Guarantor home loans are incredibly popular these days but what do you do when you want to remove the guarantor?

Or what happens if your property has increased in value in a short period, is it worth removing the guarantee in the background?

In this post, we’re going to take you through how to remove a guarantor from your mortgage, how much it will cost and the steps you need to go through to cut ties with your guarantor.

These are the exact strategies we use to help home buyers remove their guarantee.

Table of Contents

How long do you keep a guarantor on a mortgage?

According to DFA, The bank of Mum and Dad is officially Australia’s ninth-largest lender and has about $34 billion in loans, making it bigger than HSBC, AMP and Bank of Queensland. Over 60% of first home buyers in Australia are getting financial help from their parents either through gifts or as guarantors on loans.

The way the banks see it, your guarantor is being placed onto the loan for the entire 25 to 30-year loan term and will continue until the bank approves your request to remove it. This is the default setting for guarantor loans.

In other words, if you did nothing after your loan was settled, your parents’ property would guarantee your loan until you either sell your home or pay it off in 25 to 30 years’ time.

When should I remove the guarantor?

Realistically you should aim to remove the guarantor within 5 years or once you are in a financial position to remove it. But this comes down to your personal situation—how quick you have been able to pay down the guarantor portion and your property’s value.

Overall the best time to remove a guarantor is when you owe under 80% of your property’s value. This is done for the following reasons:

- You avoid Lenders’ Mortgage Insurance fees and could save thousands

- You could qualify for better interest rate discounts

- The process involves less paperwork

Being able to remove the guarantor usually comes down to how much you owe.

For example, if you initially borrowed $420,000 which is a Loan To Value Ratio (LVR) of 105% (because it included stamp duty, settlement fees and other costs), on a $400,000 purchase, and you have since paid down the loan to $320,000, you can now refinance your loan because the LVR is 80%.

On the other hand, if you had only paid the loan down from $420,000 to $405,000 but your property value had increased to $450,000 you could still refinance with a 90% LVR loan but you will need to pay lenders mortgage insurance (LMI) which is a one-off premium charged by the lender to protect the lender. LMI is compulsory if you are borrowing with an LVR of more than 80%. For that reason, we recommend waiting to remove your guarantor until your LVR is under 80%.

What are the steps in removing a guarantor from the mortgage?

The exact process of removing a guarantor from the mortgage varies from bank to bank. But in general, you will need to go through these steps:

- 1. Contract your mortgage broker to review your financial situation

- 2. Arrange a bank valuation.

- 3. Confirm the total loan amount.

- 4. Make sure you meet the lender’s criteria.

- 5. Submit a partial release, or internal refinance.

- 6. Wait 5-8 days for the bank to process.

- 7. Complete property release or internal refinance.

- 8. All done, your parents can pick up their title from the bank.

The biggest difference in the process is in step #5: If you have an 80% LVR loan, you can submit a partial release.

If you have a 90% LVR loan, you will need to complete an internal refinance and the loan will be subject to lenders mortgage insurance approval.

More on that below…

What are the fees involved in removing a guarantor?

Banks will charge some administrative, and possibly government fees to remove the guarantor. But these are usually under $500, provided you aren’t paying lenders mortgage insurance.

The good news, is some banks are offering up to $4,000 in refinance cash backs which can help offset any costs in removing your parents guarantee, contact our brokers today to see if you are eligible.

Your bank will let you know if there are any other application or valuation fees involved.

Removing a Guarantor from Mortgage with an 80% LVR loan

Removing a guarantor with an 80% LVR is great because you will avoid paying a Lenders Mortgage Insurance (LMI) premium. LMI can run into the tens of thousands of dollars so, if you can avoid paying it then that’s good.

Here’s exactly how it works:

- Your loan repayments need to have been made on time and be up to date for the last 6 months.

- Your loan must be less than 80% LVR.

- Your income, employment and credit history need to meet the bank’s current policy. Remember, every time you look to remove the guarantee, you are doing an application with the lender, so they’re going to assess you based on your income as of application day.

- The bank will complete a valuation on your home.

From here, different banks have different processes.

For example, St George Bank can complete the valuation and then remove the guarantor without changing your loan structure by doing a partial release.

On the other hand, other banks like CBA who set up guarantor home loans as two separate loan accounts will need to internally refinance your home loan to remove the guarantor.

ING Bank have an entirely different process and consider removing a guarantor the same as removing a borrower.

If this is all sounding too hard, don’t worry give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Removing a Guarantor from Mortgage with a 90% LVR home loan

The initial steps and process in removing a guarantor with a 90% LVR home loan are similar to the ones above However, by removing a guarantor with a 90% home loan you are effectively refinancing and removing the guarantee.

Here’s exactly how it works:

- Your loan repayments need to have been made on time and be up to date for the last 6 months.

- Your loan must be less than 90% LVR.

- Your income, employment and credit history need to meet the banks, and LMI current policy.

- The bank will complete a valuation on your home.

The biggest problem we see at this stage is that different banks will value homes at different amounts. We have seen up to a $130,000 increase in valuations on the same property by different banks.

At Hunter Galloway, we can order an upfront valuation with more than one lender to help you find the lender with the highest property valuation.

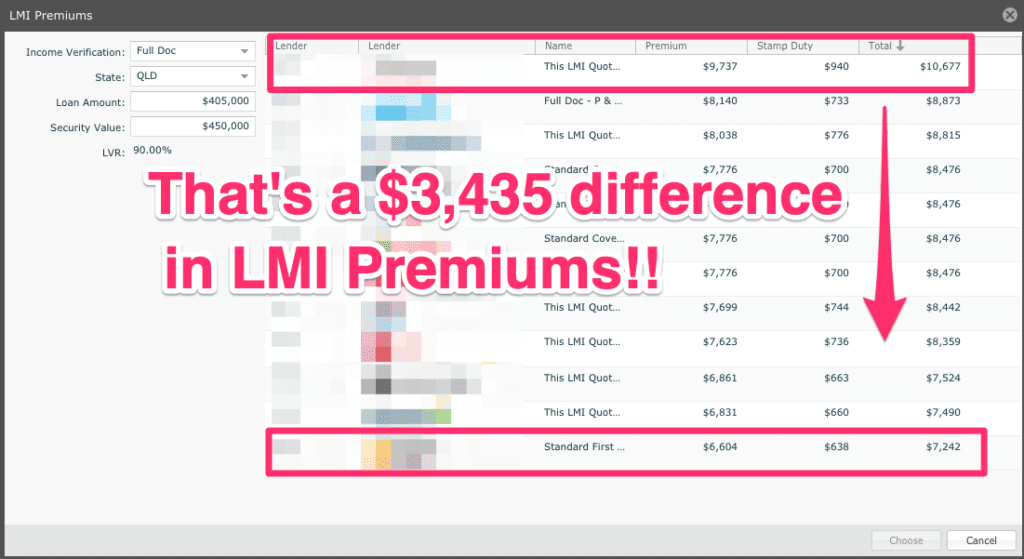

The second item to be aware of is that different banks also charge different Lenders Mortgage Insurance premiums.

In the same example, if you were refinancing the $405,000 against a property that was valued at $450,000 you could pay as little as $7,242 in Lenders Mortgage insurance or as much as $10,677, depending on your lender!

That’s a $3,435 difference in Lenders Mortgage Insurance premiums. It definitely pays to look around and we can help you do that.

Again if this is all sounding complicated, don’t worry give us a call on 1300 088 065 or get in touch online to see how we can help.

When will I have to pay lenders mortgage insurance?

Lenders Mortgage Insurance needs to be paid if the value of your mortgage is over 80% of your property’s value. So, If you have less than 20% equity in your home you will need to pay lenders mortgage insurance.

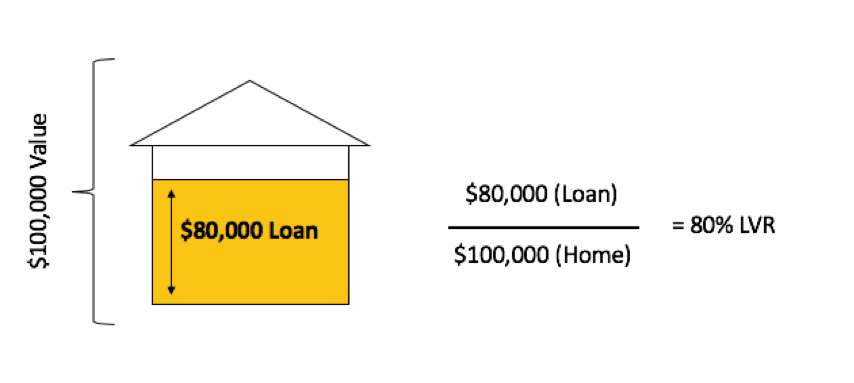

To calculate your LVR, or Loan to Value Ratio just divide your loan amount by your estimated property value.

For example, if you owe $405,000 to Commonwealth Bank and your home is worth $450,0000:

- $405,000 / $450,000 = 0.90

- 0.90 x 100 = 90% LVR

In this case, you would need to pay lenders mortgage insurance.

On the other hand, if you owe $360,000 to Commonwealth Bank and your home is valued at $450,000:

- $360,000 / $450,000 = 0.80

- 0.8 x 100 = 80% LVR

In this case, the LVR is equal to 80% so you do not need to pay Lenders Mortgage Insurance.

What if my guarantor situation changes and I have to remove them?

Keep in mind that your parents or relatives have done you a massive favour by providing their guarantee and helping you into the property market. So, it’s good to remove them as soon as possible because having their guarantee in place can hold back their future plans.

For example, they might not have enough equity to purchase an investment property with the guarantee in place or you might have a brother or a sister who will also need a guarantor.

Can my guarantor sell their home?

They can. But, you must keep in mind that there is a second mortgage registered on their property. So, when they sell their home, that second mortgage either needs to be paid out by the guarantor or you’ll need to refinance your property so that you can add that second mortgage back onto your property.

However, if your guarantor is selling their property just after you have set them up, you might not have enough equity in your property to refinance your loan.

While it is possible to place a portion of the sale proceeds as a term deposit during the time your guarantor is looking for a new home, it all comes down to your individual situation which we can discuss with you.

Give us a call on 1300 088 065 or get in touch online to see how we can help.

This situation where your guarantor wants to sell their home is tricky and we recommend you chat to us before they list their home.

Can I sell my house if I have a guarantor loan?

Absolutely. Once again, remember that if you have borrowed 100% of the purchase price and you under-sell your property, the remainder will be left on the guarantee’s property. So, make sure your selling price covers the full debt.

What happens if I get divorced and have a guarantor home loan?

We can look at refinancing your guarantor home loan to remove one of the borrowers and have you as the only owner and borrower on the home loan while leaving the existing guarantee as is .

It is also possible to refinance your existing guarantee with a new guarantor as well.

Case study:

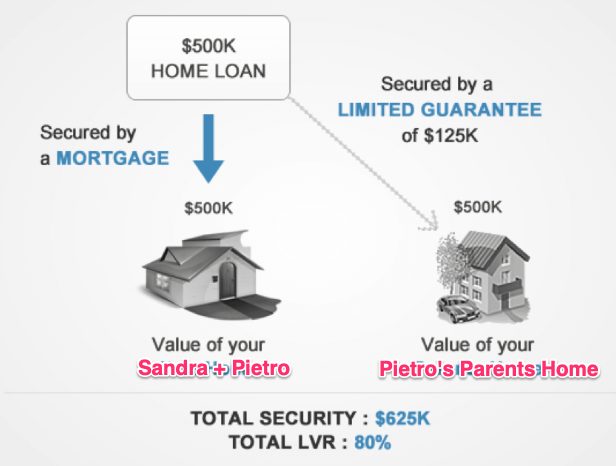

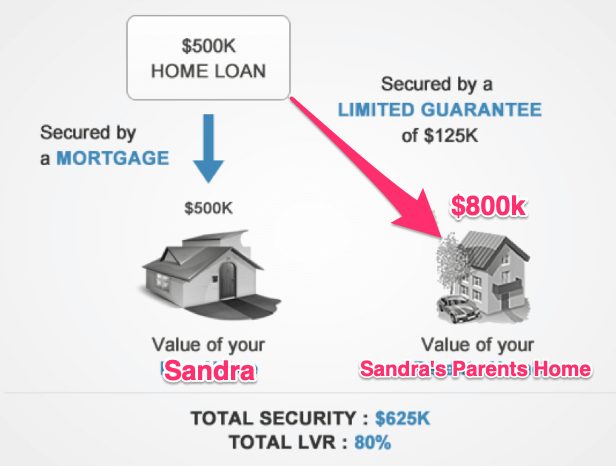

Sandra and Pietro bought their home with the assistance of Pietro’s parents. They have gotten divorced, and Sandra is going to get the property as part of the separation.

Sandra not only needs to remove Pietro from the loan and title, but also needs to refinance Pietro’s parent’s guarantee.

Fortunately, Sandra’s parents are happy to go on as new guarantors, so she completes a refinance to remove Pietro and his parents, and add Sandra’s parents on.

Sandra’s parents’ home is worth more than Pietro’s parents home, but this doesn’t matter as the limited guarantee of $125k is removed from Pietro’s parents home, and put onto Sandra’s parents home.

If you need to pay out your ex or are needing to refinance your home loan after a divorce contact us on 1300 088 065 and we can assist with removing your guarantee.

Case Study: I used my parents' home as a guarantor home loan

Thomas used his parents’ home as a guarantee for his own loan in place of an initial deposit. After 3 years Thomas’ property has increased by over $100,000 and he is in a position where he can refinance using the equity in his property to secure the total lending and remove the guarantee from the loan.

- Home value 2018: $550,000

- Initial home loan (including the guarantor): $550,000

- Initial LVR: 100%

We ordered a bank valuation for Thomas and his home was valued at $650,000. So, he was able to refinance and remove the guarantor with the same bank with minimal paperwork.

- Home value 2018: $650,000

- Current home loan (including guarantor): $520,000

- Current LVR: 80%

As his LVR reduced from 100% to 80% Thomas was also able to qualify for better interest rate discounts and overall lower interest rates.

Bonus: Buying a house with your friend

Many people who buy a property with their mates or partners make the mistake of getting into a jointly and severally liable loan. This means that if your mate can’t (or refuses to) pay the mortgage, the bank will go after you, even though you have been faithfully making your payments every month.

Worst case scenario, the bank will repossess the property, and a default will be listed against your credit file. If you have a default listed against your credit file, you may be unable to borrow for up to 7 years!

So, if you have a mate or someone that isn’t related to you that you are looking to buy a property with, then a Property Share is a good option. Property Share allows you to split the cost of buying a home with friends (or family) while still retaining individual control of your finances.

This arrangement helps first-home buyers and investors get into the property market sooner. All property share borrowers will be owners of the property and will guarantee each other’s home loan(s) as security. A maximum of 2 home loan applications per security is allowed, but each application can have multiple loan products, e.g. a split loan.

The benefits of Property Share are as follows:

- Pooling your money with friends and family will reduce the amount of time you need to save a deposit. This is especially important when the average time it takes to save a house deposit is now 11.4 years!

- You will have higher borrowing power, meaning you can afford a bigger and better property than if you were going at it alone.

- Since you retain control of your finances, you can split the loan whichever way you want, and each person can decide how they want to manage the repayments.

- You can still access a wide range of features, such as redraw facilities, offset accounts and lines of credit.

Before buying a property with a friend, talk to a Mortgage Broker who will ensure you get the right type of loan.

Learn more about the home buying process:

- How Much Deposit Do I need to buy a home (without a guarantor)

- 21 Mistakes nearly all first home buyers make

- Find the best suburbs in Brisbane

Chat with our team at Hunter Galloway now about removing your guarantor from home loan guarantee, call us on 1300 088 065 or get in touch here.

Speak to Guarantor Home Loan Experts

If you would like to chat about removing your guarantor or arranging a new guarantee, we’d be delighted to help you out, speak with one of our experienced mortgage brokers to walk through the next steps with you.

At Hunter Galloway, we help home buyers get ahead in this competitive market. We can give you strategies that have actually helped other home buyers like you secure a property even when there have been 5 other offers on the table!

Enquire online or give us a call at 1300 088 065.

Start again

Start again