Do you want to buy a house but are worried about your HECS/HELP debt? Then this article is for you. In this article, we uncover what HECS/HELP debt does to your borrowing capacity and how it will affect your home loan application.

We will show you the following:

- How much your HELP debt is affecting your home loan

- How to calculate exactly how much it is reducing your borrowing power by

- How to check what you owe on your HELP debt

- Lots of case studies and real-life examples

Let’s get started.

How Does A HECS/HELP Debt Work?

In Australia, citizens can borrow money from the Australian Government to pay their course fees. This loan is called HECS-HELP.

- Higher Education Contribution Scheme (HECS)

- Higher Education Loan Program (HELP)

During your studies, the Government pays the loan amount to your educational institution. Then, when you have finished studying and are earning an income, you begin your loan repayments. These repayments are made directly to the Australian taxation system and are often shown on your payslip.

The fine print?

- Repayments are made by those earning over $$54,435 per annum.

- People living overseas are not required to commence repayments until returning to Australia.

- You can make voluntary repayments at any time.

If you took out a HECS-HELP loan many years ago and still have money owing, it’s time to consider how this will affect your borrowing capacity.

Does HECS Debt Affect Your Home Loan?

Why will HECS affect my home loan application?

At the start of any loan application, you must disclose any outstanding debts – Including your HECS-HELP loan. Depending on what you’re earning financially, you may already be repaying the debt or have deferred it.

Wait, how do I defer it?

As we explained above, if you earn less than $$54,435 per annum or live overseas, the debt is put on hold until you fulfil the repayment criteria.

How can a HECS debt affect my borrowing power?

When you apply for a loan, your lender will consider this debt like other personal liabilities. Then, your financial situation will be determined based on this debt.

(But wait, not all debt is created equally. We’ll get to that later in this post.)

In short, HECS/HELP debt reduces your assessable income significantly, in some cases.

Your income will be reduced by the percentage (per annum) of repayments that you’re making.

So if you’re earning $60,000 and making repayments at 1% of your income, your debt would lower your borrowing power by 1%.

But the good news is different lenders have different criteria.

Be transparent with your mortgage broker about your HECS debt from the beginning. This will help your broker choose the right lender for you.

Case Study: Sarah’s HECS Loan And How It Affected Her Home Loan

Sarah recently got in touch with our Mortgage Brokers to arrange a loan for her first home.

- Sarah is earning $91,500 before tax

- She has a credit card with a limit of $20,000

- The HELP repayments on her payslip were 5% of her income, or $381 per month.

Based on Sarah’s situation, her maximum borrowing capacity was $400,000.

The kicker was she only owed $1,450 on her HELP debt.

So, by repaying her HELP debt, her borrowing capacity increased from $400,000 to $480,000!

If she closed her $20k credit card, her borrowing capacity would jump all the way up to $600,000!!!

Would you like to know our borrowing power? Chat with our mortgage brokers, or call us on 1300 088 065.

Why Can Credit Cards Have A Significant Impact On Your Home Loan?

While we’re on the topic of debt, let’s look at other forms of debt that can impact your loan.

Credit cards can significantly impact your loan, especially if you have a large credit limit available.

For example, Talulah has a $30,000 credit limit on her credit card. When she moved house, she spent $800 for a new couch on the credit card, and she is still slowly paying off. Yet when Talulah applies for a loan, the $800 is looked at, along with the total $30,000, which is removed from her borrowing capacity.

Why did a credit card make this big a difference?

Because at any moment, Talulah could potentially spend the other $29,200 available. This type of debt is considered BAD debt.

Talulah needs to lower her credit limit on the card to $1,000 so that the other $29,000 is not considered by the lender.

Each form of debt that you have will also be looked at and lower your borrowing capacity.

Other types of debt include:

- Car loan

- Credit card loans

- Personal loans (i.e. holiday loans)

- Afterpay and GoMoney Cards

So, try to reduce your overall debt in general before applying for a home loan.

Something else that catches people out is interest-free cards from Harvey Norman and Afterpay. Just like a credit card, while you may not be using this money and have nothing owing to your name, the lender will consider it potential money you could borrow. So, it’s best to close any of these accounts that are not in use.

If you’re getting a little excessive with Uber Eats or dining out a few nights a week, that’s also something to slow down on. Lenders will go through your bank statement with a fine-tooth comb, so start saving (or spending) money more responsibly to prepare.

How To Check HECS Debt?

Now that you have identified the effect of HECS debt on your borrowing capacity, it’s time to figure out the next step.

Do you know how much you’ve left to pay on your loan? And how can you minimise this? Let’s get right into it.

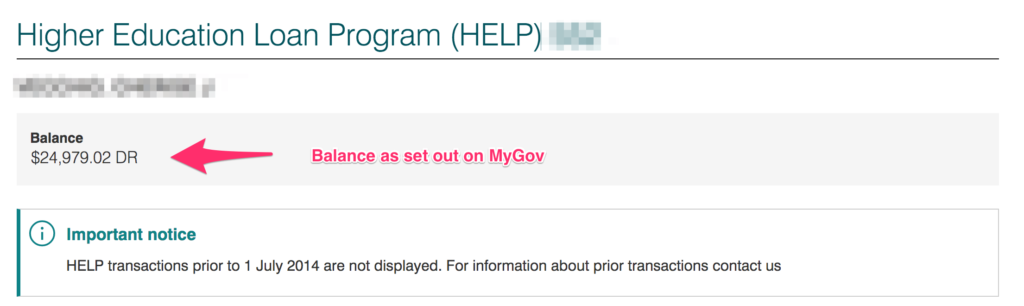

Checking HECS debt is easy. Jump on to your myGov account, and you’ll immediately see how much you’ve left to pay. If you don’t have an account, you can set up one through the ATO website.

How much are my HECS Repayments?

HECS repayments are determined by how much you’re earning. The lender will look at this percentage and take it off your entire loan.

So, let’s take a look at an example.

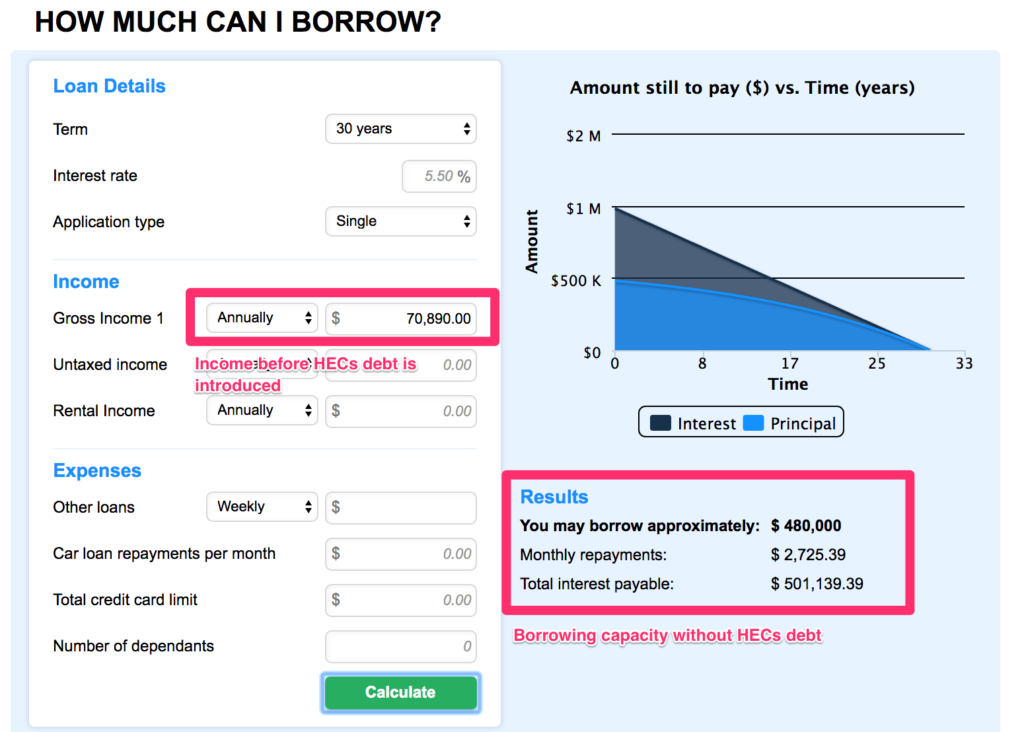

Case Study 2 – Layla’s HELP Debt

Layla earns $70,890 per financial year, and her HECS repayment rate is 4.0%.

If she pays down her HECS loan and applies for a home loan debt-free, her borrowing capacity will be at $480,000.

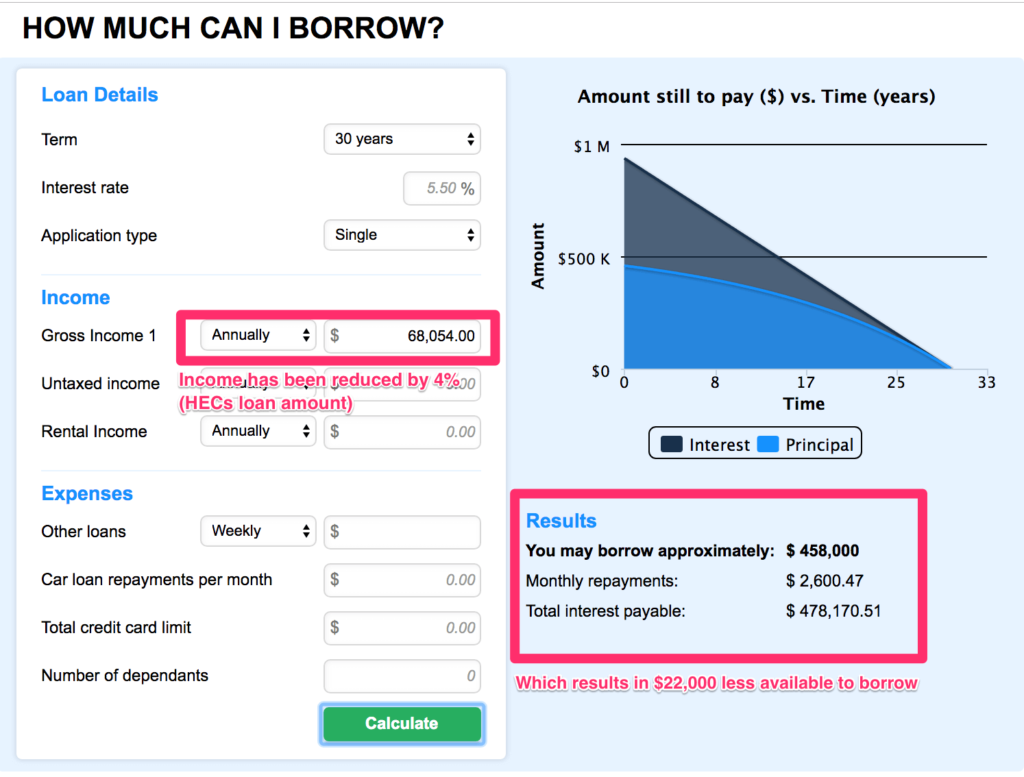

However, with her current HECs debt, Layla applies for a home loan and her borrowing capacity drops by $22,000.

The 4% per annum has been taken off her overall income, changing it to $68,054.

As a result, Layla can borrow $458,000 with her current HECS/HELP debt.

Read More: How Much Home Can I Afford [Calculator]

The Difference Between interest and indexation

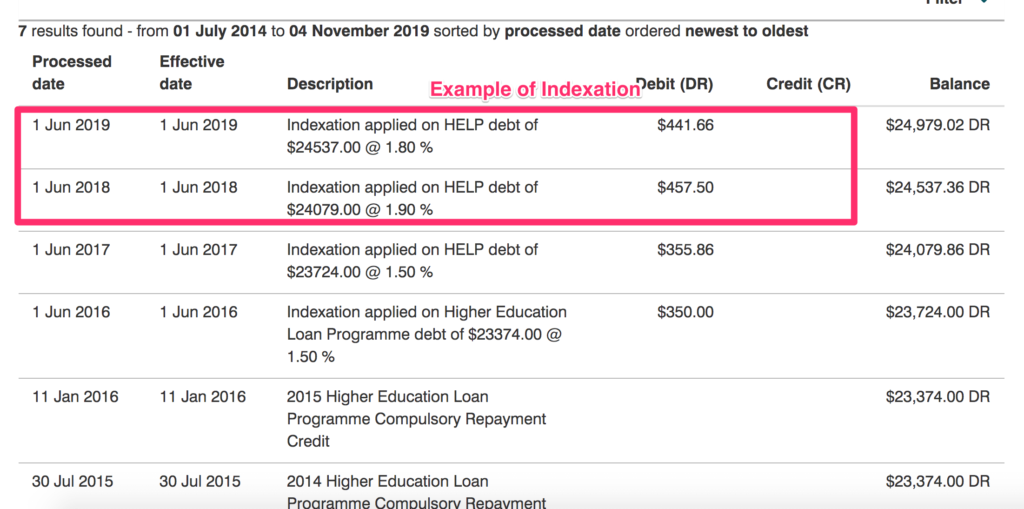

You’ve just checked your HECS account and noticed that it’s gone up and not down, and you are wondering why…

This is because of indexation.

A HECS/HELP debt is raised in line with the cost of living each year. So, whatever the indexation rate is, your loan will increase with it. Yet, there’s no interest on the loan.

So, when it comes to comparing HECS debt with credit card debt, a student loan is a much better type of debt to have.

Interest-free means that even if you take years to pay off the loan, the indexation is minimal in comparison to the other debts.

How Do I Get My HECS Debt Written Off When Applying For A Home Loan?

Your next step is to decide whether you will go ahead with your application with or without the debt.

And make no mistake: every little bit counts when it comes to getting finance.

In this section, we’ll cover what to do if you still have a significant HECS debt.

HELP! I still have a significant HECS/HELP debt!

If you went travelling for a few years and, in turn, got behind on the HECS repayments, You’re probably wondering what to do with your HECS debt.

Don’t forget that this advice is not specific to your personal circumstances. Contact our team for a chat about your particular situation.

But speaking in general terms, a HECS debt is the best (well, cheapest) kind of debt you could have. While it does affect your overall borrowing capacity, the amount you pay each year towards the loan is small. So, deciding whether to pay it down or not really depends on where your income is at.

But we’ll get to this in further detail in a moment.

Should I Make Voluntary Repayments?

This depends on where you sit with your financial situation.

- If you ONLY have HECS debt

- have no other forms of debt,

- you need to increase your borrowing capacity,

- AND you have some spare cash…

Well, why not? You can make voluntary repayments.

But if you have other sources of debt that are considered bad debt, like personal loans, car loans and credit cards, which have much higger interest rates, then this is where you should start because this form of debt is considered bad debt.

After that, student debt follows.

And then money into property and shares, which are considered good debt, can come into play.

In summary, student debt isn’t “make or break” when it comes to applying for a home loan. The good thing is that most people have HECs/HELP debt. So, it’s a pretty common aspect of applicants applying for a home loan.

Should I pay off my HECS/HELP debt before I apply for a home loan?

As we said above, HECS debt is one of the better (cheaper) debts you’ll ever have. To answer the question of whether or not you should pay it off…

If the amount of money you owe on the loan is small enough to pay off, then it is worth it.

As we covered in Sarah’s scenario above, paying out the $1,450 HELP debt increased her borrowing capacity by $60,000!

What happens if I still have a high HELP balance?

f you’re still sitting within a reasonable amount left on your HECS debt—say, over $10,000, and it would be taking a significant amount off your savings to pay it off, then wait…

In this case, it’s not worth paying it off because it will leave you with less for other expenses.

The more critical debts to get rid of are car loans, personal loans and credit cards.

The ultimate goal should be to save for a deposit. HECS has no interest and takes off a small amount of your income. So, paying it down gradually works just as well.

How Can I Increase My Chance Of Loan Approval?

Now that you’ve got your estimated borrowing capacity and know what to do with your HECS loan, it’s time to increase your chances of approval.

In this section, we’ll show you the right (and wrong) ways to increase your chances of home loan approval.

How can I Improve My Chance Of Qualifying For A Home Loan With HECS Debt?

Yes, HECS debt adds a little extra hurdle to your loan application. But the good news is, there are a few ways to improve your chances of qualifying.

Reduce existing debt

Sorry to sound like a broken record, but reducing existing debt is a great way to increase your chances of home loan approval. Consolidate your debt where you can. However, pay attention to different interest rates that come with different terms. Adding the debt to your new mortgage is not always a good idea.

Why? Because it’s a 30-year time frame that will significantly add to your overall interest paid.

Check your credit

Good credit. Bad credit. Some credit. No credit. If you’re unsure where your credit stands, get in touch with our team to review.

Some people do a credit check and find out they’ve got bad credit without realising it. It could be anything, like a missed payment from over five years ago while you were overseas.

So before you apply for a loan, always do a credit check. This will help your mortgage broker determine the best lender for you, depending on your credit record. You will then be able to take steps to improve your credit status once you know where you stand.

Save, save, save away.

You might be sick of hearing the s-word, but it is the truth… Before you’re ready to apply for a home loan, make sure that you have been steadily Saving for at least three months.

Regular deposits into a savings account will show the lender that you are disciplined.

Speak to us ( mortgage brokers)

We are here to help you.

You can ensure that you qualify for a loan by speaking to a broker before proceeding with your application.

Your broker will check that you have all the paperwork and strategies in check. And they will also negotiate for the best rates on your behalf. #winning

If you would like to chat, contact our mortgage brokers or call us on 1300 088 065.

Be honest and always be conservative with income and asset estimation.

As we said about telling your broker about the HECS debt, try to establish a transparent and honest approach with them regarding your income and assets. After all, your income is shown on your payslip.

What about your yearly earnings? Many first-home buyers include their superannuation in their yearly income. But since this money doesn’t go into your pocket, it should be left out.

Making a sound estimate will help you stay in a stronger financial position later on…

We see all kinds of situations every day, deal with financial stress, and encounter unique situations all the time. So there is no need to be embarrassed about your financial situation. We’ve probably heard it before, anyway!

Make sure to include all expenses.

Any extra expenses, like childcare or phone bills that you haven’t factored in are essential. So, sit down and make a comprehensive list of all your monthly expenses. The lender will use this to determine how much you can afford to make in repayments.

Overapplying won’t help.

Every time you apply for a home loan, the lender will review your credit file. This review process is added to your credit file.

The next lender will be able to see a history of each time you have applied for a loan. And since no outcome is stated on your credit file, they will assume your previous application was unsuccessful. This history can be seen as a red flag by lenders.

In summary, only apply for a loan when you’re 100% ready and have all your ducks in a row.

Next Steps And Getting Your Home Loan

Our team at Hunter Galloway is here to help you buy a home in Brisbane. Unlike other mortgage brokers, who are one-person operations, we have an entire team of experts dedicated to making your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again