A year to date calculator (or YTD Calculator) will help you work out your annualised salary from the income you have earned in a portion of the year. It is also known as an income annualisation calculator.

In other words, Year to Date (YTD) income represents what you should earn over the course of 12 months if your pay rate stays the same.

When banks or lenders are trying to work out your annual income, they will use a YTD calculator to work out your annual income. They will compare this to your group certificate or ATO Income Statement from the previous financial year.

In many cases, they will use the lower of the two figures. For example, if your annualised income from the YTD calculator is $120,000, but your group certificate or ATO Income Statement is only $100,000, they will be inclined to use the $100,000 figure when they are looking at your income and ability to pay off your loan.

Luckily, this isn’t always the case. We work with some lenders who will use the higher figure, especially if we are able to give them a compelling reason as to why they should accept the higher income figure. That’s one of the benefits of working with a mortgage broker rather than going directly to a bank or lender for your loan.

The higher your income, the more a bank is going to be comfortable lending you a higher loan amount. This has become even more important in recent times, as many lenders have put a cap on the debt-to-income ratio (DTI). Generally speaking, if your DTI is over 6 (for example, you are looking for a $650,000 loan with an income of $100,000), then you are considered a higher risk and the lenders may not approve your loan.

Table of Contents

YTD Calculator

How do I use the YTD calculator?

Using the Year to Date income calculator is fairly simple if you follow these steps:

Get a copy of your most recent payslip

Get a copy of your most recent payslip- Enter the date when you started your job. If you aren’t sure of the exact date just put the approximate month and year.

- Enter the end date from your most recent payslip. For example, if the pay period was 01/03/2019 to 31/03/2019 then you enter 31/03/2019 into the calculator.

- Enter the YTD gross income from your most recent payslip.

- Press calculate on the calculator to calculate your yearly gross income.

If you have any questions on the calculator please contact our team with an online enquiry, or give us a call on 1300 088 065.

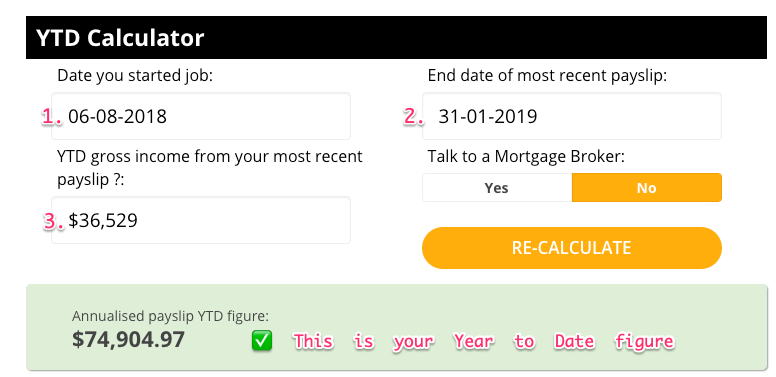

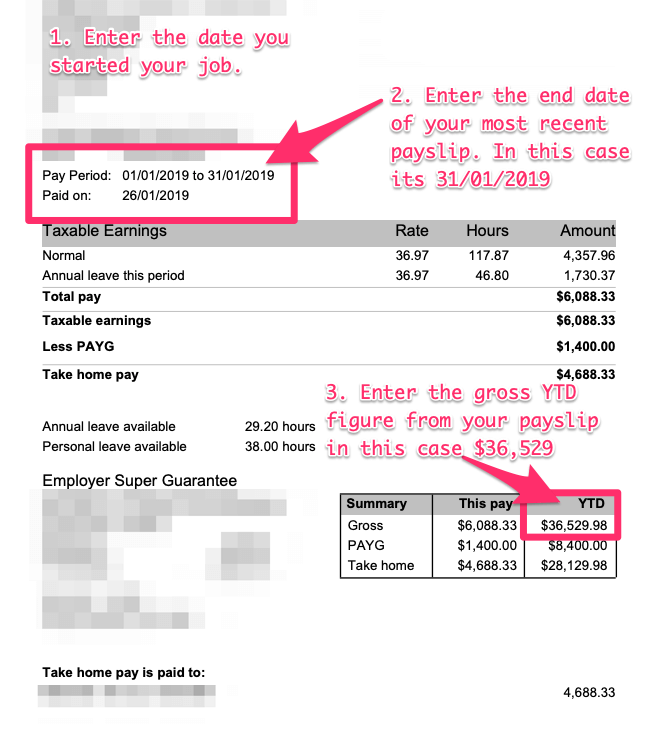

Here is an example of using the YTD calculator

We’ve also included a salary payslip to show you where the information comes in this example:

- 1. Enter the date when you started your job: 02/08/2018

- 2. Enter the end date from your most recent payslip: 31/01/2019

- 3. Enter the YTD gross income from your most recent payslip: $36,529

- 4. Press calculate on the calculator to calculate your yearly gross: $74,904.97 per year!

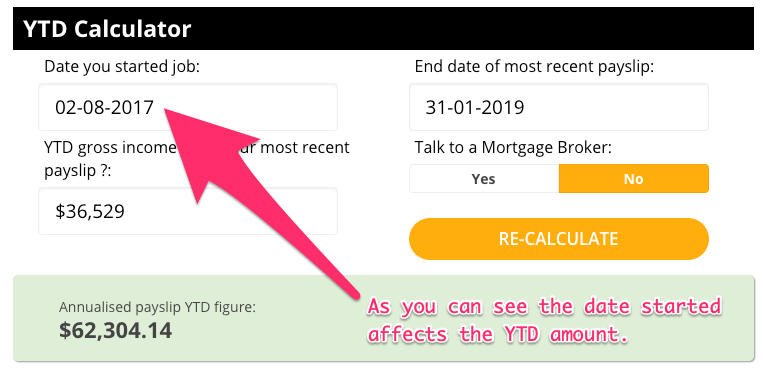

Why does it need to include the start date?

The year to date income is calculated by financial year, which in Australia begins on the 1st of July of each year.

Our calculator looks at the months you have worked in the current financial year and annualises this to get the yearly figure.

Why does it need to include the start date?

So if you have started after the beginning of the financial year (for example, if you started your job in August), the annualised figure will be lower than your true annualised income unless you include your start date.

How is YTD calculated from July to September?

Using the YTD calculator to determine your annual income is a little trickier in the first few months of the financial year. The new financial year begins on the 1st of July, and most payslips will have their YTD figure reset on this date.

So if you’re calculating your YTD income in July, August, or September, there isn’t much history to go on. A small amount of unpaid leave or a few days of overtime could dramatically increase or decrease your annualised income calculation.

In these months, some lenders will ask for your group certificate or ATO Annual Income Statement instead of using your YTD income. These documents will show a full 12 months of income or the date that you started with your new employer in the previous financial year. Either way, it allows the banks to get a more accurate idea of your annual income.

How to calculate YTD income on a new job?

If you have started a new job in the middle of a financial year you might have noticed your year to date income figure might look a little low. And that’s nothing to worry about – it’s the exact reason why we use a YTD calculator to calculate your annual income rather than just taking the number from your payslip.

For example, if you started a job on 1st February 2024, and you have a payslip dated 1 March 2024 with a year to date figure of $5,000, we’re not going to assume that you’ve only earned $5,000 for the entire financial year. Annualising this figure calculates your YTD income as $65,187.

If you have just recently started a new job, be aware that you may find it a little more difficult to get your home loan approved. Lenders typically do not like to lend to people who are still on their probation period, as they see it as a higher risk. However, we can help you to get a policy exception with some lenders which will give you some more flexibility in getting a loan.

How to calculate YTD income for a casual worker?

If you are employed on a casual basis, the YTD income is especially important. As a casual worker, your income could vary from week to week, depending on how many hours you’ve been rostered on and any overtime or other allowances. If they just looked at your last couple of payslips and annualised those figures, your estimated income could be much higher or lower than it actually is.

The YTD calc will annualise your income to understand how much you will be making in that year.

Keep in mind, if you are a casual worker most banks will need you to be in the job for at least 6 to 12 months, and some lenders are even stricter. Some lenders will only lend to casual workers if they can see the last two years’ group certificates. Others are more flexible. We work with several lenders who will accept casual employment even if you’ve only recently started your job.

If you’d like to know more, please call us on 1300 088 065 or fill in our free assessment form, and one of our mortgage brokers will give you a call to discuss your situation.

How to calculate YTD commission income?

Commission income, along with other types of supplemental income, are usually treated differently than your base income. They will still usually accept this as part of your income when they are assessing your application, especially if you have at least a 1-2 year history of receiving commission.

Most banks will let you use all of your commission income towards your loan application if you have a 20% deposit. If you have less than a 20% deposit, they may accept a lower amount of commission (sometimes as low as 50%).

However, other lenders are a bit more flexible and we work with several lenders who will accept a higher amount of your commission income. If you’d like to know more, get in touch with our mortgage brokers on 1300 088 065 or fill in our free assessment form.

Bonus: Tips for getting a loan when you have a unique income

When it comes to getting a home loan, every case is unique. Here are some types of unique income and how you can get a home loan if you have these types of income.

- Maternity leave. Many banks may decline the loan because a lot of people that go on maternity leave may not even come back to work. However, if you provide a return to work letter from your employer, some banks can consider your return to work income. Keep in mind that if you return to work, the lenders require you to do it within 12 months and return to the same role, not a different one.

- Casually employed. Since casual work is not always guaranteed, most lenders will need you to be in the role for 6 months. There are one or two lenders that can think outside the box. For example, suppose you are an IT contractor or you’re in the film and television industry, where the nature of the industry requires you to move from contract to contract. In that case, some banks will actually consider one day in a role providing it makes sense. So keep that in mind. If you’re casually employed, there isn’t always a hard no if you’re less than six months in the role.

- Recently self-employed. In most cases, lenders will want you to have 2 years’ tax returns, which can be very hard, especially if you have just started your business. There are some lenders who can consider 1 year’s financials provided you have 18 months of ABN history. The good news is there are others that will waive it completely. In most cases, they require a 20% deposit, but it’s on a case-by-case basis.

- On a probationary period. Most providers and lenders will want you to pass your probation period, which is typically 6 months in Australia but can be 3 months in some cases. If you are doing a really good job, you can ask your employer to pass your probation early. If your employer says no, then a few lenders will look at other things like do you have 2 years of employment history in the same industry. There are even some lenders who will grant your application even if you are on probation. It’s just a matter of talking to the right mortgage broker.

- Working in multiple jobs. The first thing lenders will want to consider is whether or not it’s sustainable. So, for example, if you are working 40 hours at job 1 and 40 hours at job 2, most lenders will say it is not sustainable because you will eventually burn out. In this case, they will consider only a portion of your income. In addition, the banks will want to see that you have been in both roles for a minimum of 12 months.

In conclusion, having a unique income should not disqualify you from getting a home loan. There are so many lenders with so many different policies, and a no from one lender isn’t a no from all of them. The right mortgage broker will be able to find a solution for you.

How will a bank look at my income?

Do you realise that only a handful of banks will use 100% of your extra income like overtime, shift allowances, bonuses, casual income and maternity leave income?

Our team at Hunter Galloway can help you gain a detailed understanding of YTD income and will help you find the right lender.

Chat with us now on 1300 088 065 or get in touch with our team for a free assessment.

Ready to take the next step toward buying? We’re happy to help. Click on the button below to complete a Free Assessment and we’ll be in touch to assist you with the next steps on your path towards home ownership.

Start again

Start again