Mortgage stress rarely has a single cause. Usually, a mix of personal changes and shifts in the economy creates a “perfect storm.” Understanding these triggers helps you spot the warning signs early.

In Australia, several key factors push homeowners toward financial difficulty:

Between 2024 and 2026, many Australians faced a massive financial shock. This is often called the “mortgage rate cliff.”

During the pandemic, thousands of borrowers locked in ultra-low fixed rates around 2%. As those fixed terms ended, loans automatically rolled over to variable rates. By early 2026, many saw their rates jump to over 6% or 7%.

Sometimes, the cause is closer to home. Illness, injury, or a relationship breakdown can quickly drain your savings. These events often happen without warning. Because of this, having an “emergency buffer” in an offset account is a vital safety net.

Hunter Galloway Tip: If you feel the “cliff” approaching, don’t wait for your fixed rate to end. Talk to us three months early to plan your next move.

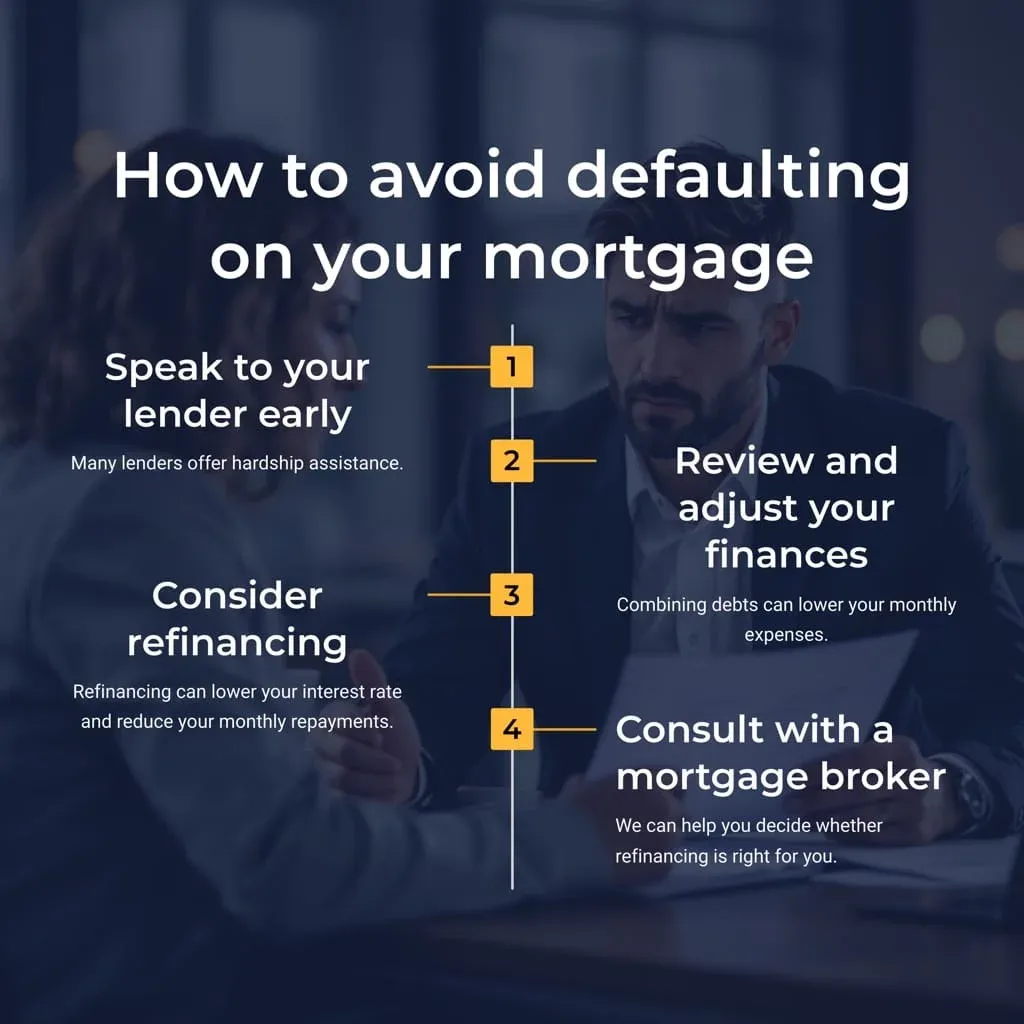

By knowing these causes, you can take action before a “stress” phase turns into a formal “default.” Acting early gives you the best chance to protect your equity and your home.