Lenders Mortgage Insurance (LMI) is a once-off insurance fee that protects the bank, not you, in the event that you default on your loan.

LMI is paid when your loan is settled and generally does not affect your interest rate but can affect your home loan repayments as it can be added (or capitalised) to the loan, meaning you don’t need to pay for it upfront.

Table of Contents

Why do you need Lenders Mortgage Insurance?

Banks require lenders mortgage insurance for high-risk loans such as borrowing a high percentage of the property value or when you have a lower deposit.

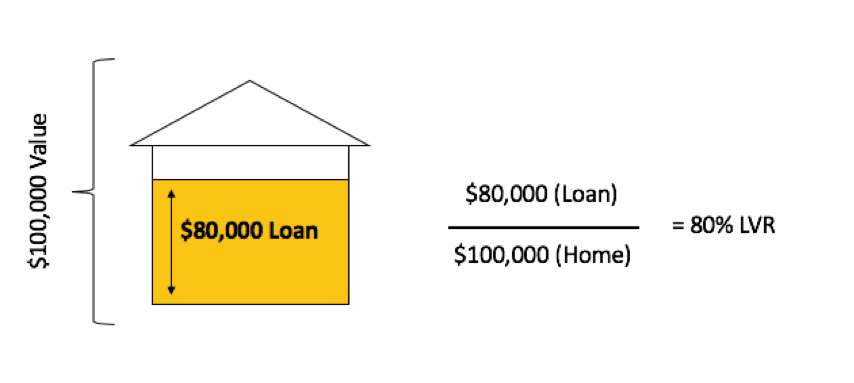

As a general guide, the lender’s mortgage insurance will become applicable when lending over 80% of the property value (also known as loan-to-value ratio).

You’ll pay LMI if you have less than a 20% deposit.

Self-employed clients who want to apply for a low-doc loan will usually have lenders mortgage insurance applied to them when borrowing over 60-70% of the property. This is because they are unable to adequately prove income.

The premium the insurer charges varies depending on the loan amount and the property value.

Who does Lenders Mortgage Insurance protect?

Around 20% of home loans in Australia get LMI coverage, but still, only a few buyers are aware of what it actually is and why the lender charges it.

Lender’s mortgage insurance or LMI is a type of insurance that provides protection to a lender (home loan providers and banks) against any risk of default by the borrower. Some borrowers have a misconception that they pay this for their own protection.

One study has shown that 40% of people do not know what lender’s mortgage insurance is.

2018 white paper by Mortgage Choice and Core Data’s Evolving Great Australian Dream showed that 42%of 1000+ respondents did not know what LMI is.32% said that they need it to purchase a house. 18%of the respondents believed that it is designed to safeguard both buyers and sellers, 8% said that it protects borrowers and only 32%knew exactly why they needed this insurance.

What are the benefits of Lenders Mortgage Insurance?

LMI can be quite useful, especially when property values are rising, because if you own your property for just a year, your home equity level increases and this will cover the cost of the lender’s mortgage insurance.

It allows you to get into the property market with a lower deposit, like less than 20% of the property value, which means you can get in sooner rather than having to wait and save up a big deposit.

Read More: 11 Hidden Costs of Buying a Home

What are the downsides of LMI?

The cost of LMI can be quite high, and in many cases, it restricts a borrower from refinancing as they would have to pay this cost again if LVR (loan to value ratio) remains over 80 per cent. Read more about how to calculate LVR.

Moreover, LMI decreases the overall return on investment and cannot be refunded.

In other words, once you pay LMI on the loan when you go to refinance or sell the property, it is a cost that has to be paid upfront on the loan.

Read More: 5 First Home Buyer Myths & Mistakes Revealed

Do you pay LMI when refinancing?

You need to pay LMI when refinancing with another bank if your loan-to-value ratio or LVR is above 80%. Unfortunately, you will still need to pay Lenders Mortgage Insurance when refinancing your loan, even if you paid it when you initially purchased your property.

For example, if you wanted to refinance your home valued at $600,000 and you owed $500,000, the LVR would be calculated as 83.33% and being over 80% LVR, you would still need to pay LMI.

Read More: 7 Reasons to Refinance your Home Loan

What does Lenders Mortgage Insurance cost?

Lenders Mortgage Insurance costs vary depending on the lender.

Lenders Mortgage Insurance is priced on a sliding scale—the higher your deposit amount, the lower the insurance costs. So, for example, a home purchase of $600,000 with a 10% deposit ($60,000) will mean you’ll end up paying around $10,000 in LMI – but the higher the loan amount, and the lower the deposit, the more this goes up.

Purchase Price | Deposit (%) | Deposit ($) | LMI |

$500,000 | 15% | $75,000 | $4,725 |

$500,000 | 10% | $50,000 | $9,860 |

$500,000 | 5% | $25,000 | $17,655 |

$750,000 | 15% | $112,500 | $9,033 |

$750,000 | 10% | $75,000 | $18,173 |

$750,000 | 5% | $37,500 | $34,372 |

*LMI amount calculated as the average of the big 4 banks on a purchase in Queensland.

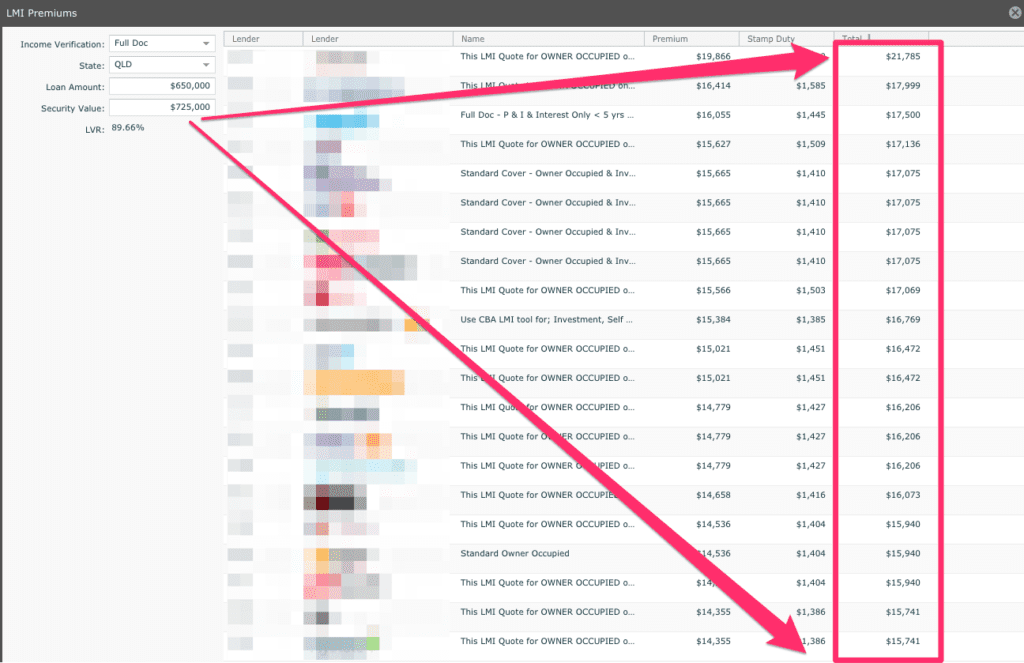

These costs change significantly across different banks, so in the same $600,000 purchase scenario, when you compare 7 different lenders, you can see there is a difference in cost from the cheapest ($10,301) to the most expensive ($16,121) of over $6,000!

Read More: 11 Hidden Costs of Buying a Home in Brisbane

Try the Lenders Mortgage Insurance calculator

Using our Lenders Mortgage Insurance calculator, you can work out what LMI will roughly cost to purchase or refinance your home. Just enter the estimated purchase price (or property value) and how much you would like to lend, and we will calculate the LMI for you.

Our LMI Calculator also finds ways of Avoiding Lenders Mortgage Insurance based on your job type. So, If you are a Doctor, Medical Professional or work in a few other types of professions, you may be able to have LMI Waived. Talk to our team to find out more.

Why is LMI so expensive?

Lenders mortgage insurance is very expensive as it represents a significant cost to the loan.

Therefore, whenever you plan to buy a house, it is important to seek the advice of a financial expert or a real estate broker, as they will be able to guide you in the right direction whilst keeping your financial goals in mind.

The cost of LMI depends on various factors, such as

- Loan amount

- Level of home equity

- Whether you are a first-time home buyer or an investor, and

- The risk associated with a particular loan package you are planning to buy

- The particular bank or lending institution

It’s important to understand that each case is different and dealt with differently. Therefore speak to our team of experts about your personal financial situation.

Having the right person guiding you will help you save a lot of money on LMI and will allow you to make home loan repayments on a timely basis, making it possible for you to repay the loan in full.

How to avoid LMI

There are several ways you can avoid paying LMI.

Increase Amount of Deposit

- You can purchase a home without having to pay lenders mortgage insurance. For that, you need to have raised a reasonable deposit. If you have a small deposit and your loan-to-value ratio is more than 80%, the risk of loss for the lender increases. On the other hand, having a bigger deposit means the loan amount will be lower; hence, lending to you will be a lower risk for the lender.

- You do not have to pay Lender’s Mortgage Insurance if you have a deposit worth 20% of the property value. Therefore, you need to decide whether the dream of buying a new home should be delayed while you save a little more money or if you should buy a property sooner with the added cost of the lenders mortgage insurance.

Find a Guarantor

- If you don’t have 20% of the loan, finding a guarantor can be a good option to avoid LMI costs. Your guarantor will ensure they will cover a part of your loan if you fail to make the loan payment.

- The guarantor can be the ‘bank of your parents’ that provides financing for your home with a loan or cash gift. The amount paid by a guarantor can also add up to your deposit and enable you to avoid the lenders mortgage insurance payment.

Seek Professional Advice

- Last but not least, always seek professional advice. A mortgage express broker can assess your financial position. Your broker can also help you secure the right finance source that aligns with your financial goals. Certain jobs and professions are eligible to have LMI Waived.

Read More: How to get no LMI and 90% LVR.

Can I get an LMI refund?

Several banks have changed their agreement with LMI providers in order to help customers so that they can pay lower premiums. Unfortunately, most of these changes happened in 2012, so if you have gotten your loan since then, you probably do not qualify for an LMI refund.

Is it possible to transfer an LMI Policy?

The answer is no. You cannot transfer your LMI policy to another bank. However, if you stick with the same lender, you can get a discount on a new LMI premium. This can happen if you internally refinance your loan or increase the existing loan amount.

Next steps and getting your home loan…

Buying your first home is a challenging job. In fact, it involves a lot of hard work, such as searching for the right property, going for inspections and sometimes auctions and searching for the right property. On top of that, you have to bear the financial burden that comes along with it.

In the current environment with low-interest rates, it might take years to save up to 20% deposit, especially if you are buying a house for the first time. Therefore, ensure you understand what LMI is and how to avoid it.

We can tell you if LMI can be waived for your mortgage!

Call us on 1300 088 065 or fill out our online assessment form.

Read More:

Start again

Start again