Thinking about buying out your partner after a separation? It’s a big decision — both financially and emotionally. Whether you’re trying to stay in the family home or keep things stable for the kids, this guide will walk you through the legal, financial, and personal angles—so you know exactly what to expect.

We’ll cover the key steps, including preparing your finances, negotiating the buyout terms, and completing the legal and financial transactions.

To learn more about how to calculate buying someone out of a house in Australia, you can watch the video below or read on for our detailed guide.

How To Buy Someone Out Of A Mortgage

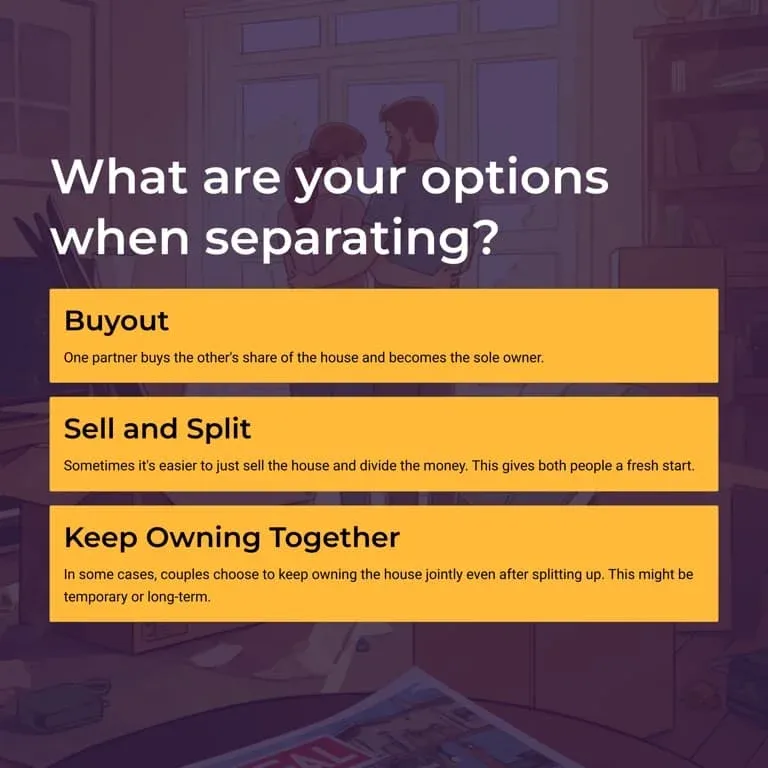

When separating from a partner and deciding what to do with a shared home in Australia, there are usually three main options:

Buyout: One partner buys the other’s share of the house and becomes the sole owner.

Sell and Split: Sometimes it’s easier to just sell the house and divide the money. This gives both people a fresh start.

Keep Owning Together: In some cases, couples choose to keep owning the house jointly even after splitting up. This might be temporary or long-term

Here are some things to think about with each.

Buyout

Can you afford to pay the other person’s share and handle the mortgage alone?

Do you want to stay in the home for emotional reasons or to keep things stable for kids? While this is important, be careful you’re not sacrificing too much financially for emotional reasons.

Does the property work for your long-term plans? Staying could be good if you want to remain in the area.

Sell and Split

Selling gives both people a clean break financially and emotionally. It splits things simply and fairly.

Consider whether the housing market is good for selling now.

Think about where you’ll live after selling – will you have enough money to buy or rent a new place?

Keep Owning Together

Keeping the house could provide consistency for kids. It could be temporary until selling is better. However, this can be messier and more difficult to manage.

If the market is bad for selling, waiting and co-owning allows more time.

If you choose this option, make sure you have agreed on a clear plan for selling the home or buying out your partner’s share of the house.

Making Your Decision

There’s no one-size-fits-all option. Get input from lawyers, financial advisors, and real estate agents to understand your full situation. Think about budgets, emotions, and future plans. This is a big choice for your money and well-being, so consider carefully!

How The Family Law Act Influences The Property Split When Buying Out Your Ex

In Australia, property settlements during a separation are governed by the Family Law Act 1975.

If you’re planning to buy your ex-partner out of a shared home in Australia, it’s easy to assume everything will be split 50/50. But in reality, property settlements during a separation—whether you’re married or in a de facto relationship—are guided by the Family Law Act 1975.

This means the final property split might not be exactly equal – especially if one person contributed more or has greater future needs.

Understanding how the Family Law Act works can help you calculate a fair buyout amount and avoid surprises during negotiations.

What Does "Just and Equitable" Really Mean?

The Family Law Act focuses on making the property split just and equitable, not necessarily equal. That means the court (or your legal team) will look at a range of factors before deciding who gets what share of the home.

Even if you’re not going to court, most lenders and lawyers will want to see that your buyout arrangement reflects these legal principles — especially if you’ll be refinancing the mortgage into your name alone.

Let’s look at the key things the law considers.

1. Financial Contributions

This is usually the starting point. It includes things like:

Paying the house deposit

Making mortgage repayments

Covering major renovations or upgrades

Paying rates, utilities, or insurance

If one person contributed more financially, that might increase their share of the equity.

2. Non-Financial Contributions

The Family Law Act also values unpaid efforts, such as:

Maintaining the home (repairs, gardening, cleaning)

Supporting your partner’s career or studies

Acting as the primary homemaker

Even if you didn’t earn an income, your contributions to the household still count.

3. Parenting and Homemaking Contributions

If one partner took time off work to care for children or managed most of the home duties, that’s also considered a significant contribution. These roles often impact future earning potential—and that’s factored in.

4. Future Needs of Each Partner

This part looks ahead. The law considers:

Your age and health

Your income and job security

Whether you’ll be the primary carer of any children

Any other financial obligations or dependants

For example, if you’ll have full-time care of the kids, you may be entitled to a larger share of the equity to support long-term stability.

5. Length of the Relationship

In long-term relationships, the courts usually treat most assets as shared, regardless of who paid for what. But in shorter relationships, direct contributions (like who paid the deposit) may carry more weight.

Why This Matters for Your Buyout

Even if you and your ex agree on the numbers privately, banks and lawyers may still ask for a financial agreement or court order that reflects the Family Law Act’s principles. If your agreement seems unfair, the bank may reject your refinancing application—or it could cause problems down the track.

Understanding these factors can help you:

Avoid underpaying or overpaying during the buyout

Strengthen your refinancing case with the lender

Finalise the property transfer smoothly and legally

Step-by-Step Buying Someone Out Of A House

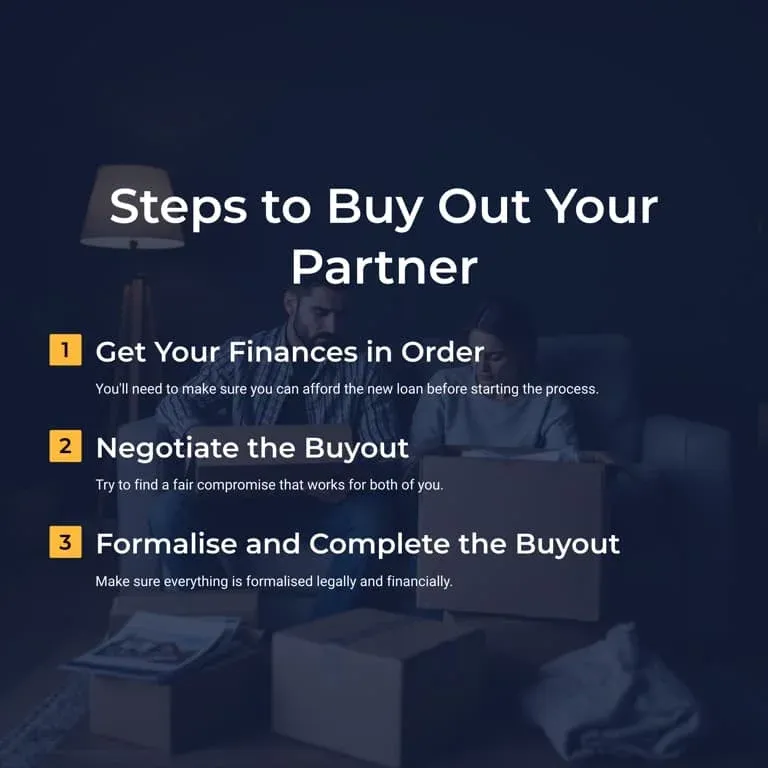

Step 1. Initial Preparation

If you decide that buying out your ex’s share of the home is the best option, here are some key steps to take first:

Get Your Finances in Order:

Talk to a mortgage broker to review your budget and what you can afford.

Look at your income, expenses, savings, loans, and more. This helps you know if you can handle the buyout.

Discuss options to get money for the buyout, like using savings or getting a loan.

Get an independent certified valuer or agent to formally value your property. This is vital for calculating your ex’s share.

The valuation considers recent area sales, the home’s condition, market trends, and more. This info helps both the buyout and your future investment.

Make sure the valuer understands the local market and has experience valuing similar homes.

Learn About Your Mortgage Options:

If you have a joint mortgage, talk to your lender or broker about refinancing the loan into your name only.

They’ll check if your income, credit, and obligations allow you to qualify for a new loan.

Explore different products to see what loan terms may suit your new situation best.

After organising your finances, having the property valued, and researching mortgages, you’ll be in a better position to move ahead with the buyout process.

Step 2. Negotiating the Buyout

After getting your finances in order and obtaining a property valuation, the next big step is to negotiate the buyout details with your ex. This can be tricky, but having some support in place helps.

Communicate Openly and Fairly:

Have honest talks about what you both want and expect. Listen carefully to understand your ex’s views.

Any agreement must be fair to both of you — consider both legal rights and emotional attachments.

Remember, this impacts both your futures in big financial and emotional ways.

Get Professional Help:

Mediators facilitate talks, offer neutral advice, and guide you through disagreements.

Legal advisors make sure deals follow all laws properly and formalise contracts.

Many couples use both mediation to negotiate and lawyers to finalise agreements.

Set Things Up for Success:

Have all your financial information (budgets, valuations, etc.) handy to keep discussions fact-based.

Be prepared to compromise on some wishes and keep your expectations realistic.

Know that this process can be lengthy and emotional. Respect and patience matter.

Balancing openness, fairness, and professional support can lead to a buyout contract that works for both people—setting you both up for brighter futures.

Step 3. Completing the Buyout

Once you’ve agreed on the buyout terms, it’s time to formalise everything legally and financially:

Transfer Ownership Legally:

Engage a conveyancer or property lawyer to handle the paperwork for transferring the title from both names into just your name.

A conveyancer or property lawyer handles filing the right documents properly.

They’ll organise a settlement date to finalise legal and financial transactions.

Refinance Your Home:

If you have a joint mortgage, you’ll need to refinance in your name only. This releases your ex from the loan.

The lender decides if you can afford the full mortgage based on your finances.

Discuss the new loan’s interest rate, repayment term, and other conditions with your lender.

Document Everything:

Draft a contract outlining every buyout detail, like amounts and timelines.

Have your lawyer review to ensure it is binding and protects you.

Both of you sign the needed paperwork and file it with authorities.

Keep copies of all documents related to the buyout.

Completing all the legal, financial, and paperwork steps will ensure a smooth transition to you becoming the property’s sole owner

How To Calculate Buying Someone Out Of A House

The first step in calculating the cost of buying someone out of a house is to understand home equity.

Understand How Home Equity Works

A key piece is deciding how much money your ex gets in the buyout. This depends on the home’s total equity and valuation.

Equity is the portion of the home’s value that you truly own outright, not counting what’s owed on the mortgage..

To get the equity, first find the property’s current market value. Then subtract what is still owed on the mortgage.

For example: a $500K home with a $300K mortgage has $200K equity.

Home buyout calculator

How Valuation Impacts Equity

Themarket value can shift a lot based on market conditions, nearby sales, the state of repair of the home, and other factors.

So you need an independent, certified valuer to consider location, size, age, trends, and other things.

If the home’s valuation has increased since purchase, there will be more equity to split – which likely means a higher amount needed for the buyout.

Getting the equity and valuation right is vital for figuring out a fair buyout amount to offer your ex for their share.

Factors That Affect The Buyout Price

Calculating a buyout involves more than basic math – factors like the remaining mortgage, home improvements, and the current housing market can all influence the final price.

Mortgage Amount Left:

The remaining mortgage owed directly lowers the total equity to split.

For example, an $800,000 home with a $300,000 mortgage has $500,000 in equity. One partner’s half share would be $250,000 – significantly more than if the mortgage were $500,000 (which would leave only $300,000 equity to split).

Also, remember that refinancing to take on the entire loan yourself will affect your budget (higher repayments, different loan terms, etc.).

Home Improvements:

Upgrades and renovations can raise the property value, increasing the equity and buyout price.

Keep records of major home projects to show the valuer and justify a higher price.

However, not all renovations add value – for example, an outdated kitchen remodel may no longer increase the property’s value in today’s market.

Shifting Housing Markets:

Property values can rise or fall significantly based on buyer demand, the broader economy, and other factors..

Current market conditions will heavily influence the valuation; for instance, a sellers’ market versus a buyers’ market can lead to very different outcomes.

Even local developments (like new construction projects or major employers moving into the area) can affect your home’s value.

By considering all these factors, you can calculate a fair buyout amount. This diligence helps ensure your ex-partner receives their fair share.

Check to see if you are eligible for a home loan

Case Study 1: Buying Out The Family Home – Married Couple in Melbourne

Sarah and James bought a 3-bedroom house in the outer suburbs of Melbourne in 2019 for $720,000.By 2025, it’s valued at $880,000. They still owe $420,000 on the mortgage.

Sarah wants to stay in the house with their two kids. That means she needs to buy out James’s share of the equity in the property.

Here’s the breakdown:

Current property value: $880,000

Remaining mortgage: $420,000

Equity in the home: $880,000 – $420,000 = $460,000

Each person’s share (assuming 50/50 split): $230,000

Sarah’s buyout amount: $230,000

Sarah refinances the home loan to $650,000 (covering the existing $420,000 balance plus James’s $230,000 equity share). With a binding financial agreement and a Family Court consent order in place, she avoids paying stamp duty on the transfer. She does incur some costs, including legal fees (approximately $3,000–$5,000) and refinancing charges ($1,500).

Case Study 2: Unit Buyout – De Facto Couple in Brisbane

Daniel and Mia were in a de facto relationship and bought a 2-bedroom unit in Brisbane in 2021 for $520,000. By 2025, it’s valued at $590,000. They still owe $360,000 on the home loan.

Daniel wants to keep the unit and buy out Mia’s share.

Here’s the breakdown:

Current property value: $590,000

Remaining mortgage: $360,000

Equity in the property: $590,000 – $360,000 = $230,000

Each person’s share (50/50 split): $115,000

Mia’s buyout amount: $115,000

Daniel refinances the loan to $475,000 to cover the remaining mortgage plus Mia’s $115,000 share.

They formalise the arrangement with a Family Court consent order, so no stamp duty is payable on the transfer.

Total extra costs (legal fees, refinancing fees, valuation costs) came to around $5,000.

Tax Implications Of Buying Out Your Partner

When you buy out your partner’s share of a property, it’s not just about refinancing. You also need to consider the tax consequences—especially capital gains tax (CGT) and stamp duty.

The good news: in most family law settlements you can avoid major tax hits — as long as the property transfer is handled correctly.

In a relationship breakdown scenario, CGT can be deferred if the property transfer is done under a binding financial agreement or a court-issued consent order.

Here’s how it works:

You won’t pay CGT at the time of the buyout.

Instead, the cost base of the property transfers to the person keeping the home.

If you later sell the property, any CGT will be calculated based on the home’s original purchase price (the cost base).

Important: If you don’t formalise the transfer with a legal agreement or court order, CGT could apply immediately as a normal taxable sale.

Stamp Duty When Buying Out Jointly Owned Property

In most Australian states, you won’t have to pay stamp duty on a buyout if:

The property is being transferred due to a separation, and

You have a binding financial agreement or Family Court consent order.

This exemption applies to married, de facto, and same-sex couples. Always check your state’s regulations, as stamp duty laws and processes vary between jurisdictions (NSW, VIC, QLD, etc.).

Other Tax Considerations

Rental properties have additional CGT implications.

If the property was your primary residence, it’s likely that no CGT will apply when you eventually sell.

Talk to a tax adviser to avoid costly mistakes.

Breakdown Of Fees And Costs When Buying Out Your Ex

Buying out your ex involves more than just paying their share of the home. Here’s a full breakdown of the key fees and costs you’ll need to factor in:

Property Valuation Fee – You’ll need a formal independent valuation to determine the current market value of the home. This helps calculate how much you owe your ex. Valuations typically cost between $300 – $600 in Australia.

Legal Fees – You’ll need a solicitor or family lawyer to draft the settlement agreement. This ensures the buyout is legally binding. Legal fees range from $1,500 up to $5,000, depending on complexity of the case.

Refinancing Costs – If you’re refinancing the home loan under your name, the lender may charge fees. These can include loan application fees, settlement fees, and discharge fees. Expect to pay around $600 to $1,200 in total.

Stamp Duty (Sometimes) – In many cases, stamp duty is exempt if the transfer is court-ordered or part of a family law settlement. But if it’s not, stamp duty can be a big-ticket cost, especially in states like NSW or VIC. Check your state’s laws or speak to your conveyancer to confirm.

Court Order or Consent Order – To avoid stamp duty and make the split legally enforceable, you might need a consent order or binding financial agreement. These can cost around $1,000 to $3,000, depending on your lawyer.

Title Transfer and Registration – You’ll need to update the title to remove your ex’s name. This is a straightforward process but comes with state-based fees. In most states, expect to pay between $200 to $400.

Lenders’ Mortgage Insurance (if applicable) – If refinancing pushes your loan-to-value ratio (LVR) above 80%, you might have to pay Lenders Mortgage Insurance (LMI). This one-off premium can amount to thousands of dollars added on top of your loan. It’s best to check with your broker before committing.

Loan Break Costs (Fixed Loans Only) – If your current home loan is fixed, breaking it early can attract penalties. These vary by lender and the remaining fixed term. Always ask your lender for a payout figure before refinancing so you’re aware of any break costs.

Pros and Cons Of Buying Your Ex-Partner Out Of The House

Buying your ex out of the home can feel like a win, but it’s not always the right move. Let’s break down the pros and cons so you can make a confident decision.

Pros of Buying Out Your Ex

Buying out your ex has many pros - including keeping the family home

You keep the family home – You won’t have to pack up or move, avoiding major upheaval in your life. Staying in a familiar space can also provide emotional comfort and closure after the separation.

No need to sell and move. Selling the property involves hiring real estate agents, hosting open homes, and negotiating with buyers. By buying out your ex’s share, you skip all of those hassles. The process becomes much smoother and more private, allowing you to move forward on your own terms.

Kids stay in a familiar environment. Children often cope much better when their home life remains the same after a separation. They can continue with the same school, local friends, and routine, which reduces disruption during an already emotional time.

You avoid costly selling fees. Selling a house comes with real estate commission, marketing costs, and legal fees. A buyout skips all of that. You save tens of thousands and avoid the hassle.

You gain full control of the asset. Owning the home outright means you have complete say in what happens next. You can renovate, refinance, or sell on your own timeline with no need for joint decisions or negotiations.

You retain all future capital growth – If the property is in a high-growth area, keeping it could be a very smart financial move. By staying as the sole owner, you’ll reap 100% of any future increase in value, which can significantly boost your net worth over time.

No arguments over sale price or timing – Selling jointly can lead to disagreements about when and for how much to sell. With a buyout, those conflicts disappear. You can decide if and when to sell in the future entirely on your own terms..

You maintain stability after separation – A home is more than just bricks and mortar; it represents security and familiarity. Keeping your home can provide both emotional comfort and financial stability, which is vital after a major life change.

Cons of Buying Out Your Partner From The House

You must qualify for a new loan on your own – Lenders will assess your income, expenses, and debts based on a single income now. This can make it harder to borrow the full amount needed. You might need a bigger deposit or an excellent credit history to get approved.

You might face stamp duty costs – In some states, stamp duty still applies to a buyout, even between ex-partners. While exemptions are available in many cases, they only apply under certain conditions (usually with the right legal orders in place). It’s important to get legal advice to know if you qualify for an exemption.

You might need a court order or agreement – Most lenders will require a Family Court consent order or a binding financial agreement outlining the terms of your settlement. This protects both parties and clearly states who gets what. Arranging this paperwork takes time (and legal fees), so factor that into your plan.

You take on a larger debt load – Buying out your ex means you’re taking over their share of the mortgage (and possibly increasing the loan to pay them out). Your monthly repayments will increase accordingly. It’s critical to budget carefully and ensure you can comfortably service the bigger loan.

You might get a higher interest rate – Refinancing the mortgage could result in a higher interest rate than you had before (especially if your financial situation has changed). This means you could pay more interest over the life of the loan. It’s wise to shop around and compare offers to get the best rate possible

The process can trigger emotional stress – Handling both a separation and a large financial negotiation simultaneously can be very stressful. Discussions about the house and money might reopen old wounds. Having a neutral third-party (like a mediator or counsellor) or a supportive advisor can make a big difference in keeping things civil and on track.

You bear all financial risks (and costs) alone – Once you buy out your partner, you’re solely responsible for the property. If expensive repairs are needed or the market declines, you’ll have to handle it without someone else sharing the burden. (Of course, you also keep all the profits if the property value rises – which is a trade-off.)

A property valuation is still required – You’ll need a formal valuation to determine how much to pay. This is a straightforward process but comes with a fee (usually a few hundred dollars) and can take some time. Sometimes the valuation may surprise both of you – for better or worse.

It can be hard to agree on what’s fair – One of you might feel you deserve a larger share than the other. Personal feelings, differing valuations, and past financial contributions can all clash when determining a buyout figure. This is why having a mediator or legal advisor involved can be very helpful to reach an agreement.

Need Help Deciding?

Buying out your ex can be a smart move — but only if the numbers stack up. At Hunter Galloway, we’ve helped many Australians in similar situations weigh the pros and cons based on their unique circumstances.

Let’s run the numbers and help you move forward with clarity. Call us on 1300 088 065 to begin your free loan assessment now.

Would you like to learn about your situation?

Jurisdiction Matters: Why Your State Affects The Buyout Process

When it comes to property settlements, where you live matters. Stamp duty rules, title transfer procedures, and other legal requirements vary from state to state. Family law might be federal, but each state and territory has its own paperwork and processes for property transfers.

State

Stamp Duty on Property Buyout

Land Title Office

Key Considerations

NSW

Usually exempt with court or consent order

NSW Land Registry Services

Must submit Form 01T and supporting court orders to avoid stamp duty. Local conveyancer highly recommended.

VIC

Exempt with Family Court orders

Land Use Victoria

Transfer must be part of a binding agreement or court order. Include valuation and evidence of relationship breakdown.

QLD

Exempt if done under a legal property settlement

Queensland Titles Registry

Form 1 and Form 24 required. Stamp duty exemption applies only with proper documentation.

SA

Exempt with valid court order

Land Services SA

Consent or financial agreement must be registered. Stamp duty relief isn’t automatic.

WA

Exempt with Family Court or consent order

Landgate

Must lodge court documents with Form T2. Settlement agents can assist.

TAS

May qualify for exemption

Land Titles Office TAS

Limited exemptions—court orders must be clear and final. Always check with a lawyer first.

ACT

Exempt with sealed orders

Access Canberra

Property transfer must clearly relate to separation. Lodgment fees still apply.

NT

Exempt if ordered by court

Land Titles Office NT

Ensure family law documents are legally binding. Exemptions assessed case by case.

Frequently Asked Questions About Buying Out A Partner After Separation

Here are the top questions we get asked when someone is looking to buy out their ex-partner’s share of a property.

Can I buy my partner out without selling the house?

Yes, you can buy out your partner without selling the house. You’ll need to refinance and pay them their share based on a property valuation. Legal agreements, such as a consent order or binding financial agreement, are strongly recommended. Make sure to have the house professionally valued so you base the payout on a fair market price.

How is the buyout amount calculated?

The buyout amount is usually based on the property’s current market value. You subtract the remaining mortgage and split the equity according to your legal arrangement. A licensed valuer can help you get an accurate figure. Keep in mind this can be adjusted by any agreements you make (or court decisions) if it’s not a straight 50/50 split.

Do I need a lawyer to buy out my partner?

Yes. A family lawyer ensures everything is legally binding and tax-smart. You’ll also need them if you want to qualify for stamp duty exemptions or avoid CGT issues.

Can I use a guarantor to help buy out my ex?

Absolutely. If you don’t qualify for the loan on your own, a family guarantor can help you meet lender requirements. This is a common option for single parents or one-income households.

Do I have to pay stamp duty when buying out my partner?

Usually not—if the transfer is part of a relationship breakdown and formalised through a consent order or binding financial agreement. Rules vary by state, so always check with your broker or lawyer.

What if my ex doesn't agree to the buyout?

You may need to apply to the Family Court for a property settlement. The court can order the transfer of property or force a sale. Try mediation first—it’s faster and less costly.

How long does the process take?

Buying out a partner typically takes 6 to 12 weeks. This includes getting a valuation, securing finance, and finalising legal paperwork. Delays often happen if there’s disagreement over the property value or settlement terms.

Can I buy out a unit instead of a house?

Yes. Whether it’s a house or a unit, the process is the same. What matters most is the property value, your borrowing power, and the legal documentation.

Will my credit score be affected?

If you take on a new mortgage, lenders will assess your credit history. If you’ve missed payments during separation, it could impact your loan approval. Talk to your broker early to avoid surprises.

Can both partners stay on the loan?

No. In a buyout, one partner refinances the loan in their name only. The other is removed from both the title and the loan, which helps cleanly separate your finances.

Can I afford to buy out my partner after separation?

Yes, but it depends on your borrowing power and current income. Lenders assess your ability to make repayments on your own, including any child support or spousal maintenance. Boost your chances by reducing other debts, increasing your deposit, or getting a guarantor. Always speak to a mortgage broker early—they’ll show you your realistic options before applying.

What If I'm not on the property title—can I still buy them out?

Yes, you can—being off the title doesn’t always mean you lose your share. If you contributed financially or lived in the home, the Family Law Act may still entitle you to part of the property. You’ll need a lawyer to help you formalise the arrangement through a binding financial agreement or court order. Once that’s done, the bank can refinance the loan in your name.

Key Takeaways And Next Steps

Splitting up and buying out a shared home involves weighing your options carefully — considering financial trade-offs, legal requirements, emotional factors, and future plans.

Main Things to Remember:

Evaluate all alternatives – whether buying out, selling, or continuing to co-own temporarily – and choose thoughtfully.

Prepare thoroughly – get professional advice, understand the legal process, and organise your finances accordingly.

Negotiate fairly (and legally) – consider using mediators and involving lawyers to formalise agreements.

Calculate the buyout amount carefully, taking into account all the factors that could influence the property’s value (and each person’s share).

Address the emotional aspects, tax implications, and future planning concerns as part of the overall decision – don’t overlook any of these areas.

Get Professional Support

Because the process of buying out your ex is complex, seeking advice from professionals (financial advisors, family lawyers, tax experts, and real estate agents) is highly recommended. These experts can provide guidance tailored to your specific situation, helping you make the best decisions.

How Can We Help You?

With the right information and balanced approach, the property buyout process after separation can have fair and positive outcomes for everyone.

At Hunter Galloway, we offer a free assessment to understand your specific needs and provide expert home loan recommendations. Going through this process alone can be hard, so let our experienced team guide you every step of the way.

Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you’re ready to get started, give us a call on 1300 088 065 or book a free assessment online to see how we can help make your property buyout (and refinance) a success.

Our team of home loan experts is here to help you buy a home in Australia

Example figures are shown. Replace them with your own details.

A home buyout is when one owner keeps the property and pays the other owner for their share. Enter three figures to get a rough estimate of the payout, new home loan and repayment.

This is a guide only, not a quote or loan approval. A lender must approve the loan, and your solicitor should confirm the ownership split.

1. Enter your details

$

Use your best recent estimate. Your lender may use a different valuation.

$

Use the total balance across all home loans secured by the property. Check your banking app or latest statement.

%

Your ex receives: 50% · You keep: 50%

The calculator starts at 50%. Change this if your agreed split is different. Equity means the home's value minus the home loan. This calculator applies the percentage you enter — it does not decide what a fair or legal split should be.

Your solicitor should confirm the final ownership split and transfer arrangements.

These are example figures. Replace them with your own figures when known. Example rate and costs last updated 17 July 2026.

2. See your estimated buyout

Estimated amount to pay your ex

$100,000

This is 50% of the home's estimated $200,000 equity.

How this was worked out

Estimated property value$500,000

Less current home loan$300,000

Estimated equity$200,000

Your share before the buyout (50%)$100,000

Your ex's share before the buyout (50%)$100,000

Transfer duty (sometimes called stamp duty) may be exempt in some situations. Confirm this with your solicitor.

3. Estimated home loan after the buyout

Current home loan$300,000

Amount paid to your ex$100,000

Estimated new home loan$400,000

Estimated cash needed from savings: $6,650

This assumes the estimated $6,650 costs are paid from savings and are not added to the loan. The payout itself is usually funded by the new loan. The current loan would usually need to be replaced with a new loan in the remaining owner's name.

Estimated repayment

About $2,463 per month

Based on an example interest rate of 6.25% and a 30-year loan term. A lender will check whether the people remaining on the loan can afford it after living costs and other debts.

Loan compared with property value80.0%

Your estimated home loan is 80.0% of the estimated property value. 80% of the estimated property value: $400,000. This is also called the loan-to-value ratio, or LVR.

You are right on the common 80% limit. If the lender values the property lower, or costs are added to the loan, Lenders Mortgage Insurance may apply.

What is LMI?

Lenders Mortgage Insurance is an insurance cost that protects the lender, not the borrower. It may apply when the loan is above the lender's limit.

4. Compare your options

🏠 Buy them out — keep the home

Estimated payout to your ex$100,000

Estimated new home loan$400,000

Estimated repaymentAbout $2,463 per month

Estimated costs from savings$6,650

What happens later: You own the property. You receive all future gains and carry all future losses and property costs.

🔑Sell & split

Estimated sale price$500,000

Home loan repaid from the sale$300,000

Estimated total selling costs$12,500

Estimated cost from your share$6,250

Estimated amount you receive$93,750

What happens later: You no longer share the property or home loan.

🤝 Keep co-owning

Payout now$0

Current home loan remains$300,000

Current repaymentContinues as normal

Important: You may agree to split repayments, but both borrowers generally remain responsible for the home loan.

What happens later: Future gains, losses and property costs remain shared.

What this could mean

Buy them out: Your home loan and repayment increase, but you keep the property. Comparing upfront costs only, the estimated buyout costs are about $400 higher than your share of the selling costs. The paths are otherwise very different: buying out funds the payout through a larger loan you carry alone, while selling puts your share of the proceeds in your hand.

Sell & split: The loan and selling costs are paid, then the remaining money is split.

Keep co-owning: No payout is needed now, but you both remain connected to the property and home loan.

The main question is whether a lender may approve the estimated $400,000 home loan based on your income, expenses and other debts.

Could the new loan be approved?

Check whether a $400,000 home loan may be possible based on your income, expenses and debts.

Free, no-obligation assessment. 1300 088 065

What is not included?

This calculator only looks at the property and home loan. It may not include fixed-rate break costs, moving costs, tax, repairs, offset account balances, other assets, other debts or adjustments made as part of a legal property settlement.

General information only. This calculator uses the figures and assumptions entered. It does not provide legal, tax or credit advice, and it is not a quote or loan approval. A lender will assess the applicants' income, living costs, debts, credit history and the property value. Ask your solicitor to confirm the ownership split, transfer terms and any transfer duty. Hunter Galloway Finance Pty Ltd — Credit Representative 476903 authorised under Australian Credit Licence 389328.