Suncorp is a smaller bank with good home loan specials and interest rates compared to the bigger lenders. But they can sometimes ask for more information and documentation than the other banks!

The reality is Suncorp will suit different people depending on your situation and what specials are available. They often have sharp deals for first-home buyers and sometimes even have special rebates if you want to refinance your home loan.

So are they right for you?

Today we review Suncorp’s Home Loans and put them through their paces.

Note this review, interest rates, and product information are subject to change without any further notification. Any credit applications are subject to meeting the specific bank’s criteria, and the decision is at their final discretion.

Table of Contents

What are Suncorp’s Home Loans like?

The top 5 things Suncorp are good at:

- 110% LVR no deposit First Home Buyer Loans. Suncorp has a loan package called the Deposit Kickstart Home Loan, which allows first-home buyers to get into the real estate market faster without needing a deposit using the help of a guarantor. This is also known as a Guarantor Home Loan.

- Less Genuine Savings required. Suncorp normally requires borrowers to save up at least 5% of the purchase price. When you apply with Suncorp, you do not need to have genuine savings (i.e. funds you have held in your account for over 3 months). This means your deposit could be gifted, from a tax refund or from non-genuine savings.

- Multiple Offset accounts. Suncorp allows you to have multiple offset accounts with your home loan. This is not the case with every lender—for example, the BOQ Privileges Package Home Loan only allows 1 offset account.

- Lender’s Mortgage Insurance (LMI). The bank offers one of the cheapest LMI on the market, allowing you to save heaps of money (we’ll show some examples below). Suncorp also has a delegated underwriting authority with QBE Mortgage Insurance, which can provide faster approvals and more flexible credit policies.

- Good deals for business owners and self-employed people: Suncorp has a range of small business products to help business owners and self-employed people with lending and transaction accounts. In particular, their Business Essentials products have very low fees and good lending options of up to $3,000,000.

The top 5 things Suncorp aren’t so good at:

- Stricter document requirements. As we will cover below, Suncorp requires more documentation than other banks. They require items like 3 months’ statements for all loans, credit cards, store cards and personal transaction accounts regardless if the loan or credit cards are being paid out—other banks do not ask for this information.

- Hard to find a package for unique situations. Although Suncorp offers several benefits to borrowers, including sharp rates and good fees, people with unique income situations like irregular bonuses or overtime might find it difficult to get their loans approved.

- Lower borrowing capacity. Suncorp has slightly tougher lending requirements, and, as we will cover below, the amount they will lend you is often lower than some of the other lenders. If you want to stretch your borrowing capacity, Suncorp might not be the right lender for you.

- Slow Assessment Process (if you go directly to the bank): Compared to other lenders, the assessment process of Suncorp is slow if you go directly to the bank, depending on how busy they are. Hunter Galloway has Priority Status with Suncorp, which means we can get you a faster approval. Talk to our team if you need a fast approval.

- Not the highest customer satisfaction (compared to other small banks). Suncorp customers gave the bank a relatively low net promoter score compared to BOQ and Gateway Credit Union. According to Suncorp’s 2022 Annual Report, their net promoter score was 20% compared to BOQ, which scored 87.2% and Gateway Credit Union, which scored 87%.

What are the different home loan products they offer?

Suncorp Bank has a wide range of home loan products, and the 4 most popular include:

1. Home Package Plus

The Suncorp Home Package Plus is similar to most other banks’ professional package loans, where you receive a discounted interest rate and other backing products like offset accounts and credit cards under one annual fee. It is only available on new home loans and subject to Suncorp’s credit criteria.

The variable home loan rate under Suncorp’s package is called the Standard Variable Home Loan. You can download their brochure here.

The annual package fee of $385 is slightly cheaper than other larger banks (who generally charge between $395 to $399) and includes benefits like:

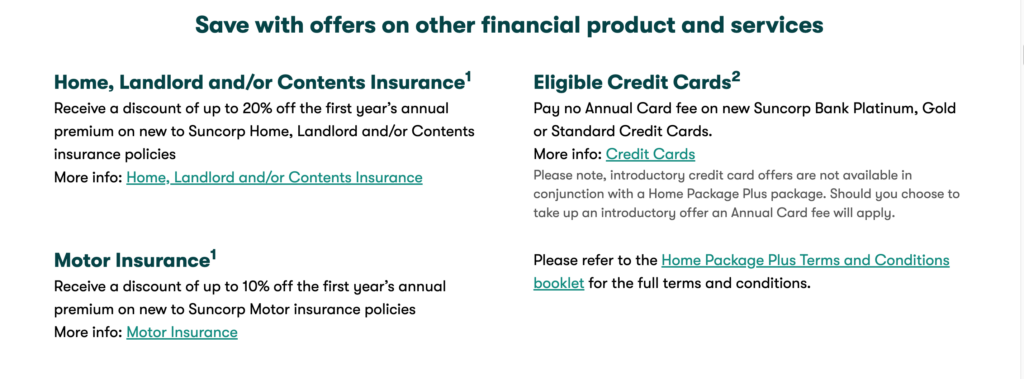

- Sometimes has specials for first-home buyers and new customers. For example, for a limited time, Suncorp is offering no annual fees over the life of the loan for eligible home loans. This is a saving of $11,250 over 30 years!

- Discounts of up to 20% off home, landlord and contents insurance.

- Discounts of 10% on the first year’s motor insurance.

- No annual fees on eligible Suncorp Platinum, Gold or Standard Credit Cards.

- No monthly maintenance fees on associated Suncorp Offset Accounts.

- Access to discounted brokerage fees on share trading.

- Interest-only options are available but are significantly more expensive than P&I repayments.

- Annual package fee is only slightly cheaper than the big 4 banks.

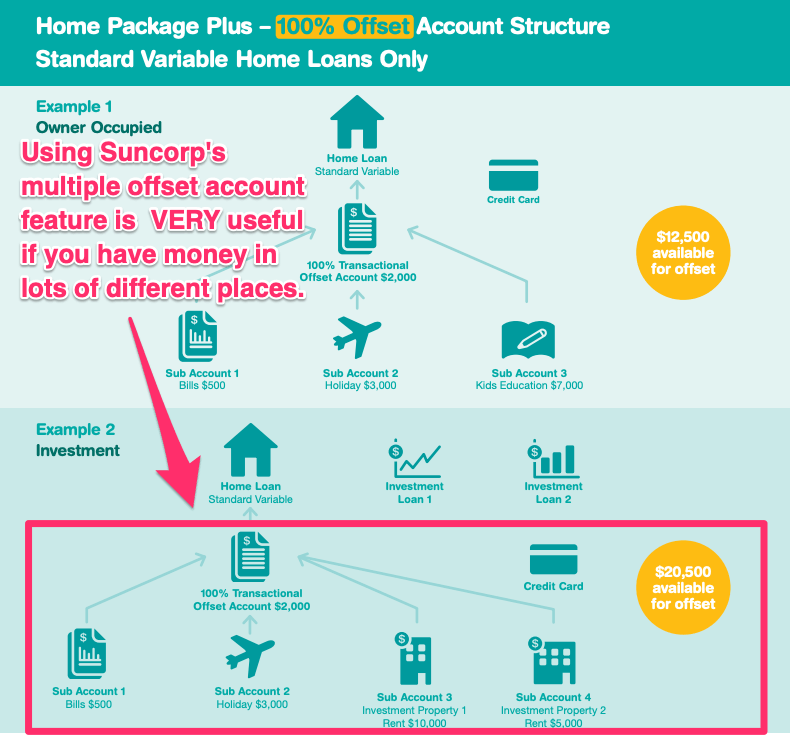

Multiple Offset Accounts

Under the Home Package Plus, Suncorp offers the feature of multiple offset accounts, allowing you to have more than one offset account against a single home loan. This is quite unique, as most banks will only allow one offset account against one home loan.

What this means is if you have more than one transaction account, you can link them all to your home loan account and save LOTS of interest.

You can also use investment accounts and other accounts to offset your home loan to reduce interest costs.

For more information, you can also take a look at the Home Package Plus Terms and Conditions brochure.

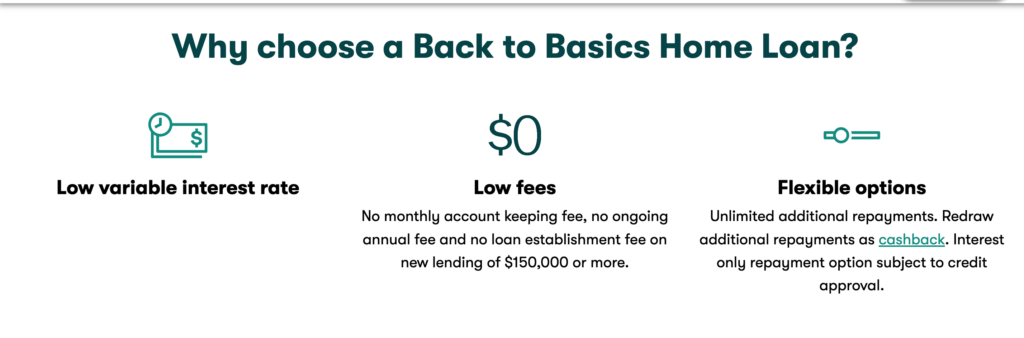

2. Back to Basics Variable

Suncorp’s basic home loan is just that, a product that is cheap and cheerful but has fewer features and fewer fees than the Home Package Plus product.

You can easily save money using a basic home loan product like the Back to Basics Variable if you don’t need any of the other features like an offset account and discounts on credit cards.

Some of the features include:

- Available for both personal, investment and construction purposes.

- No monthly or annual fees or establishment fees for lending over $150,000.

- You can make unlimited extra repayments without any penalty.

- Redraw is available but limited to only one free redraw per month.

- Mortgage offset is not available.

3. Access Equity Line of Credit

The Suncorp Access Equity Line of Credit works similarly to a credit card. After the bank has approved the loan, you can withdraw the funds from your line of credit (LOC) where needed and pay it back when you want.

Your approval limit is set by the total equity in your property, which is the difference between what your property is worth and the amount of lending you have against it. For example, if your home is worth $500,000 and you have a home loan of $400,000 against it, your home equity is $100,000.

The advantage of a Line of Credit over a regular Interest Only Home Loan is that LOCs are called evergreen, and their interest-only period finishes at the end of the loan term.

- Interest-only repayments, with interest, only paid on the balance of the loan.

- Can be used as a day-to-day facility, similar to a credit card.

- Access Equity Line of Credit can be covered under the Home Package Plus annual fee.

- Loan term of between 8 to 30 years.

- The interest rate isn’t as cheap as Suncorp’s other products.

Suncorp is also offering a Green Upgrades Equity Home Loan. However, this offer is only Valid until 29 Feb 2024.

The Green Upgrades loan is an equity loan that allows you to borrow between $10,000 to $25,000 against your home equity to make your home more environmentally friendly.

Acceptable upgrades and installations include:

- Solar system (lights, batteries, hot water systems e.t.c)

- Home insulation

- Energy-efficient glazing on windows and doors

- Water collection systems

- More energy-efficient appliances

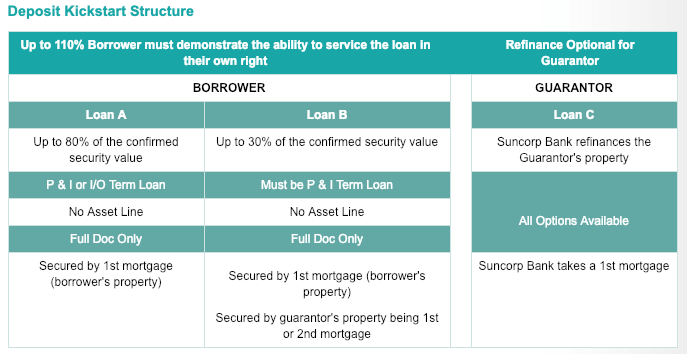

4. Deposit Kickstart Home Loan

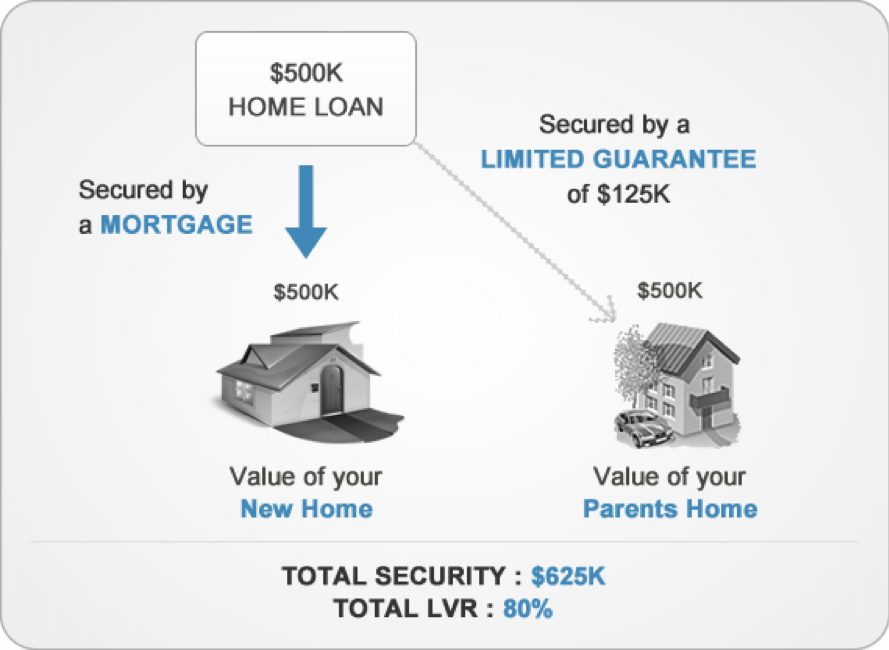

Like many other lenders, Suncorp offers a guarantor home loan called the Deposit Kickstart. A Guarantor Home Loan allows you to use a parent’s or close relative’s property to secure the deposit portion of your loan, meaning you don’t pay lenders mortgage insurance.

Suncorp’s product is a bit different because they will let you borrow up to 110% of your purchase price compared to the majority of other lenders who only allow between 100-105% of the purchase price.

For example, if you are buying a home worth $500,000, Suncorp Bank will let you borrow up to $550,000, while other banks would only allow a maximum of $525,000

This is, of course, subject to their credit criteria, and that your guarantor’s property has enough equity in it and is restricted to a maximum of 30% of their total property value.

Features of the deposit kickstart include:

- Borrow up to 110% of your purchase price

- Avoid paying lenders mortgage insurance when you have less than a 20% deposit.

- You can include fees and charges and even consolidate debt as a part of your 110% LVR loan amount

- Discounted interest rates as LVR is below 80% on your home + your guarantors’ homes.

- Guarantors do not need to refinance their homes to Suncorp.

- Guarantors need to obtain independent legal and financial advice.

- Tougher lending criteria compared to some other banks.

- Not available when using income from a second job, overseas income or on investment loans.

Read More: Guarantor Home Loans in Queensland [How to borrow over 110%]

What are Suncorp Bank’s Interest Rates?

Suncorp regularly offers non-advertised rates directly to Mortgage Brokers that they do not openly advertise. If you would like to know more info, call us on 1300 088 065 or get in touch.

Our mortgage brokers can help with arranging larger than standard discounts. Call us on 1300 088 065 or get in touch to have a chat.

What documents does Suncorp need for a home loan?

Suncorp’s application checklist is fairly standard compared to most banks (with a few small exceptions, which we’ve underlined below). Assuming you are a salaried employee and you are purchasing your first home, they would ask for the following:

- Signed Application Form and Privacy Act form completed by all borrowers.

- Identification documents: Current Medicare + Drivers license or Australian passport.

- 3 Months’ Bank statements showing your salary credits into your personal transaction account with your employer’s name.

- 3 Months statements showing all continuing liabilities – i.e. any open credit cards, personal loans, store cards or overdraft statements.

- 2 Most recent computer-generated payslips.

- Evidence of your Genuine Savings— statements to show the funds have been held for more than 3 months.

- Signed Contract of Sale.

The bank differs from some of the bigger lenders because they require more information if you are in casual employment, contract employment or receive bonuses and commissions.

Suncorp is a little bit more conservative around secondary income. You can download their application form here.

- If you are self-employed, they will need the last 2 consecutive years of end of financial statements and tax returns.

- If you are in casual employment, you need to be in the same role for at least 6 months. They will need your 2 most recent payslips AND most recent year’s PAYG Payment Summary (also known as a group certificate).

- If you are in contract employment, they need your 2 most recent payslips AND a copy of your employment contract with evidence of the remaining contract term.

- If you receive a bonus, regular commission or overtime, they will need your 2 most recent payslips AND evidence of at least 3 months minimum employment with the same employer and the last 2 year’s PAYG Payment Summary (also known as a group certificate). Before Covid-19, they would use only 80% of this amount. So if you received $10,000 in bonuses, Suncorp would only use $8,000 towards servicing your loan. But in September 2020, they reduced this to 60%.

These are the changes made by Suncorp in 2020:

Income | % of original income included |

Casual income earned continuously for more than 6 months will now be classified as secondary income and not core income. | 100% |

Dividend income | 60% |

Bonus payment income | 60% |

Commissions earned continuously for more than 6 months | 70% |

Seasonal income | 70% |

Overtime and allowances for nurses, police, fire and ambulance occupations | 100% |

Contract/Temporary agency income earned continuously for more than 12 months will now be classified as secondary income not core income. | |

Rental casual/holiday income must be earned continuously for more than 12 months and will now be classified as secondary income not core income. | |

What else does Suncorp offer?

Another point of difference Suncorp has from other banks like BOQ or Gateway Bank is its network of insurance brands which you might have heard of. They own AAMI, GIO, Bingle, Terri Scheer and Vero Insurance, to name a few.

Suncorp also has a good branch presence in Queensland but significantly fewer locations interstate.

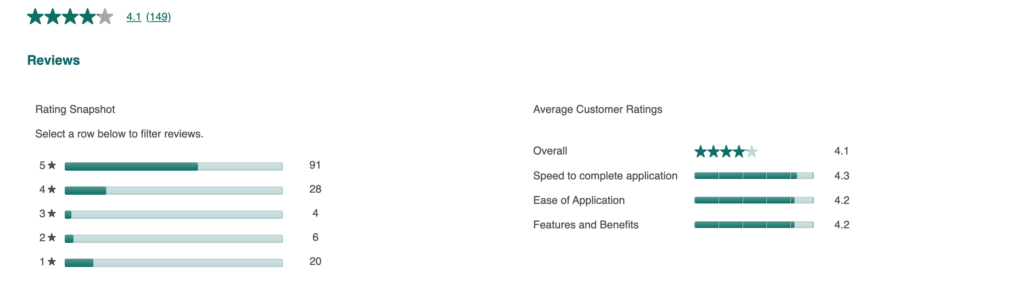

What are some Suncorp Home Loan customer reviews?

As we covered above, Suncorp’s customer satisfaction ratings are ok at 78% compared to other major banks that rank in the low 70s.

The reviews of Suncorp Bank online can be fairly mixed. This is because the majority are customers who have applied directly with the branch network rather than through a mortgage broker.

In our experience, Suncorp has been very good to deal with and has helped many of our customers get a great outcome.

BONUS: ACCC Rejects ANZ-Suncorp Deal: Impact on Home Loans

This section will cover the latest around the blocked 4.9 billion dollar ANZ Suncorp deal and how it impacts Australia’s banking competition and home loans.

What was the ANZ-Suncorp Deal?

Under this deal, ANZ would effectively acquire Suncorp’s banking licence. In addition to being a bank, Suncorp is also an insurance business. They would split it, and Suncorp would continue as an insurance business. ANZ was going to get the branches and the banking licence for 3 years then they were going to do what they wanted with it.

Suncorp wants to concentrate on insurance, particularly because the insurance business is becoming harder with all the natural disasters and everything happening. They no longer want to have to worry about banking and Home Loans. ANZ is keen to take them on because their market share has been falling behind the other three big Banks

The proposed deal was actually announced back in July 2022 — it’s been almost 12 months of working in the background, and the ACCC was one of the last hurdles. Both banks were pretty confident it would go through, but the ACCC said no.

Why did the ACCC reject the merger?

The Australian Competition and Consumer Commission has said it won’t allow the Suncorp ANZ merger in its current shape. Their main concern is that it will hamper the supply of Home Loans nationally and affect regional areas of Queensland where Suncorp is prevalent in the agriculture and commercial spaces. ACCC also said the merger would potentially reduce competition in the banking industry and make it harder for second-tier banks like Bendigo and Adelaide Bank to compete when the big four Banks become even bigger!

Bendigo Bank and Adelaide Bank are also really keen to take over Suncorp and have been fiercely fighting the ACCC, saying that if ANZ takes over Suncorp, it will reduce competition in the marketplace. Bendigo is actually saying Suncorp Bank should be sold to them because it would create more competition.

As of June 23, ANZ held about 13.3% of the mortgage market while Suncorp had 2.4% and Bendigo only 2.8%, which is why Bendigo really want to take over Suncorp.

How would an ANZ-Suncorp Merger affect home loans?

If the merger were to proceed, ANZ would likely close some of Suncorp’s branches and rationalise its lending products. This could make it more difficult for borrowers to find competitive home loans, particularly in regional areas. ANZ could also raise interest rates on Suncorp’s existing home loans.

The merged entity would have a market share of 15.7%, making it the third-largest home lender in Australia, and this would give ANZ too much power to set prices and could lead to higher interest rates for borrowers. In addition, ANZ could raise interest rates on Suncorp’s existing home loans.

The ACCC’s decision is a blow to ANZ, which had hoped to use the merger to boost its home loan market share. However, the decision may be good news for borrowers, who will likely benefit from increased market competition.

However, this is not the end of the road for the merger. ANZ has said it will appeal the decision to the Australian Competition Tribunal. The tribunal will hear the appeal in early 2024. So we will keep our ears open and update you on the progress.

How does Suncorp compare to other banks?

Overall each Bank and Credit Union has its own advantages and disadvantages, which will come down to your personal situation.

Talk to one of our mortgage brokers by calling us on 1300 088 065 or complete our free assessment to find out more details and see if Suncorp Bank is a good fit for you.

Ready to take the next step toward buying? We’re happy to help. Schedule a call today with a Home Loan Expert from Hunter Galloway, the home of home buyers.

Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again