Essential guide on bad credit home loans and how to get approved

Check to see if you are eligible for a home loan

$

By Nathan Vecchio

Wondering how to secure a bad credit home loan without hitting a wall at every bank? You’re not alone — many Australians face credit setbacks but still dream of owning a home. The good news is there are paths forward, especially when you work with a mortgage broker in Brisbane who understands how to navigate complex credit situations. In this guide, we’ll walk you through proven strategies to improve your chances of approval, compare lender options, and help you take confident steps toward homeownership — even with a less-than-perfect credit history.

Let’s dive in.

Key Highlights

Having bad credit doesn’t mean you can’t get a home loan.

Specialist lenders understand that everyone’s financial situation is unique.

Your chances of approval depend on factors like your credit score, income, and deposit amount.

There are steps you can take to improve your chances of approval.

Understanding your credit report and working with a specialist mortgage broker can make a big difference.

What Is Considered Bad Credit For Home Loans?

Before we get into exactly how to get a home loan with bad credit history, let’s quickly talk about what “bad credit” means when you’re trying to get a home loan.

Essentially, a low credit score can make lenders a bit nervous because it signals that lending to you might be risky. So, what does a bad credit score look like?

Typically, if your credit score is below 660, many lenders consider that “average” or “below average.” This could indicate to them that you’ve had some financial hiccups in the past—maybe a few late payments, missed bills, or even something as serious as bankruptcy.

Can You Get a Home Loan With A Default or Bad Credit History?

Yes, you absolutely can get a home loan even if you have defaults or a bad credit history. I know it might seem daunting, but it’s definitely possible. While the big banks might be hesitant, there are specialist lenders out there who are more than willing to help people who’ve had credit issues in the past.

These lenders understand that life’s not always smooth sailing, and a low credit score doesn’t necessarily reflect where you’re at financially today. They’ll look at your entire situation, not just the numbers on your credit report. Just keep in mind that you might face higher interest rates, and a one-off risk fee may apply — typically somewhere between 1% and 3% of the loan, depending on the lender tier and your LVR. Additionally, lenders mortgage insurance (LMI) could be required—which is insurance that protects the lender in case you can’t repay the loan.

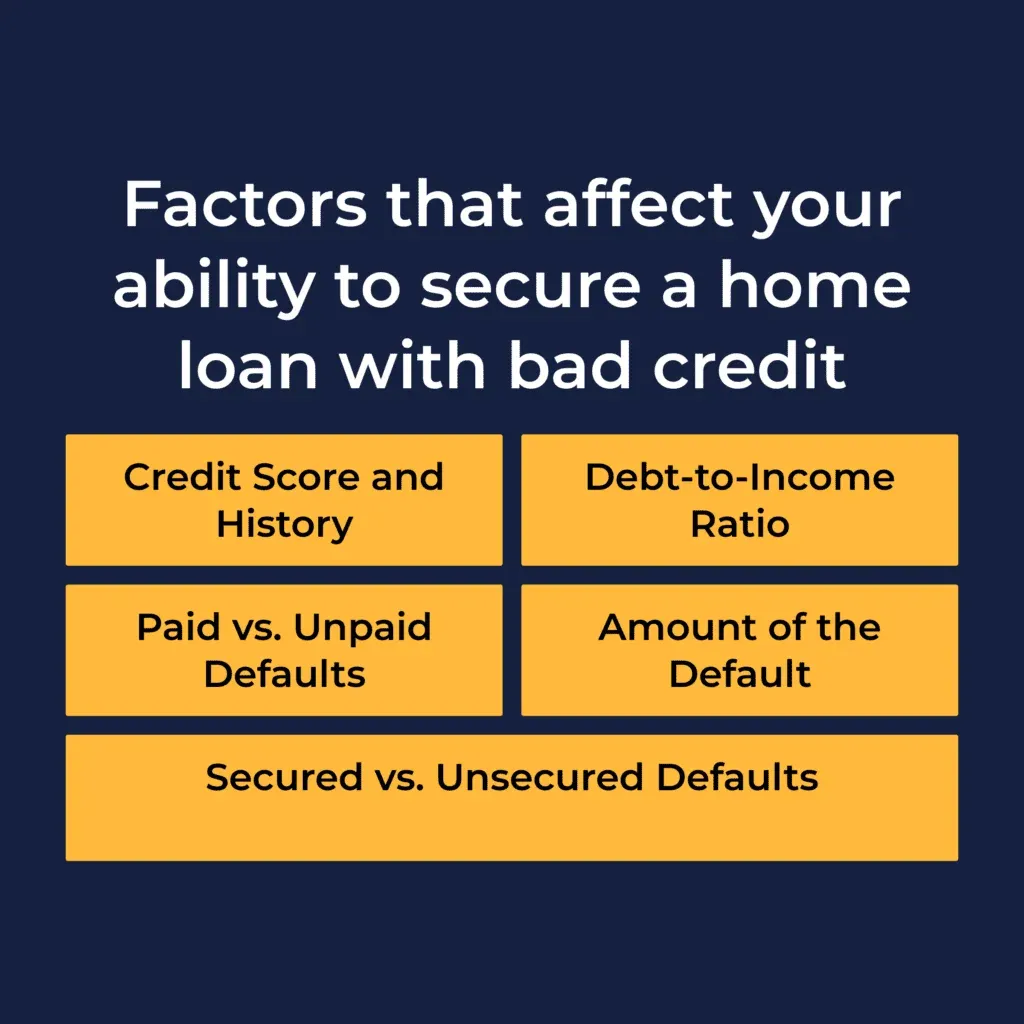

Factors That Affect Your Ability To Secure A Home Loan With Bad Credit

Understanding what lenders are looking for is crucial, especially when you’re dealing with bad credit. While your credit history is important, it’s not the only factor they consider.

Lenders will look at several key aspects before approving your loan:

Credit score and history

Payment status: paid vs. unpaid defaults

Debt-to-income ratio and other credit issues

Amount of the default

Secured vs. unsecured loans

If you can demonstrate good financial habits now—even if you’ve had issues in the past—it can really sway their decision in your favour. Let’s take a look at each of these key aspects in a little more detail.

1. Credit Score and History

Think of your credit report as your financial report card—it details your credit score and how you’ve managed your money over time. It includes everything from loans and credit cards to any late or missed payments. Having a poor credit score, also known as bad credit or adverse credit, can stem from things like defaults, late payments, or even bankruptcy. A low score can make lenders see you as a higher risk.

But here’s the thing: while your credit score is important, it’s not the whole story. Lenders also take a deeper look at your credit history to understand the context. They consider how severe any past issues were. For instance, a single missed payment from a few years back isn’t as concerning as multiple recent missed payments.

Showing recent positive financial behaviour can really change how lenders perceive you. Making payments on time demonstrates that you’re committed to improving your financial situation—even if your score is still on the lower side.

Let’s talk about defaults—specifically, paid vs. unpaid defaults. When they’re looking at your credit file, lenders will pay extra attention to any defaults that you may have. Ultimately, they want to make sure that you will pay them back the money that they lend you. And defaults make them worried because it means that you haven’t always paid your debts in the past.

Unpaid defaults suggest to lenders that you can’t—or won’t—pay your debts, which makes you seem riskier. If you are a high-risk applicant, then they might charge higher interest rates, tack on additional fees, or even decline your loan application altogether.

Paid defaults look much better. A paid default demonstrates that you’ve taken responsibility and settled your debts.

So if you do have any unpaid defaults, it’s best to address them as soon as possible. If you can’t pay them off completely, at least consider setting up a payment plan. This shows lenders that your committed to repaying your debts and can also help to improve your credit score over time.

3. Debt-to-Income Ratio and Other Credit Issues

Your debt-to-income ratio (DTI) is a big deal to lenders. It shows them how much of your income goes toward paying off debts like credit cards, personal loans, and car loans. A high DTI means you have less wiggle room for additional expenses, such as home loan repayments.

Lenders might interpret a high DTI as a sign that you’re financially stretched, which can make it harder to secure a loan. To improve your DTI, consider paying down existing debts, increasing your income, or both.

Also, lenders pay attention to other credit behaviours. For instance, if you’ve had multiple recent credit inquiries, it might appear that you’re scrambling for credit, which could raise red flags about your financial stability.

That’s why we recommend working with a mortgage broker when you’re looking to apply for a home loan – rather than apply for (and get declined for) multiple home loans, we can find you the best lender and give you the best chance of getting approved the first time. That will save you the credit inquiry and make your credit look healthier.

4. Amount of the Default

The size of any defaults on your credit file also matters. Lenders are generally more concerned about larger defaults than smaller ones. Big defaults might suggest you’ve had significant financial difficulties or issues managing money.

Borrowers with large defaults are seen as higher risk. Lenders may wonder if you can handle substantial debts like a home loan. As a result, they might impose stricter loan conditions, such as requiring a larger deposit to mitigate their risk.

On the other hand, smaller defaults—especially isolated incidents—might be viewed more leniently, particularly if your overall financial situation shows stability and responsibility.

5. Secured vs. Unsecured Loans

Lenders also consider how you’ve managed secured vs. unsecured loans in the past. Secured loans, like mortgages and car loans, are backed by collateral—if you default, the lender can seize the asset. Unsecured loans, like personal loans and credit cards, aren’t tied to any collateral.

Missing payments on secured loans is a red flag for lenders. It suggests that you might struggle to repay debts even when there’s an asset involved. Multiple missed payments on secured loans can significantly hurt your chances of getting a home loan.

In these cases, connecting with mortgage brokers who specialise in bad credit can be incredibly beneficial. They understand how to navigate these challenges and can guide you toward lenders who may be more accommodating to your circumstances.

How Specialist Lenders Assess Bad Credit

Getting a home loan with bad credit doesn’t always mean rejection. Specialist lenders evaluate more than just your credit score. Unlike big banks, they take a holistic view of your finances.

What Lenders Look At

Specialist lenders consider several key factors when assessing your application:

Current income: Lenders check your income stability to ensure you can meet repayments.

Repayment history since defaults: Showing consistent repayments can demonstrate financial responsibility.

Overall affordability: Lenders assess your living expenses, debts, and disposable income to confirm affordability.

Employment type and stability: Full-time, part-time, or contract work can all be considered differently.

Deposit size: A larger deposit can reduce perceived risk and improve approval chances.

Why Specialist Lenders Can Help

These lenders understand that life is not always predictable. They know past defaults do not always reflect current financial health. This flexibility can be crucial for first-time home buyers or those recovering from financial setbacks.

Takeaway

Specialist lenders offer alternatives if big banks say no. By understanding their assessment process, you can improve your application.

Check to see if you are eligible for a home loan

How Specialist Lenders Tier Bad Credit

Here’s the part most articles gloss over: the big banks and the specialist lenders aren’t just “strict” and “lenient” versions of the same thing — they run completely different systems. The majors use automated credit scoring with hard gates. Westpac and St.George look for a bureau score of about 650 or better, Macquarie automatically declines outstanding defaults, judgments and court writs, and ANZ’s scorecard weighs things like hardship flags and payday lender transactions. If your file trips one of those wires, a human often never even reads your application.

Specialist lenders do the opposite: a credit assessor actually reads your file, and instead of one pass/fail score they place you on a named product tier. As at July 2026, the tiers on our panel look like this:

Pepper Money runs four main tiers — Prime, Near Prime Clear, Near Prime and Specialist (plus Specialist PLUS for the freshest credit events). Prime accepts small paid defaults up to $500. Near Prime accepts unlimited defaults and judgments up to $3,000 each. Specialist takes larger defaults listed more than 12 months ago, and discharged bankruptcy from one day after discharge.

Resimac runs three specialist tiers — Clear, Plus and Assist — and counts credit events rather than individual listings (more on that below). Defaults under $2,000 are accepted up to 80% LVR on the Clear and Plus tiers.

La Trobe Financial is one of Australia’s larger specialist lenders and takes a case-by-case view of impaired credit — including recent defaults and discharged bankruptcy — rather than credit-scoring applications automatically. Specialist lenders like La Trobe price for risk, so rates and fees are higher than the banks, and the right move is usually to treat them as a stepping stone: clean up the file, build 6–12 months of good history, then refinance to a mainstream lender. Talk to us first — depending on your situation there may be a sharper option on our panel.

Roughly, here’s what that means for how much you can borrow against the property (LVR) in common bad-credit situations:

Your situation

Realistic maximum LVR

Where it typically lands

One small paid default (under $500)

Up to 95% purchase

Pepper Prime — the cleanest tier, with prime-style pricing

A few paid or unpaid defaults under $1,000

Up to 95% purchase

Pepper Near Prime Clear

Defaults or judgments up to $3,000 each

Up to 95% purchase (Pepper) / 80% (Resimac)

Pepper Near Prime; Resimac Clear or Plus

Larger defaults, listed more than 12 months ago

Up to 95% purchase, 85% refinance

Pepper Specialist

Court judgment, now resolved

Typically 80–90%

Tier depends on the size and age of the judgment

Discharged bankruptcy

Up to 80% (Pepper), from one day after discharge

Pepper Near Prime or Specialist; Resimac Clear

Current (undischarged) bankruptcy, entered 2+ years ago

Typically up to 80% (case by case)

Resimac — one of very few options in the market

Policy figures above are correct as at July 2026 and change without notice — they’re a guide to what’s possible, not a quote. Every file is assessed individually by the lender. Everything on this page is general information only and doesn’t take your personal circumstances into account — it isn’t credit advice or an offer of finance. Before acting on any of it, talk to us (or another licensed professional) about your specific situation.

One more thing the LVR number hides: loan size caps. The LVR cap and the maximum loan amount are two separate gates, and your loan needs to fit through both. At 95% LVR on Pepper’s Specialist tier, for example, the maximum loan is $650,000 (purchase only) — so if you need $1.2 million on that tier, you’re realistically capped at 90% LVR. This is exactly the kind of detail that decides whether a deal works, and it’s why we model both gates before recommending a lender.

One Life Event, Multiple Defaults? It Can Count As One

This is probably the single most useful thing to know if a divorce, illness or business failure knocked your finances around: Resimac doesn’t count your defaults one by one — it counts credit events. Their policy treats a credit event as a single cause that produced one or more adverse listings, provided all the listings trace back to that cause and fall within a six-month window.

In practice: a separation that produced four defaults across three lenders over five months is one credit event — which can keep you on the Clear or Plus tier with materially better pricing. Four defaults from four separate months of overspending? That’s four events, and a very different conversation.

The difference between those two outcomes often comes down to how your story is documented. That’s what a well-written explanation letter is actually for — it isn’t a formality, it can literally determine which tier (and interest rate) you’re offered.

What If You’ve Missed Mortgage Repayments?

Lenders treat missed mortgage repayments more seriously than any other arrears — a missed credit card payment and a missed home loan payment are not the same thing in their eyes. But even here there’s a ladder rather than a locked door (as at July 2026):

One missed mortgage payment in the last six months: still workable — Pepper’s Specialist tier accepts it, as can Resimac’s Plus tier (Resimac’s Clear tier requires a clean mortgage repayment history).

Two missed payments: you move up the risk curve — think Pepper Specialist PLUS, where the maximum LVR drops to 80% (75% for alt doc).

Three or more: you’re into the deepest tiers (such as Resimac Assist), where lending is still possible but pricing and cash-out are tightly restricted.

If you’ve caught your repayments back up after a rough patch, make sure that’s front and centre in your application — recency and recovery both matter.

What About ATO Tax Debt?

Tax debt is one of the sharpest dividing lines between the majors and the specialists. CBA explicitly excludes paying out tax debt as a loan purpose. Macquarie won’t let you pay out tax debt from the loan either (though it can live with an existing payment plan in limited circumstances). Westpac treats it as an exception needing credit sign-off.

The specialist lenders on our panel take a very different view (as at July 2026):

Pepper Money allows unlimited debt consolidation including ATO debt on its Near Prime and Specialist tiers — and can even leave an existing ATO payment plan in place after settlement.

Resimac allows unlimited cash out to pay out ATO debt on its Clear and Plus tiers (the deepest Assist tier caps cash out at $10,000).

La Trobe Financial lends for “any worthwhile purpose”, which includes paying out the tax office.

The “payment plan can stay in place” point is one most borrowers (and frankly, plenty of brokers) don’t know about — it means a tax debt doesn’t always have to be cleared, or even consolidated, for the loan to proceed.

Bankruptcy And Part 9 Debt Agreements

Most pages on this topic tell you that you need to wait years after bankruptcy. The current policy reality is more nuanced (and more hopeful):

Discharged bankruptcy: Pepper’s policy accepts discharged bankrupts from literally one day after discharge on its Near Prime and Specialist tiers, capped at 80% of the property value — so you’ll need around a 20% deposit. You don’t have to wait two years, though you’ll pay for the recency.

Part 9 and Part 10 debt agreements: Pepper accepts them on its Specialist tiers, and Resimac’s Plus tier can work with a current agreement that was entered two or more years ago — meaning in some cases the new loan pays the agreement out and you emerge with a single mortgage.

Current (undischarged) bankruptcy: the hardest scenario, but not automatically hopeless — Resimac’s deeper tiers are among the very few products in the market that can consider a current bankrupt, typically at up to 80% LVR (case by case, and subject to loan size caps).

A very honest caveat: these are the rarest, most conditions-heavy approvals in the market. Anything involving a current bankruptcy or an active debt agreement should be scoped directly with the lender before an application goes anywhere near your credit file. That’s a conversation we have on your behalf — without lodging anything.

Real Client Stories: What Bad Credit Actually Looks Like

These are real scenarios from our client work over the past year (names changed). They show how differently the same file can land at different lenders — and why the order you approach lenders in matters so much.

One missed repayment, two very different answers

Marcus, a first home buyer, had a single missed credit repayment on his file. His first-choice lender declined — their minimum credit score rule is black and white, and no amount of pleading his case changed it. The same day, we had already cleared his scenario with another major bank and moved the identical application across at 5.99% instead of 5.89%. One missed repayment cost him 0.1% — not the house.

Same couple, same income — declined at 95%, approved at 80%

Declan and Erin hit an automatic scorecard decline at a major bank on a 95% LVR application — and the assessor herself admitted nobody knows every factor the scorecard weighs. Trial runs came back declined at 90%, then approved at 80%: a $1,040,000 loan. Nothing about the couple changed; only the LVR did. It’s also why firing off application after application is so dangerous — every failed run damages the score further.

The hidden hardship flag

Sophie paused repayments for three months on a $6,000 personal loan — without realising she was being recorded as in financial hardship. The flags sat quietly next to green ticks on her Equifax file, and her lender treated them as hardship even though her other credit bureau file was completely clean. We pulled the application before it did damage and got the flags addressed — the difference between standard lending and non-conforming rates that started at 6.99% and ran to 7.79%.

The tax debt that blew out the valuation

Sarah’s refinance to consolidate an ATO tax debt hinged on a valuation that came back well under estimate, pushing her LVR from about 70% to 87% and adding $9,152 in LMI. With only a small handful of lenders accepting ATO debt at the time — Pepper Money among them — the smarter play was a personal loan to clear the tax debt first, which instantly reopened every lender on the panel for a cheaper refinance later. Sometimes the right answer isn’t the loan you first asked about.

Would you like to learn about your situation?

Steps To Improve Your Chances Of Getting A Home Loan With Bad Credit

Having bad credit might feel like a major hurdle, but there are concrete steps you can take to improve your chances of getting a home loan:

Check and understand your credit report

Pay off debts and defaults

Write a default explanation letter

Save for a larger deposit

Work with specialist lenders

1. Check and Understand Your Credit Report

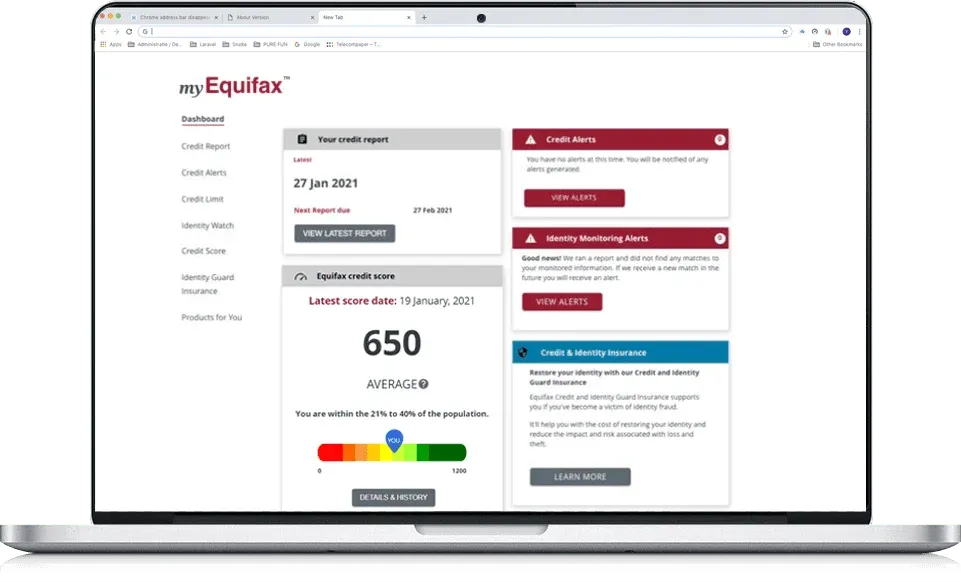

First things first, get a copy of your credit report from reputable agencies like Equifax, Experian, or Illion. This report gives you a comprehensive view of your credit history, including active accounts, payment history, and any negative marks.

Go through your credit report with a fine-tooth comb. Make sure all the information is accurate and up-to-date. Look out for errors in personal details—like incorrect addresses—or accounts that aren’t yours. These mistakes can drag down your credit rating, so if you find anything that’s incorrect, dispute these issues as soon as possible.

Late payments, high credit card balances, and multiple recent credit applications can all negatively affect your score. By adopting good financial habits, you can improve your credit over time.

Your credit report will show you your credit score and any potential issues with your credit rating

2. Pay Off Debts and Defaults

Addressing outstanding debts and defaults on your credit file is crucial for improving your home loan prospects. Lenders favour applicants with a solid payment history, as it indicates responsible money management.

Start by settling any missed payments or overdue debts.

Prioritise older debts first. Clearing these shows you’re committed to resolving past financial issues.

If you can’t pay everything at once, consider setting up payment plans with your creditors.

For multiple high-interest debts, think about debt consolidation. This involves combining your debts into a single loan with a lower interest rate, simplifying your payments and potentially boosting your credit score over time.

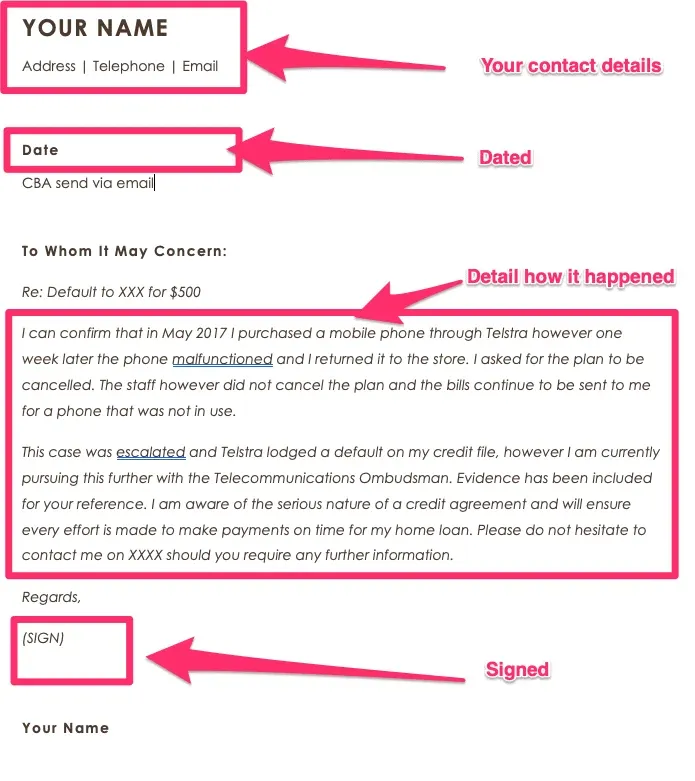

3. Write a Default Explanation Letter

Life can throw curveballs that lead to defaults on your credit file—things like unexpected medical bills or job loss. In these situations, including a default explanation letter with your loan application can be incredibly helpful. It gives lenders context and shows transparency.

A solid default explanation letter should include:

Default Details: Account name, default date, and amount.

Reason for Default: A clear explanation of what led to the missed payments.

Steps Taken: Actions you’ve taken to resolve the issue, like payment plans or settlements.

Lessons Learned: How you’ve improved your financial management since then.

Including supporting documents, such as medical bills or termination letters, can strengthen your case.

Here's an example of a default explanation letter that you can use as a template.

4. Save for a Larger Deposit

Saving up a larger deposit can significantly boost your chances of home loan approval, especially when you have bad credit. A substantial upfront payment reduces the lender’s risk and lowers the loan-to-value ratio (LVR).

A larger deposit makes lenders more comfortable, even if your credit history isn’t perfect. It signals financial responsibility and reduces the likelihood of loan default.

You might also avoid paying Lenders Mortgage Insurance (LMI) if your LVR drops below 80%, saving you money in the long run.

Overall, a bigger deposit not only increases your approval chances but also reduces the total cost of your home loan.

5. Work with Specialist Lenders

Mainstream banks might not be the best option if you have bad credit, but specialist lenders can step in to help. These lenders understand that a less-than-perfect credit history doesn’t define your current financial situation.

Specialist lenders offer tailored home loan products for people with bad credit, considering factors beyond just your credit score.

Working with a mortgage broker experienced in bad credit loans can be incredibly beneficial. They can connect you with lenders suited to your circumstances and guide you through the application process.

Contesting Or Removing Defaults From Your Credit File

Regularly reviewing your credit file is essential. If you spot errors or believe a default is inaccurate, you have the right to dispute it with the credit provider.

Gather evidence, such as payment receipts or correspondence with creditors, to support your claim.

Submit a formal dispute to the credit provider, clearly explaining why the default is incorrect.

The credit provider will investigate, and if they find the default is wrong, they will correct or remove it from your file.

If you’re not sure exactly who to contact to correct your report, don’t worry. It doesn’t matter whether you request the correction from the wrong provider or bureau. They are legally required to consult with other credit providers or credit reporting bodies to help you out. This is called the “no wrong door approach”.

For more information, the OAIC has an excellent guide to correcting your credit report. You can find it here: Correct your credit report

How To Apply For A Bad Credit Home Loan

A low credit score shouldn’t deter you from applying for a home loan. Understanding the application process and preparing the necessary documents can make a significant difference.

Consider consulting a mortgage broker who specialises in bad credit loans. They can provide valuable guidance tailored to your situation.

Timing is crucial. Applying when you’ve demonstrated financial stability can enhance your approval chances.

Timing Your Application

Applying for a mortgage when you have bad credit can be daunting, but proper timing can improve your chances.

Review your credit report thoroughly to identify and correct any errors.

Demonstrate responsible financial behaviour by paying bills on time and reducing debts.

Avoid applying for new credit, as multiple inquiries can negatively impact your score.

Once you’ve improved your financial standing, start reaching out to lenders.

Remember, lenders have different criteria, so it’s wise to compare options to find the best fit for your circumstances.

Applying with Specialist Lenders

If your credit history isn’t stellar, specialist lenders can be a viable option. They take a more holistic view of your financial situation, not just your credit score.

They consider factors like your income, employment stability, and savings history.

Interest rates may be higher, but these lenders are often more willing to work with individuals who have credit issues.

When applying, be prepared to provide comprehensive documentation, such as bank statements, payslips, tax returns, and explanations of past credit problems.

Conclusion

Getting a home loan with bad credit is challenging but certainly achievable. By understanding what bad credit entails and taking proactive steps to improve your financial situation, you can enhance your approval chances.

Regularly review your credit report and address any inaccuracies.

Pay off outstanding debts and save for a larger deposit.

Consider working with specialist lenders and consult experts like mortgage brokers who understand bad credit scenarios.

With determination and a solid plan, you can move closer to homeownership, even if you’ve faced financial hurdles in the past. Keep your eye on the prize and continue taking steps to improve your credit.

Bad Credit Home Loans Frequently Asked Questions

What’s the difference between a specialist lender and a bank for bad credit home loans?

Banks usually require strong credit scores, while specialist lenders review your overall financial situation. They may still approve borrowers with defaults, missed payments, or other bad credit problems.

Can I get a home loan if I have multiple defaults or unpaid debts?

Yes, but it’s harder. Specialist lenders might require a larger deposit or charge higher fees. Showing stable income and a repayment plan can improve your loan approval chances with bad credit.

What is the minimum credit score needed to get a home loan with bad credit?

There’s no fixed minimum. Each lender sets its own criteria. Factors such as your deposit size, income stability, and repayment history weigh more than the score itself.

How long do defaults stay on my credit file, and will they affect my chances of buying a house?

Defaults remain for five years, but their impact reduces if you maintain a good track record. Even with a default on your credit report, you may still qualify for a home loan with the right lender.

Will I always pay higher interest rates with a bad credit home loan?

Bad credit home loans often start with higher rates, but some lenders lower rates if you prove reliability. A larger deposit can also help you secure better home loan interest rates.

Can I refinance a mortgage with bad credit?

Yes. Refinancing your home with bad credit is possible, especially if your score has improved. Some lenders offer refinance loans with bad credit tailored to borrowers rebuilding their financial position.

How much deposit do I need for a bad credit home loan as a first home buyer?

Deposit requirements vary. Some lenders ask for 20%, while others accept smaller deposits with Lenders Mortgage Insurance (LMI). First home buyers with bad credit may still qualify for low-deposit options.

Can I get a home loan while still bankrupt (undischarged)?

In rare cases, yes. As at July 2026, Resimac’s deeper specialist tiers can consider a current bankrupt whose bankruptcy was entered two or more years ago, typically at up to 80% LVR. Conditions are strict and every file needs to be scoped with the lender before applying — but “you must be discharged first” is no longer universally true.

Can first home buyers use specialist bad credit lenders?

Yes — specialist lenders write first home buyer loans too, including alongside past defaults. One wrinkle worth knowing: Resimac restricts first home buyers to its Clear and Plus tiers (not its deepest Assist tier), so heavier credit histories may need a different lender.

Can I get a low-doc or no-deposit home loan with bad credit?

It’s difficult, but not impossible. Specialist lenders sometimes approve bad credit home loans for first-time buyers with little documentation or no money down, though stricter terms and higher rates usually apply.

Next Steps And Getting Your Bad Credit Home Loan Approved

Our team at Hunter Galloway is here to help you buy a home anywhere in Australia. Unlike one-person operations, we have a full team of experts who specialise in making the home loan process simple and stress-free. If you’re looking for experienced home loan brokers for bad credit, we can guide you through your options and improve your chances of approval. To get started, call us on 1300 088 065 or book a free assessment online today.