Teaming up with parents to buy a home can provide several advantages if you’re looking to enter the property market sooner. Here are some key aspects to consider when buying a home jointly with your parents:

One of the primary benefits of buying a home jointly with parents is the ability to overcome the financial barriers that often hinder first home buyers.

By pooling resources, you can much more easily save up for a deposit, making it easier to secure a home loan and enter the property market.

This can significantly speed up the homeownership journey and allows you to build equity and wealth at an earlier stage of your life than would otherwise be possible.

When buying a home jointly with parents, it’s essential to carefully consider the ownership structure that best suits your situation.

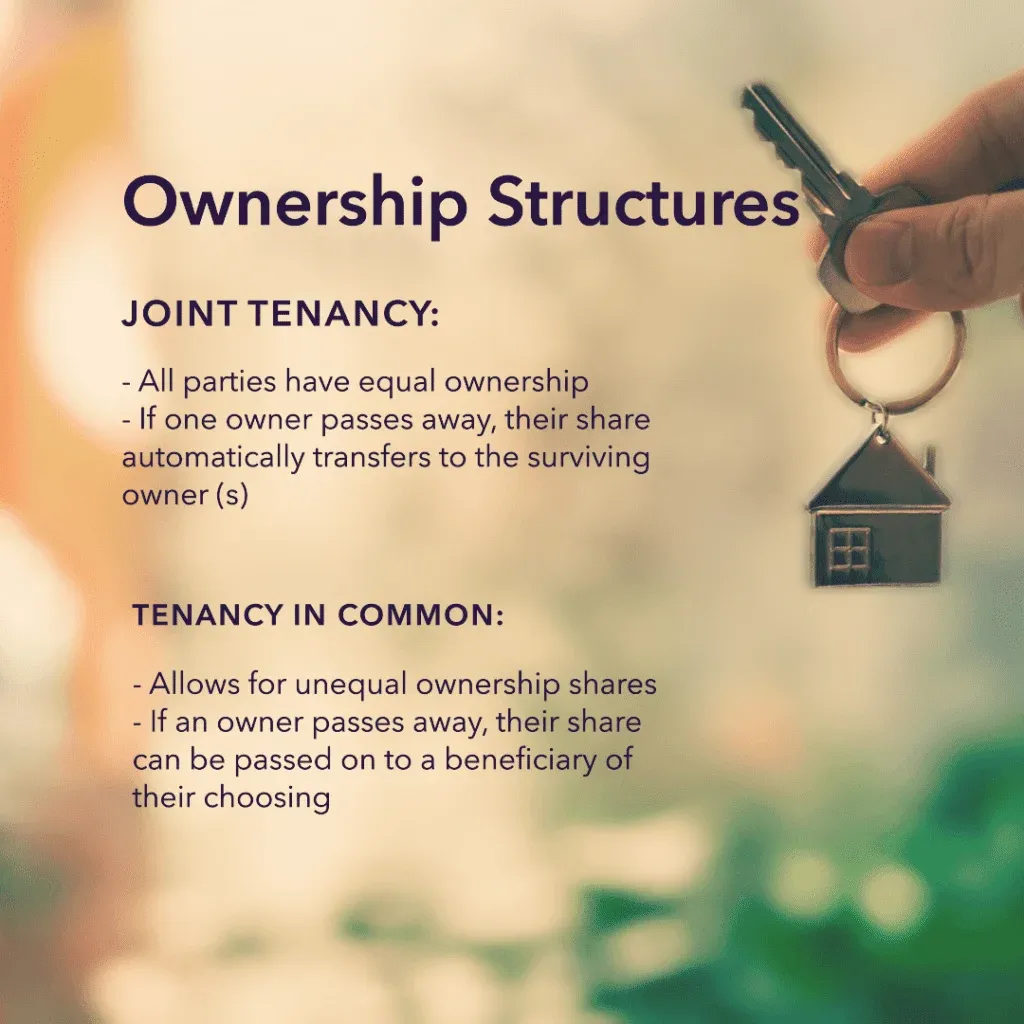

The two common ownership structures are joint tenancy and tenancy in common. Each has its own implications and considerations:

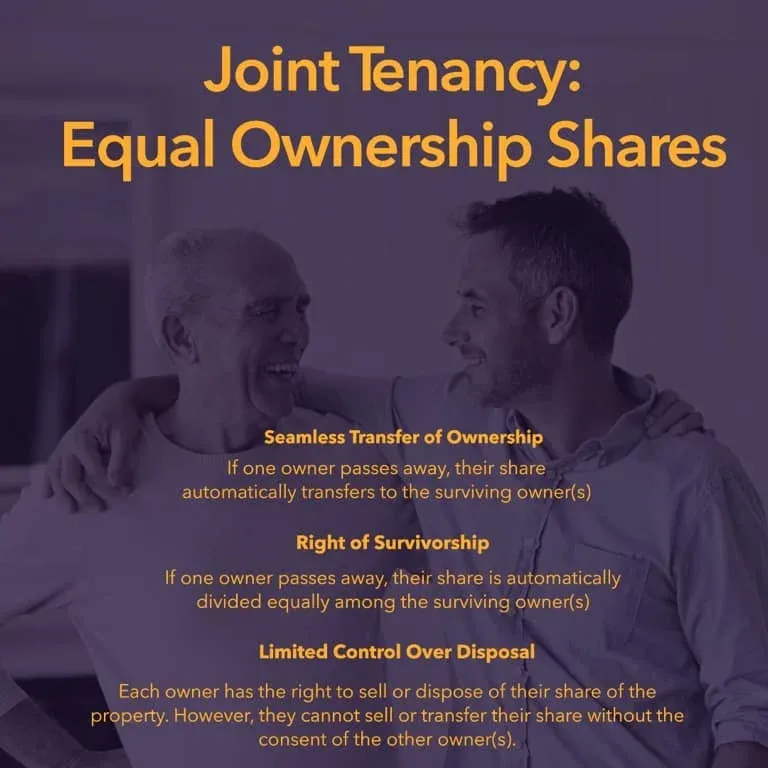

Joint Tenancy: In joint tenancy, all parties involved have equal ownership shares in the property. If one owner passes away, their share automatically transfers to the surviving owner(s). This structure ensures seamless transfer of ownership and avoids potential conflicts or disputes. Joint tenancy is often preferred when parents intend to transfer their share of the property to their children in the future.

Tenancy in Common: Tenancy in common allows for unequal ownership shares. Each party can own a specific percentage of the property, which can be determined based on financial contributions or other arrangements. In the event of an owner’s passing, their share can be passed on to a beneficiary of their choosing. Tenancy in common provides more flexibility in terms of ownership distribution and can accommodate varying financial contributions or circumstances.

It’s crucial to consult with a legal professional to understand the legal and financial implications of each ownership structure and determine which option best aligns with your needs and preferences.

We’ll cover this point in more detail later on in this guide.

Another important aspect to consider when buying a home jointly with parents is who will be living in the house. This factor can influence the ownership structure and financial responsibilities. Here are some common scenarios to contemplate:

Living Separately: You may decide to live in the house while your parents live in their current property. In this case, you may agree to pay a fair market rent for your parents’ share of the property, or come to another agreement.

Shared Occupancy: If both you and your parents plan to live in the property, it’s essential to determine the proportional share of each party’s ownership and contribution to expenses, such as mortgage repayments, utilities, and maintenance costs.

Investment Property: If you’re intending to buy the property as an investment and rent it out, ownership shares and responsibilities should be allocated accordingly, considering factors like rental income distribution and management.

Considering the occupancy arrangements and discussing them openly with your parents can help establish clear expectations and avoid potential conflicts or misunderstandings in the future. It’s advisable to seek legal and financial advice to ensure all parties are protected and informed.

To illustrate the mechanics of buying a home with parents, let’s take a look at the case of Emma, a young Australian seeking to enter the property market. Emma’s parents generously offered to help her by co-purchasing a property together. Here’s how they navigated the process:

1. Exploring Ownership Structures

Emma and her parents discussed the different ownership structures available, weighing the pros and cons of joint tenancy and tenancy in common. They opted for joint tenancy to ensure a seamless transfer of ownership in the future.

2. Determining Ownership Shares:

They decided on an equal ownership split, with each party having a 50% share in the property. This arrangement ensured fairness and aligned with their financial contributions.

3. Defining Financial Responsibilities:

Emma and her parents outlined their financial responsibilities, including mortgage repayments, property maintenance costs, and utilities. They agreed to contribute proportionally to their ownership shares, sharing the financial obligations equitably.

4. Establishing Occupancy Arrangements:

Emma planned to live in the property, while her parents would reside elsewhere. They established a rental agreement where Emma paid her parents fair market rent for their share of the property.

By carefully considering the mechanics of buying a home with parents, Emma and her parents successfully navigated the process, ensuring clarity and mutual understanding throughout their homeownership journey.