Are you a lawyer dreaming of owning a home but don’t know where to start? Look no further! Our complete guide to home loans for lawyers in 2024 has got you covered. We’ll show you what benefits lawyers get, LMI waivers, and so much more!

Let’s get started.

Table of Contents

Chapter 1: Lawyer home loan basics

If you’re a lawyer looking to purchase a home, it’s important to understand the basics of lawyer home loans. These specialised loans are designed to meet the unique financial needs of legal professionals and can offer a range of benefits that traditional home loans may not.

In this chapter, we’ll cover the basics of home loans for lawyers, including minimum income requirements and how much you’ll save with waived LMI.

First, you’ll see the minimum income requirements. Then, we’ll show you how much you’ll save with waived LMI.

Why do legal professionals get special discounts?

Legal professions get special discounts because they are considered to be low risk. Banks have spent time analyzing all their borrowers over the years and they realised that lawyers are in a similar category to doctors and other professions like Accountants – they have a lower probability of default.

What benefits do lawyers get?

As a lawyer, you will likely be eligible for discounts when it comes to lending.

Why? Because lawyers are considered to be low-risk borrowers by lenders. This is because banks view lawyers as having stable and secure employment and secure income. Lawyers often have high earning potential, making them attractive candidates for lenders.

Since the banks view lawyers favourably, you’ll be able to qualify for discounts on your home loan.

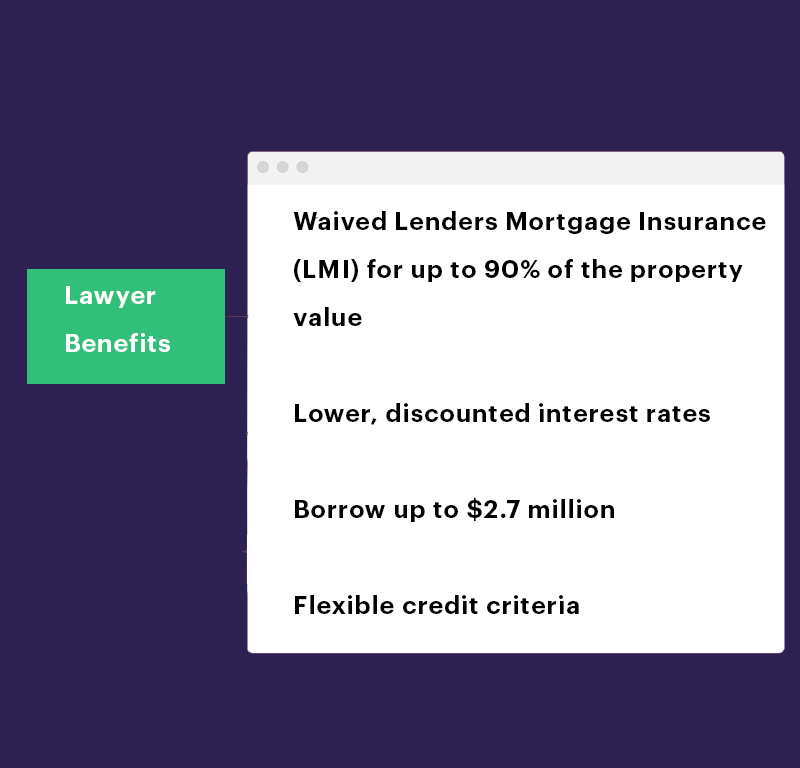

You may be eligible for the following discounts:

- Waived Lenders Mortgage Insurance (LMI) for up to 90% of the property value

- Lower, discounted interest rates

- Flexible credit criteria

Are there any maximum loan amounts for a single property?

Is there an amount you need to be aware of if you are looking at the upper echelons of the property market and even maximum exposures if you have a big portfolio? The short answer is yes.

If you’re buying a big house in Sydney, there are maximum exposures depending on the bank, usually between 5 and 7 million dollars. If you’re buying a 10 million property, you are not likely to be eligible for any discounts, so you will probably need more than a 10% deposit.

But most people are generally buying property for under a million dollars, so you should be fine. The issue only comes if you want to buy multiple investment properties, and that’s where we see a lot of lawyers who’ve got big portfolios that are split across different banks.

What is the minimum income required?

The income requirements vary depending on the state you live in and the bank you are applying through. Only certain professions qualify for these benefits.

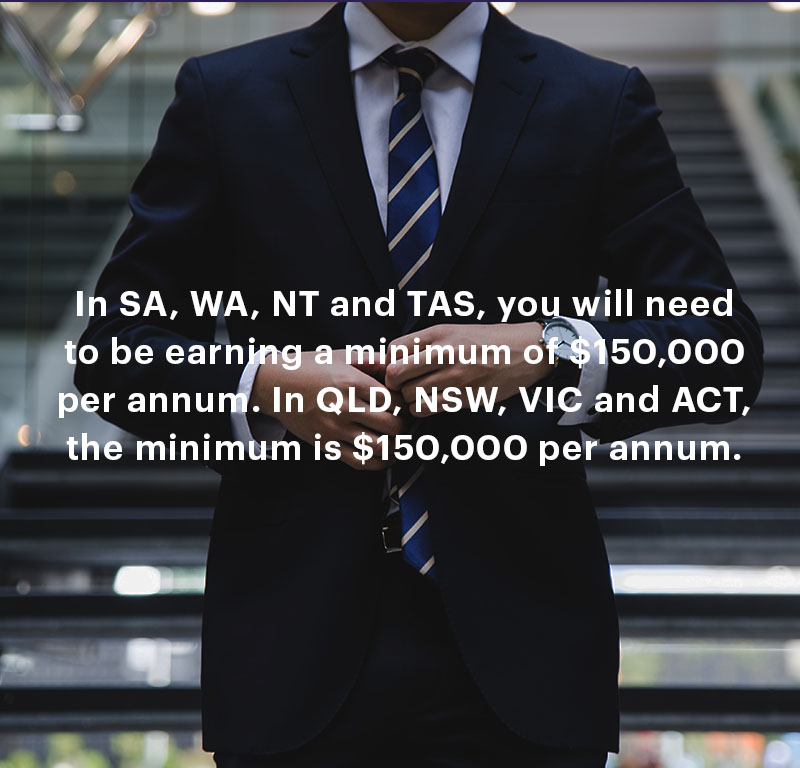

- With certain banks in SA, WA, NT and TAS, you will need to be earning a minimum of $150,000 per annum. In QLD, NSW, VIC and ACT, the minimum is $150,000 per annum.

- Your income can include rental income. You’ll need to provide evidence of your rental income, such as bank statements showing rental payments from your tenants. Banks will also account for any expenses associated with your rental property, such as maintenance or property management costs.

- If you are married or in a de facto relationship, the banks will assess only your income. They will not group it with your spouse’s pay unless they are also in the legal industry and qualify.

BUT the minimum income requirement is for only a few banks.

Other banks do not have a minimum income requirement; you just need to show your practising certificate.

Speak to our team today about your situation to confirm if you qualify to have a no LMI loan on 1300 088 065 or contact us here.

Case Study: A lawyer and a retail worker

Judy and Jim have been married for 2 years. Judy is a lawyer, and Jim works at Rebel Sport.

Judy qualifies for mortgage discounts but doesn’t earn enough on her own, as her income is $120,000 per year. Jim earns$55,000 per annum. Together, their combined income is $175,000 yearly.

Some lenders will only look at Judy’s income and say she does not qualify. But with the help of a mortgage broker, they can find a bank that will assess their combined income. In this case, they will qualify as high-income earners and for waived LMI.

As we mentioned above, In some cases, specific lenders will have different income requirements.

Speak to our team today about your situation on 1300 088 065 or contact us here.

How much will I save with no LMI?

For a regular home loan, if you borrow over 80% of the property value, you will be charged a fee for Lenders Mortgage Insurance. If you default, this money goes to the lender as security on the mortgage. LMI can be expensive, ranging from about $5,000 to $24,000+ on top of your home loan.

LMI reduces the overall return on investment and cannot be refunded. So paying no LMI on your loan could save you a fair bit of money.

Some of the benefits of having no LMI include:

Some benefits of not paying Lenders Mortgage Insurance when getting a home loan include:

- Lowering your overall mortgage costs

- Reducing your monthly mortgage payments

- Building equity in your home faster

- Having more disposable income to put towards other expenses or investments

- Being more financially secure in the long term.

Case Study: Gina, the Lawyer in Queensland

Gina is a lawyer based in Queensland and is earning $165,000 per annum. She wants to buy a house for $750,000 and currently has a 10% deposit of $75,000.

In a regular loan application, Gina would have to pay Lenders Mortgage Insurance as she doesn’t have a 20% deposit. However, as Gina fits the lawyer criteria, LMI will be waived.

Let’s take a look at the discount and savings she will receive for a 90% loan-to-value ratio loan.

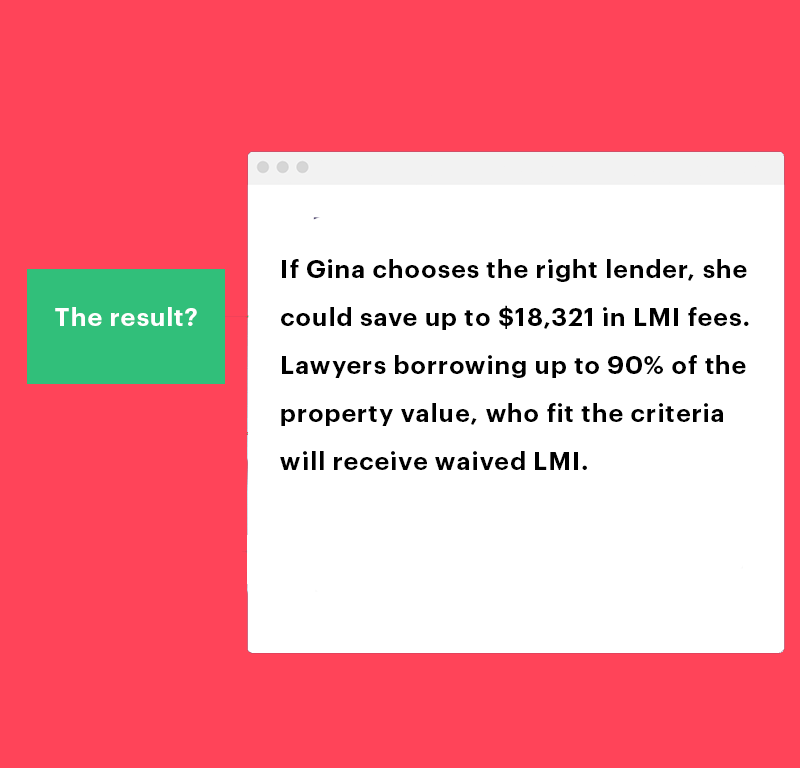

- Gina could save up to $18,321 in LMI fees if she chooses the right lender.

- Lawyers borrowing up to 90% of the property value who fit the criteria will receive waived LMI.

What kind of interest rate discounts will I receive as a lawyer?

Along with waived LMI, lawyers will also be eligible for discounts on interest rates. The discounts will vary according to the industry association, your income and the total loan.

Be sure to look around and compare different lenders and their loan products to find the right deal. Working with a home loan expert, such as a mortgage broker, can be helpful in finding the best deal that meets your specific needs and circumstances.

Chapter 2: How do I qualify for mortgage discounts as a lawyer?

As a lawyer, you may be eligible for various mortgage discounts. It is crucial to understand the eligibility criteria for these discounts so you can save money on your mortgage.

In this chapter, we will show you how to qualify for home loan discounts as a lawyer.

We’ll go through different industry associations, as well as the difference between government-hired and private lawyers.

Let’s take a look.

Do I need to be a part of an industry association?

The good news is only some lenders require membership evidence. To qualify for waived LMI home loans with these lenders, you will have to be a part of one of the following industry associations:

- Law Council of Australia

- Law Society of NSW

- Law Society of South Australia

- Queensland Law Society

- The Australian Bar Association

- Law Institute of Victoria

- Australian Labour Law Association

- Australian Corporate Lawyers Association

- The Commercial Law Association of Australia

- Australian Insurance Law Association

Individual industry bodies will be accepted on a case-by-case basis. Some lenders require no evidence of association membership but will require a qualification/degree or proof that you are still practising law.

What are eligible occupations as a lawyer to receive home loan benefits?

To receive home loan benefits, you will need to be working as a barrister, lawyer, solicitor or partner. Variations around these job titles are accepted. For example, if your job title is listed as ‘Associate’ or ‘Legal Counsel’, you can be eligible to receive home loan benefits.

You will need to show acceptable evidence, including:

- Receipt for payment of annual membership.

- Current valid membership card.

- Written confirmation from the listed association.

- Practising Certificate.

What about judges and magistrates?

If you are a judge, you must meet the same income requirements as a lawyer. You must also have evidence to show that part of your employment conditions means you are prohibited from holding a Practising Certificate.

Is there a difference between benefits for government hired and private lawyers?

Lawyers that work for the federal or state government will receive the same benefits as private or self-employed lawyers. Some banks require a practising certificate to qualify for home loan discounts. However, some government agencies do not require you to have a practising certificate. As long as you’re working in a legal position in a government agency but you don’t have one at the moment, we can help you get that passed.

So don’t worry if you are working for a government agency and it’s not required to have a practising certificate because many times, we have had clients in the same circumstances, and we have still managed to get the mortgage insurance waived.

Speak to us as you may still be eligible for home loan interest rate discounts.

Chapter 3: Home loans for Lawyers – the fine print

Now it’s time to dive into the fine print.

Specifically, we will look at the details for lawyers to ensure you fit the lending criteria.

We will also go through a few lenders that provide home loan discounts for lawyers.

Let’s get started.

Buying a property with your spouse

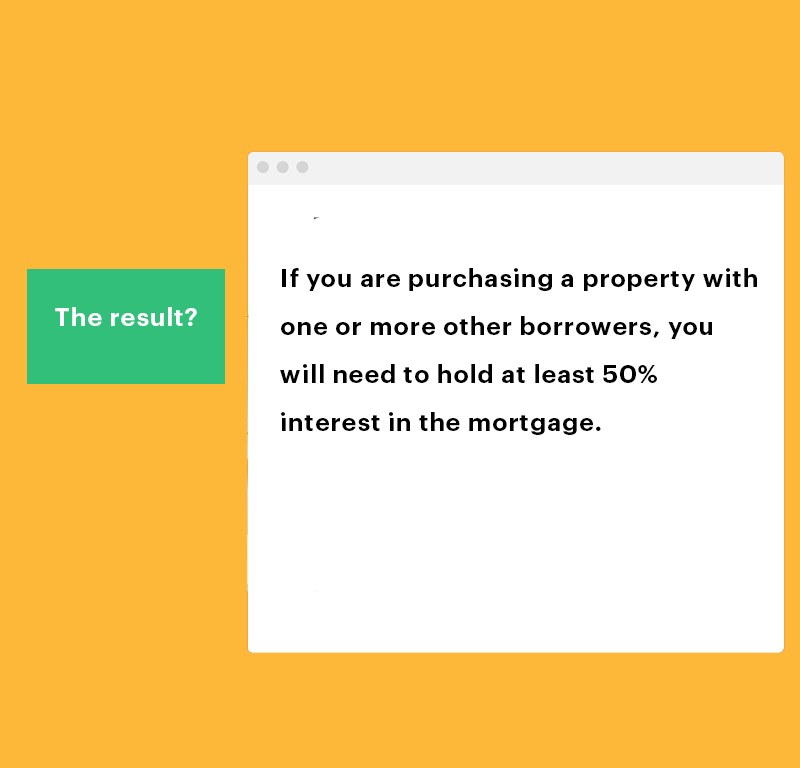

If you are purchasing a property with one or more other borrowers, you must hold at least 50% interest in the mortgage. For example, if you are a lawyer and buying a house with your spouse, who is a teacher, you should have 50% or more ownership interest in the loan. Your spouse or partner cannot own 60% of the loan.

What if my spouse's name is on the title and mine isn't?

We see many cases where lawyers try to protect their assets so they’ll purchase a property with their spouse, but the property will be in their spouse’s name only, even though both of them are on the loan.

Generally, the banks have strict rules about what they call co-borrowing. So if you and your partner are borrowing together and are on the loan, but you are not going to live in it, then the bank is not going to give you a loan in that case because you are not getting a benefit from the house. But if both of you will live in the house even though your name is not on the title, then the bank’s okay with that because they understand that, as a lawyer, you want to protect yourself from being sued.

When buying with your spouse, keep in mind that lenders are not going to consider your spouse’s income (if they are not a lawyer) to meet their income requirements.

Can permanent residents apply for these discounts?

If you’re a permanent resident, are you eligible for these mortgage insurance waivers as a lawyer? Yes, it depends on the permanent residency type, but generally speaking, permanent residents and Australian citizens are treated the same across the lenders. So as long as you’re working and living in Australia, you’re earning Australian dollars, and you’re a member of those Australian-based law societies, you would be eligible for these waivers.

Which lenders offer mortgage discounts for lawyers?

As always, different lenders offer different discounts.

Lenders like CBA, ANZ Westpac, St. George and Bank of Melbourne provide excellent deals for lawyers. However, in many cases, you will need to seek out the benefits from lenders directly, as they are not always openly advertised.

This is where a mortgage broker can help you negotiate the best home loan for you.

We can get the banks to compete with each other to find you the best deal overall!

Bonus: How to choose the right home loan for you

Choose a loan term.

Generally, the default loan term in Australia is 30 years, but you can choose a loan term of 10,20 or even 35 years. If you choose a shorter loan term, your repayments will be higher, but you will finish paying off your loan faster. But you will pay more interest if you choose the 35-year loan term.

For example, if you had a $500 000 loan paying 5.5% interest over 30 years, you’d pay $520 000, compared to $620,000 if you had a 35-year loan term. If you are having difficulties with borrowing capacity, you may elect to go for a 35-year loan, but we recommend making your repayments as if you were on a 30-year loan. That way, you pay off your loan faster, but you still have the 35-year loan term as an option.

Select Offset or Redraw facility.

An offset account is just a normal day-to-day transaction account that’s invisibly linked to your home loan. If you have an offset account, you could have, say, $1,000 in that offset account and that $1,000 will reduce your loan balance and save you interest.

Redraw, on the other hand, is a feature that allows you to make extra payments to your loan and transfer it back out so you can have that hundred dollars in your everyday offset account. You have to actually physically transfer that into your home loan account.

When choosing between an offset account and redraw facility, know that in most cases, the offset will cost you money from a $10 account-keeping fee to an annual package fee of up to $395. But if you want to turn your property into an investment later, the offset will help you maximise your tax deductions—have a chat with your accountant or mortgage broker about this.

Interest only or principal and interest repayments.

On a principal and interest loan, you are paying down the original loan that you took as well as the interest. So typically, on a principal and interest loan, you are progressively paying down this loan balance from $500 000 to zero dollars over a 30-year period.

Now with an interest-only loan, you aren’t paying any of that principle down, so your monthly repayments are much less, but the downside is you pay much more interest over the life of the loan. The banks also see it this way, and their preference, by and large, is to look at principal and interest repayments.

Introductory rate (aka honeymoon rate).

These are really great because you get a high discount for the first couple of years, and then the discount disappears, reverting to a higher variable rate subsequently. So you might get a 2% discount for the first 2 years, and then it drops back to a 1% discount. The biggest Allure is that for the first two years, you think all the repayments are really cheap, so you can get ahead of your home loan and start paying it off.

However, after year 3, you could be stuck paying a much higher interest rate for the next 27 years of your home loan if you can’t refinance. You might have to pay lenders mortgage insurance again, your job situation might have changed, you might have kids, you might not be earning as much, and you are stuck paying much more for this loan.

Next steps and getting your home loan

Our team at Hunter Galloway is here to help you buy a home in Australia. Unlike other mortgage brokers who are just one-person operations, we have an entire team of experts dedicated to helping make your home loan journey as simple as possible.

If you want to get started, please call us on 1300 088 065 or book a free assessment online to see how we can help.

Start again

Start again