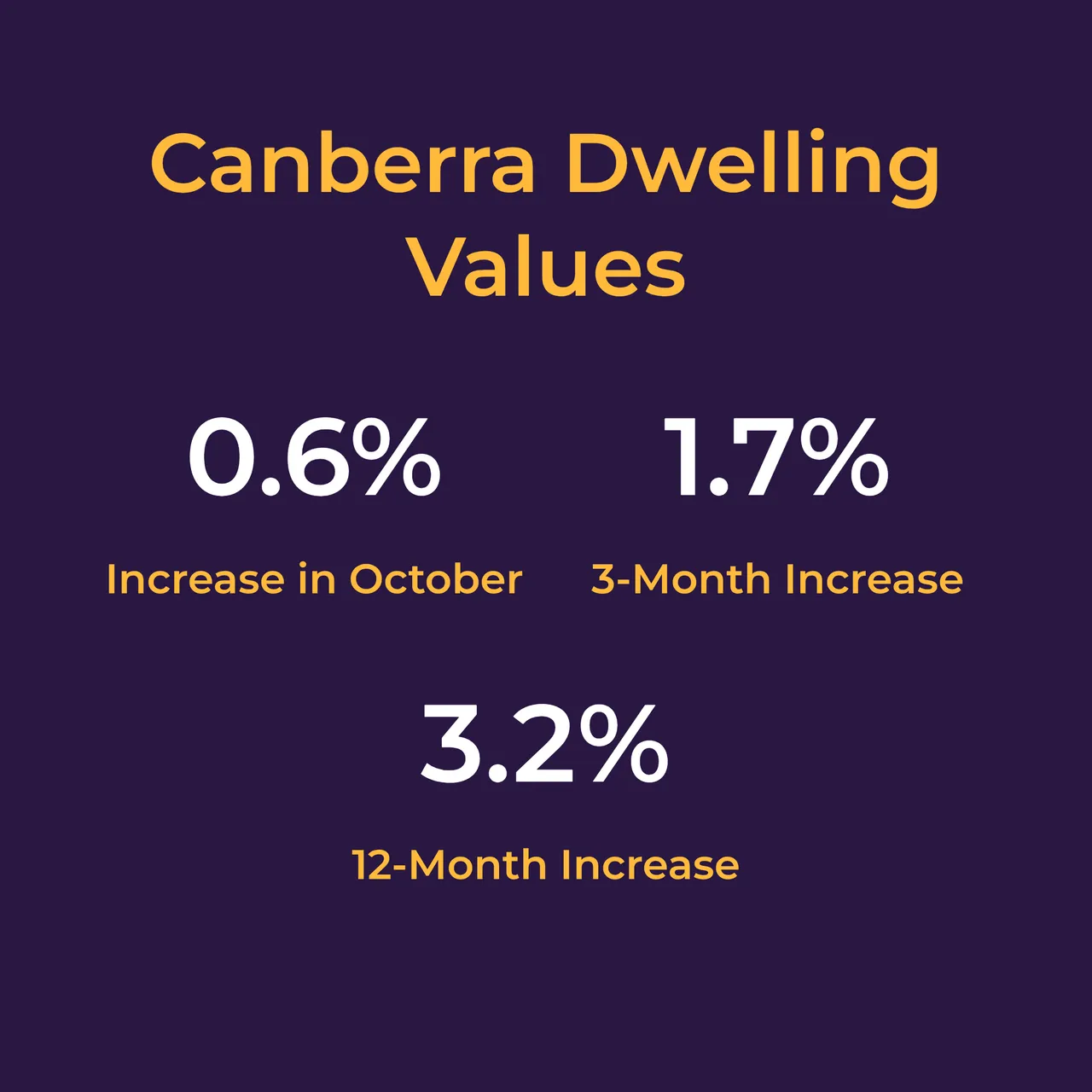

Canberra remains expensive, with a median around $873k.

Values grew 0.6% in October, 1.7% over the quarter, and 3.2% annually, but remain 3.5% below the 2022 peak.

Rental Market

Canberra’s rents are among the highest in the country at $680 per week. Some reports show vacancy rates as low as 0.3%, making renting incredibly tough.

Supply & Demand

However, land release is limited and planning is tight. Detached houses are rare; new stock is mostly apartments.

First-Home Buyer Activity

Canberra is surprisingly supportive for first-timers:

zero stamp duty for most eligible first-home buyers

$10k grant for new builds

federal FHG cap of $1m

Most first-home buyers start with units or townhouses due to the high cost of freestanding homes.

Hobart

Price Overview

Hobart’s boom has eased. Prices rose only 0.3% in October, 0.5% over the quarter, and 2.4% annually, still 8.9% below the 2022 peak.

Median dwelling value is about $680k, making it cheaper than most capitals.

Rental Market

Median rent is around $580 per week with vacancy between 1.7–2.2%. Conditions are tight but not as extreme as earlier in the decade.

Supply & Demand

Hobart’s small size makes it volatile. After huge investor-driven growth in the 2010s and COVID, demand cooled — but supply remains limited due to geography and slow construction.

Affordable homes under ~$600k still attract strong competition.

First-Home Buyer Activity

$10k FHOG (new builds)

stamp duty exemptions on established homes up to $600k

Local wages lag behind other states, making deposits challenging, so many buyers look to nearby regional towns or older fixer-uppers.

Darwin

Price Overview

Darwin is the cheapest capital city with a median around $553k.

But it’s also the fastest growing: values rose 1.6% in October, 5.4% over the quarter, and a massive 15.4% annually, hitting record highs.

Rental Market

Rents average around $650 per week, with vacancy around 1.7%. High yields (often 6–7%) attract investors.

Supply & Demand

Darwin’s market moves quickly because it’s small. Earlier oversupply of apartments has now been absorbed.

The current tightness is pushing both rents and prices higher, and any new mining or LNG project would increase demand even further.

First-Home Buyer Activity

Darwin remains accessible due to lower prices.

The NT offers:

$10k FHOG

stamp duty discounts

Many first-home buyers choose Palmerston or similar suburbs for affordability.

Because Darwin’s economy is tied to major projects, job stability is important — but strong rental yields make buying potentially attractive for long-term investors.

Conclusion and Next Steps

Buying your first home in Australia is challenging, especially in 2025. Prices are at record highs, and although interest rates have eased, they remain well above the ultra‑low levels of a few years ago. Supply shortages and strong demand continue to push values upward. Rents are high and vacancies are low, making the rental market tough. On the positive side, governments are offering more generous incentives than ever before, and lenders are cautiously increasing credit as rates stabilise.

Here are some key takeaways and next steps for first‑home buyers:

Start with a budget:

Work out how much you can afford to borrow based on current rates and stress test at higher rates. Consider your deposit, monthly repayments, and other costs like stamp duty, insurance and maintenance.

Explore incentives:

Check if you’re eligible for the First Home Guarantee, state grants, stamp duty concessions and other programs. These can reduce the up‑front cash you need significantly.

Consider different locations and property types:

Prices and affordability vary widely between cities and even suburbs. Don’t assume you must buy in the most expensive area you know. Look at units vs houses, or outer suburbs vs inner suburbs. Sometimes “rentvesting” can be a stepping stone into the market.

Get pre‑approval:

Speak with a mortgage broker to understand your borrowing capacity and obtain pre‑approval. This makes you a more credible buyer when you find a property.

The market evolves. Keep reading updated guides like this, follow property news and monitor economic indicators like interest rates and inflation. Being informed helps you act quickly and confidently when the time is right.

Seek professional advice:

Consider talking to a financial adviser or accountant, especially if using schemes like the FHSSS or contemplating a longer mortgage term. They can help you weigh the pros and cons based on your personal circumstances.

We hope this guide empowers you to take the next step toward owning your first home. While the journey may seem long and daunting, thousands of Australians achieve it each year by planning carefully, taking advantage of available support and making informed decisions. Good luck!