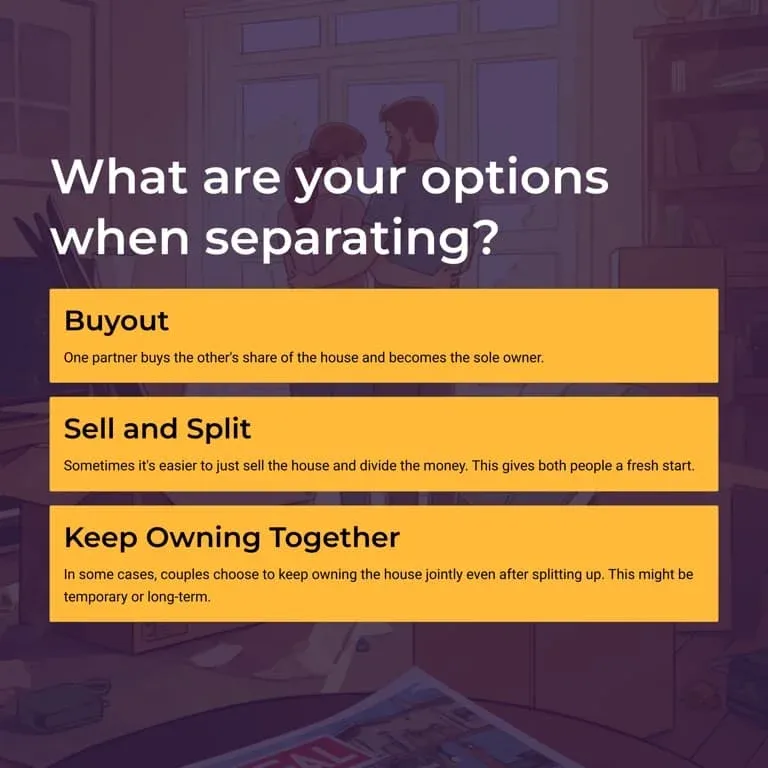

Thinking about buying out your partner after a separation? It’s a big decision — both financially and emotionally. Whether you’re trying to stay in the family home or keep things stable for the kids, this guide will walk you through the legal, financial, and personal angles—so you know exactly what to expect.

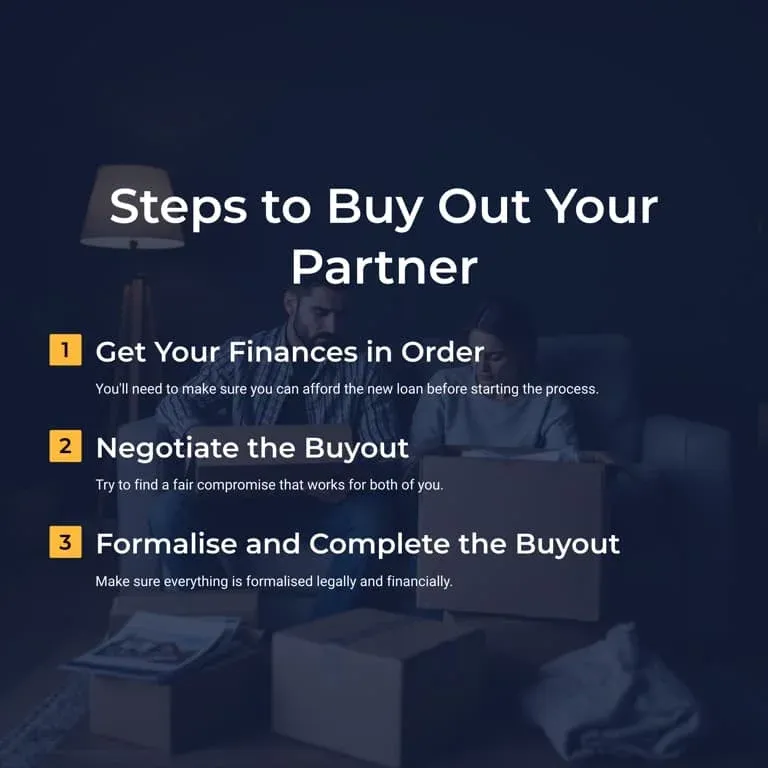

We’ll cover the key steps, including preparing your finances, negotiating the buyout terms, and completing the legal and financial transactions.

To learn more about how to calculate buying someone out of a house in Australia, you can watch the video below or read on for our detailed guide.