This is a complete guide to comparison rates.

In this guide, you’ll learn the following:

- What a comparison rate is

- How to find the best comparison rate

- Dozens of comparison rate best practices

So, if you want to understand how comparison rates work and what the hype is all about, you’ll love this new guide.

We’ll give you research strategies and how to use comparison rates to your benefit.

Let’s dive in…

Table of Contents

What is a comparison rate?

A comparison rate is a way to represent the total cost of your loan.

According to ASIC, a comparison rate turns the cost of your loan fees, interest rates and other charges into a percentage. It is there to show the true cost of your loan and is used to compare different loans.

But what’s the catch?

The comparison rate doesn’t take into account payment terms, upfront fees, establishment fees and other associated costs.

So, in reality, it can miss out on a lot of extra costs.

What does a comparison rate cover?

There are a few key things that the comparison rate covers, including:

- The interest rate of the loan

- Some Fees

- Loan terms

- Loan amount

- Frequency of repayments

A comparison rate is a good way for borrowers to compare loans as it gives a nice estimate of all costs involved.

But remember that this is just one part of the loan and does not consider all the other features you might want from a loan. You should only choose a loan that aligns with your financial goals. For example, the comparison rate is not a very helpful tool if any of the below features are a priority to you:

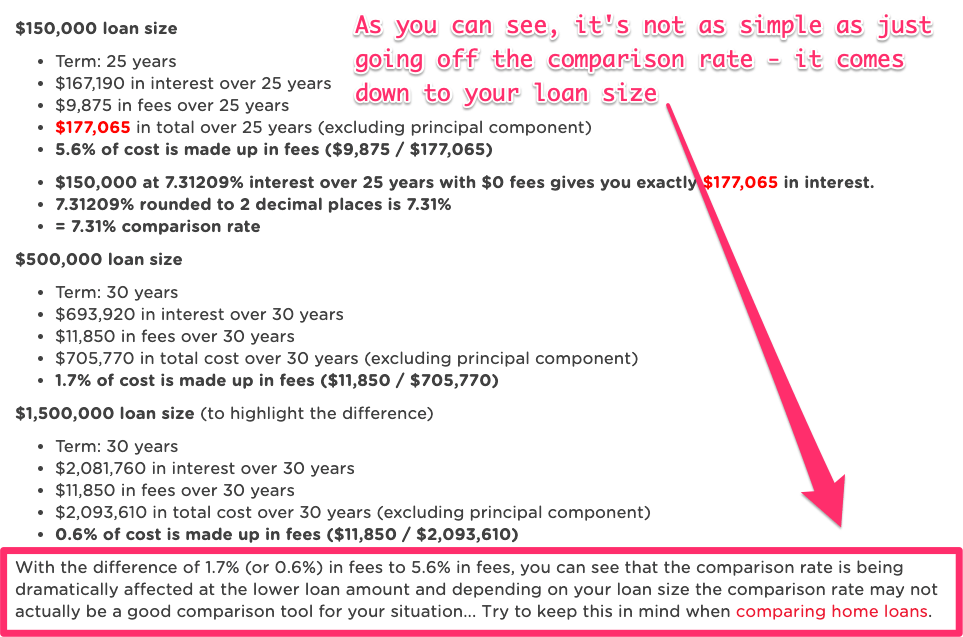

- Understanding the true costs of all loan amounts. All advertised comparison rates are based on a $150,000 loan over a 25-year loan term. If you are going to make extra repayments to your loan or are borrowing a higher amount, the Comparison Rate won’t be a true representation of the actual costs of your loan.

- Redraw facility. If a loan offers a redraw facility, you may choose it despite the higher comparison rate. Redraw facility provides you access to the extra cash you deposit in the home loan.

- Offset account. You may choose a loan despite the higher comparison rate if it has a linked offset account. An offset account is a transaction account that is connected to a mortgage account. It decreases the overall interest payments because the interest rate is applied to the net balance. The net balance equals a mortgage balance less the balance of the offset account.

- Opportunity to make extra repayments. There are some loan packages that allow you to make extra repayments. This offers flexibility and makes it easier for you to meet your financial obligations.

To get a more in-depth understanding of whether a better comparison rate has priority over these kinds of features, chat with our team of mortgage brokers. We will explain the comparison rate mechanism in detail, tell you the impact of this rate on the repayment terms of a loan and explain other features.

What is the difference between the comparison rate and the interest rate?

The difference between a comparison rate and an interest rate is unclear to most people.

But two keywords will help you differentiate between the two. These are True Cost.

An interest rate simply looks at the interest on the loan and nothing more.

The comparison rate is about figuring out the true cost of the loan. It compares loan fees and charges, terms and repayment frequency.

Many homebuyers are always surprised to hear that a lower interest rate doesn’t always mean it’s the best loan option.

This is where the comparison rate comes in. However, as we mentioned earlier, there are other factors you should consider, such as features that are beneficial to your personal circumstances. These can have more weight in decision-making.

How is the comparison rate calculated?

To understand a comparison rate entirely, you need to understand how it is calculated. Fortunately, figuring it out is easy.

A comparison rate can be calculated in three steps. In fact, no matter the loan size, the basic formula includes these three things:

- The loan amount – let’s say your loan is $500,000

- The loan term – the standard home loan term is 30 years

- Whether it’s principal and interest or an interest-only loan (for this example, let’s say P&I)

So for a Commonwealth Bank Extra Home Loan, the advertised comparison rate is based on a $150,000 loan over a 25-year term, so it’s not going to be accurate for your situation:

- 4 Year intro variable rate (First Home Buyer)

- Interest rate: 4.62%pa LVR 70% (accurate as of 16 December 2022)

- $0 establishment fee

- $0 monthly loan service fee

- Additional fees may apply

- The comparison rate is 4.63%.

Why isn't it applicable to my situation?

On the website, the comparison rate is calculated on a $150,000 loan, but you want a $500,000 loan.

So what you’re seeing is that a comparison rate of 4.63% isn’t an accurate example of your loan size.

In this case, if you’re looking for a higher loan, you’re essentially being misled by what the bank is showing you online.

Next, we need to see what the comparison rate is based on your actual loan size.

Let’s look at how the rate differs and how the fees affect the overall costs of your home loan for a higher loan.

How can the comparison rate be used?

In a few ways, actually.

If you’re applying for a loan, you’ll need to look at all the different variables and features on offer. But comparing loans with different time-frames, interest rates, and fees can be complicated.

This is where a comparison rate comes in and how you can use it.

So let’s take a look at an example:

Jill is trying to decide between two different loans. The first (Loan A) provides an interest rate of 5% with other charges of about 1%. The second (Loan B) has a 5.45% interest rate and 0.5% in other charges.

When we add the two percentages together, this creates a comparison rate.

So for Loan A, the comparison rate is 6% (5%+1%), and for Loan B, the comparison rate is 5.95% (5.45%+0.5%).

When we look at these two loans side by side, We can see that while Loan A provides a better interest rate, the overall cost of B works out a little lower.

So, in short, that’s how a comparison rate is used.

What comparison rate doesn't include

Just like many pieces of advice you will be given, a comparison rate is there only to guide you, not to be the final decision point.

Why?

Because comparison rates miss out on the finer details and every little extra cost.

- It leaves out things like break fees, redraw fees, late payment fees, and external charges, which can vary between loans.

- Comparison rates also miss government fees and other non-mandatory fees that may be imposed, like optional fees for redraw or offset accounts.

- Comparison rates shown are based on a $150,000 loan with a 25-year loan term. If your loan isn’t close to this, then the number you’re seeing isn’t an accurate reflection of your comparison rate.

To help you overcome these drawbacks, speak directly to your mortgage broker about how this will affect your loan.

Does the comparison rate make a big difference?

A comparison rate can simplify decision-making by revealing the hidden costs and showing a total number that can be used to compare between 2 loans. So, between two loans with the same interest rate, you can see the variable factors that set them apart.

No two loans are the same, and a comparison rate shines a light on the differences.

So, a comparison rate is a good starting point to help your decision-making process between two loans on offer.

Most common comparison rate mistakes

According to the Australian Bureau of Statistics, Australia has one of the highest levels of home ownership in the world.

This means that home loans are in hot demand!

As you know, setting up a home loan is about finding the best rate for you. If you don’t do your research properly and use a comparison rate to your advantage, you could be losing money each year on your loan.

So, here are some of the most common comparison rate mistakes and how to avoid them:

Mistake #1—Relying on a comparison rate ONLY to help you choose a loan

The main mistake we see buyers make before they speak to us directly is relying completely on the comparison rate to do all the work.

Remember that comparison rates are product-specific and do not include a particular loan’s features and other inclusions. This means offset accounts, redraw fees, credit cards, and insurance savings are not included in this number or comparison.

Mistake #2 — Thinking all rates are created equally

Comparison rates don’t look at different types of loans, which means that fixed-rate and variable-rate loans are dumped into the same category, together with the loan size.

So, the comparison rate you’re seeing is only for a $150,000 loan, not your specific loan size.

This is where problems can occur.

For example, fixed-rate loans can be misleading because it is assumed that once the fixed period is over, the rate continues as a standard variable rate.

But here’s the catch.

If you’re like most borrowers, once the fixed rate period is over, you will refinance. Refinancing saves you money because you can get the best available rate at the time.

…Usually, even lower than the regular one because the lender will offer you a deal.

Comparison rates can’t predict this.

Questions you need to ask about your comparison rate

Now that your processes are in check and you know the ins and outs of a comparison rate, it’s time to take things to the next level and ask some questions.

Why is the comparison rate important?

A comparison rate sets a benchmark for evaluation. It gets the numbers in line and helps strip back the details of a loan so you can see the difference between a few different loans, side by side.

But as we have said again and again throughout this guide, the comparison rate should not be the ONLY factor to consider when applying for a home loan.

How do lenders calculate comparison rates?

Double-check that your lender is looking at the following elements to create a formula for your comparison rate:

- Interest rate

- fees and charges

- loan term

- payment frequency

- loan amount

When you’re researching and comparing home loans to find the best deal for you, the comparison rate will help you figure out the true cost of the loan.

However, it shouldn’t be the only factor you consider.

Compare home loans accurately according to loan type, flexibility, features and inclusions.

This will help you narrow down the right loan types to suit your individual financial needs.

Read More: How to find the Best Home Loan in 2023

Next steps and getting your home loan…

Do you have any questions about the comparison rate? Or are you ready to buy a home?

Our team at Hunter Galloway is here to help you buy a home in Brisbane. Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please call us at 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again