Can you buy a home while pregnant or on maternity leave? In this ultimate guide, we will help you understand whether or not you qualify for paid parental leave as well as maternity leave letters (including downloadable templates).

You will love the actionable tips and templates in this guide as we will unpack what’s involved in setting up a maternity leave home loan.

Let’s dive in.

Table of Contents

Watch: Buying a home when pregnant

Maternity leave letter

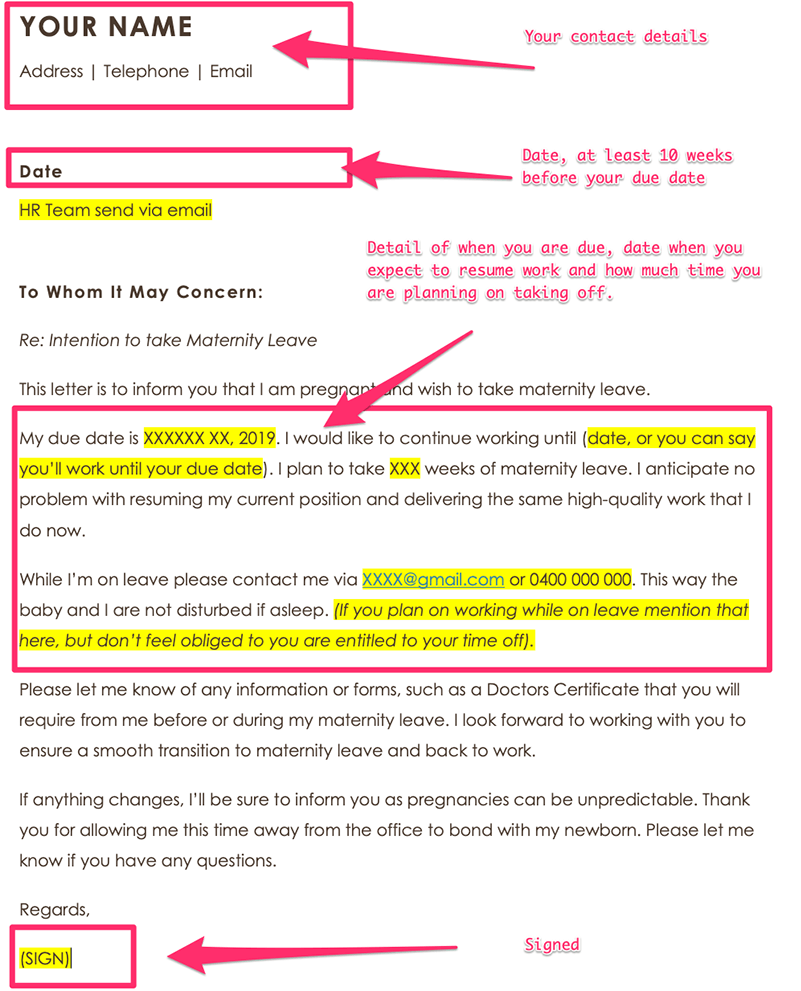

You will need to give your employer written confirmation that you intend to take some personal time off to have your baby.

In Australia, this should happen at least 10 weeks before your due date, and in many cases, it happens much earlier (when it gets harder to hide that baby bump).

While you need to tell your work that you will be taking Maternity Leave at least 10 weeks before your child’s expected date, you must confirm your parental leave dates at least 4 weeks before taking your leave.

If you have to go on leave sooner, for example, if the baby is premature, you are still entitled to take your leave — you just need to tell your work as soon as you can.

Template for a maternity leave letter in Australia

Some employers in Australia have strict requirements for letters requesting Maternity Leave.

Use the outline below to help make this process as smooth as possible:

Your letter should:

- Have a date.

- Include your signature.

- Contain your full name and address.

- Have information about the expected date for leaving work and when you plan to return.

- Include the expected date of birth for your baby. If you are adopting, the expected date of placement.

- If you like, you may include a medical certificate from your Obstetrician or Doctor confirming your pregnancy and the expected arrival date of the bub. Mums will often not worry about including this with the letter, but your employer has the right to request this from you, so it’s worth having it on hand.

Usually, an email copy of the Maternity Leave Letter to your Manager or HR team should be acceptable.

Make sure you keep a copy on your personal email or print it out to keep at home – so you have confirmation of everything in writing even when you aren’t in the office.

Paid Parental Leave Scheme

There have been some major changes to the laws in Australia, which mean if you are the primary carer of a newborn or adopted child, you are entitled to 18 weeks of paid leave.

In addition, eligible working dads and partners (including same-sex partners) get 2 weeks of paternity paid at the national minimum wage.

If you are a permanent employee who has worked for at least 12 months without taking parental leave, then your employer is required to provide 12 months of unpaid leave.

What are the criteria for Paid Parental Leave?

According to Centrelink, you need to:

- Be in paid work, having received an income of $150,000 or less in the previous financial year

- Have worked continuously for at least 10 of the 13 months before the birth

- Have worked at least 330 hours in those 10 months

The Paid Parental Leave scheme also covers casual workers, contractors and self-employed workers.

How much do I receive from Paid Parental Leave?

If you meet the eligibility criteria, you get paid the minimum wage of $812.60 per week (before tax) for up to 18 weeks.

Your partner could also be eligible under Dad and Partner Pay for up to 2 weeks, meaning in 20 weeks, you could receive $16,251.

Read More: Parental Leave Pay from the Department of Human Services

Buying a home while pregnant or on maternity leave

So, you’re expecting a little bundle of joy.

But what does that mean for you and your plans to buy the home you’ve always dreamed of?

Do you have to choose between a baby and a home?

…Or can you have both?

The good news is that some lenders will approve a home loan for you even if you’re not making an income. And the even better news is that a maternity leave home loan is one example of this.

Can I get a home loan while on maternity leave?

Yes, you can get a mortgage while you are on maternity leave. Here are a few things to take note of:

- Under the terms of a maternity leave home loan, you can borrow up to 80% of the property price, and it can be as high as 90%, depending on each individual case.

- If you are on unpaid maternity leave, you’ll need to have some money set aside to use for making repayments.

- You are still eligible for special discounts, packages and offers even if you are pregnant or on maternity leave when applying for a mortgage.

Applying for a home loan during pregnancy

Our number 1 tip is that it’s actually best to apply for a home loan when you are pregnant and still working.

This cuts out many complications because it can be much harder for you to secure a home loan whilst on maternity leave.

But before applying for the loan, sit down and create a clear financial plan before the baby arrives so that you’re prepared for how you will deal with the change in circumstances.

Remember that you’ll need a bit of extra money to use for the bad days too.

In summary:

- Apply for your home loan before the baby comes, if possible.

- Organise your finances and get a clear plan in place, so you know what you’ll be able to afford whilst on maternity leave.

Which banks will offer maternity leave home loans?

Unfortunately, most banks simply reject your loan application as soon as they find out you are on maternity leave.

Why?

Because they consider it risky – based on the possibility that you may not return to your job after pregnancy. There are also some banks that won’t accept maternity leave home loan applications because they base the evaluation on current income – so be aware of this.

The good news is even though lending policies for this type of home loan are stricter, we work with several banks that still offer a home loan to those who are on maternity leave.

Give us a call on 1300 088 065 or fill in our free online assessment, and one of our mortgage brokers will call you to discuss your situation.

Documents required to apply for a home loan on maternity leave

To qualify for a Maternity leave home loan, you will need to provide the following documents:

- Evidence of income or employment, such as salary slips from three months before starting the leave. It also helps to have your group certificate or PAYG summary showing your previous year’s income.

- A letter from your employer that states that you are on maternity leave. The details of your employment after you return to your job should also be mentioned, along with the return date and working conditions for when you return (full-time or part-time). The letter should be on your employer’s letterhead.

- Statements showing your savings held in your accounts, loans or investments.

- Details of any government entitlements you are currently receiving, like Paid Parental Leave or Family Tax Benefits.

Assessment criteria of a lender

Some banks will consider using your return-to-work income towards your borrowing capacity, provided you can meet your commitments during any unpaid leave.

Below are some of the main things a bank takes into account when assessing your ability to repay the loan, with larger importance placed on your savings to ensure you have enough to cover any income shortfalls each month:

- The equity you have in your home

- The savings you have on standby

- Government benefits you are entitled to

- When you intend to return to work

The duration of maternity leave is also a key factor for banks when they assess your Maternity leave home loan.

How long can I take maternity leave for?

The maximum leave period accepted by lenders is 12 months. However, lenders consider it a more favourable option if the duration is between 4 to 6 months.

If the lender finds out that you may struggle to keep up with the home loan repayments during pregnancy, it is unlikely your loan will be approved.

So, make sure you stay up to date with your finances and have a clear plan set in place over this period.

Unpaid or paid maternity leave: does it make a difference?

Banks positively view paid maternity leave over unpaid leave. This is because you’re still l making money each week.

But there is one issue; most employers only pay half of your salary when you are on leave; therefore, lenders don’t evaluate the home loan based on a normal salary.

This can affect your application because your weekly income is much lower than usual.

Is it possible to put my mortgage payments on hold?

You might have had bub and want to consider putting your Mortgage Repayments on hold until you return to work.

This is sometimes called a Repayment Holiday, Mortgage Safety Net or Repayment Pause.

What options do I have for repayment holidays?

If you have already applied for a loan and have started paying your loan off, then you may have a bit of equity in your home. This is the best scenario because you could release equity to help you with the repayments.

The equity may also cover your day-to-day expenses while you are on leave.

Some banks will allow you to increase your loan to cover the additional costs while you are off work. However, in this case, you cannot pause the payments… but there is another option…

Get a 50% reduction on your home loan repayments

A repayment holiday is a home loan with a break of up to 12 months, reducing your mortgage repayments by up to 50% during this period.

This offer is only available if you:

- Make extra repayments

- Have a defined return date

- Always make repayments on time.

What are the criteria to reduce my home loan payments?

Westpac Bank is one bank that offers the option to reduce your payments while on parental leave.

There are both positives and negatives to this:

- Your monthly loan repayment will be discounted for up to 12 months while on parental leave, giving you room to breathe financially.

- Your loan balance will increase by the difference between the monthly interest charge and the reduced monthly loan repayment during your parental leave period.

- At the end of the parental leave period, the repayment amount will be adjusted so that the new loan balance is repaid within the current approved term, meaning your repayments can increase to more than they were before you took the holiday.

- The maximum term for parental leave is 12 months per application— fees and charges might apply.

- This is only eligible for Westpac Home Loan customers who have been with the bank for over 12 months.

While this could be a good option if you feel financially squeezed while on Parental Leave, you are just delaying making the payment until you return to work, so some caution needs to be exercised.

How long will it take to make up for my repayment holiday?

A repayment holiday is a break from repaying your loan, but it will add another 6-12 months to your home loan.

A great plan would be to start saving a year or two before you plan to conceive, as this will relieve you of financial pressure during maternity leave.

How can I set up a maternity leave loan?

Speak to our team at Hunter Galloway to help you choose the best lender for you and go through all the options when setting up a home loan during maternity leave.

Our team of mortgage brokers will set up a free consultation to determine which home loan option is best for you.

Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

Talk to one of our mortgage brokers on 1300 088 065 or complete our free assessment.

Start again

Start again