Today we are going to show you exactly how to get to settlement after you’ve signed a contract of sale on a home.

This is the same process that’s helped over 1000 homeowners settle their properties.

This is a non-technical step by step guide. So if you’re not super technical, you’ll love the simple steps in this guide.

Let’s get started.

Settlement: 5 Simple Steps

- Step #1: Pay your house deposit

- Step #2: Get your loan formally approved

- Step #3: Arrange building & pest inspection

- Step #4: Sign your documents

- Step #5: Get the power connected & mail redirected

- Talk with a Mortgage Broker that understands the settlement process

- Bonus: Is a 21 day finance clause right?

- Bonus: How to get a finance extension on house contract?

- Bonus: What does a Contract of Sale Contain?

- Bonus: Details of different contracts across Australia

Step #1: Pay your house deposit

There is always a deposit payable to the real estate agent when you have signed a contract of sale…

But did you know the deposit is paid in two parts?

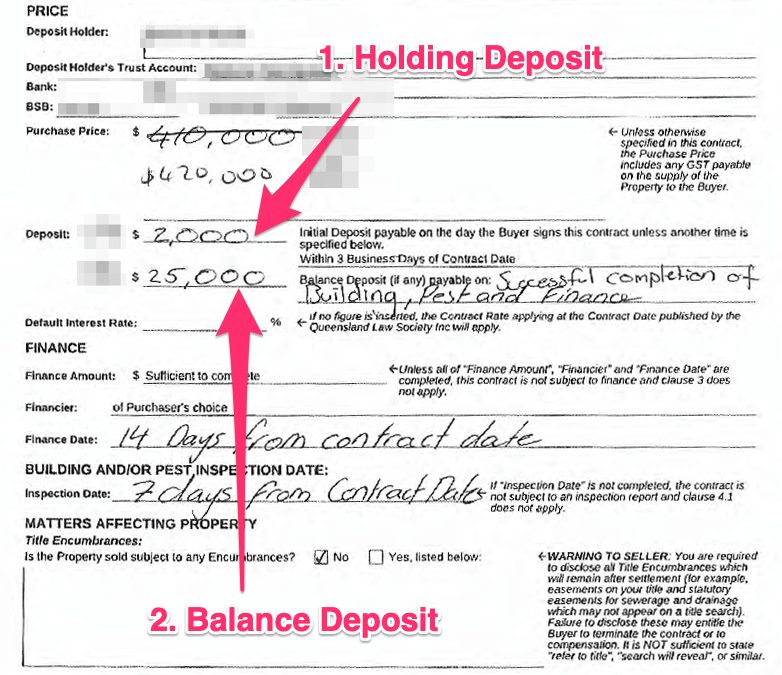

The deposit is detailed on Page 3 of the signed Contract of Sale. In Queensland, the deposit to buy a home is split into two parts on the Contract of Sale, (1) the holding deposit and (2) the balance deposit which in this case is payable upon successful completion of the building, pest and finance approval. Both need to be paid for the contract to become unconditional.

The first part is a holding deposit (also called the initial deposit) and is usually a small amount of $500 to $2,000 (or up to 0.25%) to secure the property.

The holding deposit shows that you are serious about buying the property and needs to be paid within 3 business days of signing the contract of sale. If you do not pay the holding deposit, your signed contract can be considered void!

The second part is the balance deposit and is more substantial. It is either a set per cent of the purchase price (like 5% or 10%) or a fixed amount like $25,000.

The balance deposit is paid once your finance and other conditions have been met.

The deposit is paid directly to the real estate agents trust account via electronic funds transfer, cheque or in rare cases cash.

The deposit is paid directly to the real estate agents trust account either by Electronic Funds Transfer, Cheque or Bank Transfer.

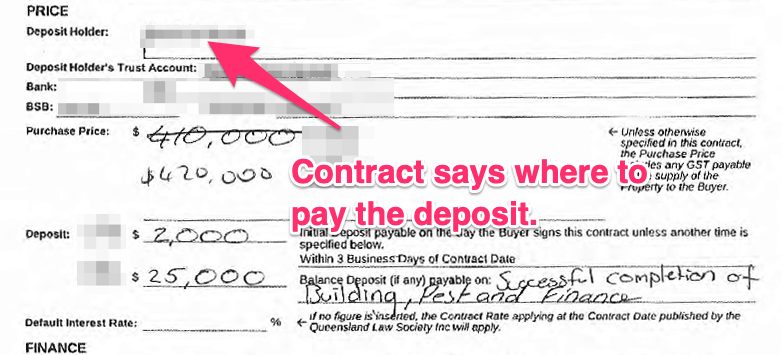

The deposit holder’s trust account details are on page 3 of the standard signed contract of sale in Queensland. The real estate agent is usually the deposit holder.

The signed contract of sale also tells you where to make the deposit payment, usually, this is to the real estate agents trust account.

Once you pay your holding and actual deposit, you need to request a receipt from the real estate agent to confirm this has been paid.

The real estate agent will hold the deposit in their trust account until settlement, and the amount you pay in deposit will reduce how much you need to pay at settlement.

For example, if your purchase price is $500,000 minus the bank loan of $450,000 and you had paid a $10,000 initial deposit, you only need to pay the deposit balance or $40,000 at settlement.

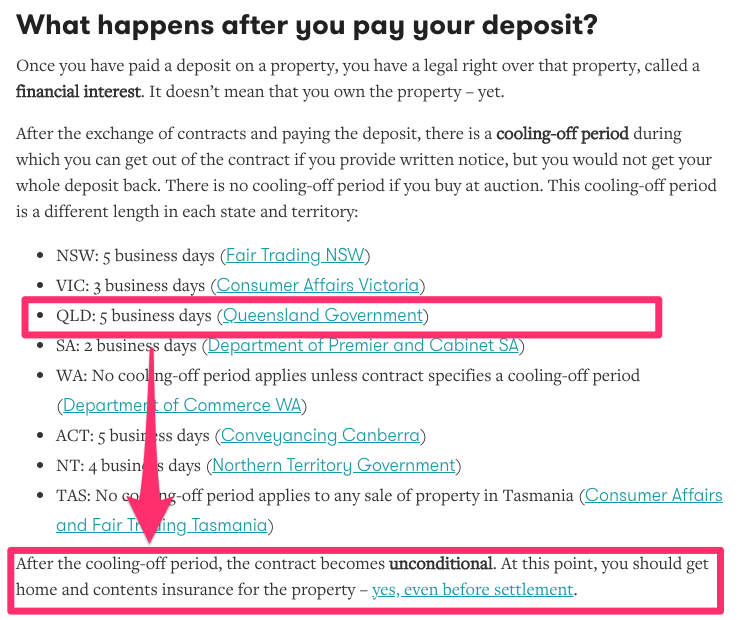

Once you have paid your deposit on a property, you have legal right over the property called a financial interest… Make sure you get your insurance sorted ASAP. Source: Canstar.

Read More: Step-By-Step First Home Owners Guide Brisbane

Step #2: Get your loan formally approved

Now it’s time to get in touch with your Mortgage Broker.

Working with a good Mortgage Broker makes this part of the process smooth and easy.

The steps in getting your loan formally approved include:

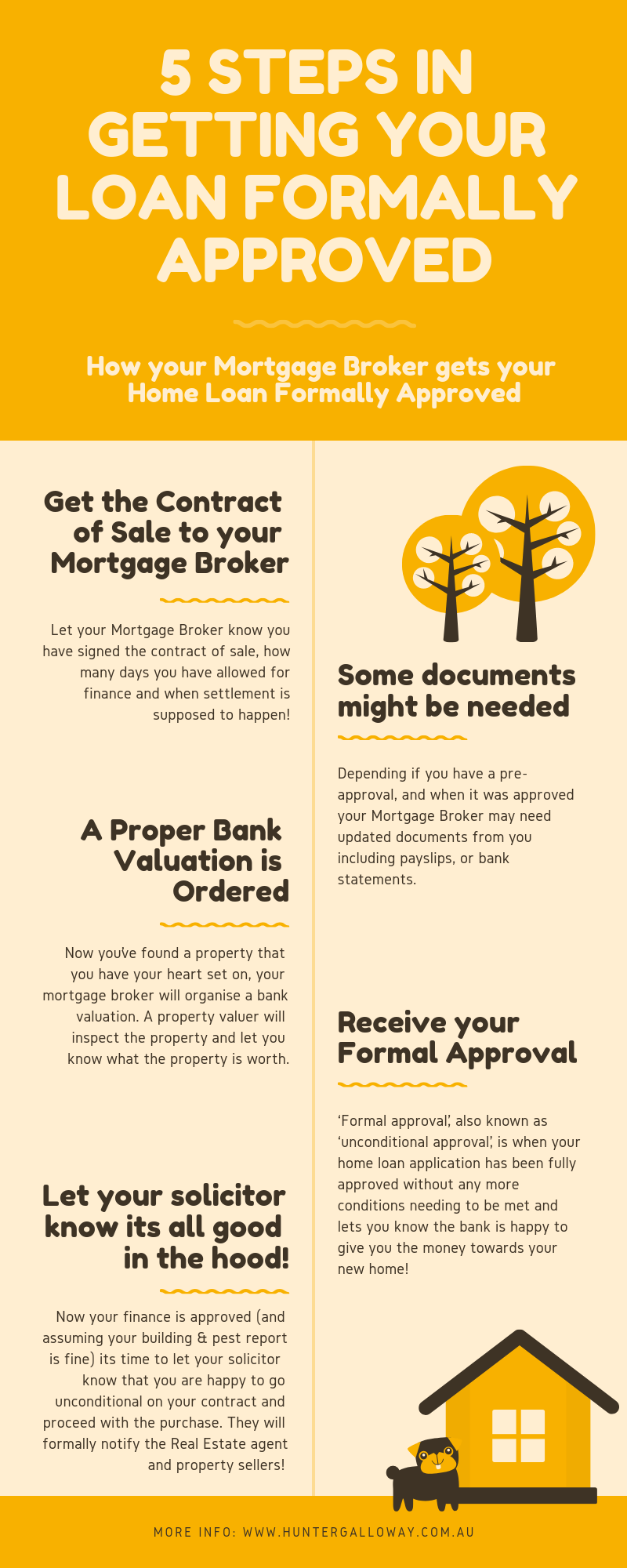

- Get the Contract of Sale to your Mortgage Broker. Let your Mortgage Broker know you have signed the contract of sale, how many days you have allowed for finance and when settlement is supposed to happen!

- Some documents might be needed. Depending on whether or not you have a pre-approval and when it was approved, your Mortgage Broker may need updated documents from you, including payslips or bank statements.

- A Proper Bank Valuation is Ordered. Your mortgage broker will organise a bank valuation now that you’ve found a property that you have your heart set on. A property valuer will inspect the property and let you know what the property is worth. Sometimes this may be different to your purchase price.

- Receive your Formal Approval (also referred to as unconditional approval). ‘Formal approval’, also known as ‘unconditional approval’, is when your home loan application has been fully approved without you needing to meet any other conditions, and the bank is happy to give you the money towards your new home!

- Let your solicitor (or conveyancer) know it’s all good in the hood. Now your finance is approved (and assuming your building & pest report is fine), it’s time to let your solicitor know that you are happy to go unconditional on your contract and proceed with the purchase. They will formally notify the Real Estate agent and property sellers.

What happens if my home loan gets declined?

Having your loan declined isn’t the end of the world.

Don’t worry this happens sometimes. Did you know in 2018 over 40% of home loan applications were rejected by the banks?

You have 2 options when your home loan has been declined by a bank –

- Option 1: Speak with your Mortgage Broker about applying for another loan with another bank.

- Option 2: Provided you signed the contract of sale subject to finance, let your solicitor know you were unsuccessful with finance. They can terminate the contract and get your deposit refunded.

Read More: First Home Buyer Loans

Step #3: Arrange building & pest inspection

Building & Pest reports are what we would consider the most common and almost mandatory cost when buying a house.

These reports look at the building’s structural soundness and pests to ensure you aren’t flatting with termites or white ants.

A typical building inspection for a 4 bedroom home can cost $400-500 and pest inspection $200-300 – the good news is you can save a few hundred dollars by getting a combined building and pest report for around $500-600.

Termites are surprisingly common in Brisbane homes.

I can say that Building & Pest reports have saved me over 5 times from buying complete dumps of properties.

With white ants, termites or even damp you can’t physically see it from the outside.

Building & Pest Inspectors (who in Queensland are generally licenced builders) will inspect under the house, in the roof and use their own technical equipment to check for damp and other issues.

I’m not kidding when I say these reports have saved me over 5 times.

In one year I literally spent over $2,000 on reports for different properties before finding the right place but I’m glad I did!

One of the properties had concrete cancer, another had issues with flooding and water leaking through the walls which were going to cost the new owner $9,000 to fix, another had termites in a tree in the backyard, and evidence of old damage in the roof.

This was all stuff they I wouldn’t have found out without using a building & pest inspector.

What happens if I get a bad building & pest report?

Not to worry, just let your solicitor know there is an issue with the building & pest report and they can terminate your contract.

Provided you had signed the contract subject to a building & pest report you will get a full refund of your deposit.

Read More: Why should I waste money on Building & Pest reports?

Step #4: Sign your documents

At this point, your Mortgage Broker will arrange a time to sign your loan documents.

You will need to sign your Home Loan Contract, Mortgage (title) Document, Direct Debit Agreement and any other bank forms.

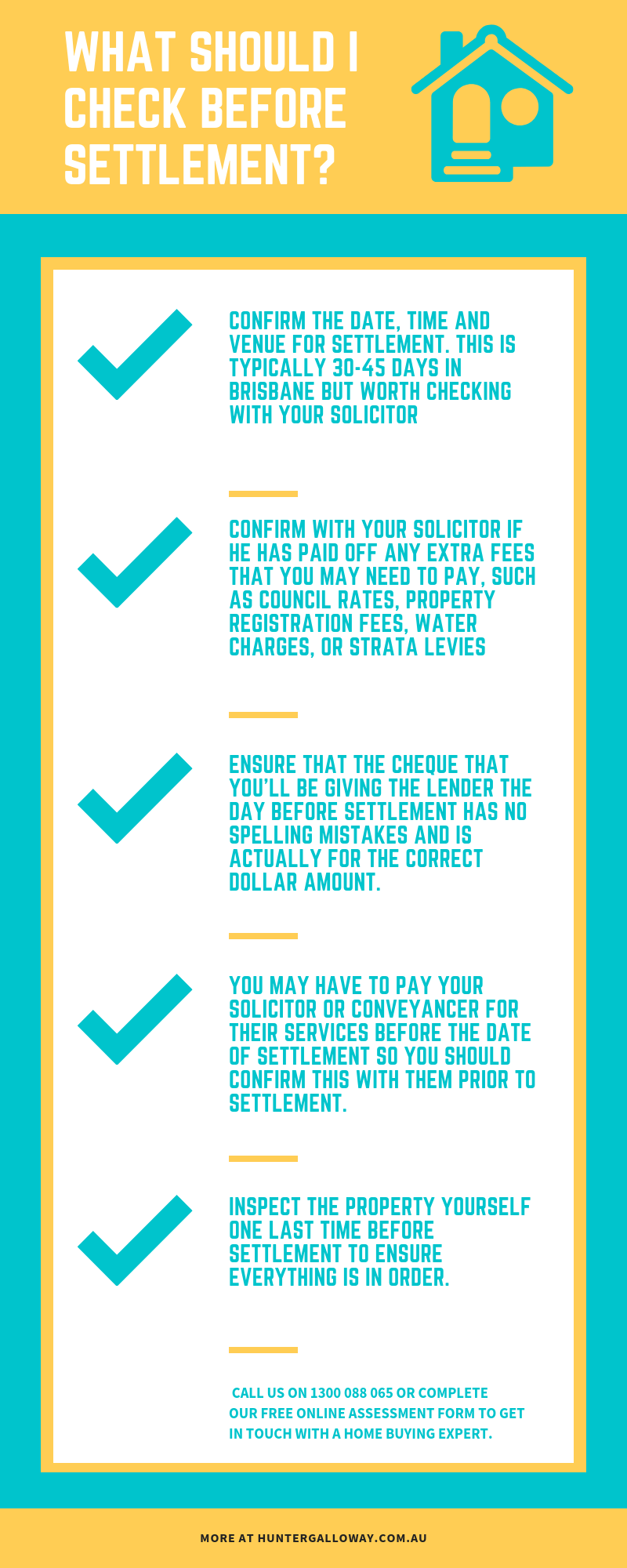

You should also get in touch with your Solicitor to confirm some important details like the date of settlement, if there are any other fees payable and if you need to arrange any cheques for settlement…

There are a few things to do even after you’ve signed your loan documents.

Step #5: Get the power connected & mail redirected

Moving costs might seem like an obvious one, but have you thought about getting the power connected and mail redirected?

Houses don’t have power connected unless someone is paying the bills…

And I’ve moved into houses without power, and had to wait 2 days to get it connected… 🌃

No power and no internet is not as fun as it looks… It’s pretty hard to keep the housewarming beers cold without any power… It was NOT fun

So remember to plan ahead, and shop around to see what deals you can get on your power.

With the increase in competition in the energy market in Brisbane, I have found you can get any connection costs waived provided you sign up for a 12-month contract. Phone around and see what you can do, but companies like Origin make this pretty easy when moving into a new home.

Redirecting your mail is pretty easy too, Australia post has details but a word of warning – it takes them 3 days to set up the redirection. So try to do this before settlement!

Just make sure you are organised to not lose any mail in the post!

So try to do this before settlement!

Read More: Moving & Connection Costs when buying a home

Bonus: Is a 21 day finance clause right?

When you buy a home in Queensland, you can sign a contract subject to certain conditions such as:

- ✅ You being approved for finance

- ✅ A satisfactory building and pest inspection

- ✅ If you can sell an existing property

It’s important to double-check these conditions are in your contract before you sign, otherwise, you can be bound to the contract. As the buyer, this is your responsibility.

The most common conditions we almost always recommend are the finance clause and building and pest clause. There’s a good reason we recommend these.

The finance clause: If you are buying a home in Queensland, the finance clause includes the total time you have as a buyer to get your home loan approved after signing the house contract. While you can increase your chances of your loan being approved by doing a pre-approval, a pre-approved loan is not a guarantee that the bank will approve your loan. If your financial circumstances change, or if the bank changes their lending policies in between your pre-approval and your formal application, then they may decline you. If you have a finance clause and your loan is declined, you can simply walk away. If you don’t have a finance clause, then you will be contractually bound to proceed with the purchase and you risk losing a lot of money if you can’t find a lender who will approve your loan.

The building and pest clause: As I mentioned above, the building and pest clause is another essential condition to add to your contract. While many agents will offer their own building and pest reports during the inspection process, there’s always a chance that their inspector missed a crucial issue. If your inspector finds something concerning, you may be able to renegotiate the price or decline to proceed with the purchase.

One question we get asked all the time is:

How long should my finance clause be? Is a 21-day finance clause good?

The short answer is no.

In a competitive property market like Brisbane, 21 days is WAYYY TOO LONG and you could miss out on your property.

Finance clauses represent a risk for the property seller. If they accept an offer for a purchase with a 21-day finance clause, then they run the risk of you walking away from the contract on day 20. That means they will have to go back to the market or see if any other bidders are still interested in the property. The shorter the finance clause, the “safer” the offer is in the eyes of the seller since they won’t lose any momentum with the property sale if anything does go wrong with your application.

When the property market is really hot (like we saw during the last couple of years), many buyers will submit an offer without any finance clause at all. So if you want your offer to remain competitive (without risking financial losses) then you want to keep your finance clause as short as possible.

We suggest a 14-day finance clause if you do not have a pre-approval, or once you have a pre-approved home loan you can even reduce it down to a 7 day finance period. If you choose Hunter Galloway as your mortgage broker, we will let you know the best finance clause length.

Read More: How to Make an Offer on a House

Bonus: How to get a finance extension on a house contract?

Your finance clause is due at 5 pm on the date noted on your contract.

In other words:

If you have finance due Wednesday – you have until 5 pm Wednesday to go unconditional on the contract and pay the balance deposit…Or decide not to proceed and get your deposit refunded.

But what happens if your home loan isn’t approved by the time your finance clause is due and you need to ask for an extension?

According to First National Real Estate Agents, “approximately 70% of the contracts we receive every year with a 14 day finance clause require an extension“ so don’t worry it is very common to ask for an extension on a house contract.

To get a finance extension on a house contract you need to:

- ☑️ Contact your solicitor/conveyancer and ask them to formally request a finance extension from the sellers.

- ☑️ You can also give a heads up to the Real Estate agent you will be needing a finance extension.

- ☑️ Your solicitor will send a request in writing to the sellers requesting the extension.

- ☑️ The seller’s solicitor/conveyancer will send confirmation back in writing confirming your finance extension.

From the seller’s perspective, they have 3 options when it comes to extending the finance clause: they can either grant the extension, do nothing or terminate the contract.

In most cases, we find the sellers will extend the finance clause.

This is because they have spent the last 7 to 14 days waiting for your finance to be approved, and a simple extension of 3-4 days is a much better prospect than starting the clock at 7 to 14 days with a new buyer.

Bonus: What does the Contract of Sale Contain?

It contains information about all the parties to the contract, including their addresses and names. Following is a list of information you will normally find in a contract of sale:

- ✅ Certificate of the title information

- ✅ Offer date

- ✅ Warnings, such as the necessity for a smoke alarm

- ✅ Settlement date of an intended property

- ✅ The cooling off period

- ✅ Information about furnishing and fixture

- ✅ Improvements to the property

- ✅ Property address

- ✅ Loan details, such as the terms and conditions of the payment, and initial deposit

- ✅ The price of a property

- ✅ Name of a seller

- ✅ Purchasing party information, and

- ✅ Information about the selling agent

Normally the special conditions are included in the contract of sale that can override the general conditions of the contract. Therefore, don’t sign the contract until you are fully aware of all the terms and conditions. The seller is required to attach the following with the contract of sale:

- ✅ Notification about the defects

- ✅ Warranties

- ✅ Sale conditions

- ✅ Disclosure documents

- ✅ Cooling off notice

- ✅ Warranty insurance certification

- ✅ Easement and restriction documentation

- ✅ Property certificates

- ✅ Zoning certificates, and

- ✅ Plans of sewer lines

If a seller fails to include these things, it gives a buyer the right to cancel the contract within a certain period of time.

Bonus: Details of different contracts across Australia

Victoria

The Instruments Act 1958 states that a verbal agreement is not binding unless you honour a contract of sale in full.

Before signing a contract of sale, the seller is bound to provide the potential purchaser with the seller’s statement. Both parties sign each contract’s copy and exchange it through a real estate agent. The cooling-off period in Victoria is 3 days.

New South Wales

In New South Wales and Sydney, you cannot sell a residential property without signing a contract of sale. A seller of a strata scheme or a single freehold must also provide a valid non-compliance certificate, an occupation certificate, and a valid compliance certificate.

Moreover, the vendor and purchaser are under no obligation to honour the contract until they exchange signed copies. These copies can be exchanged in a face to face meeting or via mail. The cooling-off period in New South Wales is 5 days.

Queensland

In Queensland, the cooling-off period is 5 days. The contract should include the following information for it to be valid: If the purchaser terminates the contract during a statutory cooling-off phase, they will be bound to pay a penalty of 0.25% of the purchase price. So if you terminate the contract for a $500,000 property, you will have to pay $1,250.

Therefore, we advise that you do a property valuation independently and seek legal advice regarding cooling-off rights and the contract before signing a contract.

In this state, the buyer signs the contract first, and the seller only signs it if he accepts the offer. It becomes binding only after the buyer receives an acceptance notification. It is important to note that in Queensland, only lawyers can act as conveyancers.

South Australia

In South Australia, a seller is bound to provide the buyer with a Form 1 Disclosure statement before signing the contract. After both parties sign the contract, they are bound by its terms and conditions. The cooling-off period in South Australia is 2 days.

Bonus: What to do when the seller backs out of the contract

In rare cases, a seller can choose to back out of a contract. What do you do then? Here are some of the steps a buyer can take when a seller backs out of a contract:

- Talk to your conveyancer or lawyer as this is a legal matter.

- The seller has to give back any initial deposit you had paid to them.

- The seller can be given an order to pay damages like money spent on building and pest reports, legal fees and any other expenses you incurred in the process.

- Sometimes the seller can be forced to go through with the sale. In this case, you must prove that the seller just paying damages is not enough to make up for your loss if you don’t get the property. For example, if the property is so unique, you will never find another like it.

- If the seller refuses to cooperate, there is always the option of taking them to court. Now bear in mind that this is costly and extremely time-consuming, and you may not get the results you want. However, on the flip side – a court case is expensive and time-consuming for the seller as well. So this motivates level-headed sellers to settle the dispute out of court.

Talk with a Mortgage Broker that understands the settlement process

The biggest secret to getting your home settled easily is working with an experienced Mortgage Broker.

Homeowners have a much higher chance of getting their loan approved quickly (and easily) if it is submitted to the right bank.

The Hunter Galloway Mortgage Broker Brisbane team is here to help. We have a team of home loan experts.

We specialise in helping homeowners with Finding the Perfect home Loan and focus on delivering the best service in Brisbane.

At Hunter Galloway, we are experts and would love to help you buy a home. We can First Home Buyers and Existing Homeowners with getting settled quickly and easily.

Please call us on 1300 088 065 or complete our free online assessment form to get in touch with a Home Buying Expert.

Start again

Start again