Superannuation isn’t just for retirement. Under the right rules, you can use super to buy a house and reach your property goals sooner. Whether you’re working with a mortgage broker Brisbane trusts, using the First Home Super Saver Scheme, buying property through a Self-Managed Super Fund, or accessing super after preservation age, each pathway has unique rules, timelines, and benefits. In this guide, we break down the steps, share real-life examples, and show how to combine super strategies with other government schemes to get the best outcome

Quick Summary

- As of 2025, the First Home Super Saver (FHSS) scheme allows first-home buyers to save up to $50,000 in eligible voluntary super contributions for a house deposit. Couples can access up to $100,000 combined. [Source: ATO]

- Concessional contributions are taxed at 15% when made, and when you withdraw under FHSS, the released amount is taxed at your marginal tax rate, with a 30% offset.

- The scheme can potentially save 30% or more compared to standard savings accounts.

- Pros include tax savings and higher interest rates; cons include limited contribution amounts and potential delays in fund release.

- Alternative options for home buyers include getting a guarantor, saving a larger deposit, or buying with a partner/family member.

- Self-Managed Super Funds (SMSF) can be used to buy investment properties but with strict rules and potential risks.

- Using personal loans as a deposit is strongly discouraged due to reduced borrowing power and potential loan rejection.

Can I Use Super To Buy A House?

In this section, we’ll help you figure out if you’re eligible to buy a house with superannuation. So, if you’re not sure if buying a house with super will work for you, this section will get you on the right track. Then, later on, we’ll show you a bunch of advanced strategies and techniques.

What are the features of the FHSS?

Let’s get one thing straight: you can’t technically use your superannuation to buy a house. But, first home buyers are eligible to make voluntary contributions towards their super and use it as a deposit. This strategy is called the First Home Super Saver (FHSS) scheme.

- This scheme allows first home buyers to save up to $50,000 of voluntary contributions overall.

- You can save a maximum of $15,000 per year.

- Another great feature is that couples could save up to $100,000 combined.

- You don’t have to be an Australian resident or citizen for tax purposes to be able to use the scheme!

The scheme can also be used in conjunction with the First Home Owners Grant too.

The main benefit of this scheme is that when you take the money out, it will be taxed at a discounted fixed rate of 15%.

Am I Eligible To Make Voluntary Contributions Towards My Super Deposit?

In order to use the scheme, you should meet ALL of the following requirements:

- You must be 18 years or older.

- You must be a first home buyer. This means you must not have owned property in Australia before including vacant land or commercial property. Your name must be on the title of the property you want to buy.

- You must intend to occupy the property for at least 6 months within the first 12 months of it being practicable to move in, and be a member of an Australian super fund

- You don’t have a completed release request in relation to a FHSS determination made in relation to you.

If you have owned a property before, you may still qualify for the scheme, provided you prove that you suffered a FHSS financial hardship.

Using Super For A House Deposit: Does The FHSSS Earn You More Money?

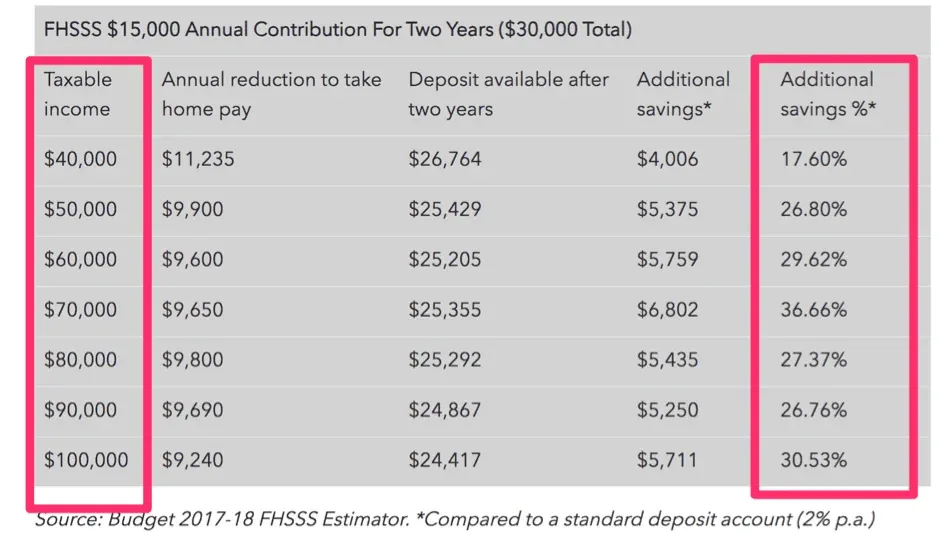

The Government’s FHSSS has estimated that you can save up to 30% or more using the scheme.

For example, someone earning $65,000 per annum and sacrificing $15,000 per year can save up to $25,280 towards a deposit. This is $5,834 (or 30%) more than if you were using a standard savings account.

Differences In Using Super For Low and High Income Earners?

It depends on the timeframe. The difference becomes greater in savings over two years for high-income earners. In the table below, you can see the difference between incomes.

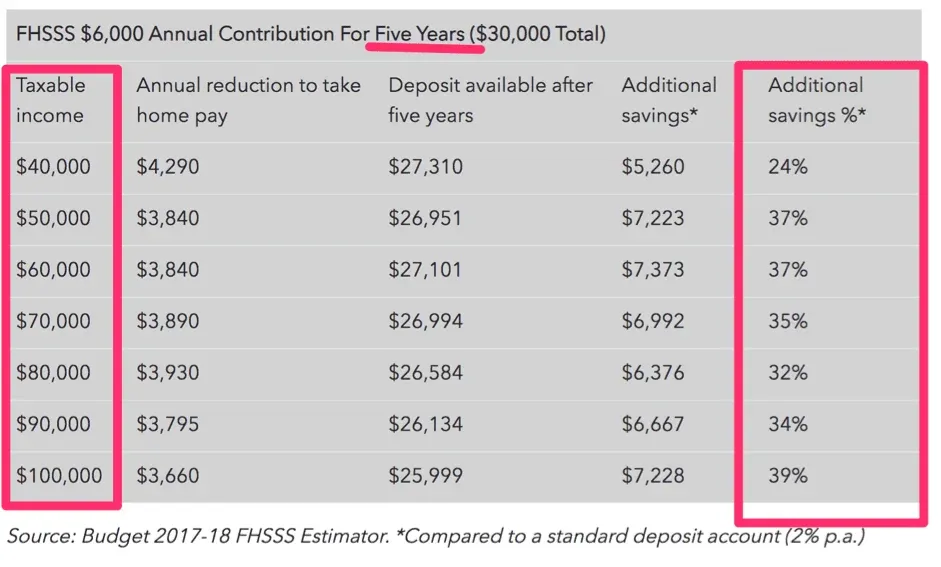

However, smaller long-term contributions for low-income earners have proven to generate better savings and a higher additional savings amount.

How To Request Funds From Super?

First, you’ll need to figure out how much money you have contributed to the fund. When you review your super balance, you can check the total to keep track of the maximum amount you can release ($50k). Once you’re ready to release the funds, you will need to apply for a FHSS determination and release form.

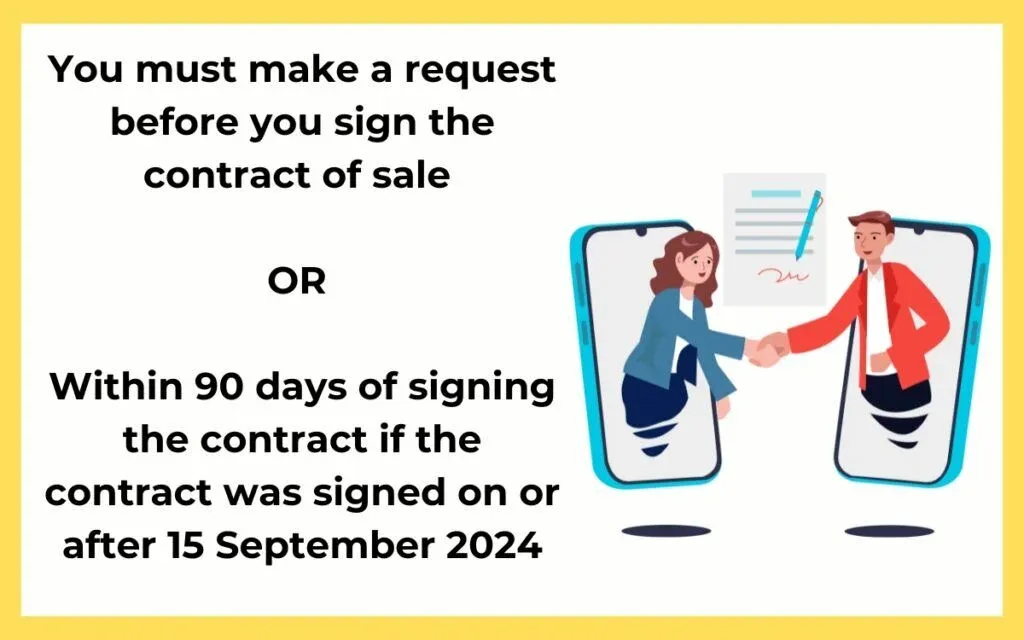

You must request an FHSS release before signing a contract, or if you’ve already signed, within 90 days (for contracts signed on or after 15 September 2024). Previously, the window was just 14 days. If you miss these time frames you will be subject to the 20% FHSS Tax.

Ensure all your details are correct, as you can only have one active request even if you have requested an amount below what you have in your super.

Wait, what’s an FHSS Determination?

The First Home Super Saver Scheme determination form is what you will need to lodge first. You must apply for and receive an FHSS determination before applying for the funds to be released. After you have an FHSS determination signed, with the signed contract, you cannot request another one. From there, you need to request that your funds be released.

Step-by-Step Timeline For Accessing Your Super To Buy A Home

Here is a simplified step-by-step timeline of using super to buy a House

Before Week 1: Build your super contributions

The FHSS only works if you’ve already made eligible voluntary contributions over time — often 12–24 months or more to build a meaningful amount. If you haven’t started yet, your first step is to plan and contribute regularly before you even begin the withdrawal process. For SMSF buyers, ensure your fund is set up and compliant before considering a purchase.

Week 1–2: Request your FHSS determination or start SMSF loan process

If you’ve already contributed, ask the ATO for your FHSS determination to see your maximum withdrawal amount. SMSF buyers should begin the loan pre-approval process and check that the property meets fund rules.

Week 3–4: Prepare documents and update strategies

FHSS applicants confirm contribution records and line up a property search. SMSF trustees update their investment strategy and seek member/trustee approval for the purchase.

Week 5–7: Secure approvals and prepare funds

The ATO’s FHSS release approval can take several weeks. SMSF loan offers also require extra documentation. Work with your lender or broker to ensure your deposit is ready when approvals arrive.

Week 8+: Align with settlement deadlines

Once FHSS funds are released or your SMSF loan is approved, move quickly to exchange contracts and meet settlement. Any delay can put your purchase at risk.

Tip: Build in a buffer. Processing times can change, especially during peak ATO or lender periods.

Check to see if you are eligible for a home loan

Real-Life Savings Scenarios

Seeing the numbers can make your options clearer. Here are three real-world examples showing how using super to buy a house can work.

Case 1 – FHSS First-Home Buyer

Sarah earns $80,000 a year and contributes $12,000 over two years into her super. These contributions are taxed at 15%, saving her around $1,800 compared to saving after tax. With earnings included, she boosts her deposit by $24,000.

Case 2 – SMSF Investor

David has $200,000 in his SMSF. He uses it to buy a $500,000 investment property through a Limited Recourse Borrowing Arrangement (LRBA). The property is rented until he reaches retirement age, generating rental income that goes back into the fund.

Case 3 – Preservation Age Purchaser

Linda is 60 and has $300,000 in super. She takes a lump sum to buy a smaller home mortgage-free. She reduces her living costs and secures financial stability in retirement.

These examples show the diverse ways super can help you enter the property market or improve your housing situation.

Pros And Cons Of The Scheme

Not every Government scheme is perfect. So, let’s look at the pros and cons of the First Home Super Saver Scheme to give you a clear idea of whether it is for you.

The pros of the First Home Super Saver Scheme

- Save money on tax repayments.

- You can use the scheme as a couple, combining your funds.

- Your contributions are deemed to have earned the Shortfall Interest Charge (SIC) rate, currently 7.38% p.a. (March 2025). This is not the actual investment return of your super fund, but an ATO-set calculation used when releasing funds.

- The amount you can withdraw doesn’t vary with falling markets.

- You will be given a 12-month buffer to purchase a home with the funds after you withdraw the money.

The downsides of the scheme

- It is subject to change in line with government changes.

- You will have less take-home pay as the money will be salary-sacrificed.

- The ATO states most FHSS release requests are now processed within 20 business days (90% of cases). Allow extra time during peak periods.

- If you sign a contract BEFORE releasing the funds, you will need to pay a 20% FHSS tax.

- $50,000 is the maximum a single person can contribute to the fund, which might not be enough for a deposit (if you don’t want to pay LMI).

- Returns are limited to the Shortfall Interest Charge (SIC) rate of 7.38% p.a., which is low compared to other super funds.

Combining Super Strategies with Other Government Schemes

You don’t have to choose one path. You can combine super strategies with other government support to get into a home sooner.

FHSS + First Home Guarantee

The FHSS helps you grow your deposit faster, while the First Home Guarantee lets you buy with as little as 5% deposit without paying Lenders Mortgage Insurance (LMI). Combining both can significantly reduce your upfront costs.

SMSF + Negative Gearing

If you buy an investment property through your SMSF, you may be able to use negative gearing benefits. This could help offset loan interest against rental income, improving your fund’s cash flow.

Preservation Age + Downsizer Contribution

If you’re 55 or older and selling your home, you can use the Downsizer Contribution to boost your super. This works well if you’re also accessing super to buy a smaller property.

When you combine schemes, check all eligibility criteria first. Rules can be complex, and the benefits depend on your personal situation.

If I Can't Use Super As My Deposit, What Other Options Have I Got?

If you are not eligible for the FHSS, don’t despair. Fortunately, there are other options for you to get into the property market. In this section, we will lay out a few different ways you can buy a house sooner rather than later.

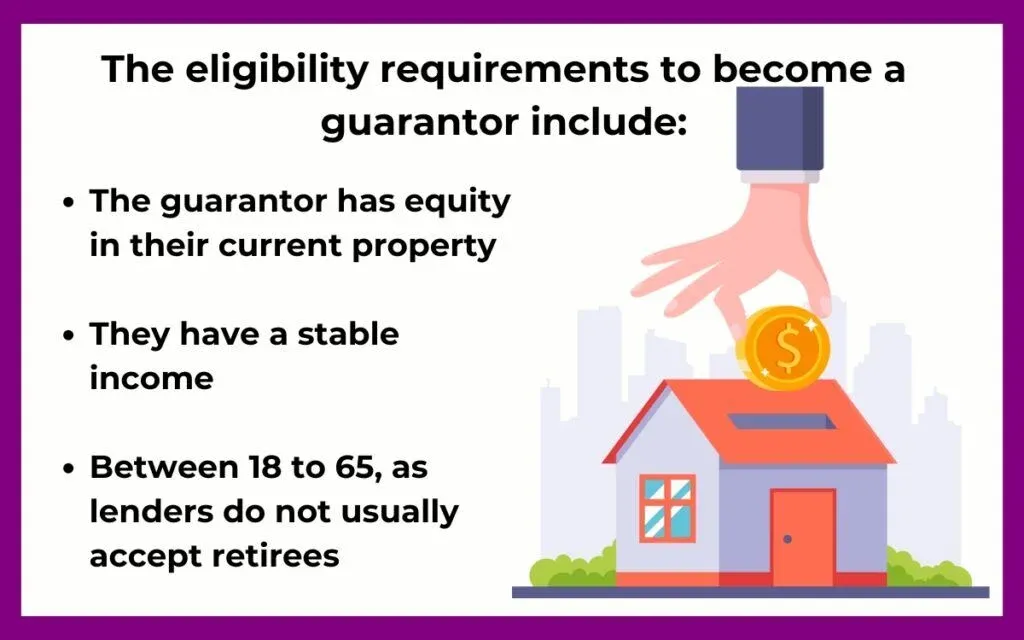

1. Get a Guarantor

If you don’t have a deposit, a great way to move ahead with buying a property is through a guarantor. Your parents, a close friend, or a family member can guarantor your property.

The eligibility requirements to become a guarantor are:

- The guarantor has equity in their current property

- They have a stable income

- Good credit

- Australian citizen

- Between 18 to 65, as lenders do not usually accept retirees

When a guarantor takes on a property with the buyer, they are legally required to pay back the loan if the buyer cannot fulfil repayments. They will need to pay any extra fees or charges, too. The good news is the guarantor can take on just some or part of the loan. So, if this happens, only a portion of the loan will fall back onto them.

If you are in a stable financial position and ready to enter the property market, having a guarantor can be a great way to fast-track this process.

Read more: Guarantor home loans

2. Save a more significant deposit

Sometimes, all you need to do is continue saving and wait a little longer. The more you save, the easier it will be to pay your mortgage and still afford to live comfortably.

A great way to maximise your savings is by starting with your expenses. Do an audit of unnecessary spending. Are you spending money on Uber Eats or AfterPay each week? Time to cut those expenses and replace that money by putting it into savings.

These small changes will help you speed up your savings process.

Read more: How to set a budget for buying a home

3. Buy with a partner or family member

A lot of thought needs to go into this one if you’re planning to buy a property with a partner or family member.

First, ensure you’re on the same page and have clear guidelines for each buyer.

Figure out a contract with ownership over the property, and have an exit strategy should either of you want to sell their half of the property.

You may feel like these steps are unnecessary, but should financial circumstances change, it’s essential to have all of your ducks in a row.

Buying with your partner or family member can be a great way to combine your savings and make the process much more affordable.

Self-Managed Super Funds – How Do They Work?

Now that you’ve thought about other options for saving, aside from the FHSS, it’s time to take a look at Self-Managed Super Funds (SMSF).

In this section, we’ll show you how to work with an SMSF and make the most of it.

This section is specifically for property investors.

Self-Managed Super Fund property rules

So, what is a self-managed super fund? It is a private super fund that allows you to manage your retirement savings. SMSF owners have full control over investment decisions and strategies as opposed to a regular super.

You can use a self-managed super fund to buy an investment property. The catch is…. You are not allowed to live in it!

You can buy the property through your SMSF, and the fund can have one to four members.

The members will need to make a decision together about how the super is invested.

What are the SMSF rules?

To buy a property through an SMSF, you must comply with a few rules.

The property must:

- Fulfil the sole purpose test of providing retirement benefits to fund members

- Not be acquired from relatives

- Not be lived in by any members of the fund or related parties of the fund

- Not be rented by a fund member or associated parties of the fund

There is a loophole that allows you to use the super to buy business premises, which you can then use. However, you will have to pay rent to your SMSF at the market rate.

What will it cost to use super for a house deposit?

Buying an investment property through a self-managed super fund will still have the same fees and even some extra charges that could eat into your super balance.

Check with your mortgage broker and lender before going ahead.

Some of the fees incurred include:

- Legal fees

- Stamp duty

- Advice and upfront fees

- Ongoing property management fees

- Bank fees

Key things to remember about SMSF borrowing

This is where things can get a little tricky.

Borrowing or “gearing” your super needs to be implemented in a controlled and strict way.

The conditions to follow are around a ‘limited recourse borrowing arrangement’.

This type of arrangement can only be used when buying a single asset – i.e. residential or commercial property.

If you are ready to commit to a geared investment, consider whether or not the investment is in line with your broader investment strategy.

What are the risks of a geared SMSF property?

- Cash flow – putting money from your SMSF into your loan is required, and you will need to have enough cash flow to maintain this

- Extra costs – SMSF property loans are often more costly and have additional fees compared to standard loans.

- Potential tax loss – The losses on the property cannot be offset against your income outside of the fund.

- No turning back – If you haven’t set up your loan correctly, like documentation and the contract, then turning the arrangement around can be very difficult. Sometimes, it’s not even possible. In this case, you would potentially have to sell the property, which would most likely result in a loss.

- No changes to the property – While the SMSF property loan is being paid off, you cannot make any changes to the property.

Would you like to learn about your situation?

Bonus: Using A Personal Loan As A Deposit

As tempting as it can be to get a personal loan and use it as a deposit – don’t do it.

Why?

- Banks nowadays are more diligent about their research, and if they find out you got your deposit from another loan, they will most certainly deny your home loan application.

- Personal loans can significantly reduce your borrowing power. By ‘significant’, we mean hundreds of thousands of dollars.

These days, there are a lot of self-proclaimed social media financial advisors encouraging you to get personal loans and use them as a deposit. As tempting as it may sound, run far, far away from personal loans. Instead, talk to a home loan expert who will help you get the home loan that is right for you.

So, no matter how persuasive the video telling you to get a personal loan is, just don’t do it.

Frequently Asked Questions

How to use my super to buy a house

You can use your super to buy a house mainly through the First Home Super Saver Scheme, by releasing voluntary contributions to boost your deposit. Another option is buying property via a Self-Managed Super Fund, which has strict rules and is for retirement purposes only. After reaching preservation age, you can also access your super as a lump sum to help with your purchase.

What happens if I change my mind after my FHSS release?

Once the ATO releases your FHSS funds, you have 12 months to sign a contract to buy or build a home. If you don’t, you must either re-contribute the money to your super or pay extra tax.

Can I use FHSS money to buy land only?

Yes, you can use FHSS funds to buy vacant land, but only if you also enter into a contract to build a home and meet the occupancy rules. Simply buying land without building does not qualify

Will using super to buy a home affect my loan approval?

Using super can boost your deposit, which helps. But lenders still assess your income, credit score, and the timing of your super release before approving your loan.

Can you use your super to buy an investment property?

Yes, but only through a Self-Managed Super Fund (SMSF). There are strict rules, including that the property must be for retirement purposes and not personal use before retirement.

Is Using Super To Buy A House Right For You?

If you are looking at using super to buy your house in Brisbane or across Australia, our team at Hunter Galloway can help.

Our service does not cost you anything, as we are paid by the lender when your home loan settles.

To chat about your deposit, lending and investment lending options, book in a time to sit down with us, or feel free to call on 1300 088 065.

Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

The information on this page is general in nature and should not be considered as advice. Before you act on this information, you must seek independent legal and financial advice.