Are you a first-time home buyer feeling overwhelmed by the amount of information out there? Don’t worry; you’re not alone. Many first-home buyers fall prey to common myths and mistakes that can be costly and time-consuming.

At Hunter Galloway, we are mortgage brokers that specialise in helping First Home Buyers navigate the home loan process. Our goal is to ensure you have the knowledge and support you need by removing some very common misconceptions about home loans and buying your first home.

In this article, we’ll reveal 11 of the most common first-home buyer myths and mistakes so you can make better, more informed decisions when it comes to purchasing your first home.

Table of Contents

Myth #1: It's cheaper to rent than own

This myth keeps renters on the lease Merry-Go-Round for years. Most people see the news—how property prices fluctuate and interest rates are increasing, and they decide that it’s cheaper just to rent. But rents have been going up, too. In fact, rents rose by a record 24% for units and 10% for houses between 2022 and 2023!

You won’t know if renting is cheaper unless you talk with mortgage brokers like us. We can determine how much you can afford to borrow, what the loan repayments will be and how much deposit is required.

Chances are you might find that loan repayments are similar to or even lower than the rent you’re currently paying. Wouldn’t you rather pay off your own home than someone else’s?

Read more: Renting vs buying calculator.

Myth #2: It's a bad time to buy

There is a saying that the best time to buy was yesterday. This saying is true because we can always look through rose-coloured glasses at low-interest rates and cheap houses of yesteryear, but nobody knows what’s coming tomorrow.

If you want to keep waiting, you might be missing out on valuable years of price growth on your home and not to mention paying off your home loan rather than paying rent…

Read more: First home buyer guide

Myth #3: You can't get a home loan if you have a HELP debt.

You can still buy a property when you have a Higher Education Contribution Scheme (HECS) or a Higher Education Loan Program (HELP) debt. Sounds too good to be true? It is good, and it is true!

The banks look at your HELP loan from an angle of how much you’re required to pay each year.

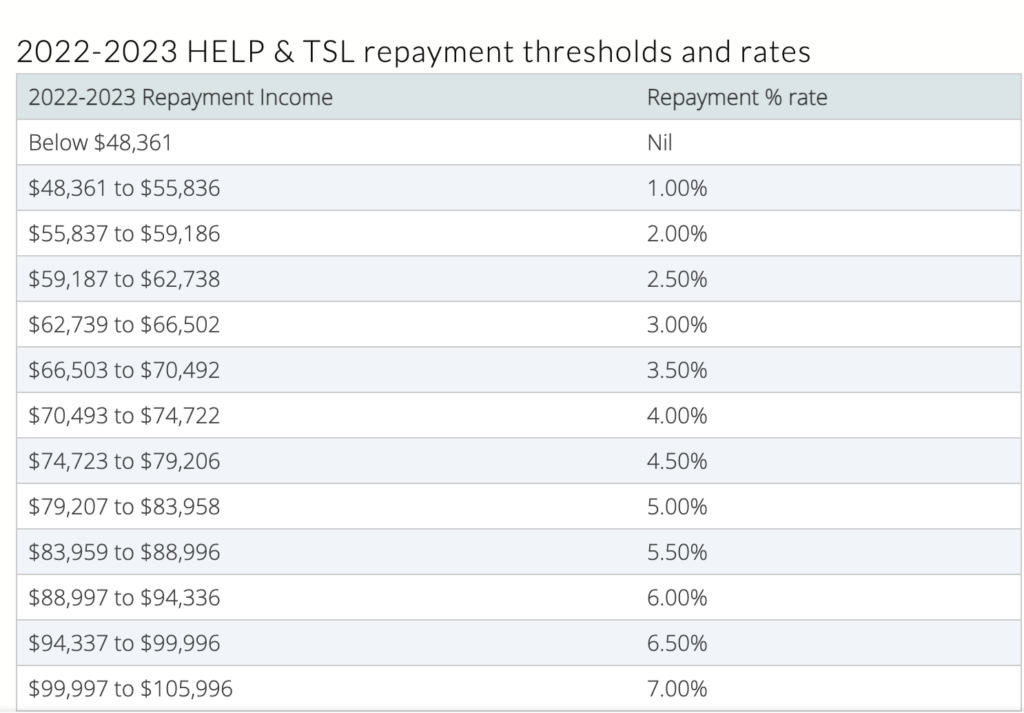

For example, if you earn $55,000 and owe HELP, the bank will factor in $55,000 at 2%, which is equal to $1,100 per year in repayments on your HELP. This will slightly lower your borrowing capacity but won’t rule you out altogether. You can see more examples of repayments for different income brackets below.

Of course, if you have very little of your HELP debt left, you can just pay it off. The bank will remove it as a liability from your ongoing assessment, and your borrowing capacity will increase. You do need to provide proof to the bank that you have paid it off.

The reason why most people think they cannot buy a home with HELP debt is because they choose the wrong lender. At Hunter Galloway, we can help you find a lender suited to your current situation. Get in touch with us online or give us a call on 1300 088 065 to see how we can help.

Myth #4: You should take a mortgage out with your existing bank

Plenty of first homeowners instinctively default to taking out a mortgage with their existing lender without even shopping around. However, just because it’s your current lender doesn’t mean they will have the best deal for you. It’s a good idea to compare different home loans and shop around to make sure you’re making the best decision for yourself.

Sometimes your existing lender has too much information on you, which can work against you. They can decline your application because they’ve seen something they’re unhappy with.

Myth #5: You should avoid fixed rates.

Many first-home buyers believe variable rates are best for them. From an outsider’s perspective, this seems like the logical option as they offer flexibility and additional repayments. There’s also the opportunity to open an offset account to reduce interest costs each week.

But you should consider a fixed rate if you want to budget over a 1-3 year timeframe. Fixed rates are great, particularly if you’ve got a family event in the future that you want to budget for and you want to know your total expenses. For example, if you’ve got a wedding coming up, your expenditure will increase, and you want to know exactly what to budget. So, fixed rates give you that absolute stability and control over your finances.

Another option that many first-home buyers don’t know about is that you can get a split loan. A split loan is a mortgage where part of the loan has a fixed interest rate, and part has a variable interest rate. This gives you the security of a fixed rate and the flexibility of a variable rate—the best of both worlds.

Bonus Myth: Offset account

Since we have mentioned the possibility of opening an offset account – this is another myth that needs to be addressed. Offset accounts are not the best option for everyone.

Don’t get this wrong; offsets are great. But remember that when you set up an offset account, the bank charges you annual fees.

There are other ways around the offset account. You can use a redraw facility which allows you to make extra payments and take them back out. Basically, redraw does the same thing as offset – with a few differences – but it has no cost.

Remember, the main goal is to reduce the interest you are paying on your mortgage and, ultimately, the total cost of the mortgage.

Myth #6: You shouldn't put down less than a 20% deposit.

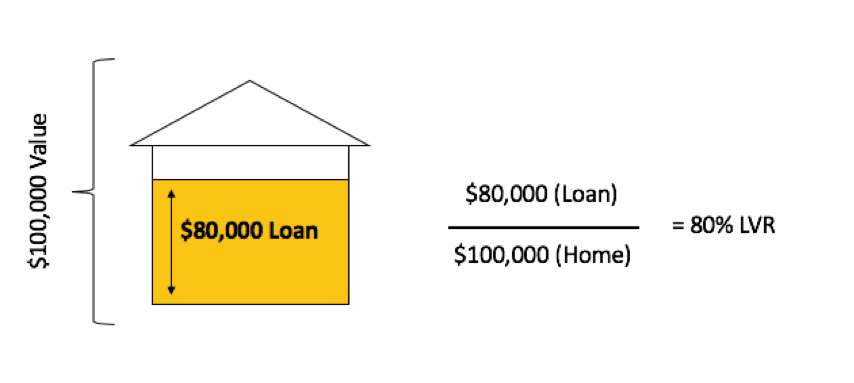

Times have changed, and the old belief of putting down at least a 20% deposit is no longer true. Of course, the bigger your deposit, the less you’ll need to borrow, which means you will avoid Lenders Mortgage Insurance (LMI).

However, trying to save up that 20% deposit can prevent you from getting your foot into the market sooner. If you do the calculations, you may see that paying LMI is better than waiting years and years to save up that 20%.

For example, we had a client who wanted to buy a $500,000 property. They had a $50,000 (10%) deposit, and we worked out that their LMI would be under $10,000. Now, if they had to save up to 20% deposit, they would need to save another $50,000 more, which would take them more than a year. So it was better to use their 10% deposit and pay the LMI.

For our buyers, anywhere between 5-8% of the purchase price is accepted. This is a great way to help get you into the market.

Our statistics show that 81% of our buyers put down less than a 20% deposit on their first home. Consider some of our low deposit options starting from as little as 5%.

Another thing to remember is that your profession impacts your deposit. Lenders mortgage insurance can be waived for doctors, lawyers, nurses and other certain lines of reliable work and high income.

If you don’t have a 20% deposit, you can also consider guarantor loans where you don’t need any deposit at all.

Myth #7: Mortgage insurance protects you.

Lenders mortgage insurance is exactly as it sounds. It’s an insurance policy that protects the bank. Some home buyers mistakenly believe that the lender’s mortgage insurance protects them if they default on their loan. Actually, the exact opposite is true. Lenders mortgage insurance is a safeguard for the bank in case the borrower defaults on their loan.

Lenders hedge their bets on all loans using a third-party insurance company. If you have a low deposit, the insurance company views you as a higher risk and will charge a premium to your lender, which the lender will, in turn, pass on to you. Now note the lender’s mortgage insurance premium is generally capitalised on top of your loan, so you don’t have to pay this out as an additional out-of-pocket expense immediately.

Read more: What is lenders mortgage insurance

Myth #8: Your pre-approval is fine for any property type.

Many first home buyers don’t realise that if you have been pre-approved to buy at a particular price, the property type can impact how much the bank will ultimately let you borrow – or if they will lend to you at all!

Not all banks lend to inner-city postcodes, and some have restrictions on unit complexes.

Typically once you’re pre-approved, some of the conditions that banks might set out to say you need to meet when getting your formal approval would be a satisfactory valuation of the property and confirmation that there’s been no change in circumstances with income deposits or roles. Sometimes they might even ask for updated bank statements and pay slips, depending on how long it’s been since you’ve been pre-approved.

This is particularly important to keep in mind if you’re going to be bidding at auction. If you win at auction, your contract will be unconditional, and you’ll be required to pay a deposit regardless of whether or not your loan is formally approved.

Once again, a pre-approval is just a great indication, and it’s not an ironclad. So, if you’re considering buying an apartment in the city, a townhouse, or even a house in certain postcodes, speak to your mortgage broker and confirm if your bank will accept it.

Read More: How reliable is your pre-approval?

Myth #9: You are locked in with the lender for the duration you have the loan.

You don’t have to stick with the lender you got your home loan from. If you later find out that their packages are less than ideal, you can always refinance your mortgage later. Refinancing can help you secure more competitive rates and access potential Equity or additional features you’re looking for in a home loan. There can be fees associated with refinancing, but there are several lenders that also give incentives to refinance.

Read more: 7 reasons to refinance your home loan

Myth #10: Lenders follow interest rates set by the Reserve Bank of Australia.

The Reserve Bank cash rate is the interest rate that every bank has to pay on money they borrow from it. If the Reserve Bank changes the cash rate, banks then choose to pass this on to customers.

For example, if the Reserve Bank of Australia drops interest rates from 3% to 2.5%, then Banks can choose to incorporate these savings into their home loan products or leave the interest rate they are offering unchanged. The opposite is also true. If the Reserve Bank increases the interest rate, banks can choose to increase the interest rates on their home loan products.

Ultimately, lenders decide whether or not to follow the interest rates set by the reserve bank. This is why comparing loans with the mortgage broker is important, as different lenders may choose to pass on the rate cuts or increases in different ways for different products.

Myth #11: Your friends and family know best.

While getting recommendations from your friends and family is good, it’s important to remember that what worked for them might not work for you.

A particular mortgage broker may have worked well with your sister, but right now, they might be too busy or dealing with more sophisticated clients. Your budget may be more or less than your family member’s, and the mortgage broker they used is not the right fit for you.

While we love referrals, our advice to you is to speak with a number of mortgage brokers before you get started with one. Read reviews, speak to previous clients and look at whether or not the broker has dealt with similar situations to yours in the past.

Consider their personality. You are going to be building a long-term relationship with your mortgage broker, so you want to make sure that they will guide you through the process. Being a first homeowner, you’re going to need a little bit of hand-holding. So you need a patient broker who will coach you through the process and give you tips and hints on the negotiation, as well as property reports. All this is critically important.

Just remember to go with a broker that will suit your style and individual situation, not your friend or family.

Bonus: Government Schemes you can qualify for as a first home buyer

Your home is likely the most expensive purchase you’ll make in your lifetime. However, this doesn’t mean it’s impossible to get a home. In fact, there have never been more government schemes and grants in place to help Australians purchase their first home than now…

Some schemes available to First homeowners include:

- The First Home Guarantee Scheme. This scheme supports eligible first homeowners to buy established or brand-new properties with the government’s support. You can put down as little as a 5% deposit. The First Home Guarantee scheme isn’t available to all lenders, so you do need to be careful here. This scheme is limited to 35 000 spots per Financial year on a first-come, first-serve basis.

- The First Home Super Saver Scheme. This allows you to make eligible voluntary contributions to your superannuation which can later be drawn as a deposit to help purchase your first home.

- The First Home Owners Grant. Under this scheme, eligible first homeowners can receive a once-off grant towards purchasing their first home. The size of the Grant and the eligibility vary from state to state.

Stamp Duty concessions. Stamp Duty is a tax imposed by state and territory governments on purchases or transfers of real estate. If you’re purchasing your first home, you can benefit from stamp Duty concessions for properties up to a certain price threshold. It does once again change from state and territory.

Read more: Grants to buy first home.

Bonus: 7 tips for buying a home

- Look at 100 properties. Many first-home buyers look at 2 or 3 properties and purchase the one they fall in love with and usually end up paying more than the market value. To be ready for an opportunity, you need to see 100 properties so you can make offers on 5 to 10, of which you might be successful in negotiating on 1 to buy.

- Have clear criteria. It’s all about reducing the number of variables at play. What are you looking for—a detached house, a townhouse or a unit? The best is to stick with the suburbs you’re looking at. We see the most success when people choose 1 or 2 suburbs to purchase in.

- Fact-check the real estate agent. Real estate agents are well trained and have experience negotiating with hundreds of sales. They know what to say and how to get you thinking that the property’s not going to be around for long. You need to be very careful about what you believe. If the agent says there’s another party interested and they’re about to make an offer, this doesn’t mean you need to rush to get in. It could be that they’re saying this to increase the urgency of your decision-making process.

- Keep emotions out. There’s no doubt about it; purchasing your first home is an emotional rollercoaster. Not only do you have the stress of trying to find the right home, but you have to deal with the frustration of missing out, especially if you find one you like. As hard as it might be, take the emotion out of the purchase, keep an even keel and gain perspective by talking to someone not involved in the transaction to give you a different perspective.

5. Talk to the neighbours. Can you imagine anything worse than buying your dream home and being stuck with neighbours from hell? It’s wise to scope out the area. You can’t exactly ask for a refund when you move in and find out you have next-door neighbours rave partying every night. It pays to chat with the neighbours. The more information you have, the better decisions you can make.

6. Mortgage on training wheels. The banks will throw money at you, and just because they say you can lend $500,000 doesn’t mean you should. This is where a mortgage with training wheels comes in handy. Work out what you’re comfortable repaying, not what the banks will lend you. Then practice your monthly repayments so you can gauge how far you’re stretching yourself and if you need to increase or decrease your initial commitment.

7. Don’t just negotiate on price. You can negotiate things like the red couch in the living room to be included in the sale. You can even choose to have a longer settlement date or negotiate the initial and balance deposits. Terms such as building and pest, finance and settlement can sometimes sway the negotiations in your favour.

Next steps and getting your home loan.

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please give us a call on 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again